NEWS

26 Mar 2026 - Becoming wary of software

|

Becoming wary of software Challenger Investment Management March 2026 (9-minute read) Many of you will have seen news over the past few weeks regarding the US Private Credit sector's exposure to software and flow on concerns regarding the impact of AI on the software businesses. Investor concerns have centred around those managers who are most exposed with most press articles focussed on Blue Owl Capital as amongst the largest players in the private credit market they have the highest exposure.

Turning to the domestic private credit market we think the following is important:

The constant challenge for investors which is especially true in this environment is that the assessment of the risk of a fund is not just about the assets, it's not just about the manager and not just about their governance practices. A major determinant of outcomes will be how other investors respond. This is a much tougher proposition for investors to assess - size and scale matters here, access to institutional capital, transparency and approach to governance. A private credit firm with one open ended fund, poor valuation discipline, external leverage and lack of scale is far more exposed than the alternative. Challenger IM Credit Income Fund , Challenger IM Multi-Sector Private Lending Fund For Adviser & Investors Only Disclaimer: This material has been prepared by Challenger Investment Partners Limited (Challenger Investment Management or Challenger), ABN 29 092 382 842, AFSL 329 828. This document does not relate to any financial or investment product or service and does not constitute or form part of any offer to sell, or any solicitation of any offer to subscribe or interests and the information provided is intended to be general in nature only. This should not form the basis of, or be relied upon for the purpose of, any investment decision. This document is not available to retail investors as defined under local laws. This document has been prepared without taking into account any person's objectives, financial situation or needs. Any person receiving the information in this document should consider the appropriateness of the information, in light of their own objectives, financial situation or needs before acting. This document is provided to you on the basis that it should not be relied upon for any purpose other than information and discussion. The document has not been independently verified. No reliance may be placed for any purpose on the document or its accuracy, fairness, correctness, or completeness. Neither Challenger Investment Management nor any of its related bodies corporates, associates and employees shall have any liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of the document or otherwise in connection with the presentation. |

25 Mar 2026 - Emerging Markets: How AI concerns are impacting India

|

Emerging Markets: How AI concerns are impacting India Pendal March 2026 (5 minutes read time) |

|

Fears that rapid advances in artificial intelligence could slow global IT spending have weakened investor confidence in Indian software stocks. Pendal's Global Emerging Markets Opportunities team investigates the implications for India's growth and current account balance. THE explosion in capability of AI models in recent months has led some equity market participants to become more cautious about the outlook for various service sector industries, leading to selloffs in sectors from software to financial planning. As investors who approach the asset-class primarily through top-down, country-level developments, the GEMO team has been thinking about what this might mean for India. India is one of a group of emerging markets that tend to run current account deficits. "These are countries that have significant latent domestic demand but where, for various historical, geographical or institutional reasons, domestic production falls short. These markets tend to have higher beta to global liquidity and risk appetite," says James Syme, senior fund manager, JOHCM. "Most pertinently for India, the growth cycles of these countries tend to be constrained by inflation and external deficits, with both vulnerabilities reflecting demand running too far ahead of supply." Since the end of 2010, India's current account deficit has averaged 1.7 per cent of GDP, although the maximum deficit was 5.1 per cent of GDP. The structure of the current account balance has developed through time, and changed with India's economic cycle, but some components remain structurally important. In 2025, India ran a deficit in non-oil goods of US$189 billion (4.9 per cent of GDP). Net oil imports were US$122 billion (3.2 per cent of GDP). The resultant trade deficit of US$311 billion (8 per cent of GDP) was substantially offset by a net positive services balance of US$210 billion (5.4 per cent of GDP). Notably, the surplus in IT services was US$227 billion (5.9 per cent of GDP). India also ran a positive income balance of US$85 billion (2.2 per cent of GDP), for an overall current account deficit of US$17 billion (0.4 per cent of GDP). Syme says this relationship between IT service exports and oil imports is key for India's economy, and the two have grown together. In fiscal year 2019, net IT service exports were US$85 billion, and oil imports were US$93.9 billion. "The varying cycles in global IT service spending and the oil price are key for the health of the Indian economy," explains Syme. At a time of higher oil prices, what does the downturn in sentiment towards software and IT service stocks mean for India? In the first two months of 2026, the MSCI India IT Index has fallen over 20 per cent in USD terms. "This is concerning, because the aggregate revenue of India's listed IT companies has a high correlation with the economy's IT service exports," says Syme. If the negative outcome that stocks are pricing in comes to pass, particularly with higher oil prices, India's growth may be constrained by the current account balance. "However, it is important to note that the 12-month forward consensus estimates for both the revenues and profits of the constituents of MSCI India IT Index have increased by 3.4 per cent year to date," notes Syme. "This steady growth in the fundamental outlook for these companies suggests both opportunity in the sector, where we remain overweight, and ongoing support for the Indian economic growth story, although we remain underweight the country on valuation grounds. "We do not feel that share price moves alone constitute a macro-level signal for India at this time." |

