NEWS

10 Jun 2026 - Performance Report: Quay Global Real Estate Fund (Unhedged) Active ETF (ASX:QGRU)

[Current Manager Report if available]

10 Jun 2026 - Australian Secure Capital Fund - Property Update

|

Australian Secure Capital Fund - Property Update Australian Secure Capital Fund May 2026 (1-minute read)

April was a slower month for Australian property values, posting a national rise of 0.3%, the lowest monthly growth rate since January 2025. Once again, Perth (+2.1%) led the way with a fourth consecutive monthly rise of greater than 2%, with its annual increase now reaching 26%. Likewise, Brisbane (+1.2%) and Adelaide (+1.1%) continued to add value, again posting monthly increases of greater than 1%. However, values in Melbourne and Sydney (both -0.6%) declined for a third straight month. Additionally, estimates of capital city home sales over the past three months were down 5.4% compared to last year and 7.4% below the previous five-year average, indicating a slowdown in buyer demand. Regional areas have been more resilient in the face of this, with values increasing by 4.2% over the first four months of the year, compared to 1.8% for the capital cities.

April Edition Funds operated by this manager: ASCF Select Income Fund , ASCF High Yield Fund , ASCF Premium Capital Fund , ASCF Private Fund (Wholesale)

|

9 Jun 2026 - Performance Report: Bennelong Concentrated Australian Equities Fund

[Current Manager Report if available]

9 Jun 2026 - Performance Report: 4D Global Infrastructure Fund (Unhedged)

[Current Manager Report if available]

9 Jun 2026 - Shock absorption: managing the impact of the Middle East conflict on listed infrastructure

5 Jun 2026 - Hedge Clippings |05 June 2026

|

|

|

|

Hedge Clippings | 05 June 2026

The ABS released the March quarter 2026 National Accounts on Wednesday, and the result was a notable slowdown. Australian GDP expanded by just 0.3% on a quarterly basis in Q1 2026, against the 0.8% rise in the prior quarter, with the country's GDP growing just 2.5% year-on-year, both figures missing expectations. The internals told a revealing story: the biggest impact in the quarter was investment in data centres. Westpac estimates that this investment, including spillover effects, drove all the growth this quarter and around 0.8 percentage points of GDP growth in year-ended terms. In other words, strip out the data boom, and the underlying economy effectively flatlined. ICT investment surged from around $2 to $8 billion per quarter as a result of datacentres, accounting for an estimated 85% of growth capital expenditure over the last year, and almost all in Q1 2026. This reveals that the uplift in investment is almost wholly reliant on the data boom, with negligible investment growth in other industries. The economy was clearly slowing even before the Middle East conflict, and we've yet to know how long Trump's short military excursion, now into its third month, is going to last. Adding to the problem is that three interest rate hikes are starting to impact the housing market, which is now subject to further negativity thanks to being side swiped by the changes to negative gearing and CGT contained in the budget. The implication for the RBA's next move is interesting to say the least. Going into their June meeting, the economy is weaker than the RBA had assumed just a month ago, and Q2 could be worse. The Middle East conflict's full impact flows through from April onwards. Adding to this is the April jobs data, showing unemployment rising to 4.5% for April. The bottom line is that the economy is in a genuine squeeze, whether Chalmers or Albanese want to admit it or not. Inflation remains well above target and fuel-driven second-round effects are still working through, but growth is slowing, the labour market is softening, and the trade account has only partially recovered. The RBA faces a classic stagflationary dilemma, albeit a mild one at this stage. Meanwhile, the potential for an acceleration in the decline in property prices further damaging consumer confidence could tip the balance, and the economy, over. Whether the RBA will about-turn again, stay on hold, or, as Westpac are predicting, increase to 4.6% will remain to be seen, but with the next meeting just 10 days away, we won't have to wait too long. News | Insights

