NEWS

9 Jul 2026 - Performance Report: Seed Funds Management Financial Income Fund - Incl Franking

[Current Manager Report if available]

9 Jul 2026 - Performance Report: Bennelong Australian Equities Fund

[Current Manager Report if available]

9 Jul 2026 - Equities outlook: Balancing AI's promise and near-term macro risk

|

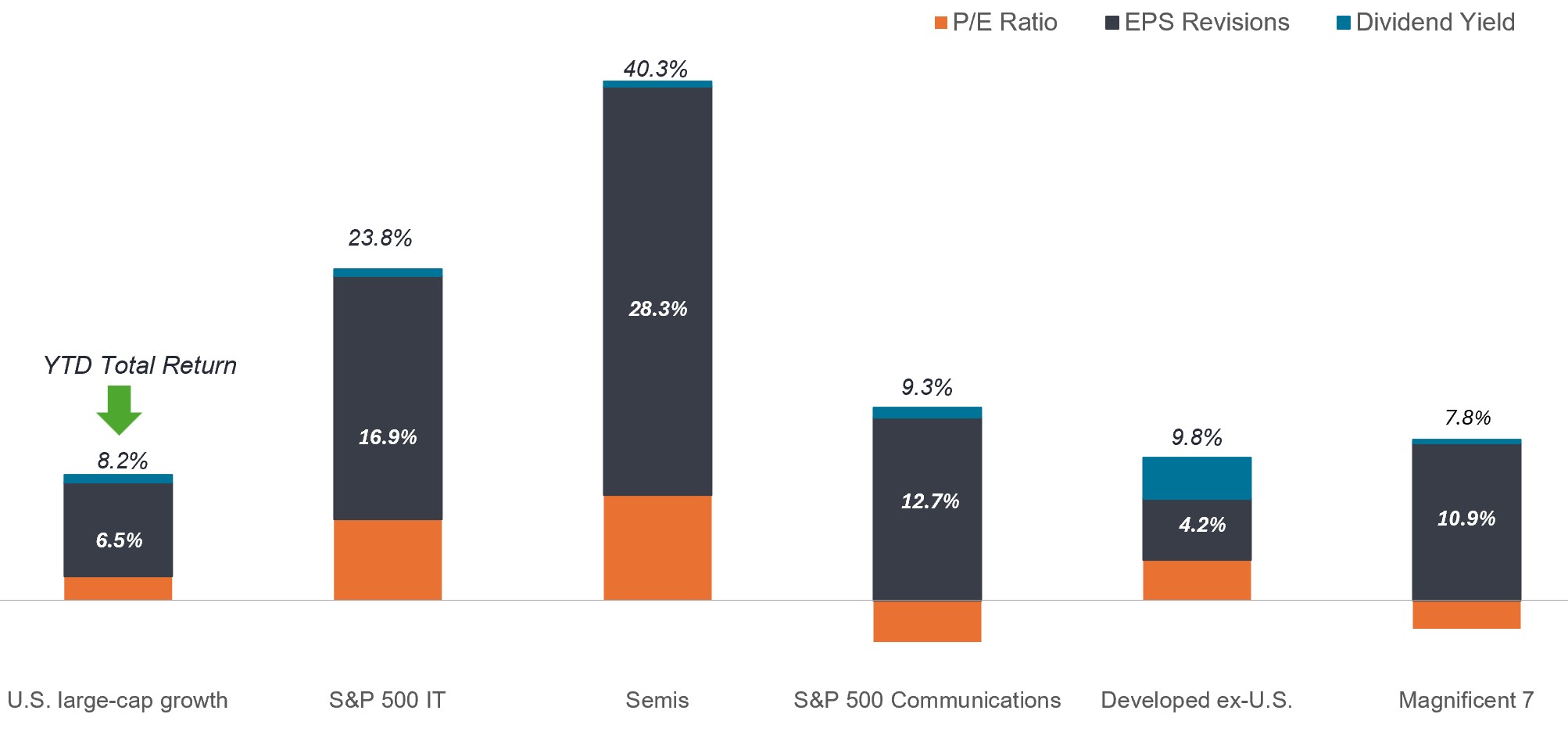

Equities outlook: Balancing AI's promise and near-term macro risk Janus Henderson Investors June 2026 (8-minute read) Head of EMEA and Asia Pacific Equities Lucas Klein and Head of Americas Equities Marc Pinto discuss how uncertainty around the artificial intelligence (AI) buildout and geopolitical conflict may allow investors to capitalize on price dislocations within these and other, underappreciated, themes, creating opportunities for excess return. Two developments have framed global equity markets in 2026: The continuation - and perhaps surprising strengthening - of the AI infrastructure buildout and the outbreak of hostilities in the Middle East. As evidenced by numerous stock indices having reached record highs in the second quarter, the market is largely embracing the former while shrugging at the latter in the hopes that the associated energy price shock will be short lived. Given the degree to which equities are reacting to these unfolding events, one could be forgiven for thinking that there is little point in fighting consensus by seeking differentiated, company-specific views that go against the prevailing narrative. We, however, believe current market and corporate dynamics are more complex than what's reflected in the headlines. It is, after all, in periods of persistent macro risk and seemingly one-way trades that investors can capitalize on price dislocations within underappreciated themes and individual securities, which can often lead to excess return opportunities over the long term. To be sure, market concentration and persistent inflation are factors investors cannot ignore. And our sentiment is more cautious than it was six months ago. But financial markets are the aggregation of thousands of companies and millions of transactions, and they are constantly absorbing new information about the corporate, economic, and geopolitical environment. While uncertainty has risen, in our view, a complicated and rapidly evolving environment creates opportunities for investors to be proactive by positioning portfolios for the future. The AI buildout: From strength to strength In late 2025, two questions hung over the AI theme: Was the scale of the infrastructure buildout too much too soon, and when could hyperscalers expect monetization from their massive investment? Fast forward six months and those many of those concerns have been assuaged. Demand at every stage of the AI value chain exceeds supply. This includes backlogs for the most advanced graphics processing units (GPU) and end users lining up to access hyperscalers' newest models. This latter development is resulting in revenue growth that exceeds most analysts' expectations. The upshot is one of the strongest earnings revisions cycles in decades. Exhibit 1: Equity earnings upgrades In contrast to the last three years, when earnings were revised downward even in the categories below - with the Magnificent 7 being the exception - 2026 earnings estimates have been materially upgraded over the past five months.