|

Funds operated by this manager: Pendal MicroCap Opportunities Fund , Pendal Sustainable Australian Fixed Interest Fund - Class R , Pendal Focus Australian Share Fund , Pendal Horizon Sustainable Australian Share Fund , Regnan Credit Impact Trust Fund , Pendal Sustainable Australian Share Fund , Pendal Multi-Asset Target Return Fund , Barrow Hanley Concentrated Global Share Fund , Pendal Active Balanced Fund , Pendal Active Conservative Fund , Pendal Australian Equity Fund , Pendal Australian Long/Short Fund , Pendal Australian Share Fund , Pendal Dynamic Income Fund - Class R , Pendal Fixed Interest Fund , Pendal Global Emerging Markets Opportunities Fund - Wholesale Class , Pendal Global Property Securities Fund , Pendal Government Bond Fund , Pendal Imputation Fund , Pendal MidCap Fund , Pendal Monthly Income Plus Fund , Pendal Property Investment Fund , Pendal Short Term Income Securities Fund , Pendal Smaller Companies Fund |

|

This information has been prepared by Pendal Fund Services Limited (PFSL) ABN 13 161 249 332, AFSL No 431426 and is current as at December 8, 2021. PFSL is the responsible entity and issuer of units in the Pendal Multi-Asset Target Return Fund (Fund) ARSN: 623 987 968. A product disclosure statement (PDS) is available for the Fund and can be obtained by calling 1300 346 821 or visiting www.pendalgroup.com. The Target Market Determination (TMD) for the Fund is available at www.pendalgroup.com/ddo. You should obtain and consider the PDS and the TMD before deciding whether to acquire, continue to hold or dispose of units in the Fund. An investment in the Fund or any of the funds referred to in this web page is subject to investment risk, including possible delays in repayment of withdrawal proceeds and loss of income and principal invested. This information is for general purposes only, should not be considered as a comprehensive statement on any matter and should not be relied upon as such. It has been prepared without taking into account any recipient's personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation. The information may contain material provided by third parties, is given in good faith and has been derived from sources believed to be accurate as at its issue date. While such material is published with necessary permission, and while all reasonable care has been taken to ensure that the information is complete and correct, to the maximum extent permitted by law neither PFSL nor any company in the Pendal group accepts any responsibility or liability for the accuracy or completeness of this information. Performance figures are calculated in accordance with the Financial Services Council (FSC) standards. Performance data (post-fee) assumes reinvestment of distributions and is calculated using exit prices, net of management costs. Performance data (pre-fee) is calculated by adding back management costs to the post-fee performance. Past performance is not a reliable indicator of future performance. Any projections are predictive only and should not be relied upon when making an investment decision or recommendation. Whilst we have used every effort to ensure that the assumptions on which the projections are based are reasonable, the projections may be based on incorrect assumptions or may not take into account known or unknown risks and uncertainties. The actual results may differ materially from these projections. For more information, please call Customer Relations on 1300 346 821 8am to 6pm (Sydney time) or visit our website www.pendalgroup.com |

24 Mar 2026 - Australian Secure Capital Fund - Property Update

|

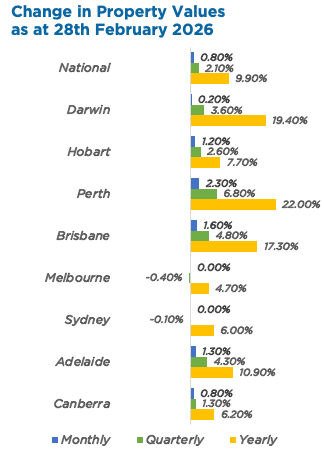

Australian Secure Capital Fund - Property Update Australian Secure Capital Fund March 2026 (1-minute read) February was another strong month for Australian property values, posting a national rise of 0.8% for the second consecutive month. Perth (+2.3%) again led the way with a second straight monthly rise of greater than 2%, adding more than $22,500 to the median dwelling value over the month. Similarly, Brisbane (+1.6%) and Adelaide (+1.3%) again saw monthly increases of greater than 1%. Conversely, values in Melbourne and Sydney were flat over February, with both cities notching slight rolling quarterly decreases of -0.4% and -0.1%, respectively. As a result, regional areas continue to outperform the capital cities, rising by 1.1% month-on-month, compared to 0.6% for the capitals. Nationally, rents increased 1.7% over the three months to February 2026, denoting the highest rolling quarterly increase since April 2025.

