NEWS

5 Aug 2026 - 2026 mid-year update & outlook

4 Aug 2026 - Income & Credit Peer Group Review

4 Aug 2026 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

||||||||||||||||||||||

| FarmCap Private Credit Agricultural Mortgage Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

|

||||||||||||||||||||||

| Rixon Credit Opportunities Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

|

||||||||||||||||||||||

| Princeton Property Income Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

Want to see more funds? |

||||||||||||||||||||||

|

Subscribe for full access to these funds and over 1000 others |

3 Aug 2026 - Global Equity Peer Group Review

3 Aug 2026 - Manager Insights | FarmCap

|

Chris Gosselin, CEO of FundMonitors.com, spoke with Jonathan Weinstock, Founder and Managing Director at FarmCap. They discussed FarmCap's private lending to Australian farmers, its conservative farmland-backed approach, and its focus on short-term funding. Jonathan also explained how the fund supported purchases, refinancing and working-capital needs while targeting strong investor returns.

|

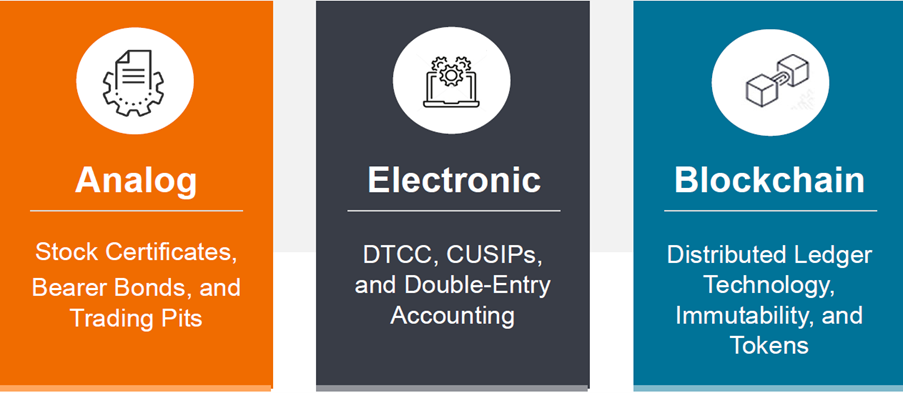

31 Jul 2026 - Tokenisation: Why blockchain rails could redefine the future of finance

|

Tokenisation: Why blockchain rails could redefine the future of finance Janus Henderson Investors July 2026 (9-minute read) Tokenisation: Closer to an inflection point than many investors realise Of the two technology trends reshaping asset management today - artificial intelligence (AI) and blockchain - AI has attracted far more attention. That is understandable. AI is already transforming how firms analyse data, automate workflows and improve productivity. Yet blockchain may ultimately prove the more significant development for financial markets because it changes the infrastructure on which finance operates. Tokenisation is one of the clearest examples of that transformation. In simple terms, tokenisation involves representing ownership of a financial asset on a blockchain. However, the key question is not whether a stock, bond, fund or sovereign bond exposure can be tokenised. It is whether the tokenised version delivers a better outcome for investors. The investment case for tokenisation is increasingly understood. What is now emerging is the operating case. As investors begin to recognise tangible benefits - including faster settlement, improved collateral management and lower administrative friction - adoption could accelerate more rapidly than many expect. Lessons from the ETF market The evolution of exchange-traded funds (ETFs) provides a useful comparison. ETFs did not become mainstream overnight. Their adoption occurred in stages. Initially, the appeal was largely structural: investors could access diversified market exposure efficiently and at lower cost. Over time, attention shifted to practical advantages such as intraday liquidity, transparency, operational simplicity and, in some jurisdictions, tax efficiency. These benefits gradually changed investor behaviour. Eventually, the ETF wrapper itself became part of the attraction. ETFs evolved from niche products into a standard investment vehicle used across both passive and active strategies. Tokenisation may follow a similar trajectory. Today, most investors understand the concept, but many have yet to experience its operational benefits directly. Adoption is likely to accelerate when tokenised products offer capabilities that improve the investment experience, such as:

As with many financial innovations, progress often appears gradual until a critical mass is reached. What needs to happen next? Three conditions are particularly important if tokenisation is to reach a meaningful tipping point. First, the industry must overcome the cold-start problem. Issuers are reluctant to tokenise assets without investor demand, while investors are hesitant to commit capital without sufficient product availability. Both sides must develop together. Institutional participation has increased over recent years, but adoption remains uneven. Second, liquidity must deepen. While tokenised assets can theoretically trade around the clock, much of the investor base continues to operate off-chain. As a result, many tokenised products remain relatively isolated. Building bridges between traditional and blockchain-based markets remains one of the industry's key challenges. Third, utility must improve. Institutional investors will adopt tokenised products when they provide capabilities that traditional structures cannot easily match. These may include the ability to utilise new protocols, programmable settlement, faster redemptions, efficient collateral deployment and streamlined product design. Ease of use is equally important. Most investors do not need to understand how ETF creation and redemption works to benefit from ETFs. Tokenisation is likely to follow the same path, with blockchain becoming largely invisible to end users. A useful analogy is the smartphone. Many of the underlying technologies--touchscreens, mobile connectivity, and internet infrastructure--existed well before smartphones achieved mass adoption. The key shift was that smartphones effectively turned the internet into a mobile experience, placing it in users' pockets and unlocking entirely new use cases. This, in turn, enabled an ecosystem large enough to make the technology indispensable. Blockchain appears to be moving in a similar direction. Utility, not technology, will drive adoption The most important test for any tokenised product is simple: Does it offer something materially better than the traditional alternative? The same principle applies to distribution. One of the most exciting aspects of tokenisation is its potential to broaden access to investment products and connect managers with new types of investors through more efficient channels. However, simply placing an existing fund on a blockchain is unlikely to drive meaningful adoption among non-crypto-native investors. Distribution alone is not enough. Investors will only embrace tokenised structures if they deliver clear advantages over traditional vehicles, whether through faster settlement, greater liquidity, protocol interoperability, improved collateral utility, enhanced transparency or a meaningfully better ownership experience. If a tokenised fund merely provides the same exposure through a different distribution channel, its appeal may be limited. The real value emerges when tokenisation changes how an asset can be used. This is where tokenisation becomes more than a digital wrapper. A tokenised Treasury exposure that can be mobilised as collateral is fundamentally different from a traditional yield-generating instrument. Similarly, tokenised credit structures with programmable cash flows may enhance transparency and operational efficiency. Ultimately, institutional adoption will be driven by utility and protocol interoperability rather than technology alone. Where adoption is already visible Despite occasional hype, meaningful progress is already taking place across several areas of financial markets. The first major wave of blockchain adoption was stablecoins, which have become increasingly important for on-chain payments, settlement and treasury management. The second wave is tokenised yield. Tokenised cash-management products and Treasury exposures are attracting investors seeking access to real-world yield while remaining within blockchain-based ecosystems. Tokenised credit is also moving beyond theory. Private credit, securitised products and collateralised loan obligations are gradually appearing on-chain. While still early in development, these structures have the potential to improve transparency, administration and cash-flow management. Other areas, including tokenised real estate and public equities, continue to attract attention but have yet to achieve significant institutional scale. The broader direction appears increasingly clear: stablecoins came first, tokenised yield followed, and the next stage may involve fully tokenised asset-management structures becoming a standard option alongside traditional investment vehicles. Exhibit 1: The entire global financial system will eventually operate on-chain

Source: Janus Henderson Investors Liquidity remains tokenisation's most significant obstacle While blockchain technology can improve settlement efficiency, it cannot create liquidity on its own. Liquidity develops through sustained participation, capital flows and market confidence. Many tokenised assets remain fragmented because large parts of the investor base continue to operate within traditional financial infrastructure. Without a sufficiently deep ecosystem of buyers, sellers and market makers, individual products risk becoming isolated. This matters because liquidity underpins institutional confidence. Investors need certainty that assets can be transferred, redeemed and deployed reliably if they are to function effectively as collateral, working capital or settlement instruments. Mechanisms such as instant redemption facilities can help address this challenge by making tokenised assets more practical and usable within broader financial markets. What institutional investors should focus on For allocators, the key question is not whether tokenisation appears innovative but whether it solves a genuine operating problem. Five factors deserve particular attention:

The most likely outcome is not a separate blockchain-based financial system, but gradual convergence between traditional and on-chain infrastructure. The cost of waiting Many institutions focus on the risks of adopting tokenisation too early. Those risks are real and include operational, regulatory, technological and reputational considerations. However, there is also a risk in waiting too long. Investor preferences can change more quickly than institutions can build new capabilities. By the time the benefits become obvious, firms that have already developed expertise, partnerships and infrastructure may hold a meaningful competitive advantage. A pragmatic approach is therefore to identify areas where tokenisation can improve client outcomes, operate them alongside existing business lines and build capabilities incrementally. Tokenisation should be viewed less as a technology experiment and more as a long-term infrastructure investment. Blockchain as the future operating layer of finance Financial markets are unlikely to move entirely on-chain anytime soon. Traditional funds, ETFs, separately managed accounts and tokenised vehicles will coexist for many years as regulation, infrastructure and investor behaviour evolve. Nevertheless, the direction of travel is towards a financial system that is more programmable, transparent and operationally efficient. That is why blockchain may ultimately become a foundational operating layer for finance. Tokenisation is not the whole story, but it is one of the most visible early manifestations of that broader transition. For active managers, investment skill remains essential. Research, portfolio construction, risk management and stewardship do not disappear. What changes is the infrastructure through which those capabilities are delivered.

