NEWS

23 May 2025 - Hedge Clippings | 23 May 2025

|

|

|

|

Hedge Clippings | 23 May 2025 This week's rate cut following the RBA's meeting on Tuesday was pretty much a fait accompli, and apart from one big bank economist who was backing a 50 bps move, it was widely expected. Had it not been for the election getting in the way, there's a good chance the RBA would have moved at their previous board meeting. We ran a webinar immediately after Tuesday's decision featuring a panel of three well-respected fund managers - Nick Chaplin from Seed Funds Management, Winston Sammut from Euree Asset Management, and Alex Pollak from Loftus Peak. While there were no surprises regarding the outcome, there were plenty of interesting insights from them on the outlook from here. If you missed it, you can watch a recording from the link in the news section below. For rate move enthusiasts, the focus now will be on how many more cuts there may be this side of Christmas. While the consensus is for two more, taking the cash rate down to 3.35% at least (assuming 0.25% each), it is worth remembering the consistent use of the word "uncertain" in the RBA's statement. Locally one big variable will be the strong labour market, with the ABS announcing wage and salary growth of 5.8% in the year to March. Of course there's always an element of uncertainty in economic forecasting, but throwing in the unpredictability of Donald Trump's policy zig-zags and U-turns makes it particularly difficult to see far ahead. Overseas, the FED's Jerome Powell is sticking to his guns given the uncertain effects of the US vs. China and the rest of the world's tariff policy. The Donald seems to have at last caught on that the uncertainty of both the magnitude and timing of the eventual outcome is harming the US economy as much as anyone else's. Trump loves to use the analogy of holding a strong hand in negotiations, but China (so far) seems to be holding their nerve. There are a number of opinions on Trump, but it's worth listening to what Anthony 'The Mooch' Scaramucci, head of SkyBridge Capital, and who served as White House Director of Communications for just 11 days in July 2017 during Trump's first term, has to say. Actually, if you Google the Mooch, you'll find he has plenty to say about everything, but particularly Trump. One wonders how he has time to run SkyBridge given the time he spends on, or in, the media. As far as Trump vs. China is concerned, his view is that Trump will have to capitulate, although if and when that occurs there's no doubt Trump won't admit to it, or frame it that way. For another view on China, it's worth reading, (here) or watching (here) Deputy Governor of the RBA Andrew Hauser's address to the Lowy Institute yesterday. Hauser is understandably less direct than Scaramucci, but having visited China just a week after Trump's (then) Liberation Day announcement, he was well placed to judge Chinese reaction first-hand. We suspect that beneath the RBA speak, Hauser may be at least on the same side, or hold a similar view as the Mooch. Changing tack, it seems at last there's some pushback against the Treasurer's plans for changes to super balances above $3 million. The issue is not really about higher taxes (30%) on large balances. Most taxpayers accept that concept on their everyday wages and salaries. It is probably not even about not indexing the $3 million level to adjust for inflation, because, as Chalmers points out, that can be left for future governments. The completely ludicrous, unfair, dangerous, and we would have thought unworkable aspect, is taxing unrealised capital gains. Sadly, post-election, jumping up and down now is a classic case of too little, too late, or closing the stable door after the horse has bolted. What were the Liberals thinking by not making the most of that argument when they had the chance, rather than now, when no one is really listening to them? Although looking back at the election result, it seems not many (or enough) voters were listening to them during the election campaign either. News | Insights | Webinar Webinar Recording | Impact of Tuesday's RBA rate decision Investment Perspectives: The clear themes emerging from the tariff chaos | Quay Global Investors Market Commentary | Glenmore Asset Management April 2025 Performance News 4D Global Infrastructure Fund (Unhedged) Canopy Global Small & Mid Cap Fund |

|

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday |

23 May 2025 - Performance Report: DS Capital Growth Fund

[Current Manager Report if available]

23 May 2025 - On the Road with Alphinity Global: The Rising Premium on Certainty

|

On the Road with Alphinity Global: The Rising Premium on Certainty Alphinity Investment Management May 2025 |

|

Over the past several months, our global investment team has embarked on a series of research trips across multiple continents, meeting more than 250 companies in five countries to gain first-hand insights and identify emerging trends. All six team members recently completed another round of visits to the United States ahead of the 1Q25 reporting season. In today's highly volatile environment, this on-the-ground perspective has proven indispensable for staying ahead of rapidly unfolding developments.