Source: Cotality HVI, 02 March 2026 February Edition Funds operated by this manager: ASCF Select Income Fund , ASCF High Yield Fund , ASCF Premium Capital Fund , ASCF Private Fund (Wholesale)

|

February due to reporting season, persistent AI disruption

fears and ongoing geopolitical tension. (2-minute read)

23 Mar 2026 - Glenmore Asset Management - Market Commentary

|

Market Commentary - February Glenmore Asset Management March 2026 (2-minute read) The volatility of the last few months was amplified in February due to reporting season, persistent AI disruption fears and ongoing geopolitical tensions. Domestically, large caps materially outperformed small/mid caps, resulting in the All Ordinaries Accumulation Index rising +3.3% compared to a -2.6% decline in the ASX Small Ordinaries Accumulation Index. The ASX50 had an extremely strong month, increasing by +7.9%, whilst at the smaller end, the Small Ords Industrials declined -4.5%. Capital light businesses, such as software and technology companies fell sharply due to investor fears around disruption from AI, whilst resources and mining services outperformed. In comparing the fund's performance versus the benchmark in February, it should be noted the fund has a strong small/mid cap focus. Over the long term, there is clear evidence that these companies deliver superior returns to large caps, however during periods of investor risk aversion (such as the current environment where the RBA is raising interest rates to combat inflation), investor funds typically move out of small caps to the perceived safety of large cap companies. In the US, the tech heavy NASDAQ was weighed down by similar factors, resulting in a -3.4% decline in the month, underperforming the S&P 500 which fell -0.9%. Outside of the US, the Euro Stoxx 50 and FTSE 100 maintained their recent momentum, rising +3.2% and +6.7%, respectively. As we have discussed, the expectation of further RBA rate hikes has continued to drive a rotation back into large caps. Bluechip names rebounded in February, including CBA (+17%), NAB (+13%), BHP (+16%) and Woolworths (+16%). Whilst the market continues to expect 1-2 more RBA rate hikes over the next 12 months, past cycles have shown that the underperformance of small/mid caps tends to bottom well before the end of a rate hiking cycle. In bond markets, the US 10-year bond yield recorded a sharp decline, falling -30 basis points (bp) to 3.94%, whilst its Australian counterpart fell -16bp to 4.65%. The Australian dollar continued to rise, increasing +2.2% to US$0.71, implying an increase of 1.5 cents. Funds operated by this manager: |