May 2026 Performance News |

|

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday |

5 Jun 2026 - What a Structural Shift in Yields Means for Portfolios

|

What a Structural Shift in Yields Means for Portfolios JCB Jamieson Coote Bonds May 2026 (6-minute read) Government bond yields around the world have reached decade highs, driven by higher energy costs and potentially ongoing inflationary pressures stemming from the U.S.-Iran conflict and disruption to global oil supply routes. Beyond the immediate conflict, there are structural reasons yields may stay elevated. Government balance sheets across many advanced economies are increasingly stretched, with debt-fuelled expenditure supporting ambitious policy reforms - from defence to energy transition. Beyond determining government borrowing costs, yields play a central role within the financial system. As the risk-free rate of interest, they underpin the cost of capital across the economy, meaning the current move higher in yields has implications well beyond bonds, reshaping valuations across equities, credit and real assets. If government bond yields stay higher for longer across most of the world, the cost of capital will also rise inexorably. Higher yields translate directly into higher discount rates, and that matters for every asset in a portfolio. Whether its equities, credit or property, valuations are derived by discounting future cash flows at the risk-free rate plus a premium for investment risk. When that base rate moves higher, asset prices adjust lower. A higher cost of capital will likely prompt investors to revise their hurdle rates higher for all investment opportunities and may suggest a more cautious approach to investment risk in general. This could reveal vulnerabilities across asset classes which have benefited from a secular decline in interest rates, and therefore the cost of capital, over the past several decades. Infrastructure, private credit and private equity have benefited from the valuation effects of a relatively low cost of capital, but this is now set to change as higher hurdle rates and revaluations unveil which asset classes and investment strategies can continue to sustain and deliver compelling risk-adjusted returns, and which will struggle to do so going forward. "When the risk-free rate rises, every asset is repriced." Higher bond yields increase discount rates across equities, credit and property--resetting valuations and raising hurdle rates for all investments. Turning to domestic developments, this month's Commonwealth Budget brought significant tax reform and policy announcements alongside a compositional change in revenue and expenditure forecasts that led to modest improvements in the budget balance over the next decade. Drilling into the tax policy changes, reforms to capital gains tax (CGT) and negative gearing may make property as an asset class less attractive to investors and dampen investment activity in the property market. Some analysts forecast a consequent moderation in house prices across the country and frame the contractionary economic effects of the tax reforms as akin to that of one or two RBA rate hikes, foreshadowing the conclusion of an already well progressed RBA rate hike cycle. As investors reassess their portfolios for tax efficiency under the new CGT regime, fixed income and other income generating assets such as high dividend domestic equities could be well placed to benefit from this shift in focus. Ultimately, the budget forecasts depict Australia's fiscal conditions in a highly favourable light relative to our peers, and re-affirms that Australia's government debt remains very low by global standards. For investors, this environment calls for a fundamental reassessment of portfolio construction - where return is coming from, what risks are being compensated, and whether allocations built in a low-rate world remain fit for purpose in a higher-rate one. Funds operated by this manager: CC Jamieson Coote Bonds Active Bond Fund (Class A) , CC Jamieson Coote Bonds Dynamic Alpha Fund This information is for professional and wholesale investors only and has been prepared by JamiesonCooteBonds Pty Ltd ACN 165 890 282 AFSL 459018 ('JCB'). Channel Investment Management Limited ACN 163 234 240 AFSL 439007 ('CIML') is the Responsible Entity and issuer of units for the CC JCB Active Bond Fund ARSN 610 435 302, CC JCB Global Bond Fund ARSN 631 235 553 and the CC JCB Dynamic Alpha Fund ARSN 637 628 918 (collectively 'the Funds'). Channel Capital Pty Ltd ACN 162 591 568 AR No. 001274413 ('Channel') provides investment infrastructure and distribution services for JCB and is the holding company of CIML. |

