NEWS

1 Nov 2024 - Hedge Clippings | 01 November 2024

|

|

|

|

Hedge Clippings | 01 November 2024 The RBA finds itself in a bind yet again. Inflation has eased somewhat, with the September quarter number just 0.2%, or 2.8% annually, down from 3.8% in the June quarter, and taking it to a 3.5-year low. However, it's still running hot enough to make the RBA think twice about cutting rates. When the cash rate decision is announced next week, most experts are expecting rates to stay steady, much to the dismay of borrowers hoping for a bit of early festive cheer, and the Treasurer Jim Chalmers, desperate to claim the credit and hopefully another three years in office come election time next year. The RBA won't be fooled either by the overall number, or Jim Chalmers desire to claim "mission accomplished" George Bush style. Prices for most goods and services rose, offset by large falls for electricity and fuel. The trimmed mean number, which excludes both, was still 3.5%, albeit below June's 4.0 percent. Only government spending is keeping the economy in positive territory, and it's only government handouts that are seriously impacting inflation - for the present. Despite the overall figure, prices of essential items like rent, childcare, and insurance have kept upward pressure on households, with many services demonstrating a particularly stubborn streak. The RBA wants to keep inflation under control without being seen as stifling economic growth, but it's no easy feat. With inflation hovering in a state of "not dead yet," the central bank is likely to maintain its cautious approach. The possibility of a rate cut before year-end remains slim, and if that's the case, borrowers, and the Treasurer, will have to wait until February for any hope of a reprieve. Meanwhile if you hadn't noticed, the United States is gearing up for Election Day next week, with seemingly the rest of the world mesmerised by the spectacle, confused by the process, and concerned about the outcome. From where we sit, it's been a bizarre lead up, with Biden slipping up (literally) and then stepping down, Trump as popular as ever among the MAGA set, in spite of - or maybe because of - multiple indiscretions and crass behaviour or reminiscences from the golf club locker room. We have no idea based on the dead heat polls, but suggest voter turnout is expected to be the key factor when the dust settles (assuming it does). Historically, US voter turnout has fluctuated between just over 50% and 62.8% over the past six presidential elections. However it is unlikely to be the overall voter turnout that will determine the result: Most states are already won or lost, thanks to the winner take all approach by every state except Maine and Nebraska, leaving the result hinged on a handful of votes in the battleground or swing states. But given the personalities and issues at play, it's not the overall turnout that will determine the result. How big a part will Roe vs. Wade play? Or the situation in Gaza, Lebanon, and Israel? And even more recently, to what extent might the Hispanic turnout sway the result? For financial markets and global stability, the stakes are high, and the outcome will not only determine the next leader but also affect the ability to govern effectively, given the divided state of US politics. Questions surrounding inflation, federal debt, and the broader economic outlook have only added to the uncertainty. Yet amazingly, the result may come down to some little known, so-called comedian's off joke. Closer to home, in political news, Prime Minister Anthony Albanese has been hitting some turbulence (apologies for the pun) following claims that he sought free upgrades from Qantas. The story, which began with whispers, has escalated to full-blown denials, with frontbenchers clarifying that Albanese did not make any requests by phone, email, or any other means of communication. The whole affair has probably been blown out of all proportion - of course airlines upgrade politicians, and Qantas made an art form of it to curry political favour. The issue is not the upgrades or perks that are handed out - it is what influence is sought or exerted in return. In this case, what input did Albo or Albo's office have on the government's decision to block Qatar Airways application for an additional 28 flights a week into major Australian airports? A decision that massively benefited Qantas' traffic, passenger loads, market dominance and profitability, at the expense of the Australian traveling public. Alan Joyce's greed and arrogance eventually cost both he and his chairman their jobs. Might it also claim his old mate Albo's come election time? News & Insights New Funds on FundMonitors.com Magellan Global Quarterly Update | Magellan Asset Management Market Update | Australian Secure Capital Fund September 2024 Performance News TAMIM Fund: Global High Conviction Unit Class Insync Global Quality Equity Fund |

|

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday |

1 Nov 2024 - Performance Report: PURE Resources Fund

[Current Manager Report if available]

1 Nov 2024 - Performance Report: PURE Income & Growth Fund

[Current Manager Report if available]

