NEWS

9 Jul 2025 - Performance Report: Bennelong Australian Equities Fund

[Current Manager Report if available]

9 Jul 2025 - Australian Secure Capital Fund - Market Update

|

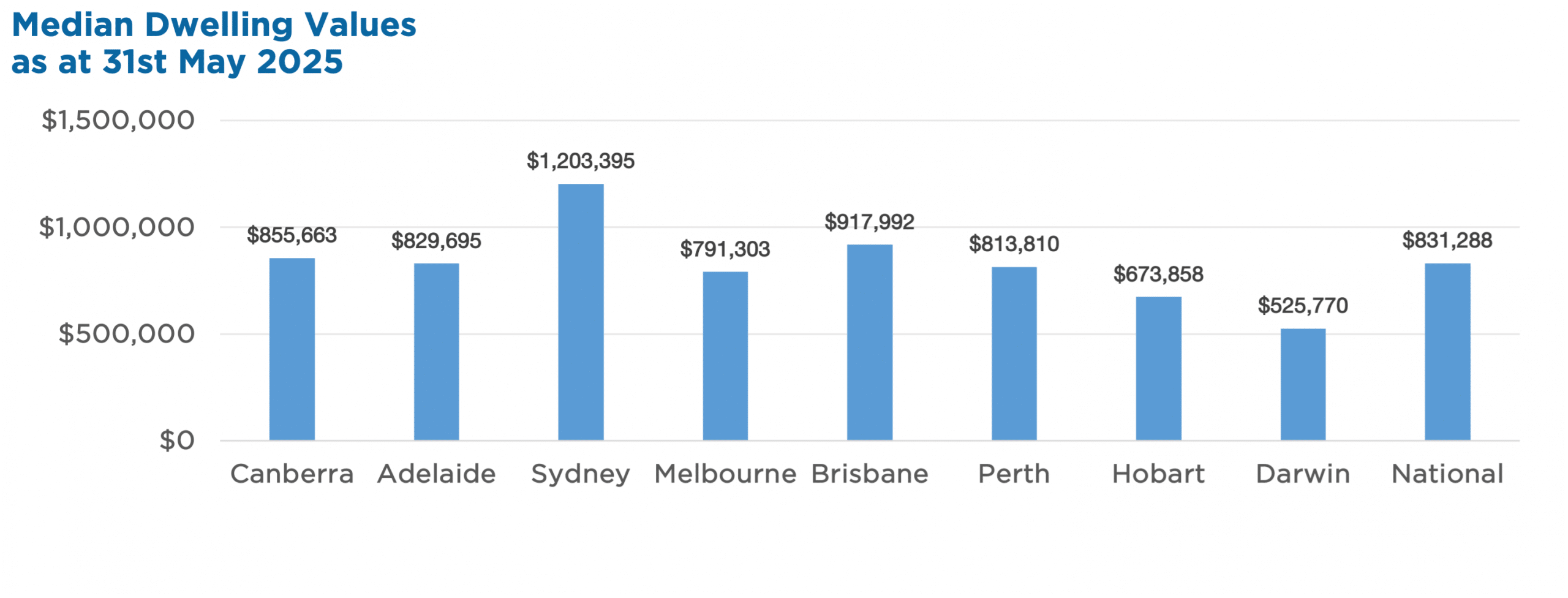

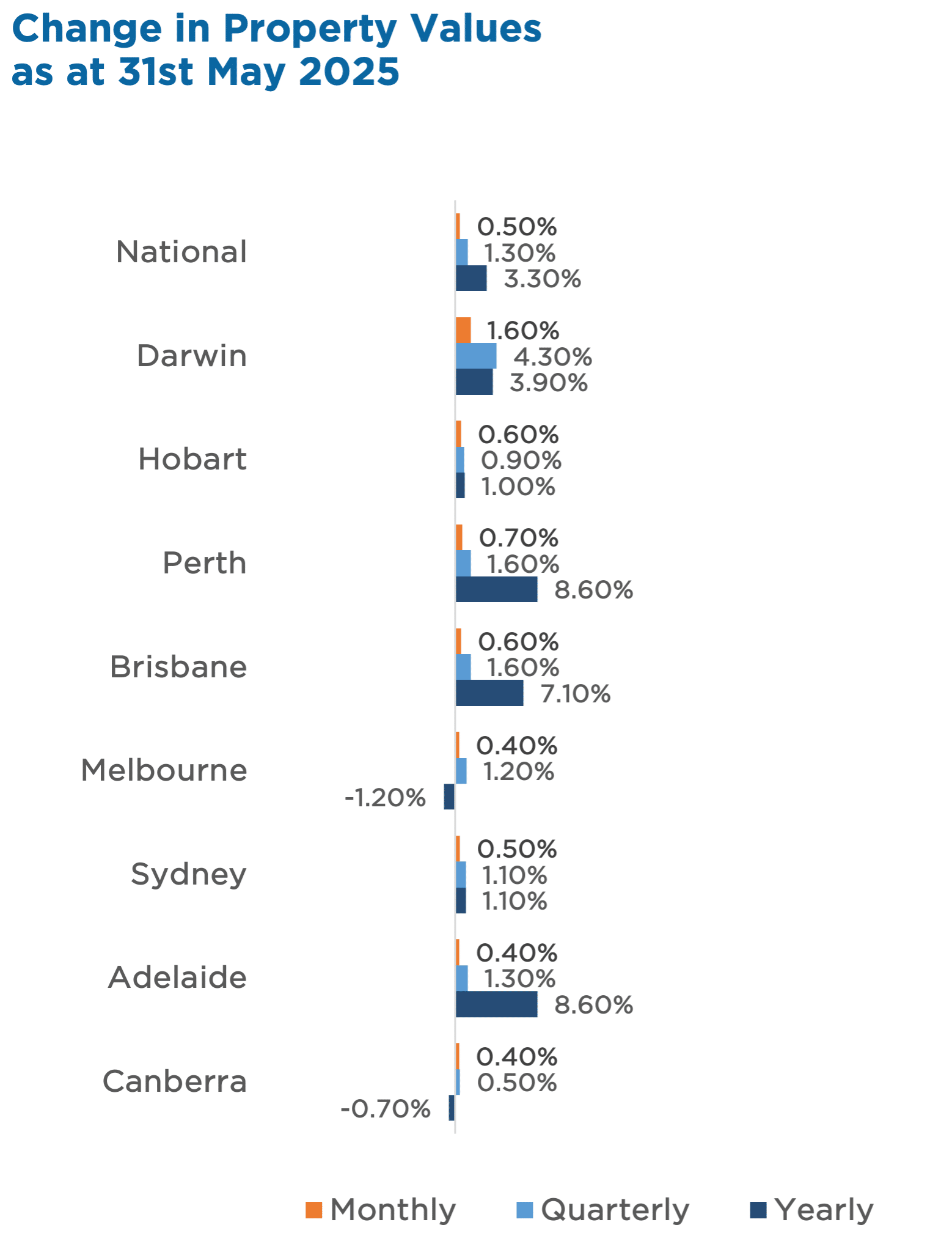

Australian Secure Capital Fund - Market Update Australian Secure Capital Fund June 2025 National housing values rose another 0.5% in May, bringing total growth to 1.7% so far in 2025, with every capital city in positive territory. The market appears to be responding to recent and anticipated interest rate cuts, with auction clearance rates also picking up post-RBA's May meeting. While annual growth has softened to 3.3%, even previously flatlining cities like Melbourne and Canberra are edging back into growth. Regionally, SA is leading the charge, up 5.8% year-to-date, while higher-end property segments in Sydney and Canberra are now outpacing entry-level growth. With values rising across capital cities and regions, many investors are keeping a close eye on how interest rates and housing supply may influence the months ahead. Property Values as at 31st of May 2025

Median Dwelling Values as at 31st of May 2025 June Edition Funds operated by this manager: ASCF Select Income Fund , ASCF High Yield Fund , ASCF Premium Capital Fund , ASCF Private Fund

|

8 Jul 2025 - Performance Report: DS Capital Growth Fund

[Current Manager Report if available]