4 Jun 2026 - Global smaller companies: When everyone owns the same names, what next?

|

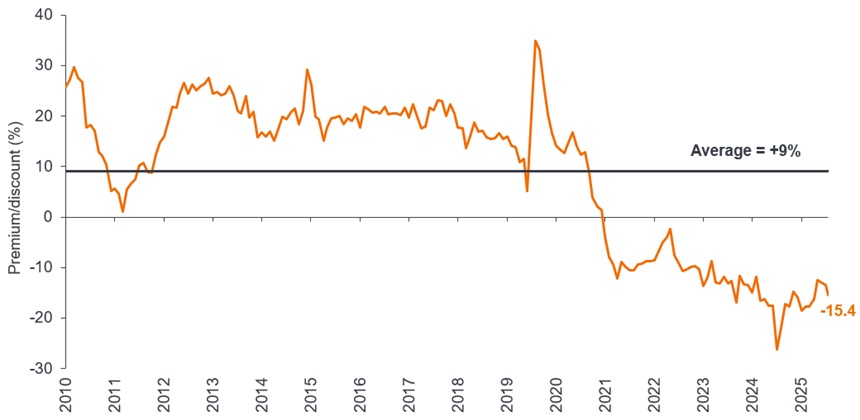

Global smaller companies: When everyone owns the same names, what next? Janus Henderson Investors May 2026 (8-minute read) Portfolio Manager Nick Sheridan explores why shifting market leadership, geopolitical uncertainty, and changing investor behaviour are bringing smaller companies back into focus, offering a broader set of opportunities beyond the most crowded trades. Markets started 2026 on an uncertain footing, pulled in different directions by geopolitical instability. The conflict in the Middle East, which began at the end of February, brought energy markets back into stark focus. Blocked supplies through the Strait of Hormuz pushed oil prices higher and raised fresh concerns about inflation just as central banks were attempting to stabilise growth. For investors, this has created a challenging mix of risks and uncertainties. Risk appetite has weakened as attention has become fixed on the conflict and its implications. Meanwhile, expectations for fiscal and monetary policies have shifted. Higher energy prices have complicated the outlook for interest rates. The uncertainty of government policy announcements via social has led to rapid swings in sentiment. The path to a lasting resolution remains obscured. Despite this backdrop, one notable feature of recent market behaviour has been the resilience of global smaller companies. This is typically the part of the market that struggles when uncertainty is elevated and policy is restrictive. In our view, this reflects modest starting valuations, positive earnings expectations, and a gradual shift in how investors are approaching markets. But even periods of tentative improvement in sentiment have seen investors look beyond the most heavily owned areas, suggesting that attention is no longer as narrowly focused as it once was. A turning point for market concentration Over the past decade, market returns have been dominated by a small group of large-cap technology companies (ie. the 'Magnificent 7' - Apple, Microsoft, Alphabet, Amazon, Meta, Nvidia and Tesla). At the same time, higher interest rates, macro uncertainty, and a preference for liquidity has favoured larger, more resilient businesses. Combined with passive flows, this has created an increasingly concentrated market, turning investor allocations into a tacit call on technology stocks. What appears to be changing is not a sudden reversal but a gradual broadening of leadership. The focus is shifting from owning what has worked to reassessing where future returns may come from. It has been driven by a subtle change in behaviour, with investors showing greater sensitivity to valuation, a more questioning approach to crowded trades, and growing awareness of how concentrated portfolios have become, particularly at a time of heightened geopolitical uncertainty. The dominance of the largest companies has not disappeared, but it is no longer unquestioned. Artificial intelligence remains a powerful structural theme, yet investors are starting to look beyond the most obvious beneficiaries, to smaller companies exposed to adjacent areas of growth. At the same time, the earnings picture for smaller companies is improving. Combined with more modest starting valuations relative to global large caps (Exhibit 1), we believe it supports the conditions for a re-rating, even in an uneven market. Exhibit 1: Attractive valuations of global small caps relative to large caps