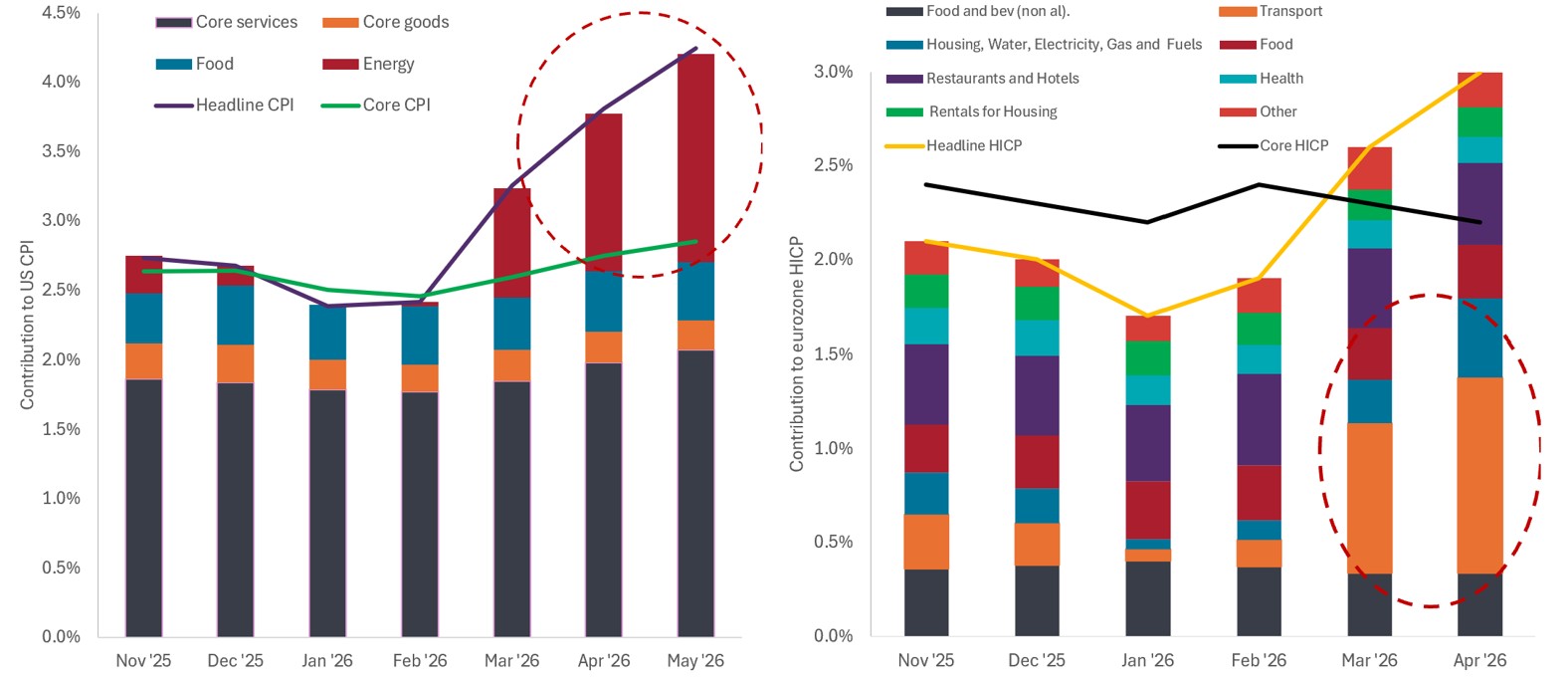

Source: Bloomberg, Janus Henderson Investors, as of 29 May 2026. U.S. large-cap growth represented by the Russell 1000 Growth Index; Semis represented by the S&P 500 Semiconductors Sub-Industry Index; Developed ex-U.S. represented by the MSCI EAFE Index. The expanding capabilities behind the voracious demand for these models is underpinned by a wider-than-expected set of technical inputs. In this year's most telling example, AI inference has been shown to require an underappreciated number of central processing units (CPUs) and memory chips, resulting in significant bottlenecks for these components. This revelation comes on the heels of hyperscalers' race to procure sufficient energy to power their data centers. As AI models become even more sophisticated and further permeate the global economy, we expect additional bottlenecks to emerge. This presents an opportunity for investors to apply deep industry knowledge to identify constraints early and position portfolios accordingly. Another potential AI-related development investors should be mindful of is a repeat of the type of disruption that recently roiled the software industry. As use cases are applied to other industries, we expect additional events like this to occur, as disruption is the tradeoff for reaping the productivity gains promised by AI. But as with the software episode, once the possibility of disruption is recognized, the market often reacts quickly, selling first and asking questions later. This elevator down, stairs up mentality can create opportunities in oversold stocks whose underlying businesses could prove resilient to, if not fortified by, AI. The global economy has been through periods of profound technological change before, although perhaps not at the scale or velocity exhibited by AI. These early days are being led by AI enablers - infrastructure companies and models architects. Investors are anxious to see evidence of productivity gains leading to earnings growth across sectors - via AI enhancers and especially end users - but, at present, any margin expansion would be dwarfed by the AI hyperscalers' historic revenue generation. The long shadow of higher energy prices A tenuous ceasefire and front-month Brent crude futures roughly 20% off their crisis highs have caused many market participants to hope that the economic impact of the Middle East conflict will be short lived in most regions. We believe this will prove too sanguine of an outlook. Even if a lasting cessation of hostilities can be achieved - and that is far from certain - we expect energy prices, and thus global inflation, to remain elevated for much of the rest of the year. The knock-on effects of such an outcome would be far ranging. Foremost, consumption and corporate margins in regions highly dependent on energy imports would suffer. Europe and much of Asia are at the top of that list. And while U.S. consumption remains steady, we are already seeing signs of stress in the value segment. With gasoline prices above $4 per gallon, every dollar going into a tank is one less available for other categories. Even without oil surging past $100 per barrel, the steady headwind of elevated gas prices could weigh on consumers during the important holiday travel and back-to-school seasons. Exhibit 2: Inflation biting in the eurozone and U.S. The duration of energy-driven inflation in the eurozone and U.S. will largely determine how consumers adjust their buying patterns and when - and to what degree - these regions' respective central banks will have to react with policy adjustments.

