NEWS

30 Jun 2026 - Performance Report: Insync Global Quality Equity Fund

[Current Manager Report if available]

29 Jun 2026 - Performance Report: Bennelong Emerging Companies Fund

[Current Manager Report if available]

29 Jun 2026 - 10k Words | June 2026

|

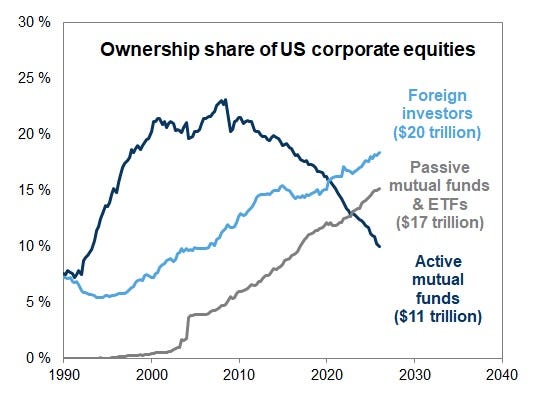

10k Words Equitable Investors June 2026 (2-minute read) A takeover of the US equities market by foreign investors and passive vehicles; leading into the equal-weighted index lagging. Demand for power surging as free cash flow generation at the "Mega Tech" collective goes the other way; fund managers' most crowded trade amid all that is semi-conductors; and AI attracts new founders like moths to the flame. The value of US equities and housing is at record levels relative to GDP; but investor sentiment remains positive; and the number of investors expecting multiple expansion is evenly balanced with those predicting contraction. Elsewhere, we see evidence of softness in the Australian employment market and the widened gap between the top decile and bottom decile of US consumers. Ownership share of US corporate equities

Source: FT.com, Goldman Sachs Ratio of the equal-weighted S&P 500 to the S&P 500 index is down to 1.1, near the lowest since 2003

Source: The Kobeissi Letter, TheDailyShot Worldwide data centre power consumption projections (TWh): 2025 - 2027

