NEWS

Performance Report: 4D Global Infrastructure Fund (Unhedged)

The 4D Global Infrastructure Fund (Unhedged) rose by +14.83% over the past 12 months. American Electric Power was the top contributor and Brazilian rail operator Rumo the largest detractor, with 4D maintaining a positive view on listed...

Read more...

Performance Report: Skerryvore Global Emerging Markets All-Cap Equity Fund

The Skerryvore Global Emerging Markets All-Cap Equity Fund has returned +4.92% per annum since inception in August 2021. In July, top contributors included Mega Lifesciences, Taiwan Semiconductor, and Hindustan Unilever, while Raia...

Read more...

Expert Analysis of the RBA's August 12 Rate Decision

Chris Gosselin, CEO of FundMonitors.com, speaks with Nicholas Chaplin, Director and Portfolio Manager at Seed Funds Management and Renny Ellis, Director & Head of Portfolio Management at Arculus Funds Management.

Read more...

Sustainable equities outlook: AI's transformative role in an evolving global...

Portfolio Manager Hamish Chamberlayne explores how, in a world marked by geopolitical upheaval, artificial intelligence (AI) is transforming traditional economic forces, presenting both opportunities and challenges.

Read more...

Performance Report: Bennelong Emerging Companies Fund

The Bennelong Emerging Companies Fund rose by +4.23% in July, outperforming the ASX 200 Total Return benchmark by +1.87%. Since inception in November 2017, the fund has returned +20.47% per annum, an outperformance of +11.18% relative to...

Read more...

Performance Report: Airlie Australian Share Fund

The Airlie Australian Share Fund rose by +2.70% in July, outperforming the ASX 200 Total Return benchmark by +0.33%. Since inception in June 2018, the fund has returned +10.50% per annum, an outperformance of +1.09% relative to the...

Read more...

Performance Report: Seed Funds Management Hybrid Income Fund

The Seed Funds Management Hybrid Income Fund rose by +1.19% in July, outperforming the Solactive Australian Hybrid Securities (Net) benchmark by +0.55%. Since inception in October 2015, the fund has returned +6.41% per annum, an...

Read more...