8 Jul 2025 - News & Views: Oil spikes and geopolitics - How does Global Listed Infrastructure fare?

4 Jul 2025 - Hedge Clippings | 04 July 2025

|

|

|

|

Hedge Clippings | 04 July 2025

News | Insights Expert analysis on what the RBA will do next Tuesday | FundMonitors.com 10k Words | June 2025 | Equitable Investors May 2025 Performance News |

|

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday |

4 Jul 2025 - Preview of RBA Board Meeting Decision, Friday, 4th July, 2025

|

Preview of RBA Board Meeting Decision, Friday, 4th July, 2025 FundMonitors.com July 2025 |

|

Summary In the lead-up to the Reserve Bank of Australia's (RBA) July policy meeting, Chris Gosselin, CEO of FundMonitors.com, hosted Nicholas Chaplin from Seed Funds Management, and Renny Ellis from Arculus Funds Management to assess the likelihood and implications of a rate cut. Despite soft inflation data for May (2.1%), both urged caution, highlighting the strength of the labour market, rebounding housing prices, and the broader economic stability. While markets are pricing in a cut, Chaplin and Ellis questioned the need for further easing given the current conditions, pointing out that GDP softness-not inflation-may be the real concern. They also compared the RBA's stance with the U.S. Federal Reserve, concluding that domestic factors should drive policy, not international pressure. Conclusion: Both Nicholas Chaplin and Renny Ellis advocate a "wait and see" approach. Despite market expectations, they caution that economic fundamentals do not yet warrant aggressive easing, especially with employment strong and inflation stable. Growth concerns exist, but the RBA has room to observe data and remain flexible in its response. Key Points: 1. Inflation and RBA Mandate

2. Labor Market Strength

3. Economic Growth Concerns

4. Housing and Asset Markets

5. Electricity Subsidies and Policy Interpretation

6. RBA vs. Federal Reserve (Fed)

7. Market Expectations

8. Recommendations from the Panel

Full Transcript: Chris Gosselin: The RBA board meets next Monday, and following two days of deliberations, they're expected to announce their decision at 2:30 PM on Tuesday afternoon. To preview that decision, I'm joined today by two experienced fund managers in the fixed income space: Nicholas Chaplin, Director and Portfolio Manager at Seed Funds Management; and Renny Ellis, Director and Head of Portfolio Management at Arculus Funds Management. Gentlemen, welcome. We're here to unpack what the RBA might decide, with markets almost unanimously pricing in a rate cut from the current 3.85%. Monthly inflation data for May was surprisingly soft at just 2.1%-well within the target range-fueling expectations of a cut. But with unemployment just over 4% and ongoing global uncertainty, is now the right time to ease? Let's dive in. Nick, let's start with you. Inflation came in at 2.1%, well below expectations. Do you think that gives the RBA enough justification to cut rates now? Nicholas Chaplin: I think Michele Bullock addressed this quite clearly on May 20 in her post-meeting media discussion. She stated that the "narrow path" narrative on inflation should be removed from their commentary-they've essentially achieved that goal. Yet interestingly, that didn't stop some banks from forecasting up to three more rate cuts this year. The rate cut in May seemed to acknowledge that CPI had reached the mid-to-low twos, which was justified when the 2.1% figure came out. But Bullock also highlighted strong labor market conditions, rising household expenditure, and a rebounding housing market. We're seeing price rises in housing across the country, which will need to be factored in-especially if CBA, NAB, or Westpac are right about a terminal rate around 3% or even 2.85%, and getting there quickly. However, the bigger driver for me is the weak GDP figure-just 0.2% in the March quarter and 1.3% annually. That's low by historical standards, though not unprecedented for Australia. That's where my concern lies and why I think a cut in July is justifiable. While many predict a 100% chance of a cut in July and 90% for August, I hold a slightly different view, which I'll explain further. But yes, in my opinion, the justification for a cut is there-more due to growth concerns than inflation. Chris Gosselin: Renny Ellis: I don't see pressing reasons to cut in July. That said, I suspect they probably will-bank bill swap rates are already trading around 3.6%. I agree with much of what Nick said, but I'd add that the RBA has indicated they'd look through the distortions caused by federal and state electricity subsidies, which have significantly impacted inflation data since March last year. Asset prices are strong, the share market is at a record high, credit margins are tight, and the yield curve is steep-all signs of a strong economy. Given unemployment is low, I don't see a need to cut. If they do, I doubt they'll follow with another. Chris Gosselin: Renny Ellis: Nicholas Chaplin: Renny Ellis:

The main downside risk she mentioned was geopolitical uncertainty. Nicholas Chaplin: Renny Ellis: Chris Gosselin: Nicholas Chaplin: Renny Ellis: Chris Gosselin: Nicholas Chaplin: Renny Ellis: The yield curve could flatten slightly, particularly in the 5- to 10-year segment. We'd also see a spike in the Australian dollar, which is disinflationary. I don't expect much impact on equity markets from the decision. Chris Gosselin: Nicholas Chaplin: Renny Ellis: But keep in mind, she's only one member of the board. The final decision is collective. Nicholas Chaplin: Chris Gosselin: Let's wrap it up there. The RBA's new two-day meeting format begins on Monday, with the decision due at 2:30 PM on Tuesday. We'll reconvene then to discuss the outcome. Nicholas Chaplin from Seed Funds Management, Renny Ellis from Arculus Funds Management-thank you both for your time. Watch the full video here. |

4 Jul 2025 - Expert analysis on what the RBA will do next Tuesday, July 8

|

Expert analysis on what the RBA will do next Tuesday, July 8 FundMonitors.com July 2025 |

|

Chris Gosselin, CEO of FundMonitors.com, speaks with Nicholas Chaplin, Director and Portfolio Manager at Seed Funds Management and Renny Ellis, Director & Head of Portfolio Management at Arculus Funds Management. With the RBA widely expected to cut rates next week, the discussion explores whether inflation, GDP weakness, and labor market strength justify a move--or argue for patience. Both managers weigh the risks of overstimulating the economy versus acting too late, in the context of local and global dynamics. |

4 Jul 2025 - FOMC: projections highlight heightened uncertainty in rate outlook

|

FOMC: projections highlight heightened uncertainty in rate outlook Nikko Asset Management June 2025 Fed keeps rates on hold, projects a mildly more optimistic outlookThe Federal Open Market Committee (FOMC) kept interest rates on hold as expected at its June meeting. The June monetary policy statement had a mildly more optimistic outlook compared to May. The latest statement noted that "heightened risks of both higher unemployment and inflation" cited in May "diminished but remain elevated". However, the June Summary of Economic Projections (SEP), compared to the March release, indicates that the direction of the economy has shifted to a lower-growth, higher inflation environment in the short term. Growth and employmentAt the post-FOMC press conference Federal Reserve (Fed) Chair Jerome Powell described current conditions as "solid", saying that the 4.2% unemployment rate "remains low". Powell pointed out that real wages are still in positive territory. However, he also cited the SEP's projection for the unemployment rate to reach 4.5% by the end of the year; conditions are expected to worsen. Meanwhile, recent GDP data have not been useful reference to gauge trend developments, with investment surging and net exports skewed by front-loaded imports ahead of anticipated tariffs. On the other hand, the consumption component was softer, and PDFP (private domestic financial purchases) growth was reliant on domestic investment to expand at a healthy rate of 2.5% in Q1. Because investment was driven by anticipation of tariffs, a temporary factor, its contribution is likely to decrease. Notably, growth expectations were shifted lower in June (1.4-1.5%) vs. March (1.6-1.7%). Projections for unemployment in 2025 remains at 4.4-4.5%, reflecting a more defined central tendency. Inflation: the big unknownPowell said inflation "eased significantly" from highs in 2022, but "remains somewhat elevated" compared to the Fed's 2% target. However, he also noted that near-term inflation expectations have "moved up" in recent months, with tariffs a big "driving factor". Although the SEP's total PCE inflation projection of 3% was higher than March, the Fed Chair expected the inflation rate to subside in the longer-term. The uncertainty associated with such an outlook, however, may make the FOMC's rate trajectory highly unpredictable. The mode in inflation expectations moved higher from 2.7-2.8% to 2.9-3%, with both upside and downside risks becoming more prominent. The full range of expectations remains clearly above 2% in 2025 and 2026, subsiding to around target level in 2027, albeit with some upside tail risks. We also note that while FOMC members' diffusion indices assessing uncertainties regarding unemployment and GDP decreased somewhat after March's substantial increase, uncertainty over inflation remained elevated at levels similar to those in March. Majority of members see two rate cuts in 2025 but outlook more disperseThe FOMC's median projection for the Fed Funds rate by the year-end remains 3.9%, unchanged from the March projection. The longer-term projection for 2027 was raised modestly to 3.4%. Ten of the 19 FOMC members see at least two rate cuts in 2025, while the number of those who do not expect the Fed to cut at all this year rose to seven from four in March. The varied projections highlight the elevated uncertainty in the outlook for the Fed Funds rate. For now, it appears that the FOMC remains data-dependent, with the main focus on the uncertainty over near-term inflation expectations. The FOMC's statement and SEP align with the central scenario of slower growth with trade détente outlined in our Global Investment Committee review: scenarios for a less certain global outlook. However, persistent uncertainty means that the probability of scenarios involving stagflation or recession with disinflation remains well above zero. Funds operated by this manager: Nikko AM Global Share Fund , Nikko AM ARK Global Disruptive Innovation Fund , Nikko AM NZ Cash Fund , Nikko AM NZ Corporate Bond Fund , Nikko AM Core Equity Fund (NZ) , Nikko AM Global Shares Hedged Fund (NZ) , Nikko AM KiwiSaver Scheme Balanced Fund (NZ) , Nikko AM ARK Disruptive Innovation Fund (NZ)

