NEWS

9 May 2025 - Performance Report: Bennelong Long Short Equity Fund

[Current Manager Report if available]

9 May 2025 - Performance Report: Bennelong Australian Equities Fund

[Current Manager Report if available]

9 May 2025 - Are You In The Matrix?

|

Are You In The Matrix? Marcus Today April 2025 |

|

Have you been told to "buy and hold"? "It'll be fine in the long run"? "You can't time the market"? You might be in the matrix. In this video, Marcus breaks down the truth behind the mantras the finance industry repeats - not to help you, but to keep you quiet. If you've ever felt like the advice doesn't quite match reality... you're not alone. DISCLAIMER: This content is for general information purposes only and does not constitute personal financial advice. Please consider your own circumstances or seek professional advice before making investment decisions. |

|

Funds operated by this manager: |

7 May 2025 - Sustainability: Is this the end for sustainable investing?

|

Sustainability: Is this the end for sustainable investing? abrdn April 2025 This is a crucial year for sustainable investing. With a heady mix of regulatory change, political backlash and changing sentiment, we ask whether it's over for sustainable investment? Investors who have set interim climate targets for 2030 have less than five years to achieve them. But even with an increase in the regularity and severity of extreme weather events, many investors have faced a political backlash against climate change and sustainable investing. These developments have accelerated in recent months with a drastic shift in the US political climate. This has led to big-name US asset managers and companies abandoning climate commitments and rushing to roll back on diversity, equity and inclusion (DEI) pledges. But behind the headlines, we see a more nuanced evolution of the sustainable investing world - one in which demand for sustainability strategies remains strong. This is being driven by institutional investors demanding bespoke solutions to meet specific goals and these asset owners are backing up their talk with action. Transatlantic splitThe US and Europe are heading in opposite directions. Political pressures have led to a retreat from sustainable investment in the US, while Europe largely remains committed. President Donald Trump plans to dismantle the previous US administration's measures to promote sustainability and wants to increase coal, oil and gas exploration on federal land - his recent executive orders demonstrating his intent. He has weakened the Environmental Protection Agency and pulled the US out of the Paris climate agreement. Some US asset managers, facing legal challenges, have turned their backs on climate targets and withdrawn from international climate initiatives, such as the Net Zero Asset Managers and the Climate Action 100+ initiatives. But across the Atlantic, it's almost business as usual for a region that has long been at the vanguard of international efforts to promote sustainability and sustainable investing. Last December, regulators there started applying the European Union's (EU) Green Bonds regulation. These rules aim to clarify eligibility criteria on what qualifies in the EU as a 'green bond'. The goal is to improve investor protection by preventing 'greenwashing'. It's not all plain sailing even in the EU. In a bid to boost competitiveness, Europe's Omnibus package rolls back flagship sustainable investment policies including the Corporate Sustainability Reporting Directive and the Corporate Sustainability Due Diligence Directive, amid proposals to dilute the region's Sustainable Finance Disclosure Regulation. This divergence in philosophy amid pressures to weaken existing measures complicate global operations for asset managers and asset owners alike. It is simply no longer possible to operate with a one-size-fits-all approach. Big investors lead the wayThat said, many institutional investors continue to demand sustainable investing strategies. This isn't always obvious, but it is a critical component of the current investment landscape. In February, a group of 27 asset owners - primarily from the UK but also representing European, Australian and US investors - signed the 'Asset Owner Statement on Climate Stewardship' to reinforce their support for sustainability principles and to spell out what they expect from fund managers. There is growing demand for tailored investment solutions. While these are predominantly focused on asset owners looking to meet their climate targets, there is also interest in deploying strategies to protect natural environments in bespoke, or 'segregated', mandates. In our own assets under management, those we classify as 'sustainable' investments, grew to £87 billion (US$112.4 billion) by end-2024 from £55 billion a year earlier. This increase was largely attributable to segregated sustainable investment mandates. We are also seeing cases in which asset managers who turn away from sustainability goals may be punished by some asset owners. For example, both the UK's People's Pension and Denmark's Akademiker Pension pulled mandates from one US fund manager amid disagreements over climate stewardship. DEI requires diverse solutionsCompanies employ DEI policies for reasons including employee wellbeing, legal compliance and enhancing brand image. But critics equate DEI with the prioritisation of identity over competence. Many US companies have been diluting or scrapping their DEI policies in response to Trump's executive order on DEI and to avoid litigation. DEI-related quotas and affirmative-action programs have been under particular scrutiny. Opponents say they are discriminatory and that employees hired through these initiatives have not been chosen on merit. Some firms have removed gender quotas on boards, for example. The response from asset managers has been mixed amid a growing number of DEI cases going to court. While some have gone quiet on DEI, other fund managers continue to engage with companies and deepen long-term relationships to drive improvements in this area. The changes companies are making with regards to DEI, as a result of navigating new pressures and expectations, is yet another facet of the evolving nature of sustainability investing in a complex world. Final thoughtsMany recent headlines have painted a grim picture for sustainable investing, with phrases like 'sustainability in crisis' making the rounds. There's no doubt that the honeymoon for sustainable investing is over. However, a closer look reveals a more nuanced story. A hostile political environment in the US makes it more difficult to follow sustainable investment principles there. However, the demand for sustainability strategies remains strong, especially from institutional investors who remain committed to achieving sustainability targets and need customised investment solutions. Once the marketing hype is stripped away, sustainable investing has always been fundamentally about financially-material issues. These issues continue to be critical regardless of the political whims of the day. This is why asset owners, as long-term investors, remain committed. This is why there are opportunities for those investors who can navigate this complex landscape. Sustainable investment is not dead - it is reforming and evolving to meet the demands of a changing world. It took over 100 years to secure agreement on globally-accepted accounting principles. We are trying to achieve the same thing with less time and as the world gets hotter each year. Is it any wonder there are a few bumps along the road? |

|

Funds operated by this manager: abrdn Sustainable Asian Opportunities Fund, abrdn Emerging Opportunities Fund, abrdn Global Corporate Bond Fund (Class A), abrdn International Equity Fund, abrdn Multi-Asset Income Fund, abrdn Multi-Asset Real Return Fund, abrdn Sustainable International Equities Fund |