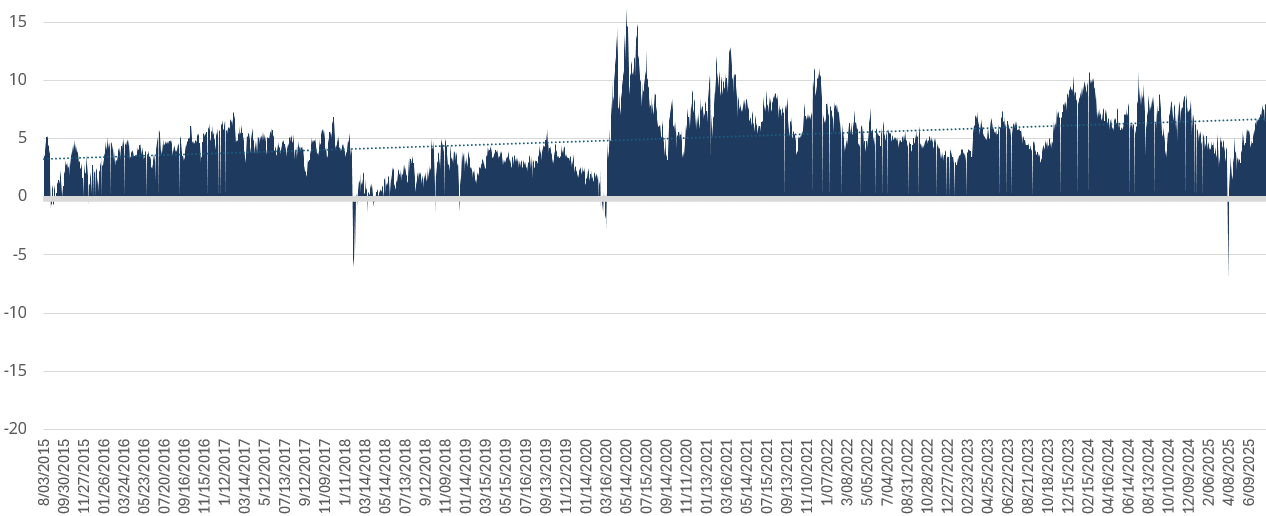

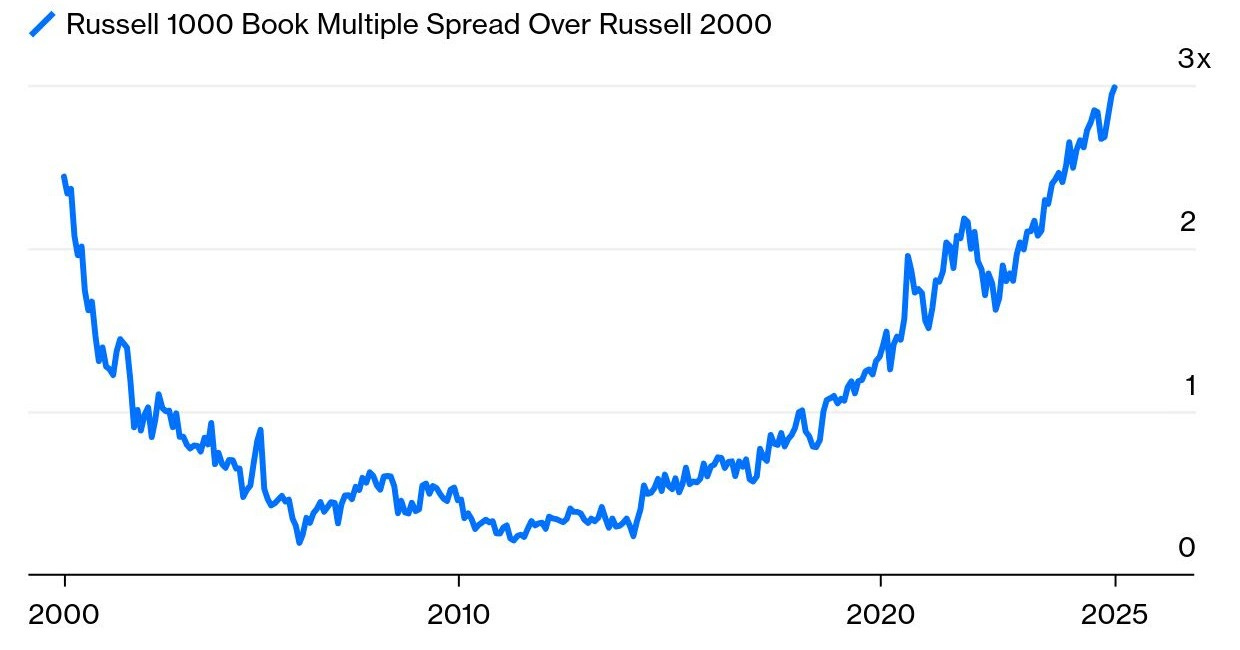

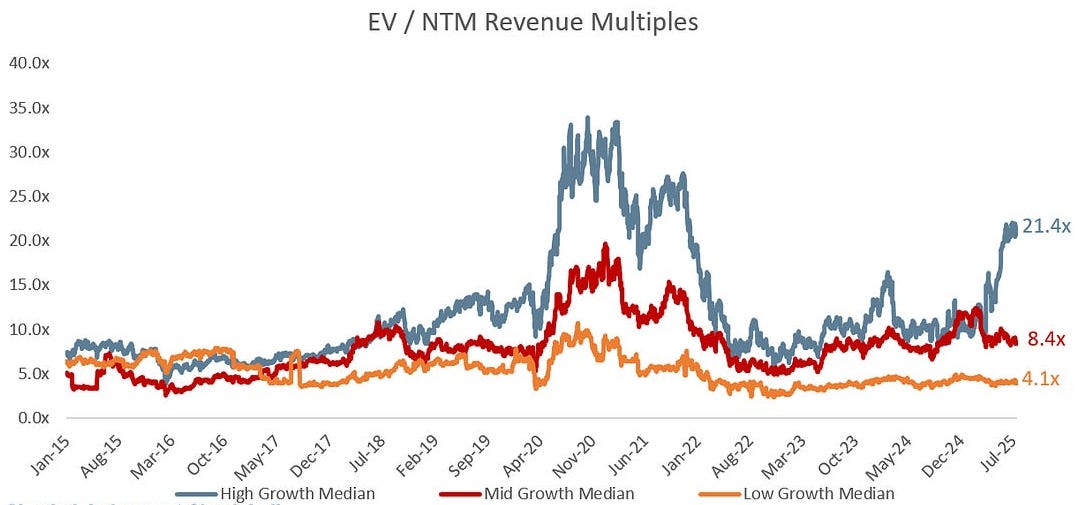

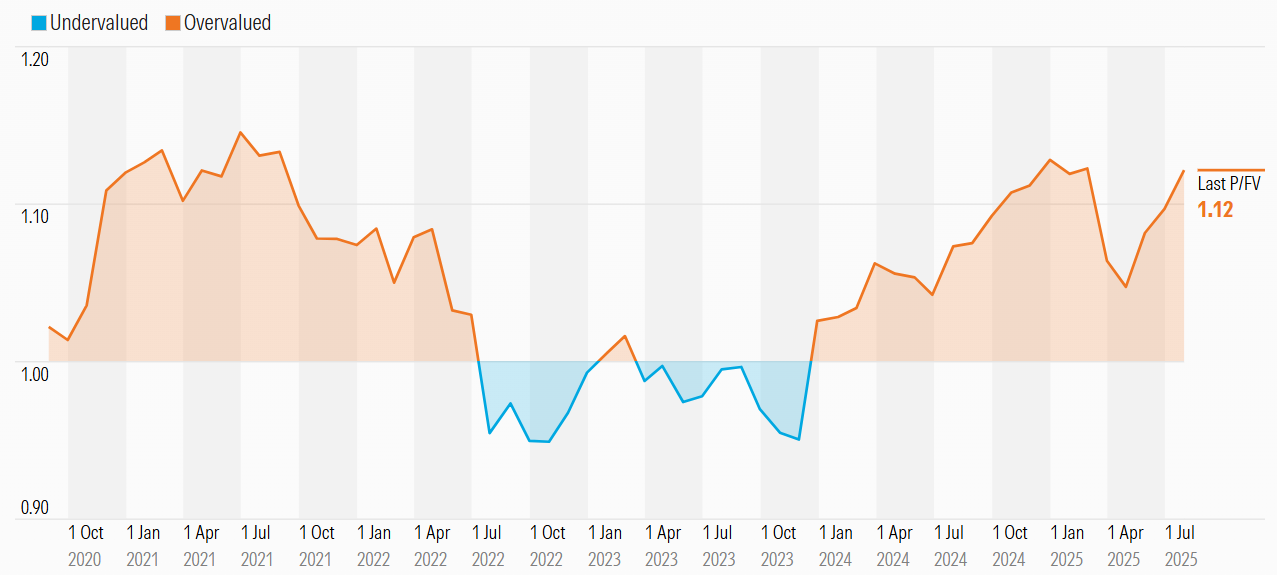