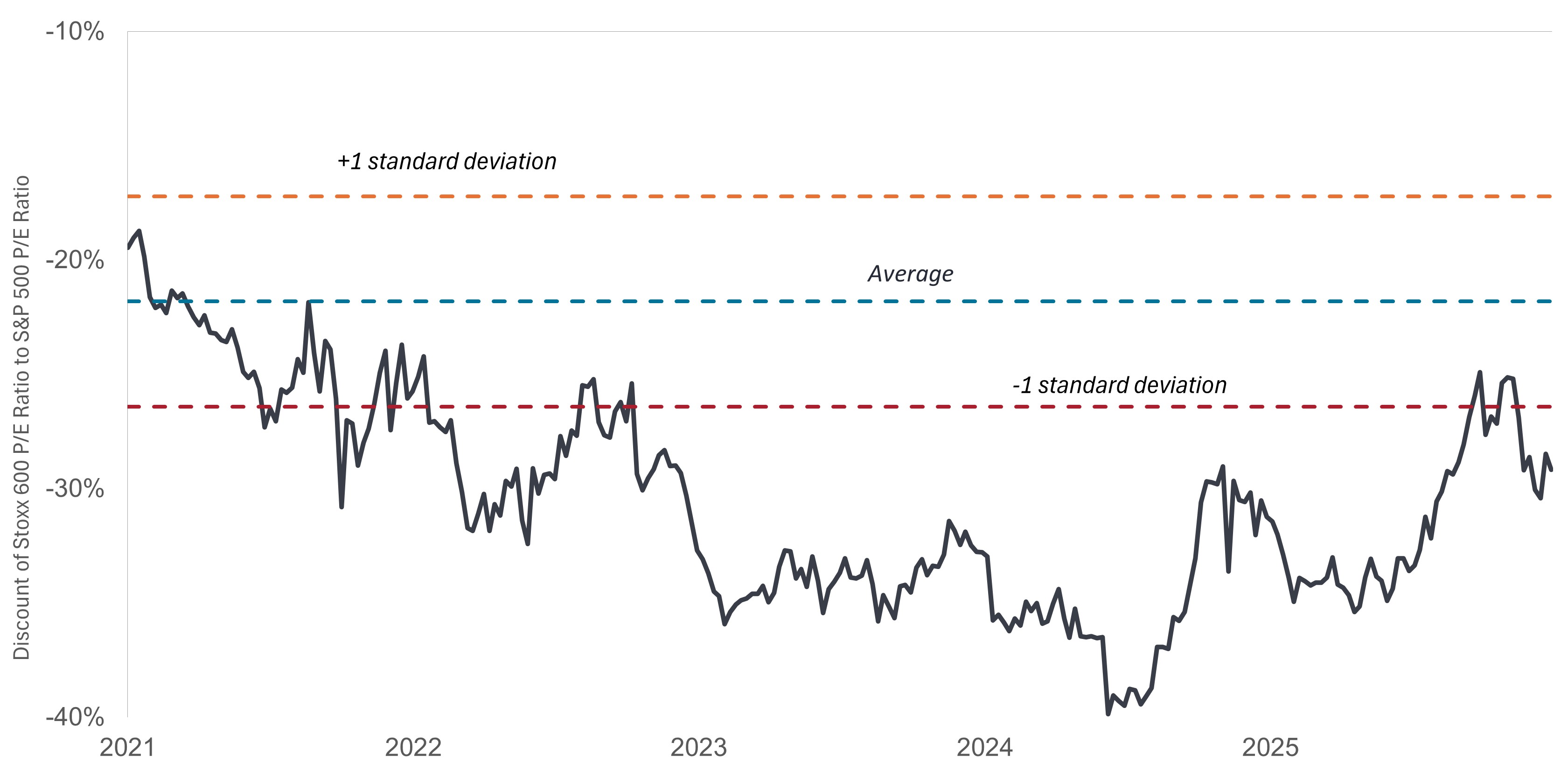

Source: Bloomberg, Janus Henderson Investors, as of 8 June 2026. The duration of high energy prices is likely to be the swing factor in the future trajectory of monetary policy. Entering the year, most major central banks were on track to cut rates to support a late-cycle economy. Now, market-implied estimates indicate the Bank of England and European Central Bank could raise rates up to two and three times, respectively, by the end of the year. And given their inflation mandate, they would have to do this despite already flagging economic prospects. While the U.S. may not be compelled to raise rates as quickly (if at all), its economy is unlikely to receive the hoped-for tailwind of lower interest rates. Not only would this diminish households' ability to benefit from lower borrowing costs, but it also undermines our earlier expectation for an equity market broadening, partly premised on typically leveraged small caps enjoying more favorable financing terms. Europe: One step forward, two steps... Higher interest rates will continue to be a headwind for the eurozone. Another comes in the form of economic reforms progressing more slowly than anticipated. The holdup is found in the banking and regulatory reforms aimed at making the European marketplace more competitive. In contrast, by necessity, the defense component of the banks and tanks initiative continues to move forward. Major European countries, chiefly Germany, recognize the need to fortify their defense capabilities, including domestic arms production, and are willing to run deficits to fund them. The Trump administration's continued ambiguity toward the North Atlantic Treaty Organization likely makes European defense an enduring theme, regardless of how the Ukraine conflict turns out. Much of our earlier favorable view on European markets was based on the potential for pro-business reforms. But another factor was the considerable discount at which European stocks have traded to their American counterparts for the past several years. That discount has narrowed considerably over the past 18 months, diminishing the argument that value alone was a reason to consider European exposure. Exhibit 3: European equities discount to U.S. stocks With Europe's valuation discount to the U.S. narrowing, the next boost for the continent's stocks will have to come from substantive pro-business reforms rather than arguing that equities are cheap.

Source: Bloomberg, Janus Henderson Investors, as of 29 May 2026. When looking at European economic conditions in isolation - including lower exposure to the AI theme - one can conclude that the region's stocks trade at a discount to the U.S. for a reason. That, however, ignores the fact that a large portion of European earnings are derived from either exports or European multinationals' global operations. In this respect, European exposure continues to represent a viable method to access attractive investment themes and global earnings streams. China finding its footing? After an extended period of tepid stock performance and worrisome economic developments, China has shown signs of progress. Part of the reason is the central government inching away from its emphasis on national service at the expense of a company's economic priorities. Beijing is again recognizing that a less encumbered private sector acting in its own commercial interest can improve a nation's economic position and social outcomes. This is most evident in innovation-centric fields like AI, biotechnology, and electric vehicles (EV). The country still must work though the vestiges of its housing overhang, and the government's typical reflex in these instances is to lean into exports. This is, in fact, part of China's current strategy in the wake of U.S. tariffs. To compensate for duties, exports have increased to other emerging markets, where some components invariably find their way to the U.S., but under more favorable terms. A star of corporate China continues to be its commanding position in EVs and batteries, both of which have gained footholds in markets across the world. Balancing the secular and the cyclical A market repeatedly eclipsing record highs on the back of a handful of AI-related companies is no reason in itself to be circumspect about stocks' prospects. This year's gains are, after all, rooted in solid fundamentals, namely materially higher earnings revisions. Still, equities' swagger belies some uncertainty. What sector will AI disrupt next, and how will corporate managers - and investors - react? Although there have been larger episodes in the past, how will the market absorb the initial public offering pipeline, including those of major AI platforms? Lingering inflation and potentially more restrictive monetary policy are legitimate headwinds. Granted, the U.S. stock market does not look entirely like the U.S. economy - with consumption being a much larger share of the latter - but stress from higher energy prices could eventually impact the purchasing decisions of higher-income households. High-end consumption remains strong, but in perhaps a nod to any workplace dislocations AI may cause, will that be enough to carry the broader U.S. economy? These are issues policymakers and investors must monitor as AI becomes more prevalent. There are invariably winners and losers in periods of rapid technological transition. Even within tech, there will be both. The analytical potential of AI could create even more winners in biotech innovation as models tackle the complexities of medical sciences. Over the remainder of 2026, the market will have to balance two opposing forces. On one side, the possible cyclical headwinds of a prolonged military conflict, inflation, and higher interest rates may very well weigh on near-term economic growth. On the other, the secular theme of AI could live up to its promise of being a force multiplier for global productivity. Neither of these trends is on a set path, and each will likely deliver unexpected developments, and thus bouts of volatility, along the way. IMPORTANT INFORMATION Aerospace and defense industries can be significantly affected by changes in the economy, fuel prices, labor relations, and government regulation and spending. Artificial intelligence ("AI") focused companies, including those that develop or utilize AI technologies, may face rapid product obsolescence, intense competition, and increased regulatory scrutiny. These companies often rely heavily on intellectual property, invest significantly in research and development, and depend on maintaining and growing consumer demand. Their securities may be more volatile than those of companies offering more established technologies and may be affected by risks tied to the use of AI in business operations, including legal liability or reputational harm. Equity securities are subject to risks including market risk. Returns will fluctuate in response to issuer, political and economic developments. Foreign securities are subject to additional risks including currency fluctuations, political and economic uncertainty, increased volatility, lower liquidity and differing financial and information reporting standards, all of which are magnified in emerging markets. Technology industries can be significantly affected by obsolescence of existing technology, short product cycles, falling prices and profits, competition from new market entrants, and general economic conditions. A concentrated investment in a single industry could be more volatile than the performance of less concentrated investments and the market as a whole. Consumer Price Index (CPI) is an unmanaged index representing the rate of inflation of the U.S. consumer prices as determined by the U.S. Department of Labor Statistics. Dividend Yield is the weighted average dividend yield of the securities in the portfolio (including cash). The number is not intended to demonstrate income earned or distributions made by the portfolio. Inflation: The rate at which the prices of goods and services are rising in an economy. The Consumer Price Index (CPI) and Retail Price Index (RPI) are two common measures. The Magnificent 7 stocks include Alphabet, Amazon, Apple, Tesla, Meta Platforms, Microsoft, and NVIDIA. Monetary Policy refers to the policies of a central bank, aimed at influencing the level of inflation and growth in an economy. It includes controlling interest rates and the supply of money. MSCI EAFE® (Europe, Australasia, Far East) Index reflects the equity market performance of developed markets, excluding the U.S. and Canada. Price-to-Earnings (P/E) Ratio measures share price compared to earnings per share for a stock or stocks in a portfolio. Russell 1000® Growth Index reflects the performance of U.S. large-cap equities with higher price-to-book ratios and higher forecasted growth values. S&P 500® Index reflects U.S. large-cap equity performance and represents broad U.S. equity market performance. S&P 500 Semiconductors Sub-Industry Index® tracks the performance of the semiconductor and semiconductor equipment manufacturers listed on the S&P 500. STOXX® Europe 600 Index represents large, mid and small capitalization companies across 17 countries in the European region. Volatility is the rate and extent at which the price of a portfolio, security or index, moves up and down. If the price swings up and down with large movements, it has high volatility. If the price moves more slowly and to a lesser extent, it has lower volatility. The higher the volatility the higher the risk of the investment. |

|

Funds operated by this manager: Janus Henderson Australian Fixed Interest Fund , Janus Henderson Conservative Fixed Interest Fund , Janus Henderson Diversified Credit Fund , Janus Henderson Global Natural Resources Fund , Janus Henderson Tactical Income Fund , Janus Henderson Australian Fixed Interest Fund - Institutional , Janus Henderson Conservative Fixed Interest Fund - Institutional , Janus Henderson Cash Fund - Institutional , Janus Henderson Global Multi-Strategy Fund , Janus Henderson Global Sustainable Equity Fund , Janus Henderson Sustainable Credit Fund All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect. The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested. Whilst Janus Henderson believe that the information is correct at the date of publication, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson to any end users for any action taken on the basis of this information. |