20 Mar 2026 - Investment considerations of prolonged uncertainty over Iran

|

Investment considerations of prolonged uncertainty over Iran Janus Henderson Investors March 2026 (8-minute read) The conflict in the Middle East has escalated over the last few days and hopes for a short war have faded. Regional diplomatic efforts to de-escalate appear to be failing and Iran continues to retaliate in response to strikes from the US and Israel. As a result, the Strait of Hormuz - the world's most important gateway for energy commodities - remains effectively closed to all but the most buccaneering of shipping companies. The Strait closure is a result of a lack of insurance, firms not willing to risk the loss of future capacity if ships are sunk, and concerns for the welfare of sailors after several fatalities already. However, there are now risks of more intensive intervention from the US and/or Israel following reports that they are considering putting boots on the ground, either to try and extract Iranian enriched nuclear material or to take Kharg Island, a key sea terminal for Iranian oil exports. At the same time, a new Supreme Leader of Iran has been chosen who is seen as another hardliner. This is unlikely to be taken well by the US, who would have preferred someone more moderate, and the choice appears unlikely to create a path to de-escalation. The desired end point is still uncertainIt is still not immediately clear what the ultimate objectives for the US and Israel are. Various intentions have been publicly stated but it is not clear which of these are red lines and which are just preferences. A further reduction of the potential for Iran to build nuclear weapons appears to be the closest to a requisite. However, given that strikes in 2025 were deemed to have achieved this, defining the outcome is difficult. Similarly, a desire to destroy Iran's long-range missile program has been expressed, but this may similarly be difficult to guarantee. Finally, regime change, either for military or humanitarian reasons, is now touted as a key objective, but it remains unclear how this can be achieved with airstrikes alone. The objective mattersUnderstanding the motivating objectives is important when considering how long the war might last and the subsequent economic impact. We can look to several factors that suggest this could be a more prolonged campaign. Iran has indicated that it can continue with its current rate of response for six months, far longer than the weeks-long engagement that markets appeared to have been pricing. The US has expressed that it wishes to remove the previously enriched uranium that could be used in nuclear weapons, but it has been a long time since the last international inspection and its whereabouts are likely to be very uncertain. Similarly, the continuity of a new hardline leader suggests that Iran is feeling little pressure to change tack yet. However, there are also ways in which the conflict could be wound up sooner. The most obvious is that US President Trump has shown a willingness to abruptly change direction on policy multiple times throughout his leadership, no matter the scale of the impact. With mid-term elections coming up later in the year, the US government is likely to be highly sensitive to anything that pushes up the cost of living. Therefore, finding a way to declare victory and return oil prices to lower levels may ultimately dominate any longer-term military objectives. The length mattersA longer-term conflict raises the danger of greater destabilisation in the region, creates greater potential for more severe damage to key infrastructure and risks longer-lasting impact on energy supplies. While there are some ways to mitigate the impact in the near term, such as sending oil through pipelines to ports less likely to be targeted, or by releasing strategic reserves outside of the Middle East, these are either inherently temporary or lack the potential capacity to offset prolonged restrictions in the Strait of Hormuz. Oil is often seen as the key commodity when considering conflicts in the Middle East, given its relevance to US gasoline prices in particular, but natural gas supplies are crucial for other regions, such as Europe, and other base products feed into areas from chemicals to fertilisers. Last week, markets appeared to be pricing energy commodities in line with a short-term interruption to the ease of supply. Assumptions around this appear to have changed over the weekend, with prices now moving to incorporate greater risk of a prolonged engagement. The lack of clarity around the US/Israeli objectives does nothing to reduce the uncertainty that markets hate. Impact on marketsThe price of oil has spiked above US$100 per barrel as concerns about supplies have intensified. European natural gas prices have almost doubled since the end of February. This is raising the spectre of the inflationary impulse generated by the Russian invasion of Ukraine in early 2022 and the subsequent removal of much of the Russian supply into energy markets. Concerns about a jump in European inflation or simply prolonged stickiness in the US are lifting bond yields. US Treasury yields have moved higher as markets have taken out one of the US Federal Reserve interest rate cuts that were anticipated by the end of the year. Yields on 10-year Treasuries have seen less movement than their European counterparts, as US jobs numbers on Friday served to offset some upward yield pressure from expected inflation. Concerns about inflation have seen surges in German and UK breakeven rates, with market pricing for the European Central Bank interest rates at the end of 2026 now looking at over 1.5 hikes. Since the end of February, expectations for the Bank of England have shifted from two cuts by the end of 2026 to a better than 50:50 chance that there will be an interest rate hike - a marked shift in the outlook. Markets are now pricing in higher oil prices for the foreseeable future, with concerns mounting about a stagflationary outcome, should higher energy costs stall a re-acceleration in economic growth. The uncertainty has provided support for the much-maligned US dollar, given the American economy is looking better set to weather an energy shock than elsewhere. However, higher bond yields and a stronger greenback have dampened gold's ability to rally in the current environment, following strong performance during other recent periods of volatility. Equity markets are seeing something of a reversal of recent performance dynamics. Markets that started the year positively, to the end of February, suddenly look under greater pressure. A stronger dollar and higher oil prices are weighing on Asian stocks that had been surging in the first two months of the year. Gas prices remain Europe's geopolitical Achilles heel and markets are clearly concerned that the region is overly exposed again. In the US, last week saw some signs of a reversal of the recent outperformance of Value stocks over their Growth counterparts. AI-related stocks have struggled in 2026 so far compared to the rest of the market, but the fears that higher oil prices could dent the very rosy economic outlook are leading to something of a reconsideration. The effective closure of the Strait of Hormuz is unprecedented, undoubtedly making for severe impacts on risk assets. However, to put the sell-off in proper context, investors must also recognise that equities entered the conflict trading at a meaningful premium over historical valuation levels. The forward price/earnings ratios (P/Es) of major global equity markets were at top quartile levels versus their 20-year histories[1], roughly a 15%-30% premium compared to median levels. Indeed, the markets experiencing the largest sell-offs are the ones that entered the conflict with the highest returns year to date[2]. Risks of a prolonged war but don't rule out a quick "victory"Situations like this demonstrate the value of well-diversified multi-asset portfolios. Geopolitical events are rarely easy to gain complete clarity on, with the current US administration apparently embracing uncertainty as a negotiation strategy. What we can take away from the events of the last few days is that it is likely the conflict could last longer than many had initially hoped. This means there is the potential for greater economic impact - and markets have moved to price in this change. There is the potential for faster inflation and slower economic growth, with assets focusing on different aspects thus far. However, risks remain two-sided. US political pressures means that a quick "victory" should not be ruled out. Asset prices, driven by energy prices, are likely to swing violently as investors alter their expectations for either outcome. [1] Source: Datastream, 27 February 2026. Past performance does not predict future returns. [2] Source: Bloomberg, 31 December 2025 to 9 March 2026. Past performance does not predict future returns. |

|

Funds operated by this manager: Janus Henderson Australian Fixed Interest Fund , Janus Henderson Conservative Fixed Interest Fund , Janus Henderson Diversified Credit Fund , Janus Henderson Global Natural Resources Fund , Janus Henderson Tactical Income Fund , Janus Henderson Australian Fixed Interest Fund - Institutional , Janus Henderson Conservative Fixed Interest Fund - Institutional , Janus Henderson Cash Fund - Institutional , Janus Henderson Global Multi-Strategy Fund , Janus Henderson Global Sustainable Equity Fund , Janus Henderson Sustainable Credit Fund All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect. The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested. Whilst Janus Henderson believe that the information is correct at the date of publication, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson to any end users for any action taken on the basis of this information. |

19 Mar 2026 - Correlation and How to Think About Diversifying Alternatives

|

Correlation and How to Think About Diversifying Alternatives Fidante February 2026 (7-minute read) Achieving diversification and uncorrelated returns are a common objective when constructing investment portfolios. Understanding what those terms really mean is essential to properly appreciate how alternative investments can contribute to robust long-term portfolios.