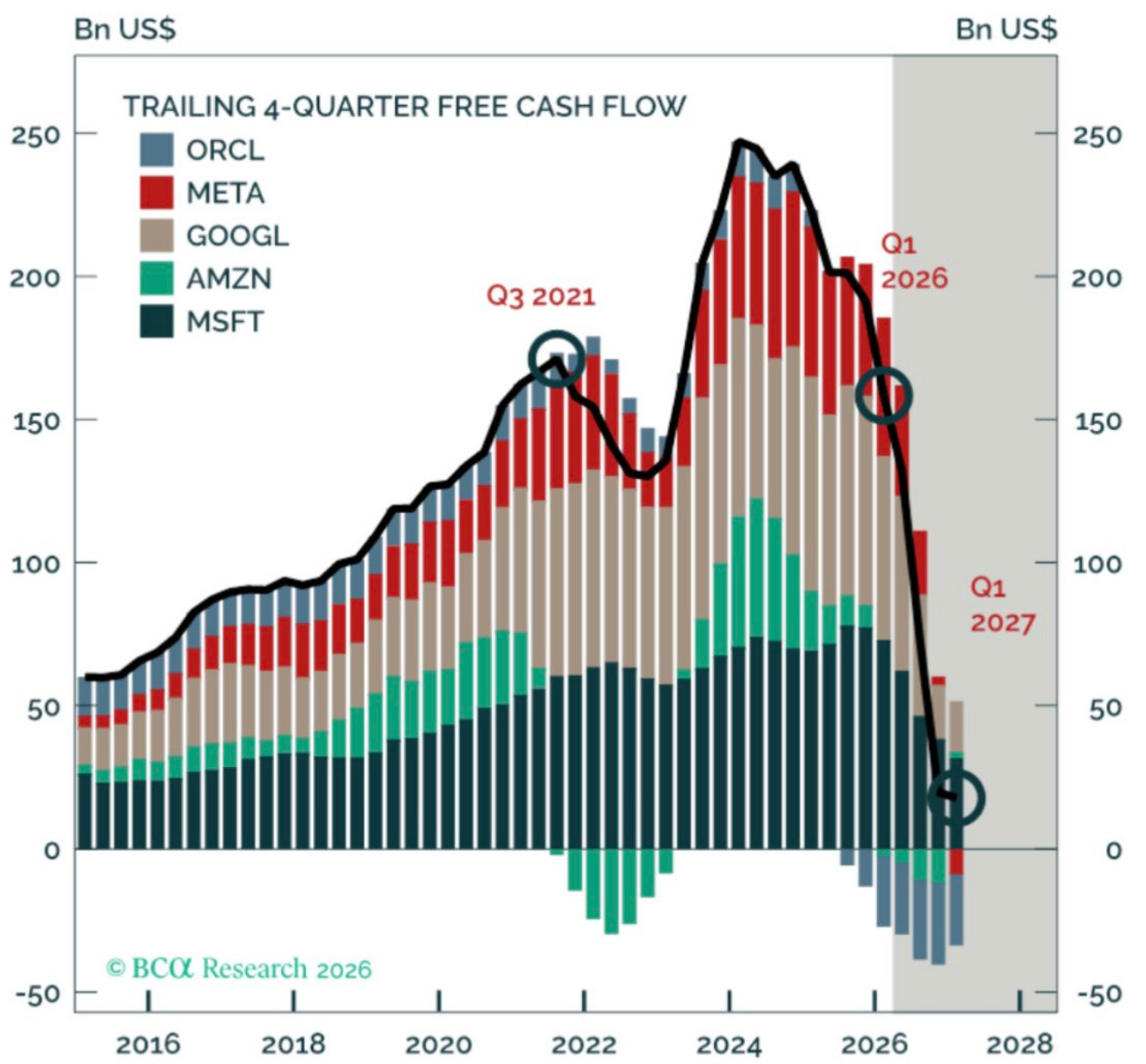

Source: Equitable Investors, Gartner "Mega Tech" free cash flow diminished - "capital light" model gone