Our conversations with management teams spanning Singapore's financial centres and San Francisco's tech corridors to Mumbai's manufacturing hubs and Beijing's policy circles have revealed a striking shift in corporate sentiment. The optimism that characterized the start of the year has been replaced by widespread operational uncertainty, especially since March, as executives navigate unpredictable policy changes and ongoing supply chain disruptions. This environment has prompted many companies to withdraw forward-looking statements, narrow their guidance ranges, or append new disclaimers to their 1Q25 earnings releases considering persistent macroeconomic volatility. In this note, we outline some of the key themes emerging from our recent travels and discuss how our on-the-ground insights are helping us refine our portfolio-balancing a more defensive stance with selective growth opportunities that have been unjustly discounted.

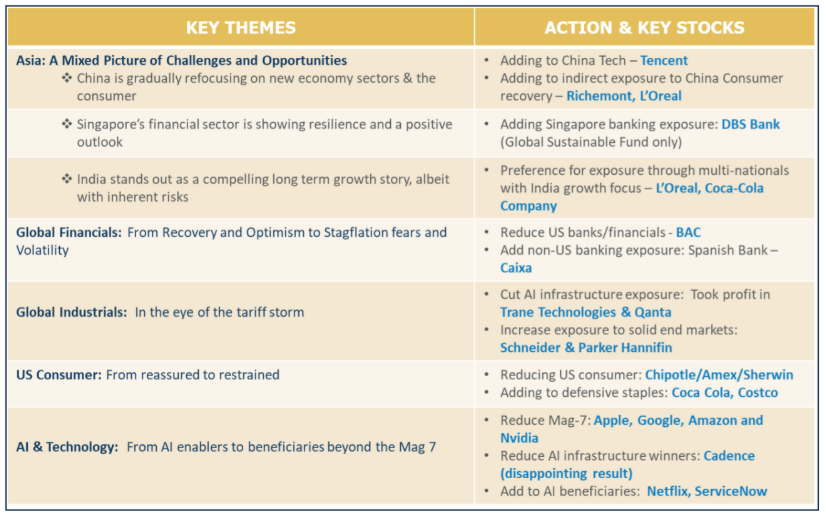

Asia: A Mixed Picture of Challenges and Opportunities

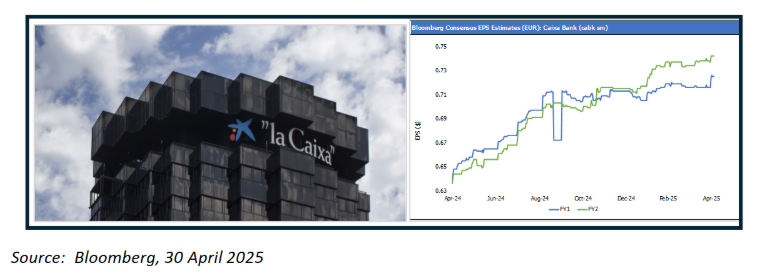

Global Financials: From Recovery and Optimism to Stagflation fears and Volatility Post-election optimism for deregulation and tax cuts initially fuelled a global banking rally at the end of 2024, buoyed by robust deal pipelines and corporate engagement. However, stagflation fears and plunging consumer confidence reversed sentiment by mid-February 2025, freezing corporate activity. Recent 1Q25 results and CEO commentary show limited numerical impact to date, with tariff-driven front-loaded spending creating sporadic activity and heightened volatility boosting trading desks like Morgan Stanley's. On the real estate side, CBRE's result reflected a continued, yet sensitive commercial real estate recovery cycle. The business was buoyed by the strength of its resilient business lines and continued benefit from scarcity within the office sector for capital markets and leasing. Across the Atlantic, Germany's €1 trillion defence and infrastructure package represent a structural break from decades of austerity. A potential growth tailwind for Eurozone banks, including Spanish lenders like CaixaBank. Spain's economy is already outpacing EU peers with 2.5%+ GDP growth likely, and we expect that CaixaBank will be a key beneficiary given its market-leading positions in mortgages, payroll services, and wealth management--sectors poised to compound gains from digital transformation and demographic tailwinds. That said, the spectre of U.S. tariffs on EU goods looms large, potentially offsetting 20-30% of Germany's stimulus benefits and introducing cross-sector vulnerabilities. CaixaBank - Leading retail bank exposed to relative strength of the Spanish economy & seeing strong earnings upgrades