1 Nov 2024 - Australian Secure Capital Fund - Market Update

|

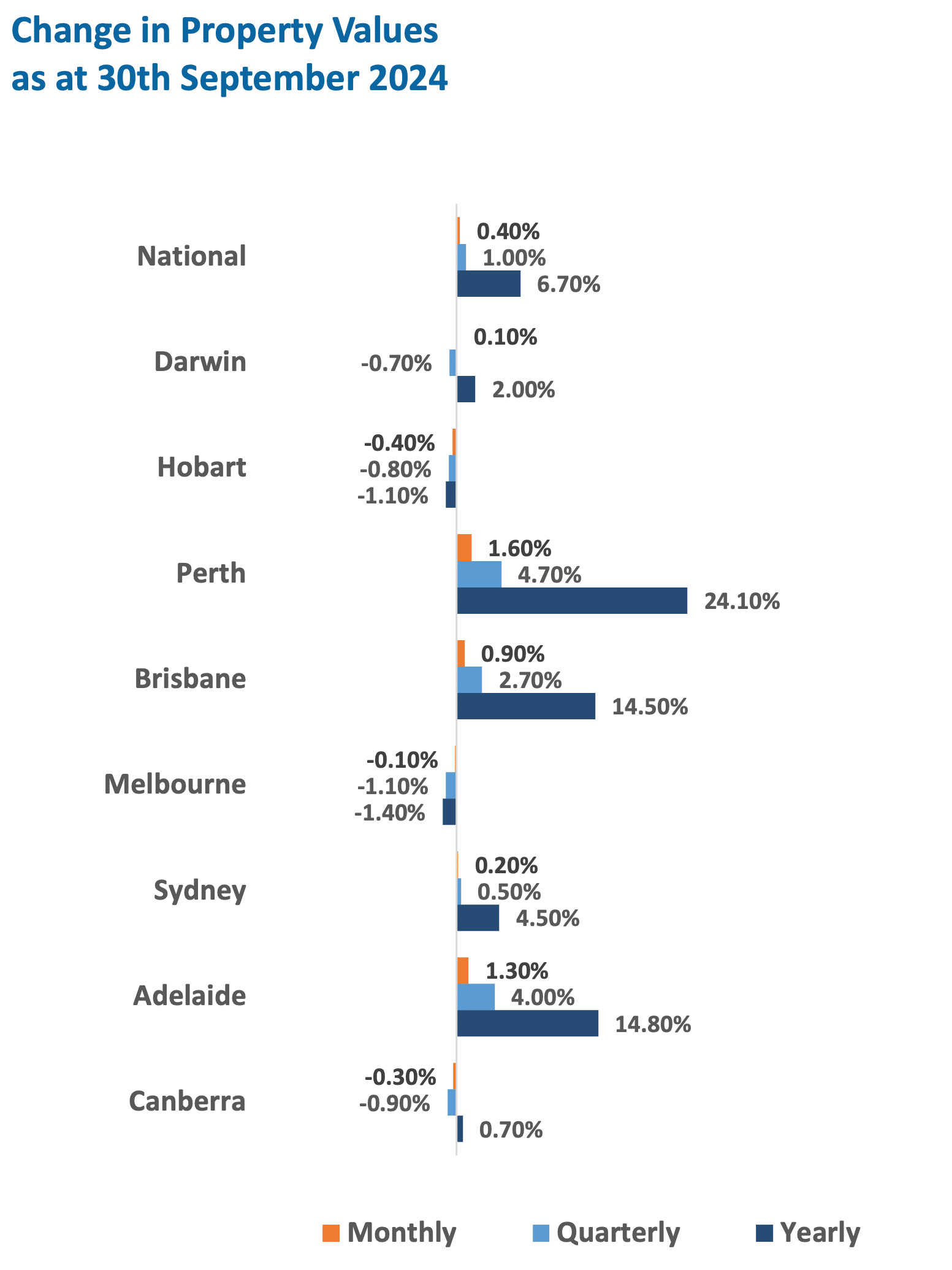

Australian Secure Capital Fund - Market Update Australian Secure Capital Fund October 2024 For the 20th consecutive month, headline national home values increased by a modest 0.4%, signalling that the strong momentum is beginning to leave the market. This is demonstrated by housing values rising just 1% for the September quarter, the lowest over a rolling three-month period since March 2023. Perth continues to be the strongest performer, growing by 1.6% for the month, followed by Adelaide and Brisbane with increases of 1.3% and 0.9%, respectively. Sydney and Darwin were the only other markets to see increases, rising by 0.2% and 0.1% for the month, while Melbourne, Canberra, and Hobart all saw housing values ease, with decreases of 0.1%, 0.3%, and 0.4%, respectively. Property Values as at 30th of September 2024