Source: BCA Research Most crowded trade

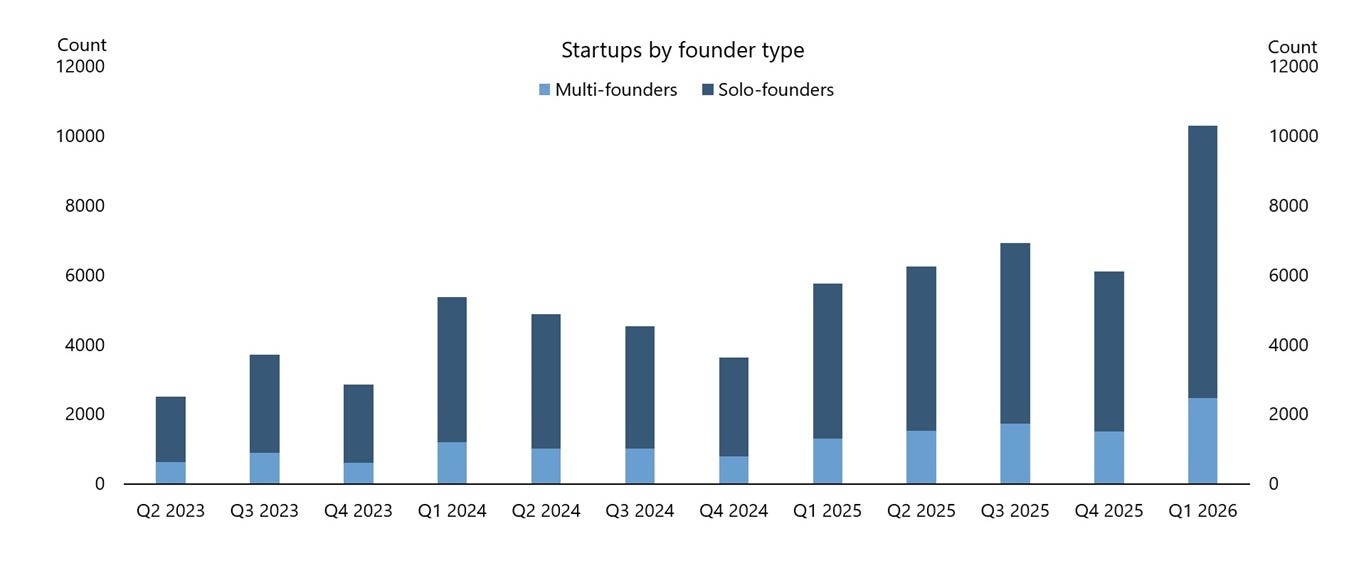

Source: Bank of America Fund Manager Survey AI-driven surge in number of startup founders