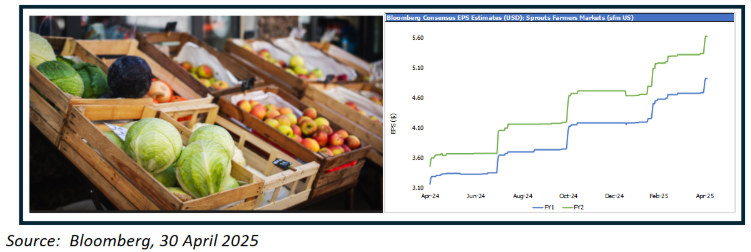

US Industrials - in the eye of the tariff storm The prevailing sentiment among US industrial players in February 2025 closely echoed what we observed during our September 2024 visit. The sector remains on a path toward gradual, measured recovery, rather than a rapid resurgence. Management teams were however cautious, reflecting uncertainties about inflation, tariffs, political instability, and the Chinese economic landscape. While there were some signs of emerging positive momentum, a "low and slow" industrial rebound is more likely. Notably, regions outside the US - particularly Europe and China - may see stronger recoveries, given their steeper prior declines. End markets continue to matter, with aerospace, electric grid and waste operators all remaining relatively positive, while in contrast the environment remains tough for agriculture, transportation and residential housing. Two key themes stood out: tariffs and a short-cycle manufacturing recovery. Companies are preparing for tariff-related cost increases, with some already passing on surcharges and viewing tariffs as an opportunity to raise prices, which likely drives inflationary pressures. A fragile short-cycle recovery was noted despite scepticism regarding the underlying causes, with inventory buildup ahead of tariffs largely dismissed by management teams. Amid these conditions, we remain focused on defensive industrial names such as Waste Connections, the third-largest US waste operator, which recently exceeded 1Q25 estimates and reiterated its FY25 guidance, reporting no material impact from recent macro volatility. Whilst our current exposure to US industrials remains aligned with resilient, high-quality industrials underpinned by resilient end markets, the recent market weakness is starting to throw up exciting opportunities at more reasonable valuations. US Consumer - From reassured to restrained During our US visit in January 2025, consumer management teams described the business environment as "generally positive" with expectations of faster policy execution under a new Trump administration. Supply chains have already notably shifted away from Chinese reliance since the previous Trump administration and any potential impact of tariffs was expected to be partially absorbed by Chinese manufacturers, maintaining competitive pricing for US retailers. The mood had shifted somewhat by March 2025, where our conversations with management were more cautious. Companies were generally reluctant to provide any detail on potential tariff impacts given the changing external goalposts and messaging from the government. There were no clear broad-based trends across the consumer aside from a continuation of the low- and high-income divergence, with the unusually cold start to the year also muddying the data. Whilst consumer confidence has since plummeted to 2022 lows, spending has been more resilient, but often more value-driven with consumers seeking the best bang for their buck and being selective about where to splurge or cut back. In response we have reduced some of our consumer facing holdings, such as Chipotle and Sherwin Williams, but added to Costco given its relatively defensive growth profile underpinned by a loyal membership base. We also added a new position in our Sustainable Fund to Sprouts Farmers' Market, a specialty grocer with a scarce growth profile within the Consumer Staples sector. We believe Sprouts should benefit both from near term consumer preferences for food at home (vs food away from home) and structural tailwinds of attributes-based healthy foods. Sprouts Farmers Market - Specialty organic grocer with multiple drivers supporting strong earnings growth

AI & Technology: From AI enablers to beneficiaries beyond the Mag 7 There was a striking disconnect during Technology meetings between the upbeat tone from technology management teams and the turbulence sweeping through equity markets. Enthusiasm around AI remains robust as functionality pushes deeper into business models, unlocking both revenue opportunities and operational efficiencies. "Agentic AI" is the next step in AI evolution where autonomous systems are created that can make decisions and executing complex, multi-step tasks with minimal human oversight. On top of AI technological advancement, there were three key themes emerged from company discussions:

Reflecting these shifts, we have steadily reduced our exposure to the Mag-7 and taken some profits in other AI capex exposed plays, such as Cadence Design Systems, and Nvidia. The capital has been reallocating towards AI software beneficiaries such as ServiceNow, while also establishing a position in Chinese champion Tencent, where growth is rebounding on the back of a revitalised gaming pipeline, surging advertising on WeChat Video Accounts, and expanding opportunities in fintech and cloud. TSMC and Netflix also remain favoured holding given the relative resilience of the business models.