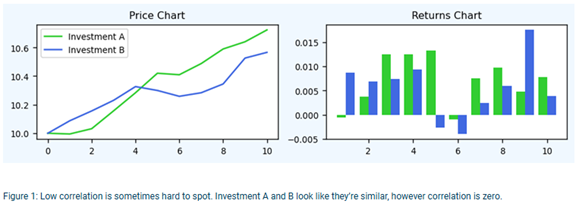

What is correlation?Correlation is a statistical measure of the relationship between the returns of two investments (rather than price levels). It ranges from -1 to +1. Investments with high correlation tend to move in the same direction at the same time, while investments with little or no correlation tend to move independently of each other. Negatively correlated investments tend to move in opposite directions. Importantly, two investments that both deliver positive long-term returns can nevertheless exhibit zero or even negative correlation. Conversely, investments that appear to move in opposite directions over time can be positively correlated. For example, daily price movements may show a very different relationship from the point to point one-year return. In figure 1, at first glance it may appear that the two investments shown in the left-hand chart below are positively correlated. After all, for the period shown, both have increased by about the same amount. Looking at the daily returns in the chart on the right, we can see that most days the two investments do indeed move up together, however, on some days they move in opposite directions. Counterintuitively, the correlation of these two strategies turns out to be zero. An important implication is that investors can derive diversification benefits from two investments that both go up over time.

It's also important to note that statistically high correlation does not imply causation. Just because two return series are highly correlated does not mean one necessarily causes the other to move. As a result, correlation can and does change over time.

Why does correlation matter?By combining uncorrelated investments, we can construct portfolios with lower risk and/or higher returns. This is the power of diversification. The lower the correlation between assets, the greater the potential benefit. This is where alternatives come in - no other asset class offers the same variety and breadth of uncorrelated investments as the universe of alternative investments.

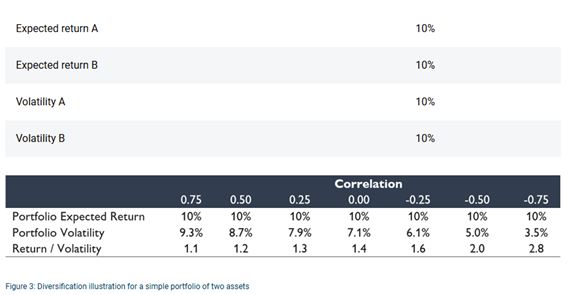

A simple illustrationTo see why uncorrelated assets produce better portfolios, consider two investments, A and B. Both are expected to return 10% per year and each has volatility of 10%.

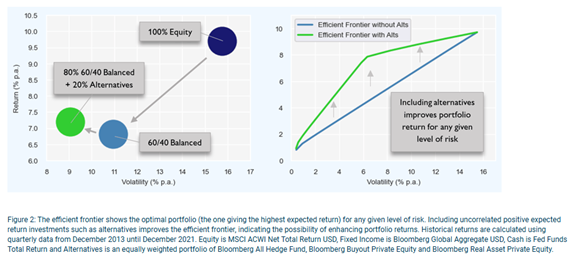

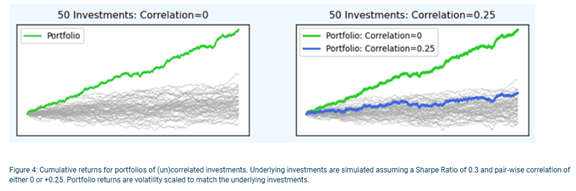

Figure 3 shows that when these investments are highly correlated, combining them does little to reduce portfolio risk. However, when correlation is low or even negative, portfolio volatility drops to levels far below that of either A or B individually, even though expected returns remain the same. This leads to higher risk adjusted returns - the portfolio earns the same return with less volatility. The effect becomes even more powerful in larger diversified portfolios. Consider an equally weighted portfolio of 50 completely uncorrelated investments, all with the same ex-ante expected return and ex-ante volatility and a modestly positive Sharpe Ratio2 of 0.3. The portfolio returns are shown by the green line on the left-hand chart, and the Sharpe Ratio is now 1.94, a significant improvement on any individual investment. However, even a small increases in correlation can significantly dilute these benefits. If these 50 investments now have a pair-wise correlation of 0.25 (still a relatively low correlation), the cumulative portfolio return becomes dramatically lower than when correlation was zero, as shown by the blue line in the right-hand chart. \While the above is a contrived example from a simulation, it illustrates just how powerful the combination of uncorrelated investments can be. This is where alternatives have the potential to play such an important role in investment portfolios.