Source: Apollo Value of US equities and housing stock relative to GDP

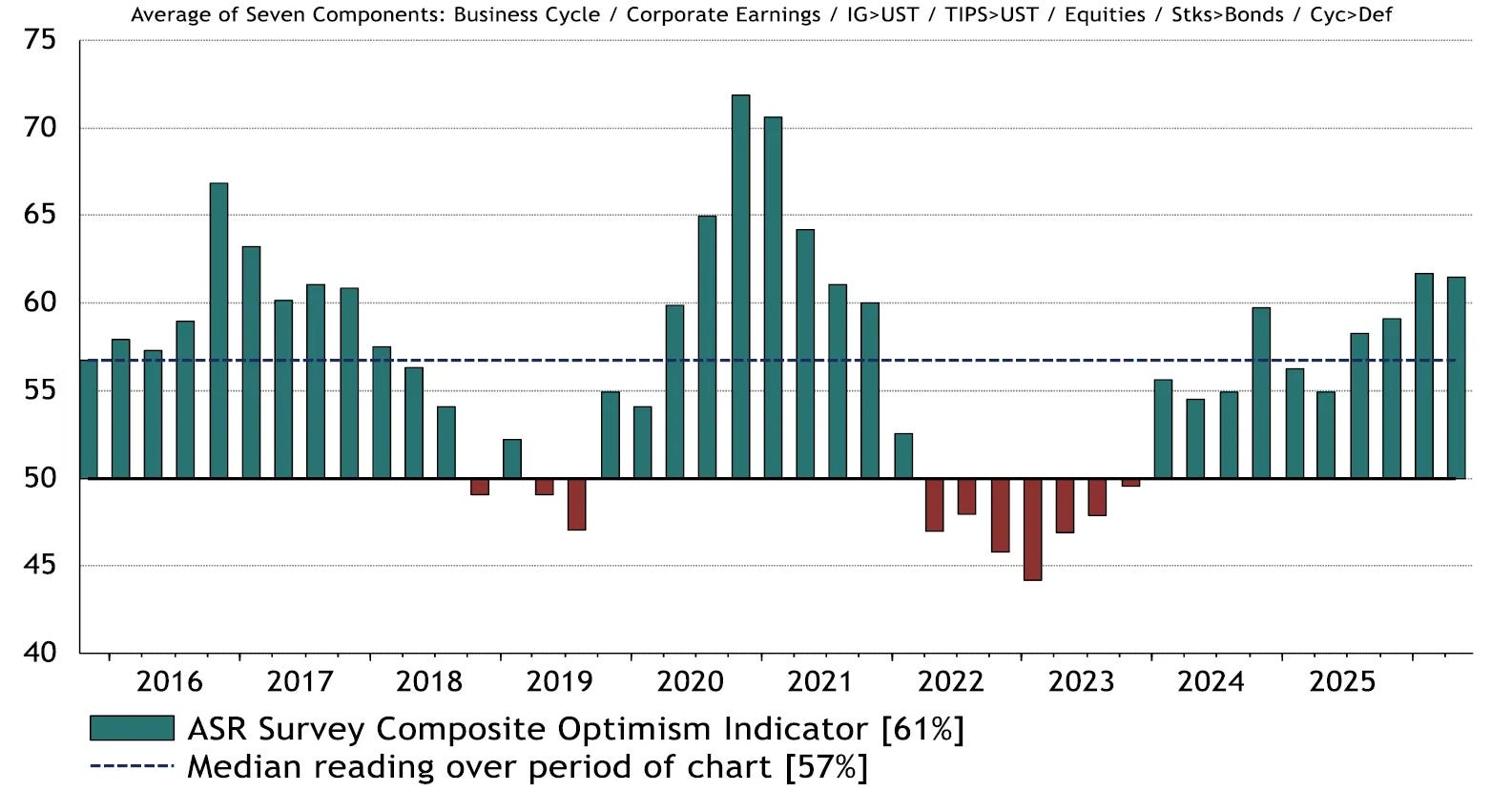

Source: re:venture ASR Asset Allocation Survey - composite optimism indicator

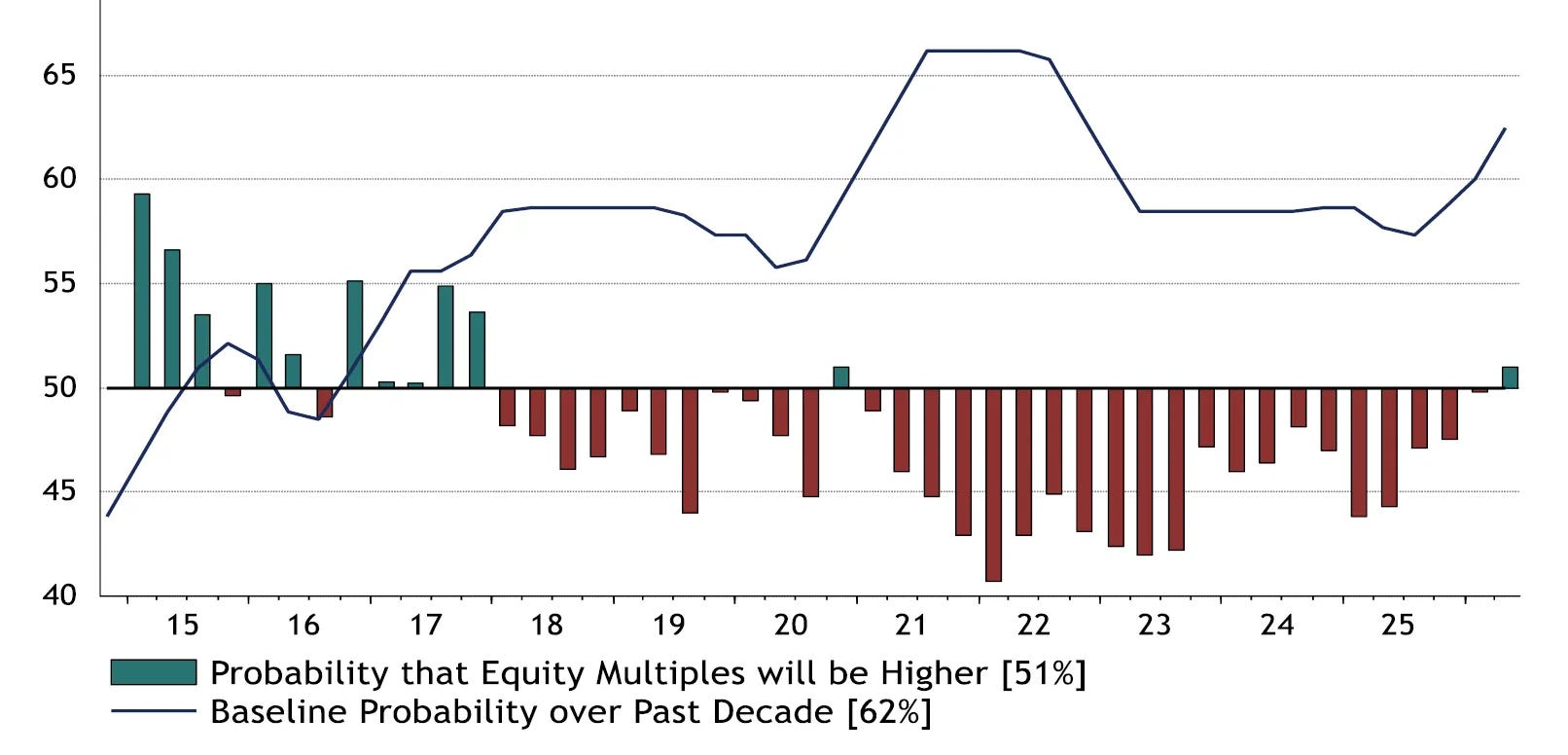

Source: Bloomberg, Absolute Strategy Research Survey on probability that global equity multiples will be higher a year from now

Source: Bloomberg, Absolute Strategy Research Seek Employment Index - May 2026

Source: Seek US consumer spending by income percentile

Source: FT.com, Moody's Funds operated by this manager: Equitable Investors Dragonfly Fund Disclaimer Past performance is not a reliable indicator of future performance. Fund returns are quoted net of all fees, expenses and accrued performance fees. Delivery of this report to a recipient should not be relied on as a representation that there has been no change since the preparation date in the affairs or financial condition of the Fund or the Trustee; or that the information contained in this report remains accurate or complete at any time after the preparation date. Equitable Investors Pty Ltd (EI) does not guarantee or make any representation or warranty as to the accuracy or completeness of the information in this report. To the extent permitted by law, EI disclaims all liability that may otherwise arise due to any information in this report being inaccurate or information being omitted. This report does not take into account the particular investment objectives, financial situation and needs of potential investors. Before making a decision to invest in the Fund the recipient should obtain professional advice. This report does not purport to contain all the information that the recipient may require to evaluate a possible investment in the Fund. The recipient should conduct their own independent analysis of the Fund and refer to the current Information Memorandum, which is available from EI. |