In conclusion, our extensive global research travels have proven essential in navigating today's rapidly shifting landscape, allowing us to gain direct, actionable insights from management teams grappling with unprecedented uncertainty. As policy volatility and trade tensions reshape corporate strategies and outlooks, the value of certainty has never been higher for leaders making critical decisions. By grounding our portfolio positioning in these first-hand observations, we are better equipped to follow new earnings leadership and remain agile and well-informed as new challenges and opportunities emerge. Author: Elfreda Jonker - Alphinity Client Portfolio Manager |

|

Funds operated by this manager: Alphinity Australian Share Fund, Alphinity Concentrated Australian Share Fund, Alphinity Global Equity Fund, Alphinity Global Sustainable Equity Fund, Alphinity Sustainable Share Fund This material has been prepared by Alphinity Investment Management ABN 12 140 833 709 AFSL 356 895 (Alphinity). It is general information only and is not intended to provide you with financial advice or take into account your objectives, financial situation or needs. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. Any projections are based on assumptions which we believe are reasonable but are subject to change and should not be relied upon. Past performance is not a reliable indicator of future performance. Neither any particular rate of return nor capital invested are guaranteed. |

22 May 2025 - Performance Report: Insync Global Quality Equity Fund

[Current Manager Report if available]

22 May 2025 - Jurassic farce

|

Jurassic farce Redwheel May 2025 |

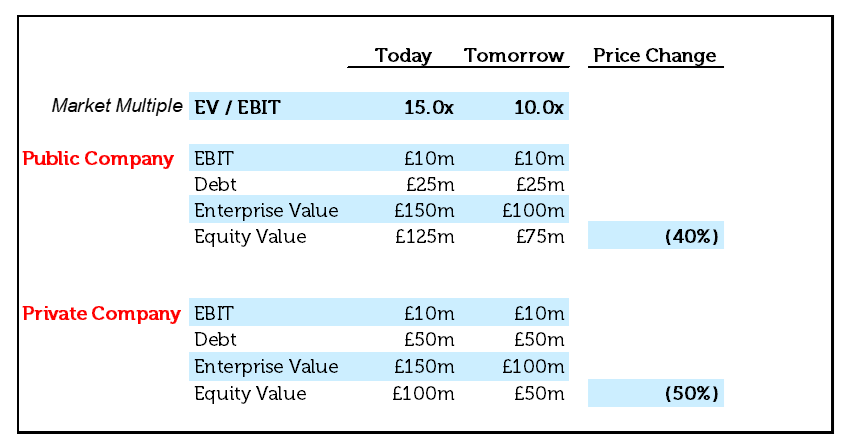

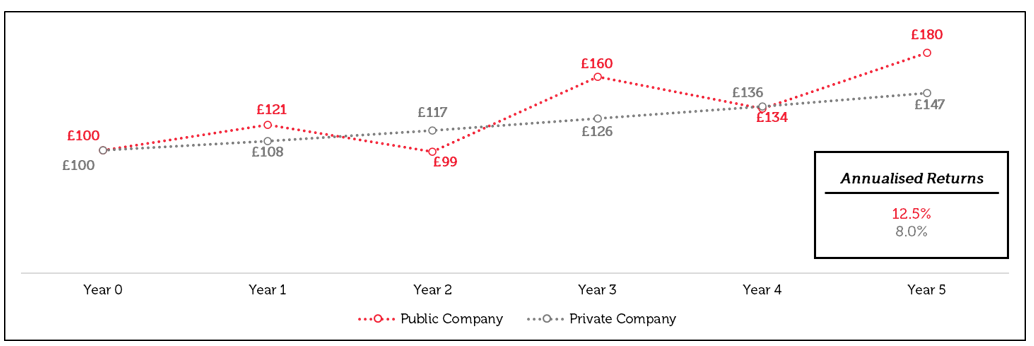

Blockbusters and buyoutsAs career moves go, it's certainly an unusual one. In 1969, a newly-minted Harvard Medical School graduate abandoned his promising career as a doctor to pursue his true passion: writing novels. As it turned out, this was a wise choice. That graduate - Michael Crichton - would go on to forge a highly successful career, churning out a string of famous novels. One of his books was catapulted to huge fame when it was immortalised in 1993 as a Steven Spielberg movie classic: Jurassic Park. In the epic film, where lab-created dinosaurs roam free on an island-resort-gone-wrong, one scene is particularly memorable. In a storm, the park's electric fences lose power just as our hero, palaeontologist Dr. Alan Grant, is sitting in a Jeep outside the Tyrannosaurus Rex enclosure - with two children in the car with him. Inevitably, the dinosaur dramatically escapes, flipping the car as it searches for an easy meal. Grabbing one of the children and standing perfectly still before the bellowing dinosaur, Dr. Grant delivers an iconic line: "Don't move. He can't see us if we don't move" [1]. Those who have read my previous blogs posts will know that I am an advocate of learning important investment lessons from all forms of art, including books, TV shows, and movies. In this case, however, I think that one cohort of investors - our cousins in private equity - have learned perhaps the wrong lesson from this film, and from this line in particular. In Private Equity Park [2], their approach to valuation and volatility is a warped version of Dr. Grant's famous line: if you can't see it, it doesn't move. The illusion of stabilityOrdinarily, when an investor wants to know the current market value of their investments, they check the listed price of their assets. Not so in private markets. Here, investors get a periodic and often lagged valuation concocted by an opaque internal process undertaken by the manager [3] rather than via a market of buyers and sellers setting a clearing price. This process is understandable - after all, they have to put a number on the investments somehow. What is perhaps less forgivable is the claim [4] that, as a result of this process, private investments are more stable and less risky asset classes - with risk often conflated with volatility - when compared to the daily price changes in public markets. To this assertion, we must object. Simply because one cannot see valuations of private companies change does not mean that they do not move in lockstep with public peers. After all, one cannot forget the "equity" part of private equity: if they are truly buying operating companies, as we do in public markets, why would the value of those companies not simply move alongside their listed peers? Moreover, private equity-owned companies typically carry larger amounts of debt [5] than their public equivalents, meaning that, all else being equal, their equity valuations should swing more than those of listed companies:

Source: Redwheel. The information shown above is for illustrative purposes. As a result, claiming that the value of your companies is more stable than public equivalents simply because they are unlisted is pure fantasy (vocal critics have termed it volatility laundering). The persistence of such claims, despite many in the industry pointing out the obvious flaws, is a reflection of the eagerness of investors to see a smooth chart, rather than a lumpy one, a mindset that seems to us to be prevalent amongst many allocators today. It's the destination, not the journeyWhilst we certainly endorse the view that investors should ignore day-to-day volatility and focus on the long-term compounding of their capital, we believe that the way to do this is simply by being more willing to tolerate short-term volatility. In our view however, it is not done by paying extremely high fees to managers to employ huge leverage - often supplied by the credit arms of their own firms, who are in turn charging high fees to their investors - to buy small companies and then only report to you their (highly subjective) valuations at various protracted intervals. Impatience is not cured by avoiding anything that requires patience. As we have argued in the past, we believe that public markets can offer better investment opportunities than those available to private equity investors, and the fact that the market value of our portfolio companies bounces around every day does not change that. What matters for investors with a long-term focus is simply how much capital they end up with, compared with how much they put in, and how long it takes them to grow that amount of money. What private markets are selling - at a steep price - is enforced long-term thinking. If investors think they can develop this ability on their own, they can save themselves a 2% management fee and possibly earn a better return by turning to public markets. We would urge allocators with private equity investments - who are to some degree self-selecting as long-term investors - to acknowledge to themselves that if they are confident in the long-term prospects of the intrinsic value of their businesses, it does not matter whether the market prices for those businesses swing on a daily or weekly basis. What matters is the potential to buy something for substantially less than it is worth and to sell it, years later, for its true value:

Source: Redwheel. The information shown above is for illustrative purposes. The patience premiumOverall, what public markets offer is fundamentally no different to what investors are accessing in private equity wrappers: ownership of stakes in businesses, the chance to benefit from the growth and success of those businesses, and the talent of their executives. Public markets also tend to offer better liquidity, less leverage, greater transparency, access to larger companies, and all at typically lower prices - if investors are willing to be as patient as private options enforce. After all, corporate valuations are no dinosaurs: even if you can't see them, they move. Sources: [1] For those curious, Tyrannosaurus Rex could probably see motionless prey perfectly well. However, it is here that Crichton's attention to detail is magnificent. The book relays that, where the park scientists were unable to replicate dinosaur DNA, they used frog DNA as the next best thing, a kind of nucleic acid stopgap. As it turns out, some frogs do indeed have difficulty focussing on motionless prey, a detail that Crichton worked cleverly into the storyline of the novel, and which became a memorable line from the film [2] An island where gilet-clad private equity investors run from the EBITDAsaurus and the PIKodocus [3] Which some sceptical commentators might equate with marking your own homework [4] Such as can be found on the websites of many large PE firms (https://www.blackstone.com/en-emea/pws/essentials-of-private-equity/, https://www.kkr.com/alternatives-unlocked/private-equity#2) [5] https://verdadcap.com/archive/explaining-private-equity-returns-from-the-bottom-up?rq=leverage |