Important disclaimer information Please note that much of the content which appears on this page is intended for the use of professional investors only. |

3 Jul 2025 - How A Second-hand Car Salesman Taught Me About Stock Market Psychology

|

How A Second-hand Car Salesman Taught Me About Stock Market Psychology Marcus Today June 2025 |

|

I used to work for a second-hand car salesman called Alex who specialised in Classic Cars. Jaguar XKs, E-Types, Aston Martins, AC Cobras, Trans-Ams, Austin Healeys, anything that an investment banker would impulse purchase (or at least, used to, in the 1980s). The name of the game was a lesson in stock market psychology. There are two things you had to do right: buy the car and sell the car. But of course, things were different in the 1980s, and the big advantage for a good salesman like Alex was that the "true value" of Classic old cars didn't really exist. There was no internet in those days, and for a second-hand car salesman, the ignorance of his customers was bliss. It was much like the stock market today, people purport to put a 'value' on a stock but ultimately they rely on a lot of rubbery assumptions which means the valuation is not 'truth' it is simply a negotiating tool in a sale and all that really matters in the end is the price someone is prepared to pay and the price someone is prepared to sell. Making money trading Classic Cars was the same as making money trading stocks; it was all about taking advantage of other people's emotions by creating fear in a seller and selling into a buyer's euphoria. Buying First - Create FearBuying first. For Alex, the main game was to create 'depression' and to do that, you had to know your stuff or at least sound as if you did, and Alex had developed a 'naked script' he could pretty much rely on whatever the car. Confronted by an emotional amateur selling their pride and joy Alex's job, indeed his amusement, was to beat them down from a "Glorious example of a Classic Car" to a rusty old lump of crap owned by a deluded fool. In the second-hand classic car market, the skill is to generate fear. In the stock market, the money is in recognising it, recognising the points of maximum fear or euphoria. Selling Was Easy - Wait for the StarsAs far as selling was concerned, that was easier, in fact it was so easy Alex could delegate it to a Muppet like me. All he did was re-spray and re-chrome and tell us to wait for an investment banker with a bonus in their back pocket and (the expression was) "Stars in his eyes" to come along, be blinded by the shiny paintwork and new chrome and pay a lot more than the metal millstone had actually cost. And if someone came in with an Austin Healy owners Club T-Shirt and opened with the comment that "the next thing to go will be the tie rod ends", we were told to simply usher them politely off the showroom floor with a smile. You don't have to sell. Eventually, someone with "Stars in their eyes" always turned up. The Stock Market Is Just Like a Car YardMaking money in stocks is the same. It is not about fundamental value, as hordes of finance industry automatons would have you believe; it is about taking advantage of other people. People with stars in their eyes who have inflated a bubble, and people consumed by fear, dumping stocks at any price. It's about inaccurate pricing, not accurate pricing. It's about timing. It's about selling stocks as a bubble bursts and buying them at peak distress. It's about exploiting the herd, not joining the herd. As the Wolf of Wall Street says, investors are sheep, and sheep are for slaughter. Be the Wolf. Be Alex. DISCLAIMER: This content is for general information purposes only and does not constitute personal financial advice. Please consider your own circumstances or seek professional advice before making investment decisions. |

|

Funds operated by this manager: |

2 Jul 2025 - Performance Report: Equitable Investors Dragonfly Fund

[Current Manager Report if available]