26 Jun 2026 - Hedge Clippings |26 June 2026

|

|

|

|

Hedge Clippings | 26 June 2026 Central banks are trying to sound calm. Markets are trying to sound confident. Neither looks entirely convincing. RBA | Waiting is not relief The Reserve Bank left the cash rate unchanged at 4.35%, but nobody should have confused that with comfort. After a year of policy reversals, first down, and then back up, the Board is now in the only other position available: waiting. That is not the same as relief. More a case of being stuck between a rock and a hard place. The latest inflation data gave both sides of the argument (and politics) something to cling to. Annualised headline CPI fell to 4.0% in May, helped by fuel-price effects, which was quickly treated in some corners as evidence that pressure is easing. The more important number, however, was the trimmed mean, which rose to 3.6% and reached its highest level since September 2024. That is the measure the RBA watches most closely, and as the chart above shows, it is not moving in the right direction. The difficulty the RBA has at this point in the cycle - apart from inflation remaining above their 2-3% trimmed mean target - is that they can see more volatility to pricing ahead. In July the fuel excise respite is due to halve, and at some stage will be removed altogether. While hostilities in the Middle East have abated (for now) it is going to take some time for the aftermath of the war, and its effects on supply driven inflation, to work through the system. The only certainty seems to be uncertainty. The labour market adds to the ambiguity. May employment rose by 40,300, which looks solid at first glance. But 35,200 of those jobs were part-time, while total hours worked fell. Unemployment eased to 4.4% from April's 4.5%, but this is not a labour market roaring back to life. It is a labour market holding headcount while reducing hours. That matters. It gives the RBA no clean reason to cut, and no urgent reason to hike. Instead, it keeps the Board exactly where it has been: staring at the next inflation print and hoping the economy does not force its hand. However, according to Renny Ellis from Arculus Funds Management, the market is only pricing in around 8 bps of tightening over the next 12 months, which he believes is under-pricing the medium-term risk of a "higher for longer" environment, which in his view is leading to a further rate rise in Q4 this year. Ellis also sees the risk of "a credible path to a second 25bp increase in 2027" as being possible. You can read his Market Commentary via this link. Property | The policy squeeze arrives before the policy changes The housing market is already showing strain. The combined capitals' preliminary auction clearance rate fell to 47.4%, the lowest weekly reading since April 2020. That is not a market looking through rate hikes. It is a market absorbing them. Sydney and Melbourne remain the key pressure points. Affordability is stretched, borrowing capacity has been hit, and consumer confidence has not been helped by the Budget's changes to negative gearing and capital gains tax. National home values were flat in May, while Sydney values are already below their November 2025 peak. The important point is that the tax changes have not yet landed. The CGT discount reform and negative gearing restrictions are not due to apply until July 2027, while the SMSF residential LRBA ban is expected around August 2026. The current weakness is therefore a combination of rate-driven, combined with investors reacting to uncertainty and fear of the tax reforms that will bite later. If consumer confidence deteriorates further, the property market could shift from a source of household wealth comfort to a source of household anxiety very quickly. Chalmers can argue about the technicalities of the property market being in a correction or not, but the reality for homeowners with a high LVR, or selling their house into a softening market are feeling the reality pinch. The bottom line This was a week of misleading headlines and uncomfortable details. Headline inflation fell, but underlying inflation rose. Jobs grew, but mostly part-time. GDP expanded, but only because data-centre investment did the heavy lifting. Property softened before the major tax reforms have even begun to bite. For investors, the lesson is familiar. Volatility does not just reveal market direction. It reveals process. It shows which managers are relying on beta, which are managing risk, and which have a framework strong enough to survive when the story changes. That is where FundMonitors matters. Weeks like this are exactly why manager research, peer comparison and performance analysis are worth doing properly. News | Insights Is the Consensus on Equities the Riskiest Trade in the Room? | East Coast Capital Management Market Commentary | Glenmore Asset Management May 2026 Performance News Seed Funds Management Financial Income Fund DAFM Digital Income Fund (Digital Income Class) |

|

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday |

26 Jun 2026 - Performance Report: ASCF High Yield Fund

[Current Manager Report if available]

26 Jun 2026 - Yields take centre stage again

25 Jun 2026 - Performance Report: Glenmore Australian Equities Fund

[Current Manager Report if available]

25 Jun 2026 - Japan - From Observation to Conviction and Two Quality Investment Ideas

|

Japan - From Observation to Conviction and Two Quality Investment Ideas Alphinity Investment Management May 2026 4-minute read |

|

Japan is changing -- and the pace of that change is easy to underestimate from a desk in Sydney. Global Portfolio Manager Chris Willcocks recently completed a week-long investor trip through Osaka, Tokyo, Kyoto and Nagoya, meeting management teams across Industrial, Consumer, Property and Technology companies. The on-the-ground experience reinforced and deepened a thesis already forming in our portfolios. Below we share the highlights from those observations -- and two quality Japanese companies which are in an earnings upgrade cycle. Three forces reshaping JapanJapan's transformation rests on three structural pillars that are now compounding positively for the first time in decades. Each alone would be noteworthy; together, they represent the most significant fundamental improvement recent memory.