|

Funds operated by this manager: Redwheel China Equity Fund, Redwheel Global Emerging Markets Fund |

|

Key Information |

21 May 2025 - Performance Report: Canopy Global Small & Mid Cap Fund

[Current Manager Report if available]

21 May 2025 - The case for small caps: why small companies are set to outperform

|

The case for small caps: why small companies are set to outperform Pendal May 2025 |

|

THE prospect of rate cuts over the remainder of 2025 should buoy small cap stocks, says Pendal portfolio manager Lewis Edgley. Markets are increasingly confident that falling interest rates over the next 12 months will help Australia avoid a prolonged economic downturn, assisted by strong employment and continued immigration. That kind of macro-economic background has traditionally been positive for small caps, which are more cyclical and growth-oriented than their larger counterparts and hence tend to outperform during periods of monetary easing. "We know from experience that when rates go down, small caps, as a category, tend to outperform large caps," says Edgley. "So, if we believe that there's not going to be a recession but there is going to be a rate cutting cycle, then running a small cap fund is going to go from feeling like we've been driving with a hand brake on the last few years to letting the hand brake off and maybe even getting a bit of a wind behind us." Edgley and fellow portfolio manager Patrick Teodorowski co-manage the Pendal Smaller Companies Fund, an actively managed portfolio investing in companies outside the top 100 in Australia and NZ. Stock selection mattersEdgley says investors are often turned off small caps due to the poor performance of the benchmark ASX Small Ordinaries Index, which has returned 5.4 per cent a year over the past two decades, well below the S&P ASX 100's 8.8 per cent return. But the headline performance disguises the fact that the median small cap manager returned 11.15 per cent a year over the same period. "Small cap investing requires time and resources and the index returns have been lower than large caps," he says. "But if you do it well, there's a huge opportunity to add value and beat the broader market return, while benefiting from diversification. "We tell people, focus on earnings, not on macro -- that's where you make money in smalls." Beware cheap stocksEdgley says from a valuation perspective, small caps are currently trading in line with their large cap counterparts, despite historically trading at an 8 to 10 per cent premium. "So, you could say small caps are a bit cheap, and maybe that's a good time to buy." But he cautions that low valuations can be misleading. "Don't be allured into buying cheap stocks. Because they're often cheap for a reason. Might be a bad management team, might be a poor industry, might be a poor capital structure. "We've made money out of cheap stocks in the past, but we've also made money out of buying expensive stocks that get more expensive. "The key is to focus on earnings - if you get that right, you make money." Why earnings matter: Breville vs MyerEdgley says a striking example of the power of focusing on earnings is the long divergence between two household names: Breville and Myer. In the 1970s, both were regarded as standout businesses. Each offered exposure to the Australian consumer, and both were widely seen as credible, reliable options for discretionary spending. But over the decades, their fortunes have sharply diverged. Breville has consistently innovated and delivered on what consumers want, from the 70s cult hit Melitta drip coffee machine to today's fully automated espresso stations. That has delivered sustained earnings growth. "As an investor 15 years ago, you probably would have thought Myer was the bigger, seemingly more credible, safer business to invest in than Breville," says Edgley. "But look what happened. Breville has had a five times increase in its earnings per share over this period, whereas Myer's earnings have faced significant challenges, down almost 90%." However, Edgley notes that Myer is currently embarking on a "self-help" journey, which presents a potential opportunity for improvement. "While Myer has had a tough history, we see a scenario where they could materially improve their earnings through a number of cost and productivity-related improvements that aren't necessarily understood or captured in today's share price," he says. "This reinforces the point that small caps are all about understanding earnings." According to Edgley, both Breville and Myer present as interesting investment prospects today. "Breville continues to have a robust outlook as it innovates and grows into new markets globally while carefully navigating the short-term uncertainties of US tariffs, while Myer has the potential to significantly improve its earnings through strategic internal changes. "Understanding these dynamics is key to making informed investment decisions in the small cap space." Author: Lewis Edgley and Patrick Teodorowski |