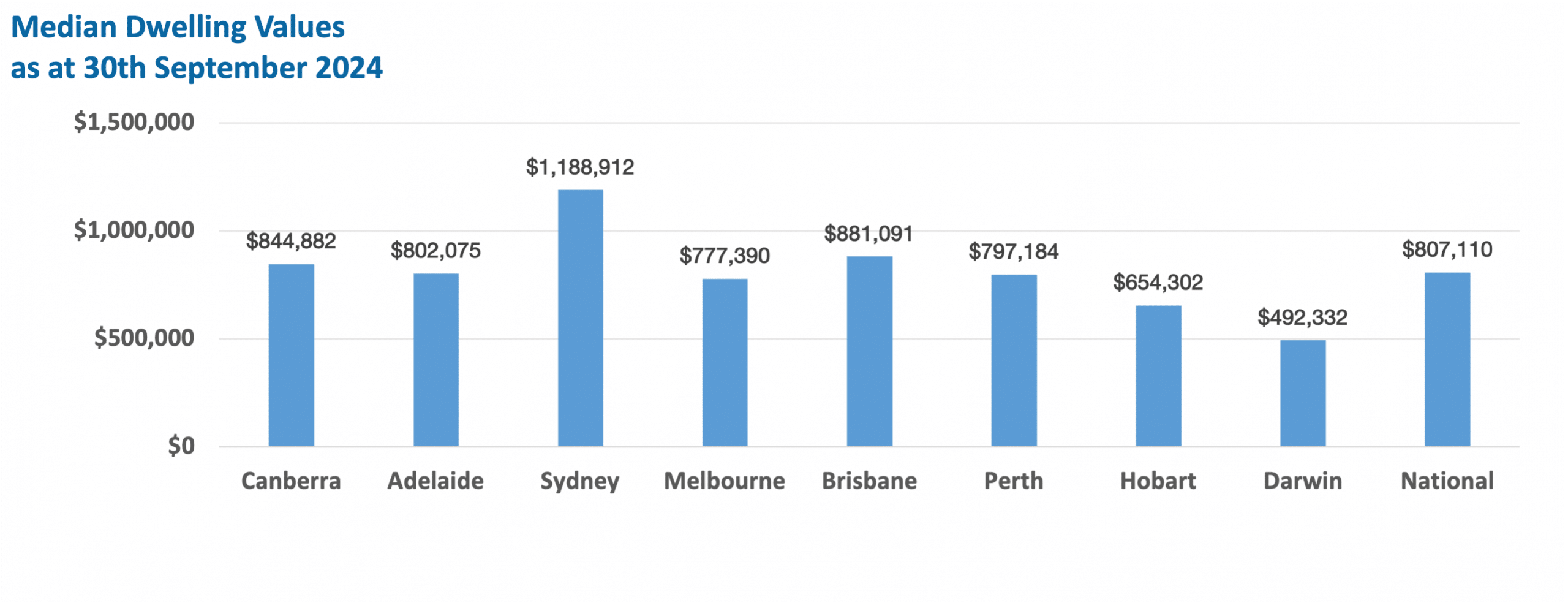

Median Dwelling Values as at 30th of September 2024

Quick InsightsRate hold slows buyers, but investor confidence remains strongProfits from home sales nationwide climbed to a record high of $285,000 on average in the June quarter. The RBA's decision to keep interest rates steady has left many homebuyers waiting, as borrowing power remains limited. While a future rate cut is anticipated, it won't significantly boost demand until it happens. Meanwhile, investors are showing renewed interest, particularly in Melbourne, where the market is stabilising despite an increase in listings. A rate cut could lead to a faster recovery than expected. Source: Australian Financial Review

Australia's housing market soars to record $11 trillionAustralia's housing market hit a record $11 trillion in September, with home values rising 6.7% over the past year, adding $900 billion in wealth. Despite higher interest rates, new listings and strong investor activity continue to drive the market. Over the past decade, house prices surged by 85.9% nationwide, with suburbs in Sydney, Brisbane, and Melbourne leading long-term growth. While price growth is expected to slow, strong demand and new housing developments will continue to support the market. Source: Australian Financial Review Author: Filippo Sciacca, Director - Investor Relations, Asset Management and Compliance Funds operated by this manager: ASCF High Yield Fund, ASCF Premium Capital Fund, ASCF Select Income Fund |