Conclusion: The wrapper is not the revolution - the rails are Tokenisation is often discussed as a product innovation, but it is better understood as infrastructure innovation. The opportunity is not simply to create digital versions of existing funds. It is to create investment products that are faster to settle, easier to use as collateral, more transparent to administer and more flexible in how they interact with the wider financial system. The ETF market provides a useful precedent. ETFs succeeded because they changed what investors could do, not merely because they offered a new wrapper. Tokenisation will follow a similar path only if it delivers meaningful operational advantages. The industry remains early in its development. Liquidity is still fragmented, regulation continues to evolve and distribution channels are adapting. Yet the long-term direction appears increasingly difficult to ignore. AI may transform how financial firms work. Blockchain may transform the infrastructure on which finance itself operates. Firms that build credible capabilities before that shift becomes obvious may be best positioned to serve clients in the next phase of financial markets. |

|

Funds operated by this manager: Janus Henderson Australian Fixed Interest Fund , Janus Henderson Conservative Fixed Interest Fund , Janus Henderson Diversified Credit Fund , Janus Henderson Global Natural Resources Fund , Janus Henderson Tactical Income Fund , Janus Henderson Australian Fixed Interest Fund - Institutional , Janus Henderson Conservative Fixed Interest Fund - Institutional , Janus Henderson Cash Fund - Institutional , Janus Henderson Global Multi-Strategy Fund , Janus Henderson Global Sustainable Equity Fund , Janus Henderson Sustainable Credit Fund All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect. The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested. Whilst Janus Henderson believe that the information is correct at the date of publication, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson to any end users for any action taken on the basis of this information. |

30 Jul 2026 - Why even the world's best players need a team

|

Why even the world's best players need a team abrdn July 2026 (3-minute read) Throughout football history, the biggest moments have often belonged to the biggest players. From Pelé and Maradona to Lionel Messi and Harry Kane, individual brilliance has the power to turn a game in a flash. Yet even the greatest stars don't succeed alone. Behind every match-winning moment stands a team providing defence, bringing balance and creating opportunities. Investing is no different. Every portfolio needs its difference-makers Of course, they're stars for a reason - and it would be remiss if we didn't talk about them. Indeed, in recent years, a relatively small group of companies - including the so-called Mag 7 - has been responsible for a large share of global equity market returns. It's not hard to see why. These businesses have become synonymous with some of the most powerful trends shaping the global economy. Artificial intelligence continues to drive demand for computing power and semiconductors. Electrification is increasing the market for critical minerals and energy infrastructure. Digital connectivity has become essential to almost every aspect of modern life. For many investors, these are the companies capturing the imagination and generating the returns. The players who make the team tick But that's not why we're here. Let's shine a light on the rest of the team - the players providing stability at the back, controlling the midfield and doing the hard yards that often go unnoticed. Every good portfolio needs those kinds of operators. Credit investments, for example, can offer a source of income and may help dampen volatility during periods of uncertainty. While they rarely generate the same excitement as high-growth equities, they often play an important role in balancing risk within a portfolio. Real estate brings exposure to the physical economy. From logistics warehouses supporting e-commerce to data centres powering the digital world, it offers access to assets that many of us rely on every day. Investors are also attracted to the potential for income and inflation protection alongside the prospect of capital appreciation. Emerging markets bring a different dynamic. Faster-growing economies, evolving consumer bases and expanding middle classes can provide access to themes that may be less prevalent in developed markets. Think of a bank expanding financial access across North Africa, or an energy firm that distributes electricity safely and efficiently to rural communities in Guatemala. These are the little-known companies that could become giants of the future, while offering return potential today. Private markets have also become increasingly important for investors seeking diversification. Whether through infrastructure projects, lending directly to businesses or investing in companies before they reach public markets, they can provide access to opportunities beyond traditional stock exchanges. They can also provide sources of return that are less correlated with public markets and, for many investors, have become a core part of portfolio construction. Bringing it all together Even the most talented football squad requires organisation. Decisions made on the touchline matter. For investors, the task isn't simply identifying attractive investments but constructing a portfolio where those different elements can work together. This is why diversification has remained one of investing's most enduring principles - providing resilient performance where it's needed. By spreading exposure across different asset classes, sectors and geographies, investors can reduce reliance on any single outcome. The objective isn't to remove risk altogether - that's impossible - but to avoid concentrating it in one place. Multi-asset investing takes this philosophy a step further by bringing together a range of investment opportunities within a single portfolio. Equities can provide growth. Credit can provide income. Real assets can provide diversification. Alternative investments can introduce additional sources of return. Each plays a different role within the portfolio. Final thoughts... Football's biggest players will always grab the headlines. But those moments are rarely created in isolation. They're built on the discipline, tactics and contributions of players across the pitch. High-growth opportunities, transformative technologies and market-leading companies can play an important role in driving portfolio returns. But long-term success is rarely built on a single idea. More often, it comes from combining different strengths, balancing different risks and ensuring every part of the portfolio has a role to play. So, stars matter. But in the end, it's the team that delivers lasting success. |