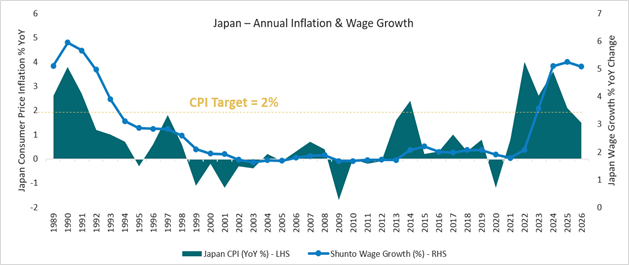

Inflation Has Finally Arrived & Wages are Keeping Pace

Source: Bloomberg, April 2026

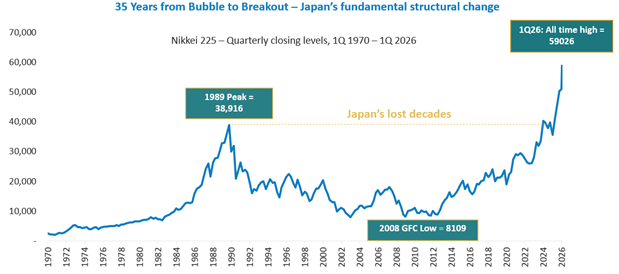

Taken together these macro forces are driving up asset prices and boosting consumer confidence. You see evidence of this across the cities and financial markets. House prices in parts of Tokyo have appreciated ~40% in six months, the Nikkei has surpassed its 1989 all-time high, inbound tourism is at record levels. There were more Ferraris and Lamborghinis on the streets of Tokyo than we have seen in any city recently. Mirroring global trends, the lower-end consumer is less buoyant, and construction faces increasing cost headwinds, but the broader picture is one of a country regaining its economic confidence. The Japanese stock market in context

Source: Bloomberg, April 2026 Against this macro backdrop, the question for active investors is not whether Japan is changing -- it is which companies are best placed to capture that change. Two high quality Japanese companiesAlphinity invests in Earnings Leaders -- quality businesses, trading at reasonable valuations, that are entering or sustaining an earnings upgrade cycle. Japan, at this point in its structural reset, is generating exactly that kind of opportunity. The two companies we discuss below are held across our global funds.

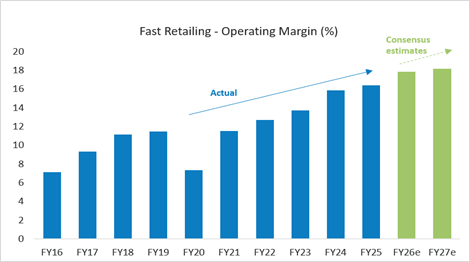

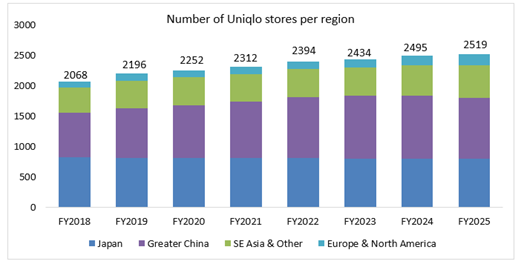

Fast Retailing -- the Japanese apparel giant behind the UNIQLO brand -- has quietly evolved from a domestic discount retailer into one of the world's most compelling consumer growth stories. Founded in 1949 and listed in Tokyo since 1999, the company today generates ¥3.4 trillion in annual revenue across over 2,500 stores in more than 25 countries, with a long-term revenue target of ¥10 trillion. At the helm is founder Tadashi Yanai, who retains a ~40% stake and remains as deeply invested in the business as ever -- in every sense.

|

|

Funds operated by this manager: Alphinity Australian Share Fund , Alphinity Concentrated Australian Share Fund , Alphinity Sustainable Share Fund , Alphinity Global Equity Fund , Alphinity Global Sustainable Equity Fund This material has been prepared by Alphinity Investment Management ABN 12 140 833 709 AFSL 356 895 (Alphinity). It is general information only and is not intended to provide you with financial advice or take into account your objectives, financial situation or needs. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. Any projections are based on assumptions which we believe are reasonable but are subject to change and should not be relied upon. Past performance is not a reliable indicator of future performance. Neither any particular rate of return nor capital invested are guaranteed. |

24 Jun 2026 - Performance Report: DAFM Digital Income Fund (Digital Income Class)

[Current Manager Report if available]