7 May 2025 - Tim Hext: Art of the deal or new world order?

|

Tim Hext: Art of the deal or new world order? Pendal April 2025 |

|

PRESIDENT TRUMP's "reciprocal" tariffs caught many - me included - by surprise last week. Until then, I mistakenly believed tariffs were all part of the art of the deal. Tariff talk, which was seen as a tactical ploy to get a better deal for the US, suddenly seemed to have larger ideological aims. How else can you explain the ridiculous calculation method for reciprocal tariffs? There is still a lot of water to go under the bridge in the weeks and months ahead as negotiations go bilateral - but understanding Trump (always a difficult exercise) will help navigate markets. When China entered the World Trade Organisation in 2001, the US trade deficit with China was $84 billion. The US had a $300 billion deficit overall in manufacturing. Over next two decades, the manufacturing deficit grew $1 trillion to $1.3 trillion by 2022. China accounted for almost $600 billion of this growth. Overall, this was seen as a win/win. China got to develop on the back of hard work and exporting to the US. And US consumers got plenty of cheap goods from China, protecting a standard of living in the face of slow wage growth. The bonus for the US was that in an attempt to keep its currency lower, the Chinese government bought US dollars and became huge buyers of US Treasuries. Its FX reserves went from $300 billion to over $3 trillion during this period. Let's not forget the most important thing: since 2000, around 500 million Chinese people have emerged from poverty to middle incomes. By 2018, however, geopolitics started to kick in. As China started to flex its muscle globally, not all in the US were happy. The narrative began to change. In his first term, Trump launched a trade war with China, causing negative equity returns. Helping the Chinese economy was now seen as a negative, not a positive. That trade war now seems tame. It seems the narrative from Trump is effectively that the US can handle some pain if it means achieving a longer-term new world order. The US will retreat back to some supposed golden age. Time will tell. Implications for bond marketsAs evidenced this week, all these actions from Trump are a mixed bag for US bonds. Firstly, economic weakness should mean Fed cuts and rallies in bonds. However, tariffs will mean higher inflation - at least near term. Throwing more confusion into the picture is foreign buying (or more likely selling) of US bonds. Smaller trade deficits mean smaller capital surpluses and therefore, at best, smaller inflows into US capital markets. Where it gets more interesting, though, is the weaponisation of financial flows - not just trade flows. Rumours have been circling that China is dumping part of its US Treasury holdings. Other countries may follow - after all, like any investments, you want to know the CEO knows what they are doing, and simply put, credibility and confidence has evaporated. Who would want to lend money to an entity that is acting so aggressively against your interests? Therefore, the flight to quality is more of a flight to cash and short bonds, not long bonds. Yield curves are steepening faster than economic fundamentals suggest. It was only late last year when US exceptionalism became the investment theme for this decade. That exceptionalism remains but is quickly being redefined from a positive to a negative. Implications for our portfoliosWe have been leaning into duration for a number of months, but are very disappointed by the lack of a reaction from our long end. Short-end duration has worked, but unlike Covid and the GFC, the long end has been left behind. The RBA will also be cautious. The expected low CPI print on 30 April will give the central bank cover to cut at its 20 May meeting, but unless it keeps getting worse, its recent form suggests only a 25-basis-point (bps) cut. It will then adopt a wait-and-see approach for how it all impacts Australia. But given there are six weeks till then, markets are right to price some risk of a larger cut - though, current levels of 40bps of cuts looks a little too much. The random nature of announcements mean we are generally keeping risk close to home. Our caution around credit means we are avoiding the major drawdowns that will be hitting more aggressive investors. Now is not the time to charge in. However, we are still looking for relative value opportunities in a volatile market to keep adding value in these stressed times. LiquidityAnd just like that - liquidity in many sectors dries up in a puff of smoke. Our portfolios at Pendal Income and Fixed Interest have always operated at the more liquid end of markets. We leave the less-liquid, high-yield chasing to others. Government bonds remain highly liquid. Semi-government bonds are hanging in there though bid/offers are widening. You can transact senior bank paper assuming manageable size and paying a wider spread. However, as we have often warned, beyond there it gets very tricky. Everything is liquid in good times, but it is a shortlist in a time of crisis. The RBA sets the liquidity rules and its world is one of cash, bank bills/NCDs and government bonds (all known as High Quality Liquid Assets). These remain open for business, but beyond that point, it is buyer-beware for liquidity. Author: Tim Hext |

|

Funds operated by this manager: Pendal Global Select Fund - Class R, Pendal Horizon Sustainable Australian Share Fund, Pendal MicroCap Opportunities Fund, Pendal Multi-Asset Target Return Fund, Pendal Sustainable Australian Fixed Interest Fund - Class R, Pendal Sustainable Australian Share Fund, Regnan Credit Impact Trust Fund, Regnan Global Equity Impact Solutions Fund - Class R |