In practice, it is extremely difficult to find large numbers of investments that are truly uncorrelated at all times. However, each additional uncorrelated investment introduced into a portfolio increases the potential diversification benefits for the portfolio. Alternative investments are often uncorrelated not only to traditional assets like equities and bonds, but also to each other, making a rich hunting ground for investors seeking to maximise the power of diversification. There is, however, an important caveat. Just as low or negative correlation enhances diversification, even small changes in correlation can undermine it, sometimes quickly and unexpectedly. What factors affect correlation?Correlation can increase during periods of market stress, economic shocks or major shifts in monetary policy. Events such as the COVID market sell off in early 2020 saw correlations spike as many assets moved sharply lower at the same time. Even if only temporary, this can have a devastating impact on portfolios if previously uncorrelated investments all move in the same direction at the same time. The experience of 2022 provided another stark example. Rising interest rates negatively affected both equities and bonds, causing the traditional 60/40 portfolio to suffer unusually large losses. Assets that investors expected to diversify one another instead moved together. Understanding the common drivers of returns is therefore critical when thinking about how correlation might change. When many investments rely on similar economic factors, such as low interest rates, correlation can rise sharply when those conditions change, as we saw in 2022. Some investors attempt to anticipate these shifts and rebalance portfolios accordingly. However, this can be difficult, so alternative investments that are less susceptible to correlation changes can be useful as 'anchor' diversifiers in a portfolio. The challenges of measuring correlation While uncorrelated investments can improve portfolio diversification and resilience, measuring correlation is not straightforward. There is no single measure to determine "true" correlation. Investors need to consider:

Useful techniques include examining rolling correlations, analysing how investments behave during market downturns and monitoring whether regime changes have altered the relationship between two investments. It's also worth remembering that correlation is only one part of the investment decision. Some investments may be attractive because of their risk/return profiles, even if diversification benefits are modest. Understanding the role of alternatives in diversification While investors often think about alternative investments as a single category, they can play very different roles within a portfolio. Broadly, alternatives can be grouped into three types based on their primary objective: growth alternatives, which aim to enhance overall portfolio returns; diversifying alternatives, which seek to improve risk adjusted returns by delivering low or uncorrelated performance; and defensive alternatives, which are designed to provide an explicit buffer during periods of market stress. Understanding these distinctions is critical, as the value an alternative investment brings depends not just on its standalone return, but on how it interacts with the rest of the portfolio. Correlation and diversification are particularly central to the second category of diversifying alternatives. Investments with low correlation can materially improve portfolio outcomes by reducing volatility without sacrificing expected returns. Diversifying alternatives can therefore allow investors to achieve better risk adjusted returns rather than simply higher absolute returns, improving the efficiency and resilience of the portfolio as a whole. In this sense, alternatives that consistently deliver diversification benefits can be among the most valuable long term building blocks in a well constructed investment portfolio. Final thoughts Correlation measures how investment returns move relative to one another, but it is not fixed and cannot be relied upon to remain stable. Because correlation is based on historical data, there is no guarantee that it won't change in the future. That said, portfolios constructed with investments with low correlation can deliver higher returns for a given level of risk than those with more highly correlated investments. Correlation can therefore be an essential part of assessing any potential investment and is of particular importance when considering alternative investments. A solid understanding of correlation, its applications and limitations allows investors to unlock the power of diversification. While correlations can change, alternative investments that deliver consistently low correlation to traditional assets can be particularly valuable in building more robust, resilient portfolios. 1Markowitz, H.M. (March 1952). "Portfolio Selection". The Journal of Finance. |

17 Mar 2026 - 10k Words | March 2026

|

10k Words Equitable Investors March 2026 (2-minute read) Geopolitical risk spikes. After a long period of significant divergence, long term bond yields and forecast earnings yields have reunited. Worth considering alongside the relative performance of "Growth" v "Value". Long-term inflation expectations seem to have stabilised at higher levels than was the case pre-COVID - possibly baking in higher volatility in inflation. Military action swung equity investors straying to emerging markets back to the US. That US market may be concentrated but its a lot less concentrated than the ASX - and in the current period of turbulence concentration has performed very differently relative to equal-weight portfolios in the two countries. There does seem to be more interest in active investing currently. Finally, we can't escape without a chart on the decline of listed SaaS valuations - but in the context of a convergence with unlisted AI valuations. Geopolitical Risk Index relative performance to VIX (US volatility) over 1 year

Source: Caldara and Iacoviello, Koyfin US 10-year bond yield v S&P 500 forward earnings yield

Source: Yardeni Growth relative to Value (iShares Russell 1000 Growth / iShares Russell 1000 Value)

Source: Koyfin US 10-Year Breakeven Inflation Rate - relatively stable for past three years

Source: Koyfin Australian 10-year Breakeven Inflation Rate

Source: Equitable Investors, RBA CPI (Australia) - standard deviation of quarter-on-quarter change (rolling 30 quarters)

Source: Equitable Investors, ABS Global yield spreads matrix

Source: Koyfin S&P 500 relative to FTSE Emerging Index - reversal post Iran attack

