NEWS

Performance Report: ECCM Systematic Trend Fund

The ECCM Systematic Trend Fund has returned +12.36% per annum since inception in January 2020, an outperformance of 7.08% relative to the SG Trend benchmark which has returned +5.28% on an annualised basis over the same period.

Read more...

Investment Perspectives: The clear themes emerging from the tariff chaos

Through all the noise, we believe some important themes are emerging which are likely to last well beyond any potential forthcoming tariff compromise (or non-compromise).

Read more...

Hedge Clippings | 16 May 2025

Consensus expectations from a significant majority of economists anticipate a 25 basis point cut next Tuesday when the RBA announces their decision following the new format 2-day board meeting.

Read more...

Performance Report: Glenmore Australian Equities Fund

The Glenmore Australian Equities Fund rose by +3.50% in April. Since inception in June 2017, the fund has returned +17.50% per annum, an outperformance of +8.83% relative to the ASX 200 Total Return benchmark which has returned +8.67% on...

Read more...

Performance Report: Argonaut Global Gold Fund

The Argonaut Global Gold Fund rose by +2.30% in April, outperforming the S&P Global Natural Resources AUD (TR) benchmark by +7.79%. Since inception in November 2022, the fund has returned +23.33% per annum, an outperformance of +21.16%...

Read more...

Tariffs, Tension and Tech: How Trump's Second Term is Reshaping Markets

It would be an understatement to say that the world has become a more volatile and uncertain place since Donald Trump moved back into the Oval Office in January. Given that markets don't like uncertainty, it's no surprise that both US and...

Read more...

Performance Report: Altor AltFi Income Fund

The Altor AltFi Income Fund rose by +0.94% in April, outperforming the RBA Cash Rate + 5% benchmark by +0.21%. Since inception in April 2018, the fund has returned +11.48% per annum, an outperformance of +4.57% relative to the benchmark...

Read more...

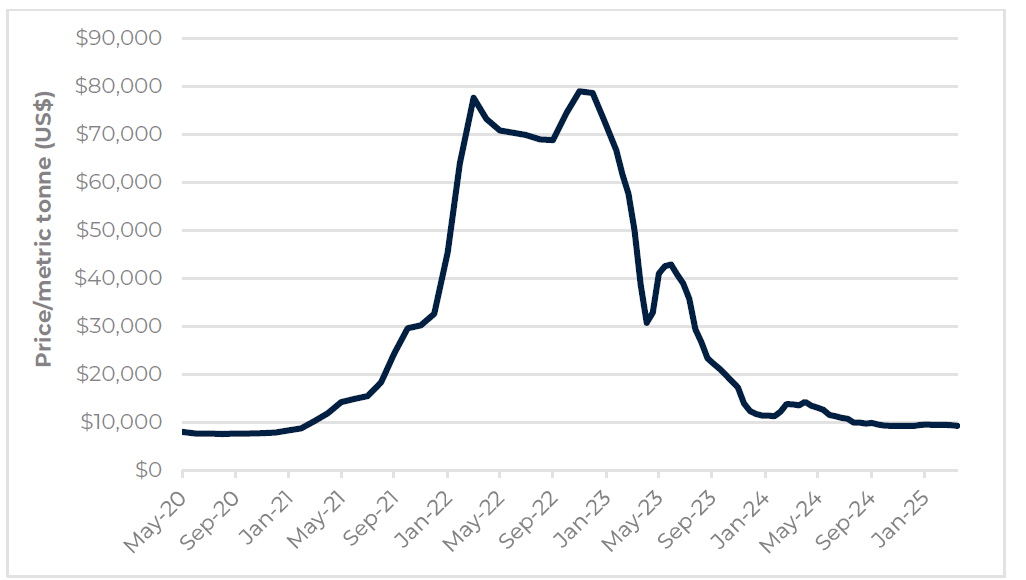

Is this now an opportunity for china exposed stocks?

After a significant price correction in China exposed stocks over the last year, Tyndall's Jason Kim recently went to China and met with various companies and industry experts to help determine whether some of these stocks now represent a...

Read more...

Performance Report: Bennelong Twenty20 Australian Equities Fund

The Bennelong Twenty20 Australian Equities Fund rose by +3.24% in April. Since inception in November 2009, the fund has returned +9.34% per annum, an outperformance of +1.25% relative to the ASX 200 Total Return benchmark which has...

Read more...

Performance Report: Argonaut Natural Resources Fund

The Argonaut Natural Resources Fund has returned +23.62% per annum since inception in January 2020, an outperformance of +17.21% relative to the S&P/ASX 300 Resources TR benchmark which has returned +6.41% on an annualised basis over the...

Read more...