|

This information has been prepared by Pendal Fund Services Limited (PFSL) ABN 13 161 249 332, AFSL No 431426 and is current as at December 8, 2021. PFSL is the responsible entity and issuer of units in the Pendal Multi-Asset Target Return Fund (Fund) ARSN: 623 987 968. A product disclosure statement (PDS) is available for the Fund and can be obtained by calling 1300 346 821 or visiting www.pendalgroup.com. The Target Market Determination (TMD) for the Fund is available at www.pendalgroup.com/ddo. You should obtain and consider the PDS and the TMD before deciding whether to acquire, continue to hold or dispose of units in the Fund. An investment in the Fund or any of the funds referred to in this web page is subject to investment risk, including possible delays in repayment of withdrawal proceeds and loss of income and principal invested. This information is for general purposes only, should not be considered as a comprehensive statement on any matter and should not be relied upon as such. It has been prepared without taking into account any recipient's personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation. The information may contain material provided by third parties, is given in good faith and has been derived from sources believed to be accurate as at its issue date. While such material is published with necessary permission, and while all reasonable care has been taken to ensure that the information is complete and correct, to the maximum extent permitted by law neither PFSL nor any company in the Pendal group accepts any responsibility or liability for the accuracy or completeness of this information. Performance figures are calculated in accordance with the Financial Services Council (FSC) standards. Performance data (post-fee) assumes reinvestment of distributions and is calculated using exit prices, net of management costs. Performance data (pre-fee) is calculated by adding back management costs to the post-fee performance. Past performance is not a reliable indicator of future performance. Any projections are predictive only and should not be relied upon when making an investment decision or recommendation. Whilst we have used every effort to ensure that the assumptions on which the projections are based are reasonable, the projections may be based on incorrect assumptions or may not take into account known or unknown risks and uncertainties. The actual results may differ materially from these projections. For more information, please call Customer Relations on 1300 346 821 8am to 6pm (Sydney time) or visit our website www.pendalgroup.com |

6 May 2025 - Performance Report: Seed Funds Management Hybrid Income Fund

[Current Manager Report if available]

6 May 2025 - Glenmore Asset Management - Market Commentary

|

Market Commentary - March Glenmore Asset Management April 2025 Globally, equity markets fell sharply in March. In the US, the S&P 500 fell -5.8%, the Nasdaq declined -8.2%, whilst in the UK, the FTSE outperformed, falling just -2.6%. Relevant for the Glenmore Australian equities fund was the ASX small industrials accumulation index, which fell -6.7% in March. Gold stocks were the strongest performer on the ASX, boosted by a +10.6% increase in the gold price. Defensive sectors such as utilities, telco's and insurance also outperformed. Growth stocks (in particular technology stocks) fell sharply, due to investors adopting a "risk off" approach as well as growing concern about the rate of global economic growth. The catalyst for the negative returns in March was continued discussion around the US government introducing tariffs on various trading partners. The proposed tariffs and general uncertainty around US president Donald Trump's policy making resulted in investors becoming very cautious towards global economic growth and equities across all sectors. In addition, the tariffs imposed by the US have the potential to be inflationary in the short term, which could pose a new risk for investors. Bond markets were quite subdued during the month despite the equity markets volatility. In the US, the 10-year bond yield fell -3 basis points (bp) to 4.21%, whilst its Australian counterpart rose 9 bp to close at 4.39%. The Australian dollar was broadly unchanged over the month, closing at US$0.62. Our view is that the recent sell off over the last two months will likely prove to a good buying opportunity for investors willing to a take a medium-term view. As is typically the case in these market corrections, growth stocks and small/mid cap stocks were sold off very significantly, whilst large caps stocks outperformed given their safe haven status. The fund currently has a cash weighting of ~15%. As we have done in past periods, we have used this period of weakness to add to a number of stocks in the fund at attractive valuations. In addition, if global economic growth does slow materially over the course of 2025, we believe central banks will consider interest rate reductions, which would likely to be positively received by investment markets. Funds operated by this manager: |

