No events currently listed.

August 2026

RBA - Monetary Policy Decision

Find a Fund

Peer Group Analysis »

| Index Selector Links | 1 Year | 3 Year | 5 Year |

|---|---|---|---|

4.01% |

9.59% |

4.11% |

|

1.78% |

7.61% |

5.80% |

|

7.47% |

8.61% |

6.12% |

|

15.16% |

15.95% |

7.17% |

|

10.47% |

14.11% |

8.52% |

|

19.13% |

13.73% |

9.44% |

|

15.90% |

12.39% |

4.33% |

|

5.54% |

8.96% |

3.60% |

|

12.29% |

13.52% |

7.57% |

|

9.07% |

8.76% |

5.74% |

|

11.85% |

8.23% |

7.63% |

|

-27.25% |

16.08% |

11.04% |

|

4.39% |

5.45% |

3.04% |

|

4.14% |

5.45% |

1.94% |

|

6.51% |

8.24% |

6.95% |

|

8.05% |

8.38% |

7.88% |

|

0.91% |

2.24% |

1.15% |

|

11.05% |

11.01% |

9.55% |

Hedge Clippings

Hedge Clippings | 07 August 2026

This week: Domestically, a trade surprise and an RBA decision already priced in by the market. Offshore, a possible end to the five month Hormuz standoff, and a genuine split forming in how markets are pricing the AI capex build out. Plus,...

Read more...

10 Aug 2026

Australian Equities Peer Group Review

This review presents the FundMonitors.com database's three Australian equity peer groups together: 127 long only large cap funds, 103 long only small and mid cap funds, and...

10 Aug 2026

Performance Report: Quay Global Real Estate Fund...

The Quay Global Real Estate Fund (Unhedged) Active ETF (ASX:QGRU) rose by +1.35% in July, outperforming the FTSE EPRA/ NAREIT Developed NET TR benchmark by +0.08%. Since its...

10 Aug 2026

Performance Report: Bennelong Australian Equities...

The Bennelong Australian Equities Fund rose by +2.68% in July, outperforming the ASX 200 Total Return benchmark by +0.42%. Since inception in February 2009, in the months...

10 Aug 2026

Manager Insights | East Coast Capital Management

Chris Gosselin, CEO of FundMonitors.com, speaks with Simone Haslinger, Chief Executive Officer at East Coast Capital Management.

7 Aug 2026

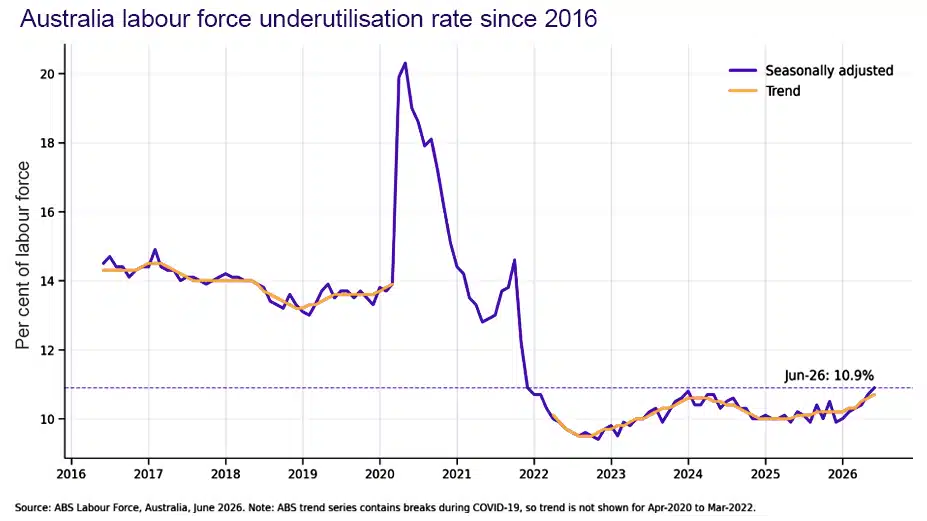

Strong jobs growth masks deteriorating picture

The latest jobs data has lifted market expectations for an RBA hike, but rising underutilisation suggests the labour market is gradually softening. (2-minute read time)

6 Aug 2026

Diversified & Alternative Strategies Peer Group...