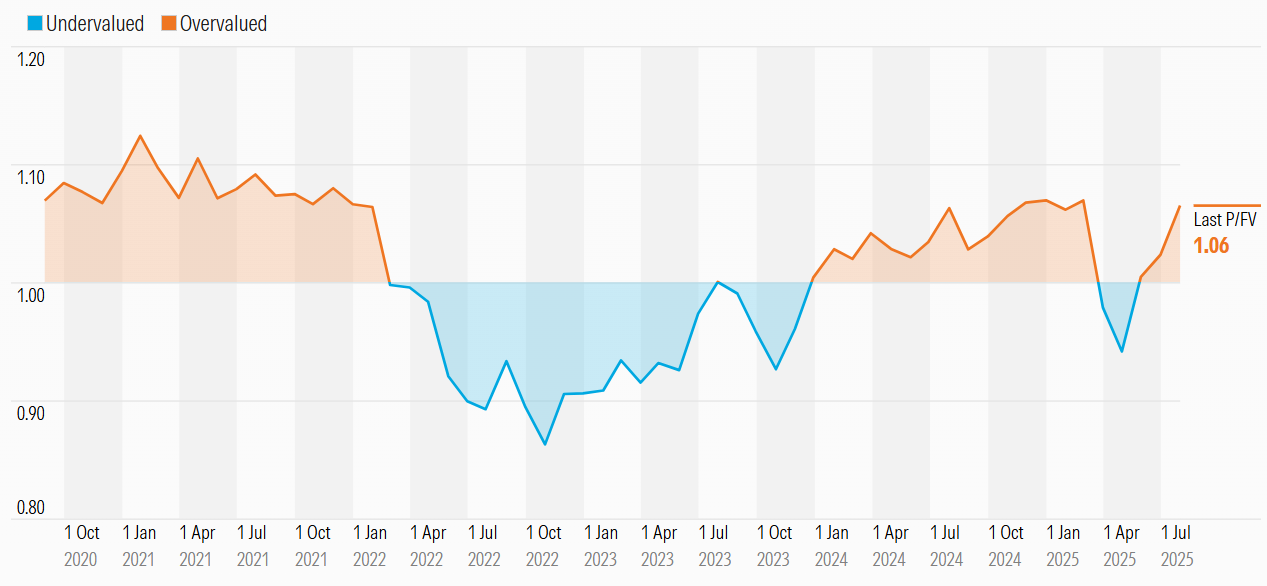

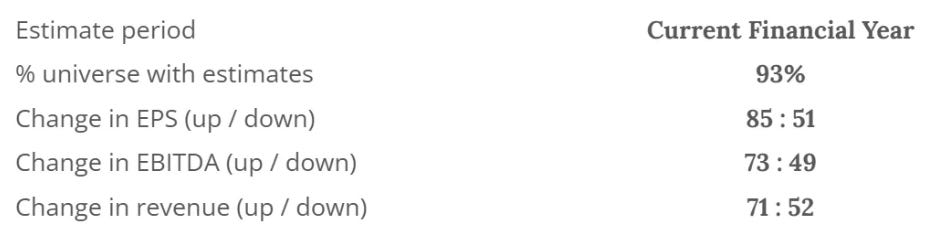

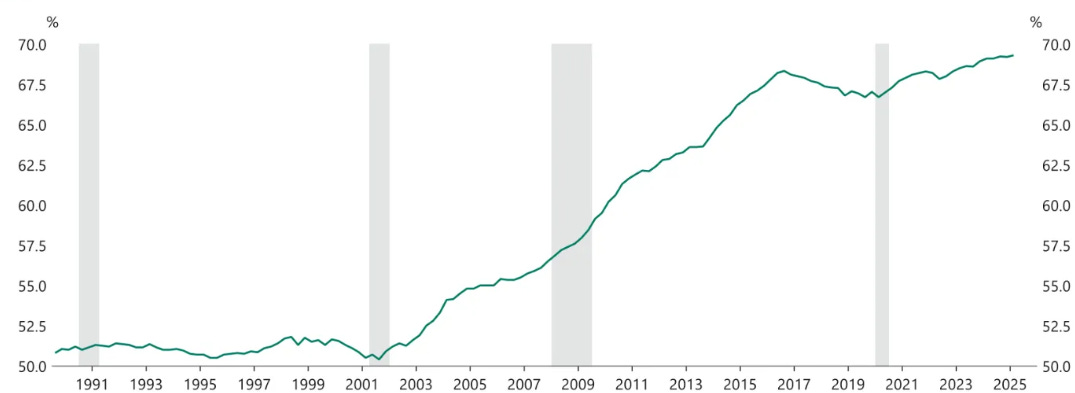

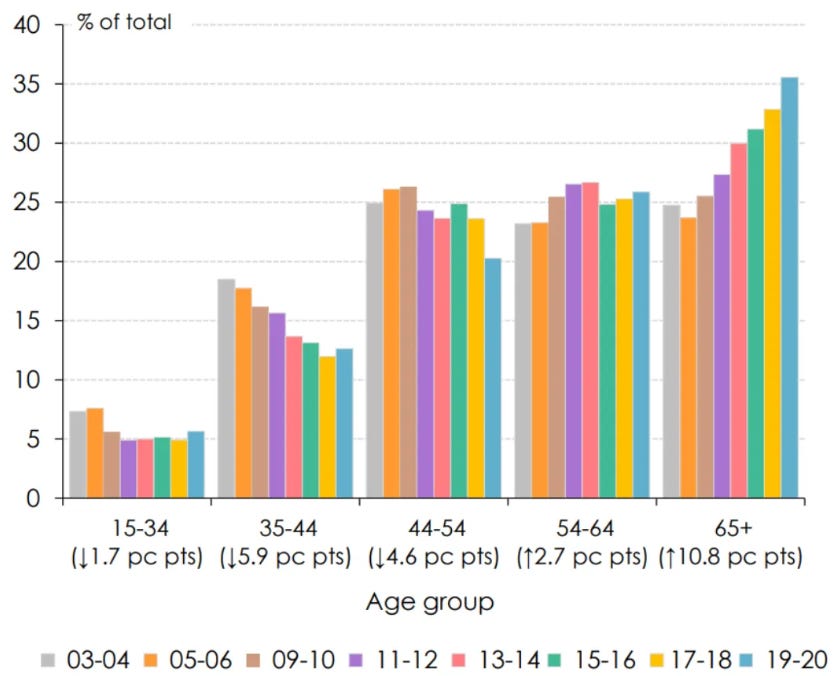

10k Words |August 2025

There's a healthy spread between the volatility investors are pricing in for small caps relative to large caps but high yield ("junk") spreads are near historical lows.