Source: Bloomberg, Janus Henderson Investors Analysis, as at 9 April 2026. Shows global small cap premium/discount versus global large caps (forward P/Es). Different regions, different strengths Much like their larger counterparts, global smaller companies provide exposure to a diverse set of local economies and sector opportunities. Unlike large multinationals, however, they tend to be more closely tied to domestic or regional growth, which can be an advantage in a more fragmented geopolitical environment. They also tend to be more entrepreneurial and agile, often driving advances within specialised niches, rather than at scale. Another defining feature is how little attention they receive. Smaller companies are typically under-owned and under-researched, with materially less coverage from stock analysts. A combination of less scrutiny and more varied outcomes creates opportunity for active investors taking a selective approach. Particularly so, given how strong earnings forecasts are for smaller companies relative to their large-cap peers[1]. But there are also important differences across regions, offering built-in diversification within the small-cap category. In the US, deep capital markets and a strong culture of innovation support a broad pipeline of companies across technology, healthcare, and specialised industrials. In Europe, the market is more weighted towards industrials, manufacturing, and niche export-led businesses. Many of these have strong technical expertise and pricing power, alongside tailwinds from defence and infrastructure spending. Japan offers another distinct profile, characterised by high-quality industrial and technology businesses. Improving corporate governance and a greater focus on shareholder returns are helping to unlock value in companies that have historically been overlooked. Market inefficiency equals opportunity for active investors Global smaller companies remain one of the few areas of genuine inefficiency in equity markets. Limited analyst coverage and the diversity of the opportunity set mean there is real scope to add value through detailed research and engagement. This increases the value of information in the small cap space, given that outcomes in smaller companies are driven more by stock-level factors than by broad market movements. Sector and stock dispersion is wide, meaning the gap between winners and losers can be significant. This makes a research-led, data-driven approach essential, with a focus on characteristics such as return on equity, balance sheet strength, and the sustainability of earnings. For investors willing to take a longer-term view, this part of the market offers exposure to businesses earlier in their growth journey. After all, many of today's dominant companies, such as Nvidia, began as small caps. This is not to overlook the risks; smaller companies can be more volatile and more sensitive to economic cycles. Navigating these risks requires a disciplined, structured approach to stock selection. Overall, we believe that global smaller companies continue to offer a compelling opportunity set. In a market long dominated by a narrow group of large-cap stocks, they provide diversification, exposure to innovation, and access to domestic growth trends across regions. The macro environment remains uncertain. However, for investors focused on fundamentals, the breadth of opportunities within global smaller companies remains significant. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned. [1] Source: Bloomberg, Janus Henderson Investors, as at 9 April 2026. There is no guarantee that past trends will continue, or forecasts will be realised. Past performance does not predict future returns. Active investing: An investment management approach where a fund manager actively aims to outperform or beat a specific index or benchmark through research, analysis, and the investment choices they make. Asset allocation: The allocation of a portfolio between different asset classes, sectors, geographical regions, or types of security to meet specific objectives of risk, performance, or time horizon. Balance sheet: A financial statement that summarises a company's assets, liabilities, and shareholders' equity at a particular point in time. Each segment gives investors an idea as to what the company owns and owes, as well as the amount invested by shareholders. Diversification: A way of spreading risk by mixing different types of assets or asset classes in a portfolio on the assumption that these assets will behave differently in any given scenario. Assets with low correlation should provide the most diversification. Inflation: The rate at which the prices of goods and services are rising in an economy. The consumer price index (CPI) and retail price index (RPI) are two common measures. Interest rates: The amount charged for borrowing money, shown as a percentage of the amount owed. Base interest rates (the Bank Rate) are generally set by central banks, such as the Federal Reserve in the US or Bank of England in the UK, and influence the interest rates that lenders charge to access their own lending or saving. Liquidity: A measure of how easily an asset can be bought or sold in the market. Assets that can be easily traded in the market in high volumes (without causing a major price move) are referred to as 'liquid'. Premium: When the market price of a security is thought to be more than its underlying value, it is said to be 'trading at a premium'. Return on equity (ROE): A company's net income (income minus expenses and taxes) over a specified period, divided by the amount of money its shareholders have invested. It is used as a measurement of a company's profitability compared to its peers. A higher ROE generally indicates that a management team is more efficient at generating a return from investment. Returns/return: The total return of a portfolio over a specified period as opposed to its relative return against a benchmark. It is measured as a gain or a loss and stated as a percentage of a portfolio's total value. |

|

Funds operated by this manager: Janus Henderson Australian Fixed Interest Fund , Janus Henderson Conservative Fixed Interest Fund , Janus Henderson Diversified Credit Fund , Janus Henderson Global Natural Resources Fund , Janus Henderson Tactical Income Fund , Janus Henderson Australian Fixed Interest Fund - Institutional , Janus Henderson Conservative Fixed Interest Fund - Institutional , Janus Henderson Cash Fund - Institutional , Janus Henderson Global Multi-Strategy Fund , Janus Henderson Global Sustainable Equity Fund , Janus Henderson Sustainable Credit Fund All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect. The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested. Whilst Janus Henderson believe that the information is correct at the date of publication, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson to any end users for any action taken on the basis of this information. |