|

Funds operated by this manager: abrdn Sustainable Asian Opportunities Fund , abrdn Emerging Markets Equity Fund , abrdn Sustainable International Equities Fund , abrdn Global Corporate Bond Fund (Class A) |

28 Jul 2026 - Glenmore Asset Management - Market Commentary

|

Market Commentary - June Glenmore Asset Management July 2026 (2-minute read) Global equity markets were again volatile in June, highlighted by a sharp intra-month reversal in the tech sector, the reopening of the Strait of Hormuz and the launch of the largest IPO in history - SpaceX. Despite a strong start to the month, the S&P 500 and NASDAQ finished -1.1% and -0.2% lower, respectively. Returns were weighed down by disappointing updates from some major tech companies (Broadcom, Adobe, Oracle) and a more hawkish than expected speech from Kevin Warsh, during his first meeting as the new chairman of the US Federal Reserve. International markets outperformed their US peers, with the Euro Stoxx 50 and FTSE 100 rising +4.6% and +0.8% during the month, respectively. As noted earlier, the debut of SpaceX garnered much attention. The company raised US$75b, almost 3x larger than the prior record held by Saudi Aramco and made Elon Musk the world's first trillionaire. After rocketing higher during its first few days, SpaceX finished the month +27% higher. Domestic markets also outperformed the US, with the ASX All Ords Acc Index rising +0.4%. Sector returns were sharply divergent. Energy was the largest underperformer, declining - 9.0%, as the crude oil price fell ~20% following the Iran ceasefire deal. On the flip side, Consumer Staples (+12.3%), Consumer Discretionary (+12.1%), and Real Estate (+1.8%) outperformed, with the RBA's decision to hold rates providing some support to rate-sensitive sectors. Small caps underperformed vs large caps, with the ASX Small Ords Acc index falling -2.0%. In bond markets, the US 10-year bond yield rose +3 basis points (bp) to 4.47%, whilst its Australian counterpart fell - 11bp to 4.72%. The Australian dollar fell during the month to US$0.69, implying a decrease of 0.3 cents, pressured by softer commodity prices and a firmer US dollar. Funds operated by this manager: |

27 Jul 2026 - 10k Words | July 2026

24 Jul 2026 - Global ABS 2026: Strong Technicals, More Selective Tone

|

Global ABS 2026: Strong Technicals, More Selective Tone Challenger Investment Management July 2026 (6-minute read) Barcelona offered an unusually dramatic setting for this year's Global ABS conference, with evening fireworks to celebrate the visit of Pope Leo XIV for the inauguration of the Sagrada Família's newest tower. But inside the conference halls and evening receptions of the 30th Annual Global ABS Conference, the tone was rather steadier. Challenger IM Credit Income Fund , Challenger IM Multi-Sector Private Lending Fund For Adviser & Investors Only Disclaimer: This material has been prepared by Challenger Investment Partners Limited (Challenger Investment Management or Challenger), ABN 29 092 382 842, AFSL 329 828. This document does not relate to any financial or investment product or service and does not constitute or form part of any offer to sell, or any solicitation of any offer to subscribe or interests and the information provided is intended to be general in nature only. This should not form the basis of, or be relied upon for the purpose of, any investment decision. This document is not available to retail investors as defined under local laws. This document has been prepared without taking into account any person's objectives, financial situation or needs. Any person receiving the information in this document should consider the appropriateness of the information, in light of their own objectives, financial situation or needs before acting. This document is provided to you on the basis that it should not be relied upon for any purpose other than information and discussion. The document has not been independently verified. No reliance may be placed for any purpose on the document or its accuracy, fairness, correctness, or completeness. Neither Challenger Investment Management nor any of its related bodies corporates, associates and employees shall have any liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of the document or otherwise in connection with the presentation. |