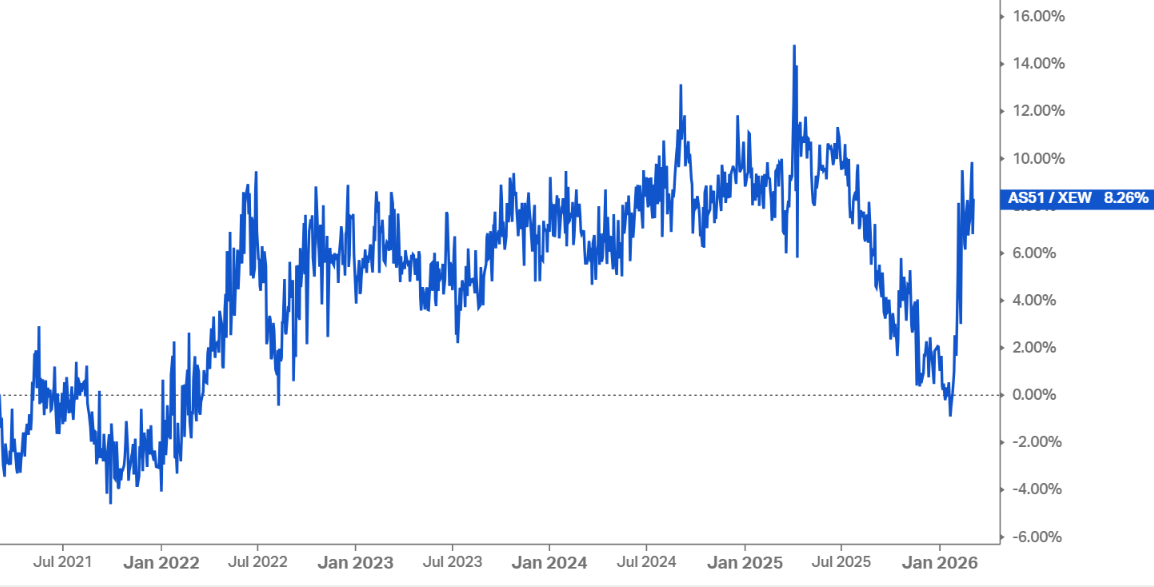

Source: Bloomberg Equities concentration - top 10 holdings' dominance of Aus and US major benchmarks (using iShares ETF proxies)

Source: Equitable Investors, Koyfin S&P/ASX 200 - Free-float weighted (AS51) v equal-weighted indices (XEW)

Source: Equitable Investors, Iress, Koyfin S&P 500 ETFs - Free-float weighted (IVW) v equal-weighted (RSP)

Source: Equitable Investors, Koyfin The number of active ETFs launched each year in the US

Source: Morningstar Public SaaS valuations have converged with AI-led software

Source: Arcadia Capital via Archtis Funds operated by this manager: Equitable Investors Dragonfly Fund Disclaimer Past performance is not a reliable indicator of future performance. Fund returns are quoted net of all fees, expenses and accrued performance fees. Delivery of this report to a recipient should not be relied on as a representation that there has been no change since the preparation date in the affairs or financial condition of the Fund or the Trustee; or that the information contained in this report remains accurate or complete at any time after the preparation date. Equitable Investors Pty Ltd (EI) does not guarantee or make any representation or warranty as to the accuracy or completeness of the information in this report. To the extent permitted by law, EI disclaims all liability that may otherwise arise due to any information in this report being inaccurate or information being omitted. This report does not take into account the particular investment objectives, financial situation and needs of potential investors. Before making a decision to invest in the Fund the recipient should obtain professional advice. This report does not purport to contain all the information that the recipient may require to evaluate a possible investment in the Fund. The recipient should conduct their own independent analysis of the Fund and refer to the current Information Memorandum, which is available from EI. |