3 Jun 2026 - Future Supply Chains ETF: reflecting on one year

|

Future Supply Chains ETF: reflecting on one year abrdn May 2026 (Duration: 7 Mins) Our two thematic future exchange-traded funds (ETFs) - raw materials and supply chains - have just turned one. To mark the anniversary, we sat down with Blair Couper and Jamie Mills O'Brien, investment directors of our Future Supply Chains ETF. They reflected on what they've learned over the past year, how the strategy has evolved, and why they believe the case for resilient supply chains looks stronger than ever. Q1. The Future Supply Chains ETF launched just over a year ago. Take us back to that moment - what was the original thinking behind launching the strategy?Blair Couper: A lot of it came down to what we were seeing in the real world. We think the next 10 years are likely to be characterised by lower growth and stickier inflation than the last decade, driven by the inexorable forces of demographics, debt and deglobalisation. Against this backdrop, we wanted to position our investors behind growth trends that can thrive even in a weaker macro environment. The changing nature of supply chains - and the structural forces underpinning them - was one such area. Supply chains have gone from being something investors barely thought about to something that suddenly mattered every day - whether it was because of shortages, delays, or geopolitical tension. We felt that wasn't a short�'term disruption, but the start of a much bigger, longer�'lasting shift. The fund was really about giving investors a way to access that change in a considered, long�'term way, rather than reacting to the latest headline. Q2. "Supply chains" can mean a lot of different things. How do you define future supply chains when you're thinking about it as an investment opportunity?Jamie Mills O'Brien: That's exactly the opportunity - one that touches so many parts of global markets. For us, future supply chains aren't just about moving goods from A to B. They're about how countries, companies and industries are rethinking where things are made, how secure they are, and how sustainable they need to be. In that sense, it represents a broad reshaping of the global economy, spanning technology, energy, manufacturing, and infrastructure. A good example is defence and reindustrialisation (two themes we favour). After more than 20 years of underinvestment in its capital stock, the US is leaning far more heavily on its treaty allies in the Indo-Pacific, particularly Korea and Japan, to help bridge the gap with China across defence and automation. The unifying idea here is adaptation: states and companies responding to a world that's becoming more fragmented and certainly more challenging. Q3. Why did you decide an ETF - and an actively managed one at that - was the right structure for this idea?Jamie Mills O'Brien: An ETF gives investors transparency, flexibility and ease of access, which we think really suits a thematic allocation. But we were equally clear that this couldn't just be rules�'based or static. Supply chains are evolving all the time, so active management allows us to adjust exposures, lean into areas we believe are gaining momentum, and step back when conditions change. It's about keeping the strategy relevant - and an active approach allows us to do that. Q4. The strategy is built around three key drivers: national security, resilient supply chains, and decarbonisation. How did those pillars emerge?Blair Couper: They really came out of looking at what's driving decision�'making at government and corporate level. National security has become central to economic policy. Resilience is about reducing vulnerability and disruption. And decarbonisation is reshaping how energy and infrastructure are built. These forces overlap and reinforce one another. We saw them less as separate themes and more as different angles on the same structural shift. Q5. Automation, reshoring and localisation are big themes globally. How do you avoid simply chasing the loudest trends or headlines?Jamie Mills O'Brien: It comes back to discipline. At the heart of our thematic process is a focus on identifying those themes - and, within them, those companies - that can create value from the most powerful structural growth trends shaping the global economy. As a result, we spend a lot of time focusing on business quality and long�'term fundamentals. At the same time, we are wary of areas where narrative and hype are driving enthusiasm, rather than company fundamentals. A company benefiting from reshoring or rising defence spending still needs a robust balance sheet, strong competitive positioning and a business model that supports attractive economics. Being aligned with the theme gets a company onto the radar - but it doesn't automatically earn it a place in the portfolio. Q6. One year on, what have you learned since launch? Have any aspects of the strategy evolved as markets - and geopolitics - have shifted?Blair Couper: If anything, the past year has reinforced our original thinking. The scale of policy intervention, defence spending and industrial support has been striking. At the same time, we've learned the importance of flexibility - some developments move faster than expected, others take time. The framework hasn't changed, but our understanding of how and when value emerges has definitely deepened. Q7. Supply chains feel even more prominent in today's headlines than they did a year ago. Why do you think they've become more relevant, not less?Blair Couper: Recent events have shown that the underlying pressures haven't gone away - they've intensified. Geopolitical uncertainty, energy security concerns and trade tensions are now structural features of the global economy. We're seeing the last 50 years of globalisation give way to a world shaped by competing spheres of influence, fragmenting across China, the US and Europe. Governments are actively encouraging domestic production and demand, and companies are responding. In this world supply chains remain front and centre - not just as an operational issue, but as a strategic one. Q8. For investors thinking about portfolio construction, how does a supply�'chain strategy sit alongside traditional global equity exposure?Jamie Mills O'Brien: We see it as a complement rather than a replacement. Traditional indices reflect where the world has been; thematic strategies are about where it's going. Supply chains touch many sectors and regions, but they're driven by different forces than broad market cycles. That can make them a useful diversifier for investors who are looking to build resilience into their portfolios. Q9. What type of companies tend to stand out when supply chains are being redesigned rather than simply maintained?Jamie Mills O'Brien: Often, it's companies enabling change rather than resisting it. That might be firms providing automation, infrastructure, energy solutions or specialist components. What they tend to share is an ability to adapt - they're helping others become more efficient, more secure or more sustainable, rather than clinging to older models. Q10. Finally, if you had to sum up what the Future Supply Chains ETF is really about, how would you describe it?Blair Couper: At its heart, it's about investing in how the global economy is being rebuilt. Supply chains are no longer just about cost efficiency - they're about security, resilience and long�'term sustainability. This strategy is designed to capture that transformation as it unfolds.