8 Jul 2026 - The hidden danger of leveraged ETFs

|

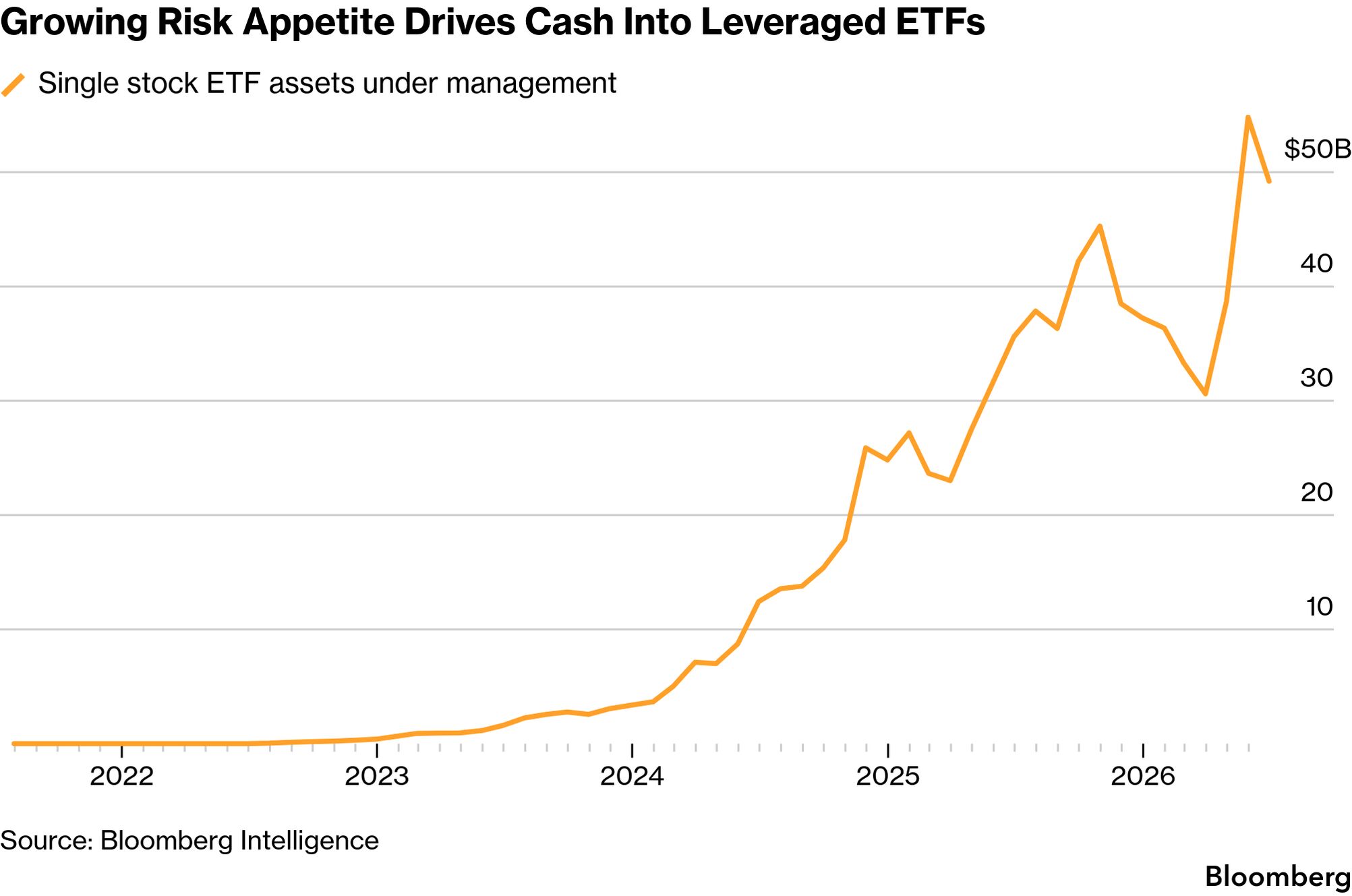

The hidden danger of leveraged ETFs Marcus Today June 2026 5-minute read I think that ETFs are a wonderful invention. They enable retail investors to get exposure to international markets, sectors and themes. Brilliant stuff and obviously has been a huge success. But success has many fathers, and huge success has many players. Competition is fierce for ETF dollars. These fund managers want your money. The fees are low (part of the attraction), so you need lots of dollars to make it work. The same infrastructure is required to manage $1bn as $100m. The same models and mechanisms. But competition can be fierce. As a result, they come up with ever more exotic themes, ever more exotic sectors and, worst of all, leveraged ETFs. These can include SNAS or LNAS. These offer leverage of around 2-2.5 times the index move. But when things get weird, worrying is the level of leverage that some providers offer in other markets. Korea is a case in point. When leverage turns against youIt is only fabulous when the market goes up, and leverage magnifies the underlying index moves. It is a bit like an option position. As the market goes up, the sellers of these ETFs are getting shorter and shorter due to the leverage. So they have to keep buying to stay hedged. This pushes the market higher and higher. The trouble is that when things unravel, they tend to unravel quickly. The market makers get longer as it goes down, and so have to rebalance and sell. Couple that with the pain from investors, and it can cascade lower. The Korean market has a huge level of leverage with new products in Samsung and SK Hynix. That is why we saw a 10% fall in the KOSPI yesterday. It feeds on itself. Even the regulator that approved these highly leveraged products has said maybe it wasn't his greatest idea! That is a stark admission. That is something that is supposed to be said in an "inside" voice! Nomura estimates leveraged ETFs now broadly generate about $9 billion of rebalancing demand for every 1% move in the market.

Korea set off the US sell-off. Everything is connected after all. At their May launch, the 16 ETFs tracking the chipmakers in Korea had combined assets of US$3bn. To date, these have ballooned to more than US$9bn. What is also troubling in all this leverage is that they are very popular with retail investors who may not be that experienced in risk management. Just rolling the dice to get rich or die trying! Up until recently, it has worked. Until recently. Leverage is a wonderful thing when it is going well. When it turns, it can be a very sub-optimal experience. And it can unwind the popular trades very quickly. That's what we are seeing at the moment. Those crowded trades unwound at breakneck speed.