31 Oct 2024 - Go beyond the point of low returns

30 Oct 2024 - Performance Report: Insync Global Capital Aware Fund

[Current Manager Report if available]

30 Oct 2024 - Stock Story: Medibank

|

Stock Story: Medibank Airlie Funds Management October 2024 |

|

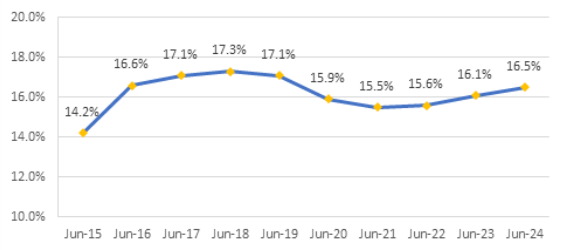

Playing a pivotal role in Australia's health transition. The Medibank and ahm private health insurance brands serve over 4.2m customers and play a vital role in funding medical care in Australia. In the most recent financial year, Medibank paid out $6.3bn in health insurance claims, taking a significant burden off the public healthcare system. Yet recently, the sector has come under fire from both the government and hospitals accused of making too much profit. In this article, we explore this regulatory tension and why we think Medibank looks an attractive investment opportunity. Private hospital profits affected by new models of careThere is no doubt the past few years have been challenging for hospitals - labour shortages have affected service levels and inflation has been rampant. Private hospital operators have responded by launching a campaign against the health insurers and pressuring the government for a bailout. While additional payments or a tax may provide short-term relief to hospitals, they do not solve the structural issues facing the sector and ultimately would drive up the cost of healthcare and premiums for millions of Australians. To build a sustainable private healthcare system, all participants must work together to find efficiencies and drive down the overall cost of care. Medibank is doing its part to lower costs by investing in new models of care away from overnight stays in expensive acute care hospitals to virtual, short-stay hospitals and home care. Without this transition, Medibank estimates the government will need to spend 50% more on healthcare as a percentage of GDP in forty years. While this transition does come at the expense of hospitals that typically earn more for longer in-hospital stays, it is beneficial for the wider healthcare system. Higher hospital costs would simply translate to higher premiums, which are likely to push more members out of private health insurance and place further strain on an already stretched public healthcare system. It is for this reason the Federal Health Minister following a review has conceded, "There's no silver bullet from Canberra or funding solution from taxpayers to deal with what are essentially private pressures in the system". Ultimately, it is not the government's job to prop up unprofitable business models and in some cases it is healthy for some private hospitals to shut where there is overcapacity in the system. Has Medibank profited at the expense of hospitals? Medibank has stuck to its promise not to profit from the pandemic and returned a total of $1.46bn in givebacks to customers for permanent claims savings due to COVID-19. This is evident in the chart below which shows Medibank's health insurance gross profit margin is still below FY19 levels.

Source: Company filings

|

29 Oct 2024 - Performance Report: TAMIM Fund: Global High Conviction Unit Class

[Current Manager Report if available]

29 Oct 2024 - Performance Report: Insync Global Quality Equity Fund

[Current Manager Report if available]

29 Oct 2024 - Magellan Global Quarterly Update

|

Magellan Global Quarterly Update Magellan Asset Management October 2024 |

|

Arvid Streimann, Nikki Thomas and Alan Pullen discuss key market themes and how the global strategy is positioned to capitalise on emerging opportunities, whilst monitoring the risks. Arvid also discusses the potential market impacts of the upcoming US election based on various possible outcomes. |

|

Funds operated by this manager: Magellan Global Fund (Hedged), Magellan Global Fund (Open Class Units) ASX:MGOC, Magellan High Conviction Fund, Magellan Infrastructure Fund, Magellan Infrastructure Fund (Unhedged), MFG Core Infrastructure Fund, Magellan Core ESG Fund Important Information: Important Information: This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 ('Magellan') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision about whether to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to a Magellan financial product may be obtained by calling +61 2 9235 4888 or by visiting www.magellangroup.com.au. Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of a Magellan financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. Magellan makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Magellan. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. No representation or warranty is made with respect to the accuracy or completeness of any of the information contained in this material. Magellan will not be responsible or liable for any losses arising from your use or reliance upon any part of the information contained in this material. Any third party trademarks contained herein are the property of their respective owners and Magellan claims no ownership in, nor any affiliation with, such trademarks. Any third party trademarks that appear in this material are used for information purposes and only to identify the company names or brands of their respective owners. No affiliation, sponsorship or endorsement should be inferred from the use of these trademarks. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Magellan. |