Read more...

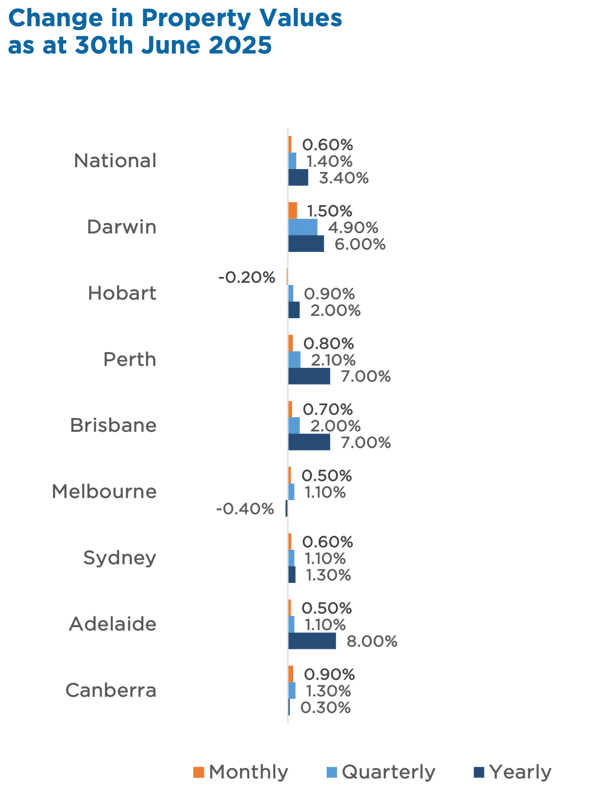

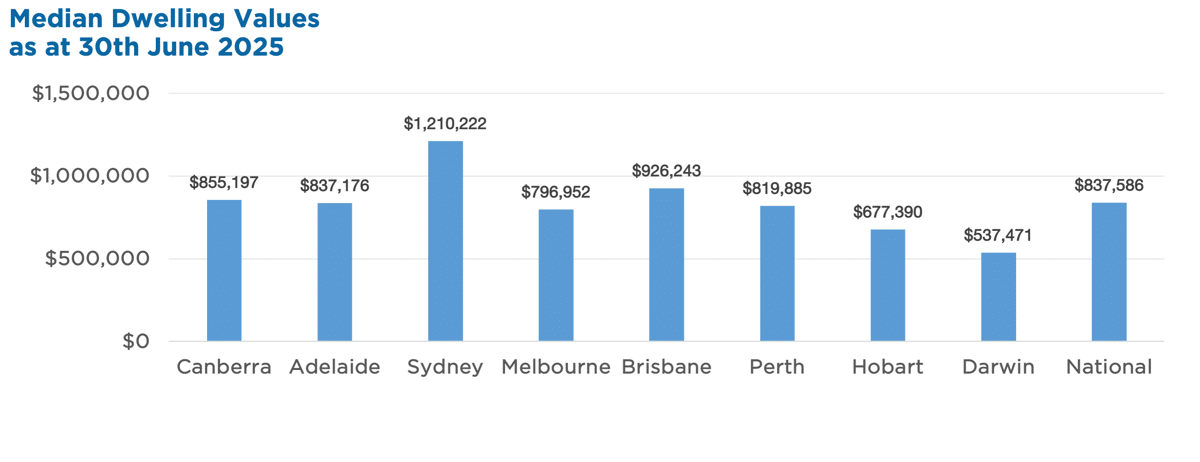

Australian Secure Capital Fund - Market Update

Australian housing values rose 0.6% in June, marking five straight months of growth. The June quarter saw a 1.4% national increase, with gains across most capital cities - driven by falling interest rates and low advertised stock.

Read more...

Performance Report: Bennelong Twenty20 Australian Equities Fund

The Bennelong Twenty20 Australian Equities Fund rose by +3.93% in July, outperforming the ASX 200 Total Return benchmark by +1.57%. Since inception in November 2009, the fund has returned +9.81% per annum, an outperformance of +1.32%...

Read more...