The real cost of the AI boom I wrote yesterday about the AI issue. That is the cost of it. It is huge. There is probably going to be a trillion dollars chucked at it this year. That requires a payback. Companies that embrace AI have to see the returns because it is expensive. And do you need a hammer gun to knock in one nail? Does "free" ChatGPT do the job, or do you need advanced Claude models to run your business? And if you are paying a fortune for your AI bots and models, do you need humans? Low value human capital. Like the reverse of the Taco Kid ad. You can't have both. What is the point? It is like buying a designer dog and then wishing you had a rescue one! If you only want one dog, that is. The goal is to save money and be more productive. The big tech stocks have gone from being massive holders of cash to issuing debt and equity to pay for all the spending! That is a significant change to the models. From cash hoarders to Shirley Bassey stocks. Big spenders. I use ChatGPT; I am not a complete Luddite, but for my requirements, it does a pretty good job. I am not into just posting AI stuff. It is nice to think about things. What does compute actually cost?The concern I have is how much does "compute" cost? Does it just become a commodity? The big spenders want you to use it more and more, in more and more sophisticated ways. Tokens, tokens everywhere and not a brain to think! If you invest $1 trillion, you would like to see a return. A pretty good one. Especially as you are not sure how long the chips will last and how quickly you will have to upgrade. Then there is the question of open-source Chinese AI models, which are vastly cheaper and sometimes free. Will the Chinese do to the tech models what they have done to German car makers? Going the way of the Dodo! Does anyone know the cost of a "compute token" in a year? What about five years? As they say, investing in resource stocks is risky because you don't know what iron ore prices will be in five years. Yet they are still investing $1 trillion a year! Is this another period when the markets have lost their minds? Irrational exuberance. Vale Greenspan. He called it. |

|

Funds operated by this manager: |

7 Jul 2026 - 4 ASX stocks we like despite the macro uncertainty

3 Jul 2026 - Hedge Clippings | 03 July 2026

|

|

|

|

Hedge Clippings | 03 July 2026

Let's look at the RBA Minutes first: The RBA's minutes from its 15-16 June meeting, released this week, confirmed the board held at 4.35% but kept the door open to further tightening, citing "excess demand and widespread inflationary pressures". Persistently weak productivity was flagged as a standing concern; unit labour costs remain above their inflation-targeting-period average despite wages growth in line with expectations, since output per hour isn't keeping pace. The board also linked flat equity prices partly to limited local AI-boom participation. CBA, ANZ and NAB all read the tone as hawkish but were split on the implications: CBA sees a hold through 2026, but with upside risk; ANZ is flagging an August rise if Q2 CPI surprises on the high side; and NAB reads it as confirmation the cash rate has peaked. Which one is on the money will depend on the June CPI due on 29th July, and PPI due 2 days later. But with the RBA not due to meet until 10-11 August, two weeks before the July CPI due on August 26th, there's going to be some crystal ball gazing around the board table. Complicating things will be the slide in the oil price thanks to the US-Iran de-escalation (assuming it holds), but offset by the reintroduction of the other half of the fuel excise levy, and lingering supply-side inflation still filtering through the system. Back to the ASX FY25-26 Close While the Australian equity market as a whole was lacklustre at best, particularly when judged against the S&P500 or Dow Jones, there was an extreme divergence between the sectors and companies that drove average returns, and those that dragged them down. A 48% materials rally carrying an entire index to a mid-single-digit total return (inclusive of dividends) says as much about concentration risk as it does about the benefit of diversification. Strip out rare earths and iron ore, and FY25-26 looks considerably flatter, and argues loudest for active management and offshore diversification vs. passive index investing. Source: IG Australia, ASX 200 FY close report The ASX 200 closed the financial year up 6.3% including dividends. Materials led at +48.2% on a rare earths and lithium re-rating, but even within the sector there were standouts: Mineral Resources (+186.9%), Lynas Rare Earths (+115.2%), Iluka Resources (+93.1%), plus Rio Tinto (+63.0%) and BHP (+62.4%) all leading the charge. While accepting averages can be misleading, stock selection, manager and fund selection, are vital to beating the index. While individual stock prices are known, fund performance for June 2026 is still pending. However in the 12 months to the end of May, just over 50% of equity funds on AFM's database outperformed the ASX200. Choice of the right sector, and fund, or funds, is obviously key. The top 10 over the past 12 months to May have returned between 75% and 126%, a list not unsurprisingly dominated by Resource Strategies such as Terra Capital, Argonaut and Paragon. By comparison, investing in a passive ASX200 Index strategy would force the investor to accept the good, the bad, and everything in between for a return of just under 7%. Finally, US Non-Farm Payrolls June's US jobs report delivered the softest headline in four months: payrolls up just 57,000 versus 115,000 expected, with April and May revised down a combined 74,000. Leisure and hospitality shed 61,000 roles on weak seasonal hiring. Notably, the month Goldman Sachs had modelled a 40,000 World Cup hiring boost that didn't materialise. Unemployment fell to a 12-month low of 4.2%, driven by a 720,000 plunge in the labour force rather than stronger hiring, pulling participation to 61.5%, its lowest since March 2021. Fed Chair Warsh's 17 June comment that labour data was "moving in a good direction" now reads as cover for an extended hold, with June CPI (14 July) the next catalyst. A falling unemployment rate built on a shrinking labour force is a weaker signal than the headline suggests. It buys Warsh time but doesn't resolve the tension between inflation and a cooling jobs market, worth watching alongside the RBA's own next move. Donald will want to focus on the US birthday celebrations this weekend, rather than the job numbers. News | Insights 10k Words | Equitable Investors Netflix: Navigating deals, AI and growth | Magellan Investment Partners May 2026 Performance News Bennelong Emerging Companies Fund |