This review presents three FundMonitors.com peer groups that occupy different sectors within alternative asset allocation: 87 Multi-Sector funds, the diversified multi-asset...

6 Aug 2026

Investment Perspectives: How the US equity cycle...

These massive increases in AI-related capex estimates will also pull up S&P 500 EPS estimates for 2026-27, given the accounting mismatch for revenue / profits (immediate...

5 Aug 2026

2026 mid-year update & outlook

4D discussed what the year ahead could bring. Reflecting upon the risks and opportunities we highlighted, and the events of the last six months, the central tenets of our...

4 Aug 2026

Income & Credit Peer Group Review

This review presents the FundMonitors.com database's four

income and credit peer groups together: 80 Australian and

49 global bond and diversified fixed interest...

4 Aug 2026

New Funds on Fundmonitors.com

Here are some of the latest additions to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports,...

10 Aug 2026

Manager Insights | East Coast Capital Management

Chris Gosselin, CEO of FundMonitors.com, speaks with Simone Haslinger, Chief Executive Officer at East Coast Capital Management.

3 Aug 2026

Manager Insights | FarmCap

Chris Gosselin, CEO of FundMonitors.com, speaks with Jonathan Weinstock, Founder and Managing Director at FarmCap.

6 Jul 2026

The changing world order and what it means for...

Geopolitical events are no longer just creating short-term market volatility, they're reshaping the global investment landscape in more lasting ways. (38-minutes)

30 Jun 2026

Netflix: Navigating deals, AI and growth

As streaming competition intensifies and AI reshapes the media landscape, Deputy Portfolio Manager Ryan Joyce explores how Netflix is navigating a pivotal period for the...

19 Jun 2026

Expert Analysis of the RBA's June 16 Rate Decision

Chris Gosselin, CEO of FundMonitors.com, speaks with Nicholas Chaplin, Director and Portfolio Manager at Seed Funds Management.

2 Jun 2026

National Adviser Roadshow - The Great Mispricing

Emma Fisher, Airlie's Deputy Head of Australian Equities, explores the "Great Mispricing" we're currently witnessing in Australian equities and where she is uncovering...

1 Jun 2026

Manager Insights | Digital Asset Funds Management

Chris Gosselin, CEO of FundMonitors.com, speaks with Clint Maddock, Director and Co-Founder at Digital Asset Funds Management. Clint discussed how the fund has remained...

21 May 2026

Global Perspectives: Addressing the most...

In this episode, Portfolio Manager Denny Fish takes a deep dive into the current state of artificial intelligence (AI), including the latest advancements, its potential to...

20 May 2026

Who's winning the AI race - and does it matter?

In this episode, we explore how artificial intelligence (AI) is reshaping global competition. (Duration: 27 Mins)

15 May 2026

Manager Insights | Datt Capital

Chris Gosselin, CEO of FundMonitors.com, speaks with Emanuel Datt, founder and Chief Investment Officer at

Datt Capital.

Datt Capital.

AFM News / Info

Australian Equities Peer Group Review

This review presents the FundMonitors.com database's three Australian equity peer groups together: 127 long only large cap funds, 103 long only small and mid cap funds, and 67 alternative structure funds spanning long/short, market...

Read more...

Online Applicatons

Free, simple and secure

Olivia123 - the fast simple and secure online alternative to completing paper based application forms.

Featured Funds

Education

What Our Clients Say

"I've been subscribing to AFM for over two years and love it. The ability to compare funds, do in-depth research and gain data-driven insights into performance metrics and performance rankings in a highly visual way is second to none. Highly recommended."

~ James Waggett,

Managing Director of Waggett Wealth Advice Ltd