5 May 2025 - 10k Words | April 2025

|

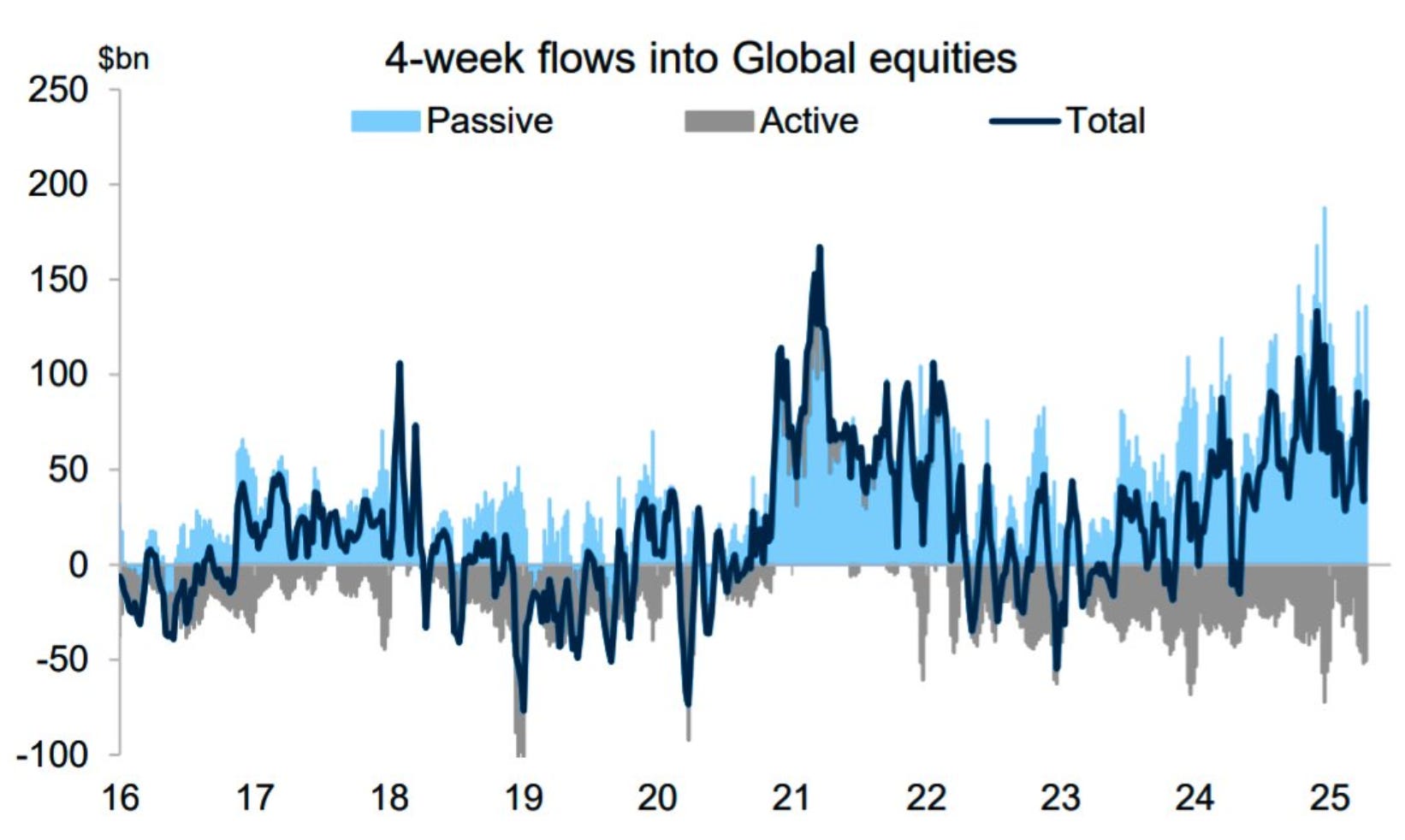

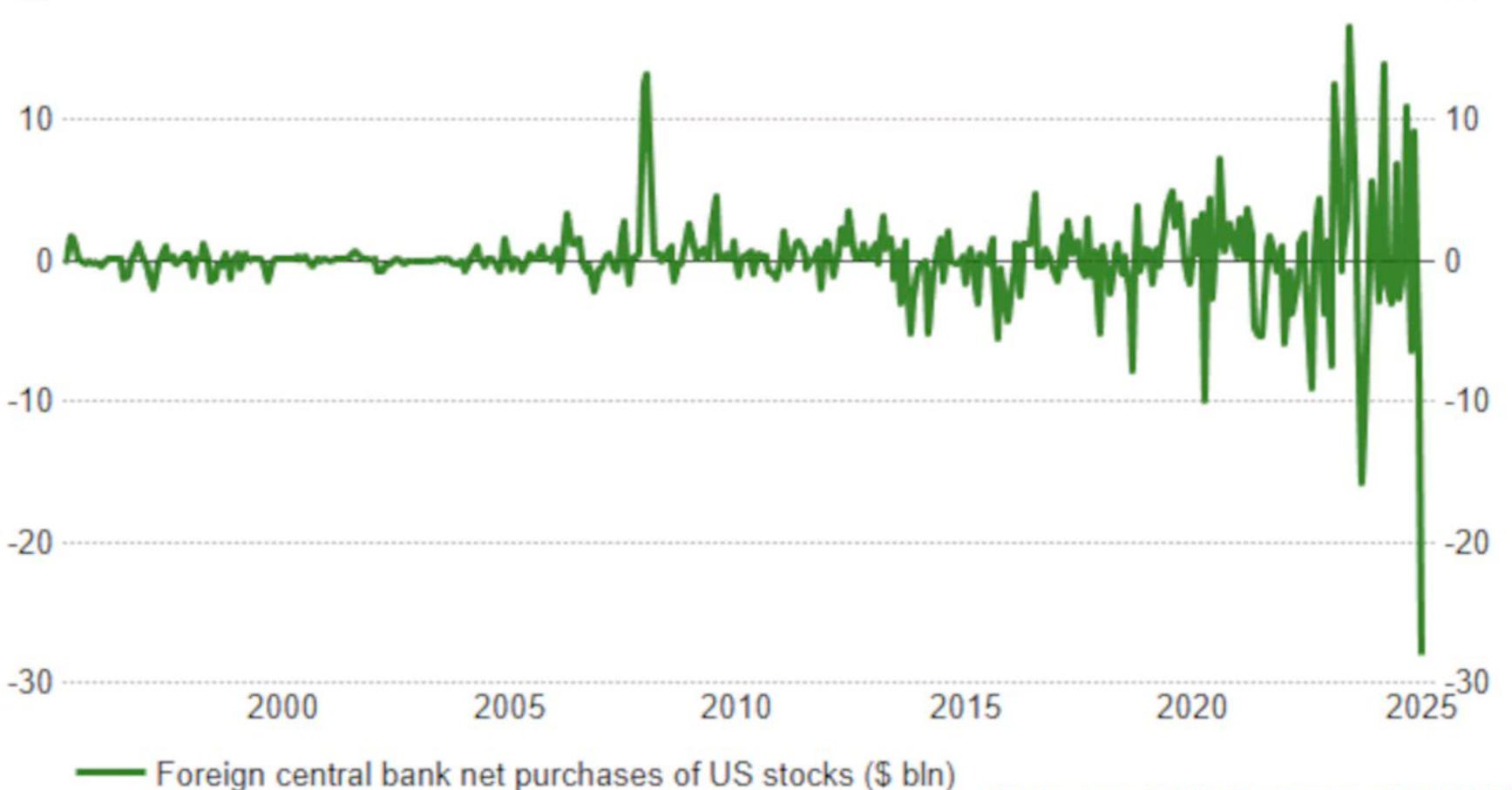

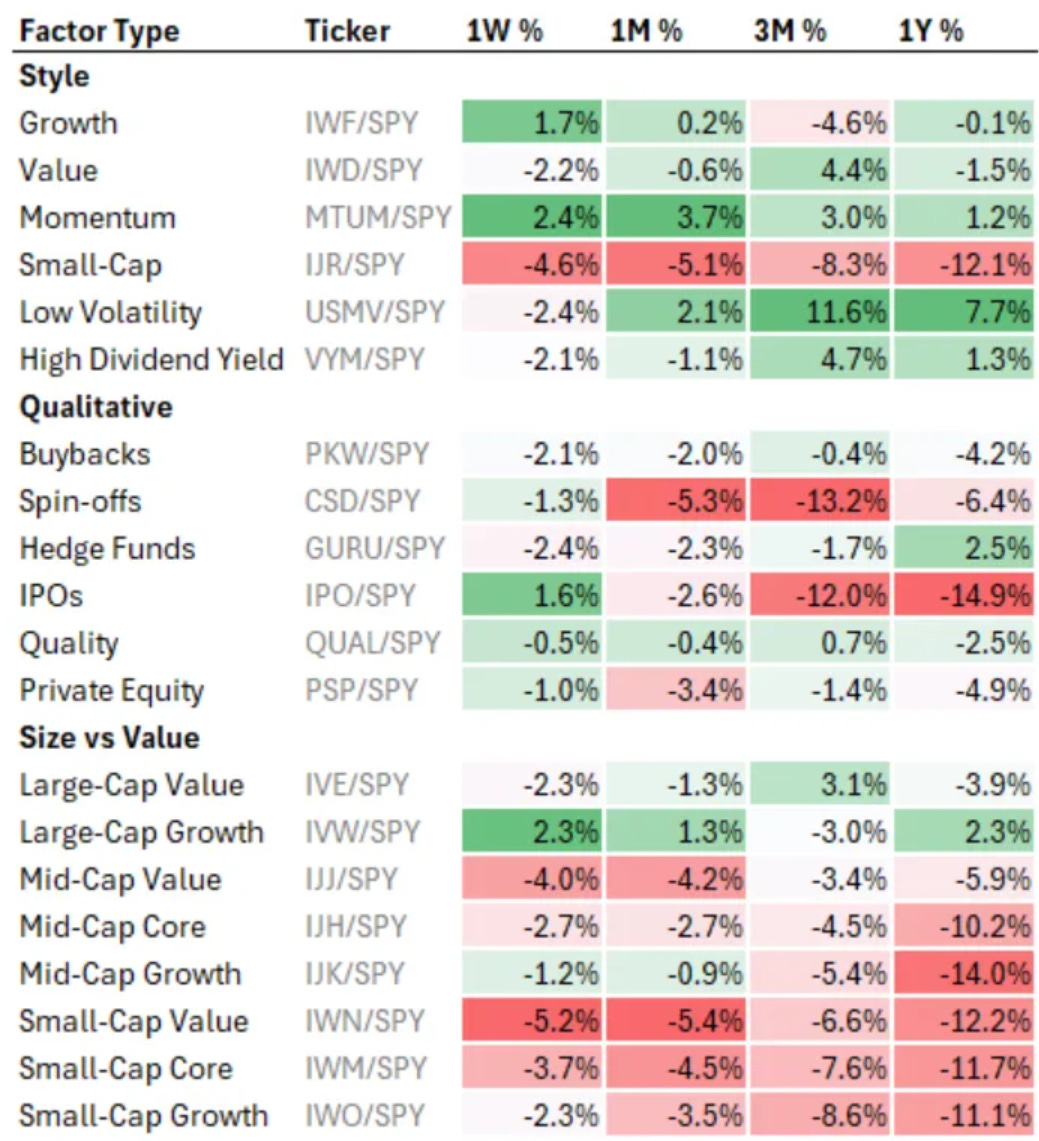

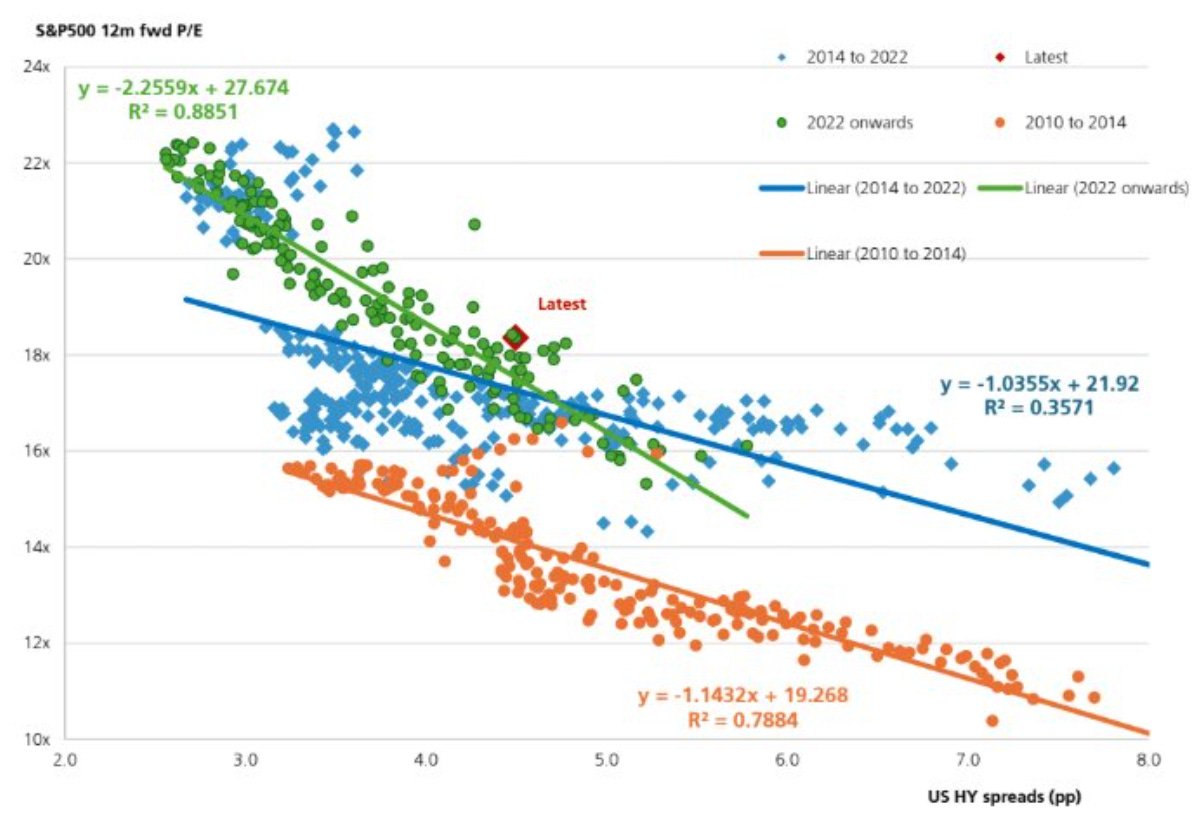

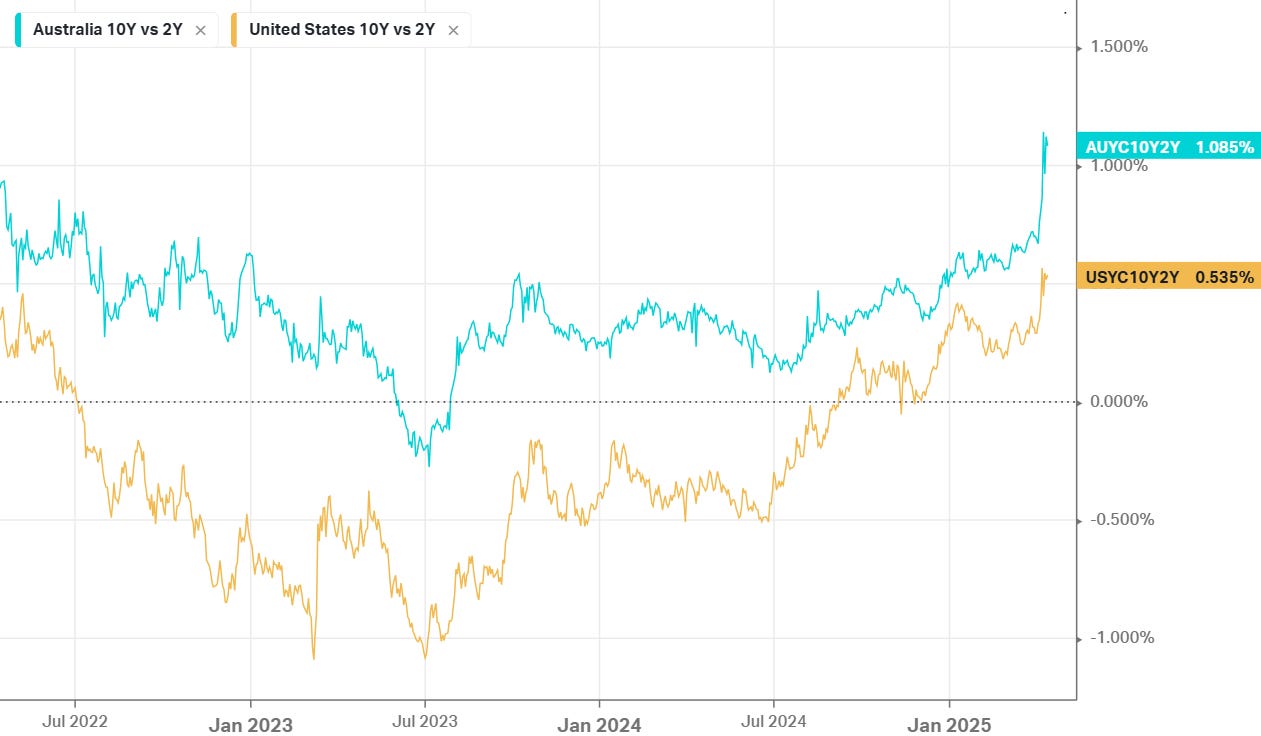

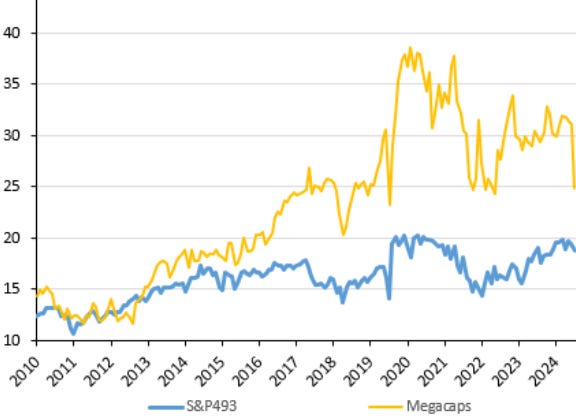

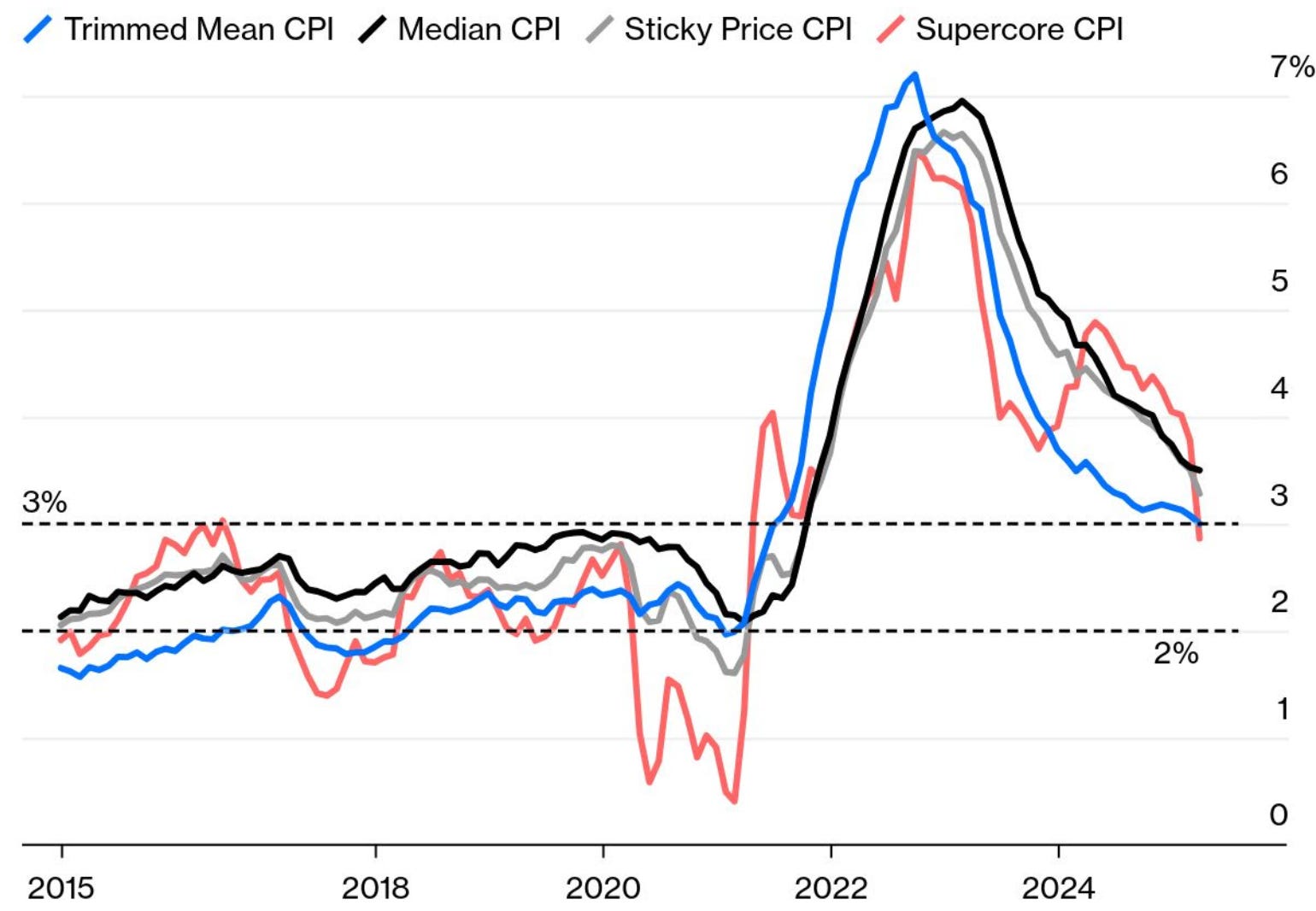

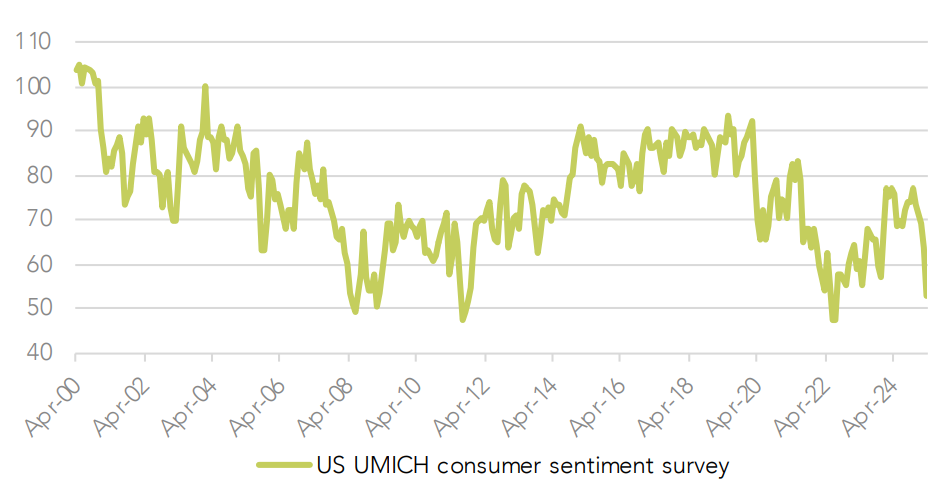

10k Words Equitable Investors April 2025 Apparently, Confucius did not say "One Picture is Worth Ten Thousand Words" after all. It was an advertisement in a 1920s trade journal for the use of images in ads on the sides of streetcars... Passive investment in global equities appears to have continued on while active flows remain negative and foreign demand for US stocks reverses sharply. But in the US, momentum was the winning factor in the past volatile week and month, a factor small caps have been lacking, with small cap earnings growth over the past decade generally not accompanied by multiple expansion. Credit spreads have been on the rise and the correlation between credit spreads and the valuation of equities has also been increasing. The post-tarrif volatility has cut back the forward PE on the ASX sharply BUT it is worth bearing in mind that the ASX's largest companies were established in a more distant era than the dominant companies in the US, where multiples are higher. On the US - inflation was retreating nicely prior to the tarrifs but consumer confidence is at GFC levels. Finally, we divert to look at online penetration of lottery sales around the world. Flows into global equities