|

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday |

3 Jul 2026 - The underappreciated strength of European banks

|

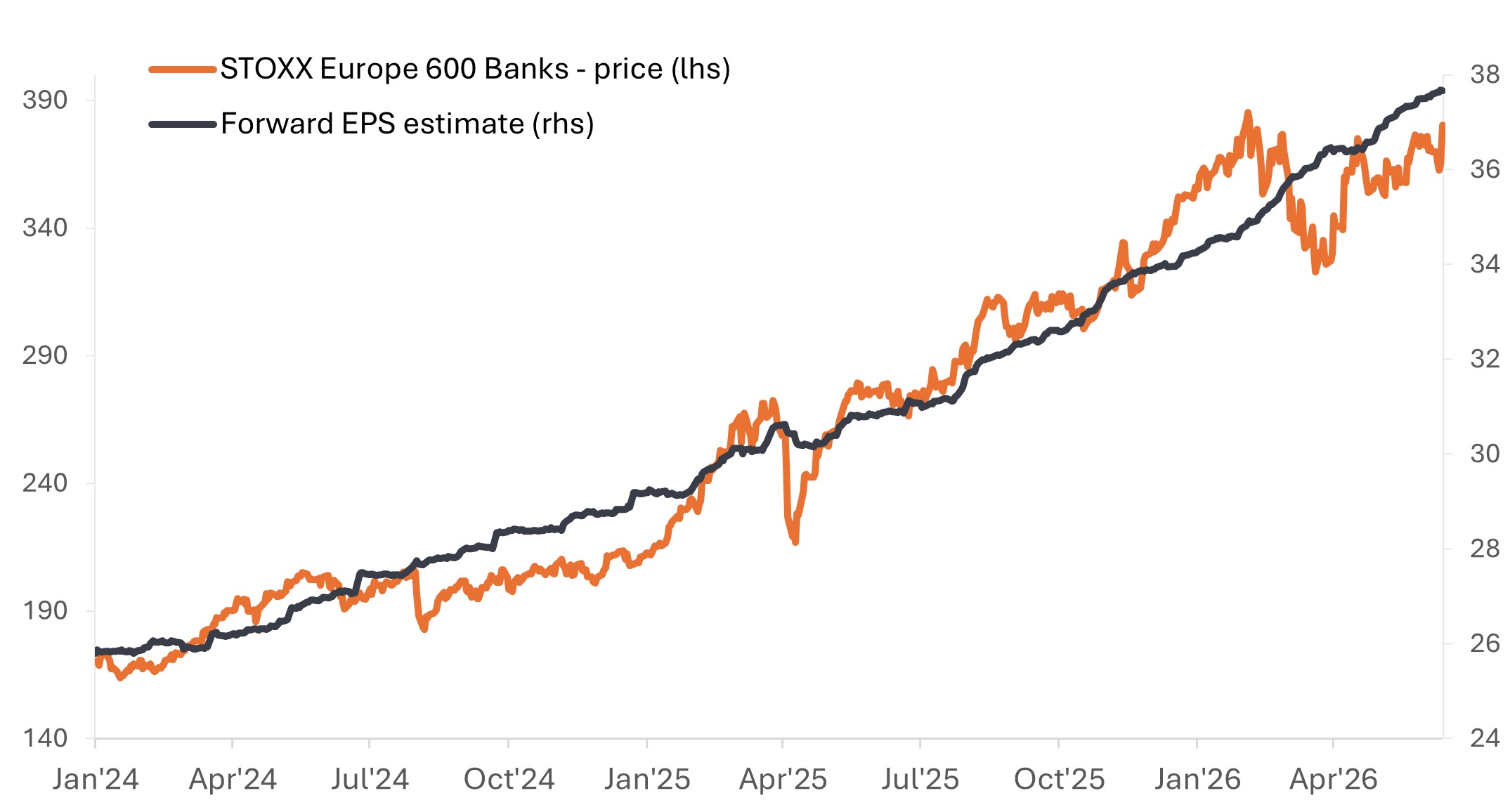

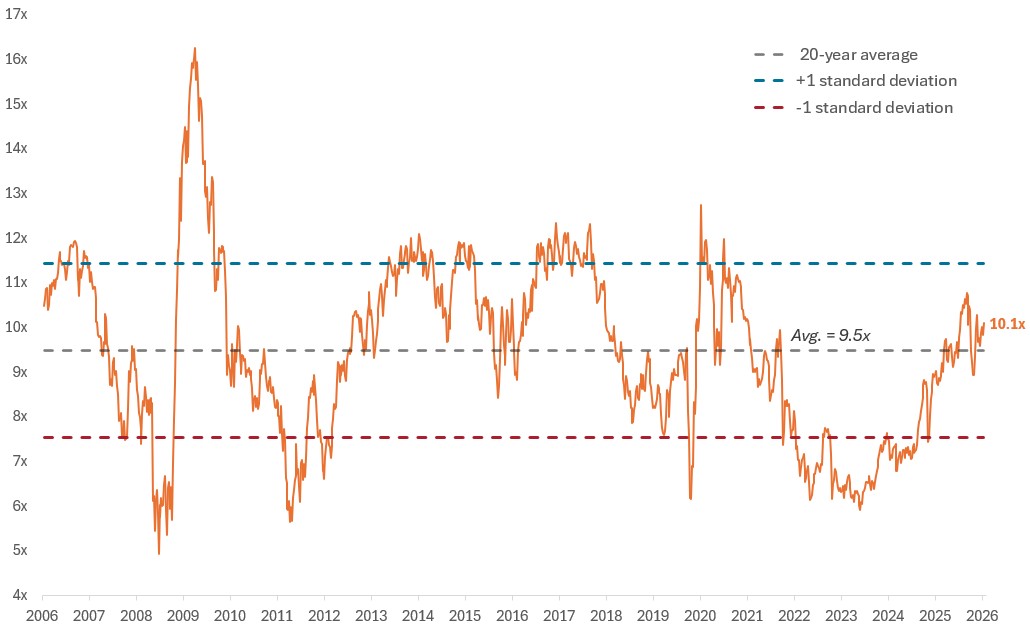

The underappreciated strength of European banks Janus Henderson Investors June 2026 (7-minute read) After more than a decade contending with the aftereffects of the Global Financial Crisis (GFC), European bank stocks have reemerged as one of the notable bright spots across the region's equity markets in recent years. In 2024 and 2025, the STOXX® Europe 600 Banks Index returned an impressive 35% and 77%, respectively, outperforming the broader STOXX® Europe 600 Index by more than 105 percentage points over that span.1 Importantly, this followed a long stretch of relative underperformance as tougher banking regulations and ultra-low interest rates weighed on profitability and loan growth. But while a low starting point and recognition of deeply depressed valuations - and subsequent multiple expansion - may explain some of the rally, improved fundamentals have been an underappreciated aspect of the story, in our view. Indeed, the rally over the last two years has been underpinned by earnings growth, as shown in the chart below. And while the Iran conflict injected a fresh dose of macro-driven volatility, valuations across the sector remain modest, and we believe the case for further rerating is firmly intact. Exhibit 1: Strong 2024 and 2025 performance driven by significant upward earnings revisions and multiple expansion

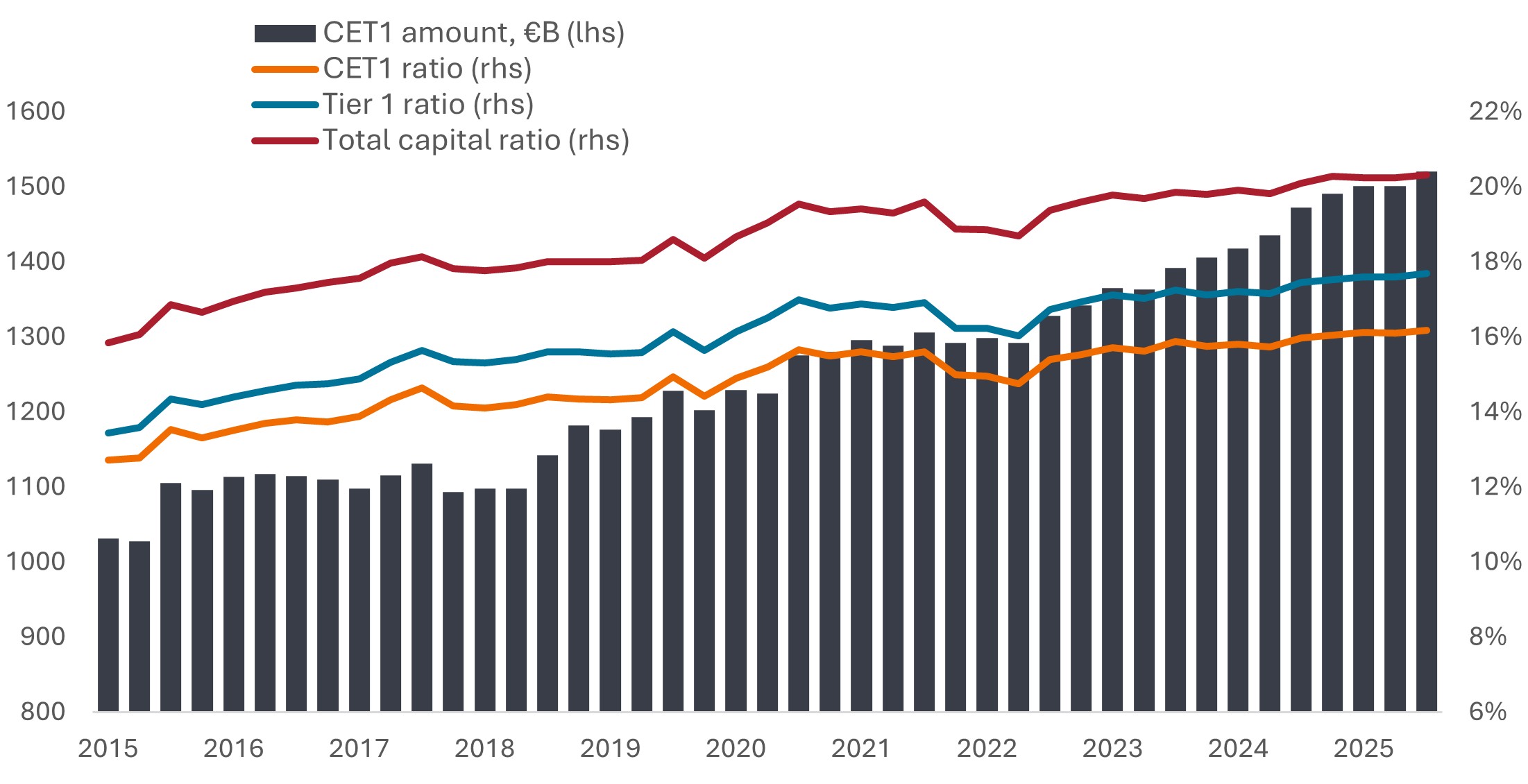

Source: Bloomberg, data from 1 January 2024 to 12 June 2026. Past performance does not predict future results. Emerging from a 15-year post-GFC deleveraging cycle In Europe, banks have spent more than a decade improving the size and quality of their capital reserves, as evidenced by a steady rise in Common Equity Tier 1 (CET1) levels and capital ratios (Exhibit 2). While this has supported banks' ability to weather exogenous shocks, it has also constrained lending, resulting in a period of muted - and at times, negative - loan growth. This, in turn, weighed on economic growth across the region, as banks provide the majority of financing to the corporate sector. More recently, there has been growing debate about whether the pendulum may have swung too far toward over-regulation. To date, progress toward deregulation has been limited, but discussions are underway around proposals to free up capital, support lending, and improve the competitiveness of European banks. Exhibit 2: European banks have built materially stronger capital positions