|

Funds operated by this manager: Pendal Global Select Fund - Class R, Pendal Horizon Sustainable Australian Share Fund, Pendal MicroCap Opportunities Fund, Pendal Multi-Asset Target Return Fund, Pendal Sustainable Australian Fixed Interest Fund - Class R, Pendal Sustainable Australian Share Fund, Regnan Credit Impact Trust Fund, Regnan Global Equity Impact Solutions Fund - Class R |

|

This information has been prepared by Pendal Fund Services Limited (PFSL) ABN 13 161 249 332, AFSL No 431426 and is current as at December 8, 2021. PFSL is the responsible entity and issuer of units in the Pendal Multi-Asset Target Return Fund (Fund) ARSN: 623 987 968. A product disclosure statement (PDS) is available for the Fund and can be obtained by calling 1300 346 821 or visiting www.pendalgroup.com. The Target Market Determination (TMD) for the Fund is available at www.pendalgroup.com/ddo. You should obtain and consider the PDS and the TMD before deciding whether to acquire, continue to hold or dispose of units in the Fund. An investment in the Fund or any of the funds referred to in this web page is subject to investment risk, including possible delays in repayment of withdrawal proceeds and loss of income and principal invested. This information is for general purposes only, should not be considered as a comprehensive statement on any matter and should not be relied upon as such. It has been prepared without taking into account any recipient's personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation. The information may contain material provided by third parties, is given in good faith and has been derived from sources believed to be accurate as at its issue date. While such material is published with necessary permission, and while all reasonable care has been taken to ensure that the information is complete and correct, to the maximum extent permitted by law neither PFSL nor any company in the Pendal group accepts any responsibility or liability for the accuracy or completeness of this information. Performance figures are calculated in accordance with the Financial Services Council (FSC) standards. Performance data (post-fee) assumes reinvestment of distributions and is calculated using exit prices, net of management costs. Performance data (pre-fee) is calculated by adding back management costs to the post-fee performance. Past performance is not a reliable indicator of future performance. Any projections are predictive only and should not be relied upon when making an investment decision or recommendation. Whilst we have used every effort to ensure that the assumptions on which the projections are based are reasonable, the projections may be based on incorrect assumptions or may not take into account known or unknown risks and uncertainties. The actual results may differ materially from these projections. For more information, please call Customer Relations on 1300 346 821 8am to 6pm (Sydney time) or visit our website www.pendalgroup.com |

20 May 2025 - Performance Report: 4D Global Infrastructure Fund (Unhedged)

[Current Manager Report if available]

20 May 2025 - Glenmore Asset Management - Market Commentary

|

Market Commentary - April Glenmore Asset Management May 2025 After steep falls in March, global equity markets stabilised in April. In the US, the S&P 500 fell -0.8%, the Nasdaq rose +0.9%, whilst in the UK, the FTSE declined -1.0%. Domestically, the All Ordinaries Accumulation index outperformed its global peers, rising +3.60%. On the ASX, the top performing sectors were consumer discretionary (beneficiary of expected interest rate cuts) and banks. The worst performing sector was energy, which was impacted by a -18% fall in the Brent oil price. Growth stocks recovered strongly in April, as investor risk appetite improved following the tariff driven sell off that was the key driver of weak investor sentiment in February and March. April was a very volatile month with the ASX falling sharply in the first week before staging a significant recovery as (in our view) investors realised the sell off was excessive, particularly given many Australian companies are not significantly impacted by Donald Trump's tariffs. In addition, it appears many of the tariffs may end up being less harsh than first announced. Pleasingly the fund was able to take advantage of this volatility by adding to many of its existing holdings at very attractive stock prices. In bond markets, the US 10-year bond yield fell -5 basis points (bp) to 4.16%, whilst its Australian counterpart declined -27 bp to close at 4.11%. The Australian dollar was stronger in April, rising +1.6 cents over the month, closing at US$0.64. The US dollar has been weakening against most major currencies as markets factor in the uncertainty from Donald Trump's tariff policies and their impact on the US economy. Funds operated by this manager: |

19 May 2025 - Performance Report: Cyan C3G Fund

[Current Manager Report if available]