13 Mar 2026 - Beyond 'Quality at any price'

12 Mar 2026 - When Geopolitics Moves Markets, Most Portfolios Aren't Ready

|

When Geopolitics Moves Markets, Most Portfolios Aren't Ready East Coast Capital Management March 2026 3-minute read There is a particular kind of market risk that doesn't show up cleanly in a spreadsheet. It doesn't follow earnings seasons or central bank calendars. It arrives through a headline, a border dispute, a sanctions announcement - and by the time most investors have processed it, the repricing has already begun. Geopolitical risk is not new. But the current environment has a different character to it. What we are seeing is not a series of isolated shocks, but an accumulation of structural pressures: fractured supply chains, sustained conflict, and policy unpredictability operating simultaneously across multiple geographies. That combination has a way of staying in markets longer, and running deeper, than a single event. The question for investors is not whether this will eventually resolve. It's whether their portfolios are positioned to navigate the period before it does. What Markets Are Actually Signalling In periods of genuine geopolitical stress, the signal tends to show up in commodities and currencies before it surfaces in equities. Energy markets become a key transmission mechanism: oil price volatility doesn't just reflect supply anxiety, it flows directly into inflation expectations, corporate cost structures, and consumer sentiment. We have seen exactly this dynamic play out. Supply disruptions have kept energy markets volatile and directional. Currency markets have repriced on shifting capital flows and policy divergence. These are not peripheral markets - they sit at the centre of how geopolitical stress propagates through the real economy. Systematic trend following is well-suited to precisely this environment. Not because it predicts geopolitical outcomes (it doesn't) but because it is built to detect and follow the price trends that geopolitical stress tends to produce. When energy trends, it captures energy. When currencies move on safe-haven flows, it captures that too. The strategy doesn't need to know why a trend is happening. It needs to know that it is. The Diversification Assumption Worth Re-examining Most portfolios carry an implicit assumption: that diversification across asset classes will provide protection when conditions deteriorate. In stable regimes, this assumption generally holds. In stress regimes, it often doesn't. When a single macro force - geopolitical risk, an energy shock, a sudden policy reversal - moves through markets simultaneously, assets that appeared uncorrelated begin moving together. The diversification that looked sound on paper compresses exactly when it needs to expand. This is not a flaw to be corrected with more asset classes. It is a feature of how modern markets behave under stress, and it requires a different solution: exposure to return streams that are structurally independent of traditional beta, rather than just spread more widely across it. "True diversification isn't about just holding more assets," says Simone Haslinger, CEO of East Coast Capital Management. "It's about holding assets that behave differently when conditions become difficult. That's a higher bar -- and it's the bar that matters." A Framework Built for Uncertainty, Not Despite It At ECCM, we are often asked how trend following performs in "normal" markets. The reality is that trend following is designed for the full range of market conditions, but it tends to earn its keep most visibly in environments like the current one. Geopolitical stress produces the extended, directional moves across commodities, currencies, and rates that trend following is built to capture. Elevated volatility, far from being a headwind, is the raw material the strategy works with. And because our approach is rules-based, it doesn't require us to take a view on how a conflict resolves, which policy will be enacted, or how long uncertainty will persist. The price action tells us what we need to know. This matters in practice. When uncertainty is high, discretionary decision-making is most prone to error: anchoring to prior regimes, hesitating at inflection points, or seeking safety in familiar assets regardless of what the trends are telling them. A systematic process removes that vulnerability. Conclusion Geopolitical uncertainty is not a phase to be endured while waiting for markets to normalise. For investors with the right framework in place, it is a productive environment - one that generates the kind of clear, sustained trends that systematic strategies are built to capture. At ECCM, our ECCM Systematic Trend Fund is designed to do exactly that: to respond to what markets are doing, wherever the opportunity arises, and to deliver return streams that remain genuinely uncorrelated to traditional portfolios through periods of stress and stability alike. Wholesale clients can find more information on ECCM and the ECCM Systematic Trend Fund at Australian Fund Monitors and ECCM's website. Funds operated by this manager: |

11 Mar 2026 - Beyond scale: rethinking the engine room of European infrastructure

|

Beyond scale: rethinking the engine room of European infrastructure abrdn February 2026 (4-minute read) The prevailing narrative in infrastructure favours scale. Large funds, large assets, and large ambitions dominate the conversation. Yet, as Europe's energy transition continues and policy reforms reshape the investment landscape, it's increasingly clear that meaningful progress is being driven by the small- and mid-cap segments. Transactions below €500 million account for the majority of European infrastructure deals. This is the centre of gravity for new investment and innovation. Our experience over more than a decade - with around €3 billion invested across energy, transport and digital infrastructure - consistently points to the same conclusion. The lower mid-market is where policy ambition, operational delivery and investor returns align most effectively. There's less need for intermediaries, and it's materially less competitive. This gives space for genuine value creation, rather than simply financial engineering. Policy tailwinds and competitive advantageRecent reforms in the EU's market design for electricity, quicker permit approvals, and the Net-Zero Industry Act have shifted the balance in favour of assets that can adapt quickly and align with local policy priorities. Small- and mid-cap platforms have a structural advantage. In practice, this means utilities that work constructively with municipalities, transport assets embedded within national and regional strategies, and energy platforms that can adapt business models as subsidy regimes and security-of-supply priorities evolve. Large, centralised assets often struggle to respond at this pace. Risk, value and evidenceThe notion that smaller assets are riskier doesn't stand up to scrutiny. In regulated sectors, risk is defined far more by framework stability and governance quality than by asset size. Our utility investments in Finland, for example, operate under the same regulatory regimes as larger peers, yet benefit from more conservative capital structures and greater scope for hands-on asset management. Agility, local solutions and systemic changeSmall- and mid-cap assets move at a different pace. Development timelines are shorter, adaptation is faster, and innovation is less encumbered by bureaucracy. In Finland, this has enabled the rapid deployment of electric boilers to exploit periods of low-cost renewable power, the co-location of data centres to capture waste heat, and the diversification of fuel sources within district heating networks to improve resilience. These initiatives were delivered through close engagement with management teams and local authorities, and implemented within months rather than years. Final thoughts...The infrastructure required to support Europe's changing economy won't be delivered solely by megaprojects or flagship assets. It will be built incrementally, through thousands of local decisions across infrastructure systems. It will also be shaped by those who can combine agility, results, and local insight to deliver measurable outcomes - especially as policy and competitiveness trends continue to evolve. |

|

Funds operated by this manager: abrdn Sustainable Asian Opportunities Fund , abrdn Emerging Markets Equity Fund , abrdn Sustainable International Equities Fund , abrdn Global Corporate Bond Fund (Class A)

|