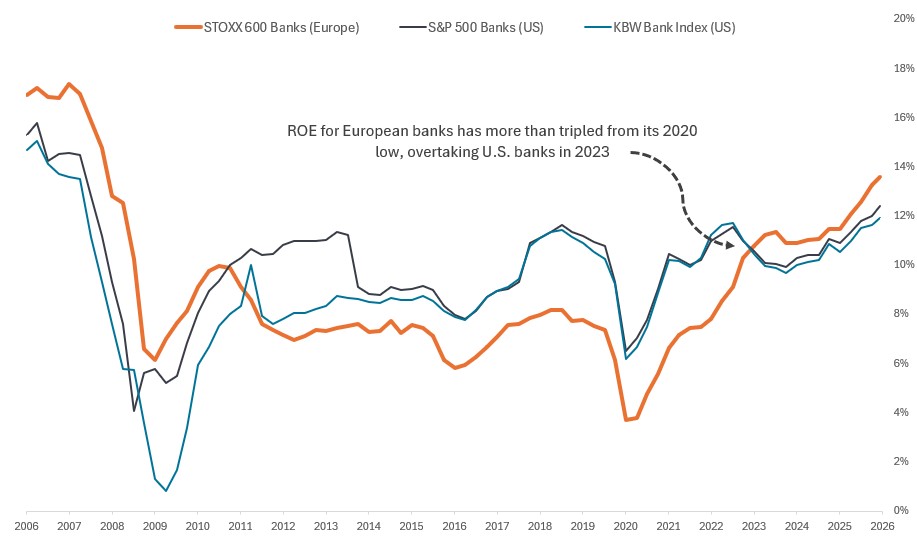

Source: ECB, "Supervisory Banking Statistics for significant institutions, fourth quarter 2025", 18 March 2026. At the same time, risk controls and cost-cutting measures honed during the days of negative rates have vastly improved many firms' operating efficiency. Loan books have also been significantly de-risked, with the non-performing loans ratio for significant institutions falling to roughly 2% in recent European Central Bank (ECB) data, down from more than 7% a decade ago.2 The upshot is that European banks have emerged from the prolonged deleveraging cycle as a healthier, more profitable sector, with higher interest rates providing an additional tailwind to earnings. A more constructive operating environment Consequently, the region's banks have been achieving their highest profitability of the post-GFC era, as measured by return-on-equity (ROE) levels. After bottoming in the mid-single-digits range in the aftermath of the pandemic, European banks have closed the gap with their U.S. peers and, in some cases, moved ahead for the first time in years. Exhibit 3: European banks have closed the profitability gap with U.S. peers

Source: Bloomberg, data as of 12 June 2006 to 12 June 2026. Past performance does not predict future results. Valuations suggest room for further rerating Despite this improved fundamental picture, European bank stocks continue to trade at a meaningful discount to U.S. banks and the broader European equity market. Although valuations have risen from deeply depressed levels, they have only recently returned to their long-term average.

Exhibit 4: European bank valuations are yet to fully reflect improved fundamentals

Source: Bloomberg, data as of 12 June 2006 to 12 June 2026. Past performance does not predict future results. Meanwhile, European banks have been returning capital to shareholders at a healthy clip in the form of dividends and share buybacks, with the dividend yield on the STOXX Europe 600 Banks Index north of 5%, more than double that of comparable U.S. benchmarks.4 All of this would argue in favor of room for further multiple expansion, in our view. While some discounting to U.S. peers may be warranted, we believe the persistently wide valuation gap also reflects anchoring bias - a tendency among investors to reference past underperformance when making investment decisions. Longer-term structural shifts and potential implications Beyond the improved earnings trajectory and still-attractive valuations, a combination of structural shifts and secular drivers is reshaping the investment landscape for European banks and could further support the case for additional upside.

While recent geopolitical turmoil has strengthened the case for European nations to boost defense spending - a potential tailwind that could support lending growth - the Iran conflict and resultant energy shock have cast a pall over the economic outlook for the region. The dual threat of higher inflation and potential demand destruction poses a risk for net energy-importing countries and bears close monitoring. The ECB responded on June 11 with its first rate increase since 2023, and markets are pricing in expectations for at least one additional rate hike this year, as of this writing. For now, the combination of modestly higher rates and still-resilient, albeit less-robust, economic growth aligns with the sort of environment in which banks typically thrive. That said, even with the recent Iran ceasefire extension, questions remain about how fully the Strait of Hormuz will reopen and the extent to which any lingering supply disruption could weigh on Europe and the broader global economy. This uncertain backdrop makes selectivity all the more critical. While we believe the case for further valuation rerating remains compelling, it is unlikely to be uniform across the European banking sector. In our view, deep fundamental research and bottom-up stock selection are essential to identifying institutions with strong capital positions, diversified earnings streams, and exposure to attractive markets supported by longer-term secular tailwinds. IMPORTANT INFORMATION Actively managed investment portfolios are subject to the risk that the investment strategies and research process employed may fail to produce the intended results. Accordingly, a portfolio may underperform its benchmark index or other investment products with similar investment objectives. Diversification neither assures a profit nor eliminates the risk of experiencing investment losses. Equity securities are subject to risks including market risk. Returns will fluctuate in response to issuer, political and economic developments. Financials industries can be significantly affected by extensive government regulation, subject to relatively rapid change due to increasingly blurred distinctions between service segments, and significantly affected by availability and cost of capital funds, changes in interest rates, the rate of corporate and consumer debt defaults, and price competition. Foreign securities are subject to additional risks including currency fluctuations, political and economic uncertainty, increased volatility, lower liquidity and differing financial and information reporting standards, all of which are magnified in emerging markets. |

|

Funds operated by this manager: Janus Henderson Australian Fixed Interest Fund , Janus Henderson Conservative Fixed Interest Fund , Janus Henderson Diversified Credit Fund , Janus Henderson Global Natural Resources Fund , Janus Henderson Tactical Income Fund , Janus Henderson Australian Fixed Interest Fund - Institutional , Janus Henderson Conservative Fixed Interest Fund - Institutional , Janus Henderson Cash Fund - Institutional , Janus Henderson Global Multi-Strategy Fund , Janus Henderson Global Sustainable Equity Fund , Janus Henderson Sustainable Credit Fund All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect. The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested. Whilst Janus Henderson believe that the information is correct at the date of publication, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson to any end users for any action taken on the basis of this information. |

2 Jul 2026 - Performance Report: Equitable Investors Dragonfly Fund

[Current Manager Report if available]