Fund-specific risks The fund invests in equity and equity related securities. These are sensitive to variations in the stock markets which can be volatile and change substantially in short periods of time. A concentrated portfolio may be more volatile and less liquid than a more broadly diversified one. The fund's investments are concentrated in a particular country or sector, or closely related group of industries or sectors. The fund invests in emerging market equities and / or bonds. Investing in emerging markets involves a greater risk of loss than investing in more developed markets due to, among other factors, greater political, tax, economic, foreign exchange, liquidity and regulatory risks. The shares of small and mid-cap companies may be less liquid and more volatile than those of larger companies. The fund may invest in companies with Variable Interest Entity (VIE) structures in order to gain exposure to industries with foreign ownership restrictions. There is a risk that investments in these structures may be adversely affected by changes in the legal and regulatory framework. Investing in China A shares involves special considerations and risks, including greater price volatility, a less developed regulatory and legal framework, exchange rate risk/controls, settlement, tax, quota, liquidity and regulatory risks. The use of derivatives carries the risk of reduced liquidity, substantial loss and increased volatility in adverse market conditions, such as a failure amongst market participants. The use of derivatives may result in the fund being leveraged (where market exposure and thus the potential for loss by the fund exceeds the amount it has invested) and in these market conditions the effect of leverage will be to magnify losses. |

|

Funds operated by this manager: abrdn Sustainable Asian Opportunities Fund , abrdn Emerging Markets Equity Fund , abrdn Sustainable International Equities Fund , abrdn Global Corporate Bond Fund (Class A) |

1 Jun 2026 - Manager Insights | Digital Asset Funds Management

|

Chris Gosselin, CEO of FundMonitors.com, speaks with Clint Maddock, Director and Co-Founder at Digital Asset Funds Management. Clint discussed how the fund has remained profitable despite Bitcoin's recent decline, highlighting its market-neutral arbitrage strategy across multiple digital asset exchanges. He also shares his outlook on crypto market catalysts, including regulatory developments in the US, and the fund's growth following its distribution partnership with Montgomery Funds Management.

|