Source: Goldman Sachs Foreign official demand for US stocks

Source: Reuters, Charles Schwab US equity market factor performance as of end of last week (ETF factor proxies)

Source: Koyfin, Equitable Investors Strong earnings growth for small caps but their returns lagged as their valuation multiples remained more or less the same (2015-2024)

Source: Robeco ICE BofA US High Yield Index Option-Adjusted Spread

Source: FRED Relationship between the S&P 500 forward PE multiple & credit spreads

Source: UBS US & Australian government bond yield spreads (10 year v 2 year)

Source: Koyfin ASX forward PE multiple

Source: Evans & Partners Australia's largest companies from a different era to the US

Source: Owen Analytics Forward PE on US equities

Source: Evans & Partners US core inflation had been falling sharply

Source: Bloomberg US consumer confidence drops to GFC levels

Source: Wilsons Advisory Online penetration of lottery sales Source: Jumbo Interactive (ASX code: JIN) April 2025 Edition Funds operated by this manager: Equitable Investors Dragonfly Fund Disclaimer Past performance is not a reliable indicator of future performance. Fund returns are quoted net of all fees, expenses and accrued performance fees. Delivery of this report to a recipient should not be relied on as a representation that there has been no change since the preparation date in the affairs or financial condition of the Fund or the Trustee; or that the information contained in this report remains accurate or complete at any time after the preparation date. Equitable Investors Pty Ltd (EI) does not guarantee or make any representation or warranty as to the accuracy or completeness of the information in this report. To the extent permitted by law, EI disclaims all liability that may otherwise arise due to any information in this report being inaccurate or information being omitted. This report does not take into account the particular investment objectives, financial situation and needs of potential investors. Before making a decision to invest in the Fund the recipient should obtain professional advice. This report does not purport to contain all the information that the recipient may require to evaluate a possible investment in the Fund. The recipient should conduct their own independent analysis of the Fund and refer to the current Information Memorandum, which is available from EI. |

2 May 2025 - Hedge Clippings | 02 May 2025

|

|

|

|

Hedge Clippings | 02 May 2025 The choice of descriptions of the 2025 election campaign are numerous, but we would suggest all are synonyms of one of the following: boring, disappointing, uninspiring. In other words lacking any real vision for the future - other than that of the individuals contesting the various seats. Primary amongst the culprits are Albanese and Dutton. Albo at best has been uninspiring during his three years in the top office, and until the start of the year when he seemed to develop some enthusiasm for the task ahead, looked like he was gone for all money. Then along came Peter Dutton, who having had nearly three years to prepare for the election, has done nearly everything he could to make Albo re-electable - or rather the least worst option in a two-horse race. Maybe he was relying on Albo to trip up (which he almost did when falling off the stage), or merely bore the electorate into ensuring he became a one term PM. The only thing to be said for Albo is he went full term - unlike his predecessors Kevin Rudd, Julia Gillard and then Kevin again. For example: For some reason Dutton (or the faceless men and women of the Liberal party hierarchy) thought that going from being a zero operator of nuclear power stations - following a dirty backroom deal in the Senate engineered by the Greens in 1998 - to having seven major nuclear stations in one swoop, would be an easy sell. It might have been to the party faithful, but where was the background media and PR campaign promoting small-scale modular reactors (SSMR's)? In its place, the government was able to mount (yet another) scare campaign, in spite of 32 countries around the world operating no less than 440 nuclear reactors, with France relying on nuclear for 70% of its power generation, and Australia signing up for nuclear powered submarines. Given Dutton's timeframe for Australia to "go nuclear" is 10 to 15 years (assuming no delays), surely a smarter move would be to hasten slowly, while getting the majority of the electorate onside, and exploring the latest technology provided by SSMR's? Meanwhile, Australia accounts for around 30% of the world's supply of uranium, which is currently selling for just over US$50 per pound. But we don't/won't use it. Go figure? Dutton has allowed himself to play catch-up with an irresponsible spendathon, and has ended up matching dollar for dollar the Labour Party's lavish vote-grabbing hand-outs, while opposing tax cuts for all. As we've noted before, voters are driven by their back pockets. Albanese and Chalmers have cynically targeted nearly every self-interested demographic group in the country, with the economic equivalent of fairy bread at a four-year-old's birthday party - looks attractive, the punters will lap it up, but it won't do them any good after the initial sugar hit. Both parties have committed to increased budget deficits, and no-one is talking about structural changes to the budget or the taxation system. Except the Labour party, who want to introduce a tax on unrealised capital gains... but haven't really been called out on it. Go figure again! Meanwhile Dutton hasn't been helped by a typical scare campaign, but he's left himself open to that. So the polls - and the media - are writing the opposition off. Maybe there's an outside chance of an upset given the peculiarities of Australia's voting system and state-based biases, but we doubt it. The good news is that the election will be over next week. The bad news is that whoever wins will be there for another three years! Back to interest rates: Inflation is now in the RBA's mid range target at 2.4%, (for the second quarter in a row) or 2.9% if you take their preferred trimmed mean measure. Capital city weighted mean was a tad higher at 3.0%, with Brisbane spoiling the party thanks to the end of $1,000 electricity handouts. On receipt of the numbers, Jim Chalmers was as keen as usual not to be pressuring the RBA, whilst doing precisely that, but it is going to be difficult for the RBA to keep rates on hold at 4.1% following their next meeting on the 20th of May. News & Insights Manager Insights | East Coast Capital Management The Future of Transport: Innovations transforming how we move | Magellan Asset Management First Do No Harm | Airlie Funds Management March 2025 Performance News TAMIM Fund: Global High Conviction Unit Class Insync Global Capital Aware Fund DAFM Digital Income Fund (Digital Income Class) |

|

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday |

2 May 2025 - Performance Report: Equitable Investors Dragonfly Fund

[Current Manager Report if available]