2 Jul 2026 - Global infrastructure: Why a selective approach matters

|

Global infrastructure: Why a selective approach matters abrdn June 2026 (Reading time: 5 Mins) What if the biggest risk in infrastructure investing today is treating it as a single asset class? Historically, global infrastructure has been perceived as an asset class offering relatively stable and predictable returns which may vary depending on market conditions. Yet, as the asset class evolves in response to structural shifts such as decarbonisation, digitalisation, and changing supply chains, broad categorisations are becoming less useful. The infrastructure label alone no longer tells investors enough about revenue quality, risk transfer, policy exposure or long-term resilience. The key question is not simply whether an asset sits within an infrastructure sector, but whether it has the economic characteristics investors expect from infrastructure in the first place. A more nuanced investment universeInfrastructure today is not a monolith. It spans a diverse range of subsectors, each with distinct drivers, regulatory frameworks, and risk-return profiles. Traditional assets such as utilities and transport continue to play a core role, but they are increasingly complemented by newer areas like digital networks, district heat, equipment leasing and other energy transition solutions. Investors need to distinguish between assets with genuinely defensive infrastructure characteristics and those that may simply be exposed to attractive themes. In this context, we believe a selective approach is becoming essential. Investors need to distinguish between assets with genuinely defensive infrastructure characteristics and those that may simply be exposed to attractive themes. This enables a clearer understanding of where risks lie - and where opportunities may be underappreciated. DecarbonisationOpportunity with complexityOne of the most powerful forces reshaping infrastructure is the global energy transition. Governments and corporates are accelerating efforts to decarbonise, driving significant capital investment into renewables, grid modernisation, energy efficiency and the wider infrastructure needed to make lower-carbon systems reliable and affordable. A selective perspective helps investors distinguish between different risk profiles, allowing for more targeted allocation. However, this opportunity set is far from uniform. In our view, the dispersion in renewable returns is being underestimated depending on geography, regulatory support, and technological maturity. Some assets benefit from long-term contracted revenues, while others are more exposed to merchant pricing, grid constraints and policy evolution. A selective perspective helps investors distinguish between these different risk profiles, allowing for more targeted allocation. It also helps avoid the assumption that every asset associated with the transition automatically offers infrastructure-like downside protection. Digital infrastructure comes of ageAt the same time, the digital economy is transforming what constitutes infrastructure. The rapid growth in data consumption has fuelled demand for fibre networks, towers, and data centres. Some of these assets exhibit infrastructure-like characteristics, including high barriers to entry, essential demand and long-term contracts. For investors, the distinction between durable digital infrastructure and technology-led growth exposure is increasingly important. Yet these assets are not without their own complexities. Technological change, evolving customer requirements, and competitive dynamics can all influence long-term value. Understanding these factors at a detailed level is critical to identifying assets that combine structural growth with durable cash flows. Rethinking transport and logisticsTransport infrastructure, long a cornerstone of the asset class, is also evolving. While passenger volumes have recovered unevenly in the wake of the pandemic, longer-term trends such as remote working and decarbonisation are reshaping demand patterns. Meanwhile, freight and logistics infrastructure has gained prominence, supporting changing supply chains and demand for more resilient networks. Here again, selectivity matters. Assets supported by contracted, availability-based or take-or-pay revenues can have a very different risk profile from those exposed mainly to volumes or discretionary demand. Regulation and inflationDetail mattersRegulation remains a defining feature of infrastructure investing, but its influence is becoming more complex. Policymakers must balance attracting private capital with achieving social and environmental objectives, creating both opportunities and risks. A detailed, bottom-up approach is essential to assess (revenue linkage, contract structures, and regulatory mechanisms) accurately. Inflation adds another layer of nuance. While infrastructure is often viewed as a potential hedge against rising prices, the degree of protection varies. Some assets benefit from explicit indexation, while others rely on pricing power, regulatory resets or contract renegotiation. Revenue linkage, contract structures, cost pass-through and regulatory mechanisms all play a role in determining how effectively inflation protection works in practice. A detailed, bottom-up approach is essential to assess these dynamics accurately. The case for active, selective investingIn an increasingly diverse and complex asset class, active management is gaining importance. Broad or passive approaches may overlook the dispersion of returns across subsectors and geographies. By contrast, a selective strategy grounded in detailed analysis can better identify mispriced opportunities, anticipate regulatory shifts, and allocate capital to areas with the strongest long-term fundamentals. For us, this means focusing on assets where essential-service demand, defensible revenues and active ownership can combine to create value, rather than relying on thematic growth alone. This also enhances diversification, ensuring that portfolios are constructed from assets with genuinely complementary characteristics, rather than simply broad exposure. Final thoughtsThe case for global infrastructure remains compelling, underpinned by a significant investment gap across energy, digital connectivity, and urban development. However, capturing these opportunities requires a more sophisticated approach than broad asset-class exposure can provide. As the market evolves, success will depend on moving beyond high-level classifications and focusing on the assets that genuinely combine essentiality, resilience and growth, embracing a more selective perspective. For investors, this shift is not only about managing risk. It is about accessing the best of what infrastructure can offer in a rapidly changing world. |

|

Funds operated by this manager: abrdn Sustainable Asian Opportunities Fund , abrdn Emerging Markets Equity Fund , abrdn Sustainable International Equities Fund , abrdn Global Corporate Bond Fund (Class A) |

1 Jul 2026 - Monthly Market Commentary

|

Monthly Market Commentary Arculus Funds Management June 2026 (3-minute read) Monetary Policy & Rates The RBA held the cash rate steady this month following three consecutive 25bp increases to open the year, a unanimous decision that Governor Bullock paired with an acknowledgement the economy still carries "a bit of excess demand." We read the pause as genuine, not the end of the cycle. Our central case is that the Bank remains on hold through the second half of the year before delivering a further 25bp increase in the December quarter - a move we expect to be driven by cost-push inflation crystallising even as the broader economy looks lacklustre. Underlying inflation is building beneath a softer headline The case for a final hike is building beneath a softening headline. May headline inflation fell to 4.0% YoY, but almost entirely on a 12% fall in fuel and a 6.9% drop in travel prices; the trimmed mean rose to 3.6% YoY, the high of its series. The persistence sits in roughly a third of the basket and is supply- and cost-side in character: new dwelling construction is running at 5.6% YoY - its fastest since mid-2023 and adding some 42bps to headline inflation on its own - while rents are reaccelerating toward 4% and market services inflation remains broad-based. Critically, this is all evident before the Fair Work Commission's 4.75% award wage increase - which lifts pay for around a fifth of the workforce - takes effect on 1 July (the concurrent ~6% rise in the National Minimum Wage reaches under 1% of employees and is macroeconomically immaterial). We expect that award step-up to feed market services through the second half, with the late-October Q3 CPI the most likely trigger for the Bank to move. A hike into a cooling economy That this tightening would land into a cooling economy is, in our view, the defining feature of the outlook rather than a contradiction of it. The housing downturn has begun, hours worked softened in the month, and household spending is growing at its slowest pace in a year. Yet the labour market remains genuinely tight: unemployment fell back to 4.4% as April's spike reversed, employment rebounded 40k, and broader spare-capacity measures - underutilisation at 10.2%, underemployment near its cycle low - sit at generational tights. A central bank facing sticky, cost-driven inflation against a still-tight labour market has limited room to look through it, weak demand notwithstanding. The 2027 risk: a wage-price spiral Beyond the December move, we see a credible path to a second 25bp increase during 2027, though we treat it as conditional and sequenced. The first condition is that money supply growth remains strong, sustaining the monetary impulse behind demand; only if that holds does the second condition - a broadening in wages growth - become the mechanism that converts cost-push pressure into a self-reinforcing wage-price dynamic. Absent strong money supply growth, we would not expect wages alone to force the Bank's hand. We flag this as a risk case rather than our base but note it runs directly counter to prevailing assumptions of an easing cycle from late 2027. On our trajectory the next move is up, then held, and the eventual cut sits materially later than consensus. Positioning With the market pricing only around 8bps of tightening over the next twelve months, we regard the front end as under-pricing both the December hike and the medium-term risk profile. This is a higher-for-longer environment, and we continue to favour carry and income over duration, with elevated BBSW reflecting a rate path that has further to climb before it turns. Funds operated by this manager: |