NEWS

Performance Report: Quay Global Real Estate Fund (Unhedged)

The Quay Global Real Estate Fund (Unhedged) rose by +1.36% over the past 12 months. In July, Goodman Group in Australia was a key contributor, while holdings in the UK and Europe detracted, and Quay remains positive on the sector,...

Read more...

Performance Report: Glenmore Australian Equities Fund

The Glenmore Australian Equities Fund rose by +5.40% in July, outperforming the ASX 200 Total Return benchmark by +3.04%. Since inception in June 2017, the fund has returned +18.91% per annum, an outperformance of +9.47% relative to the...

Read more...

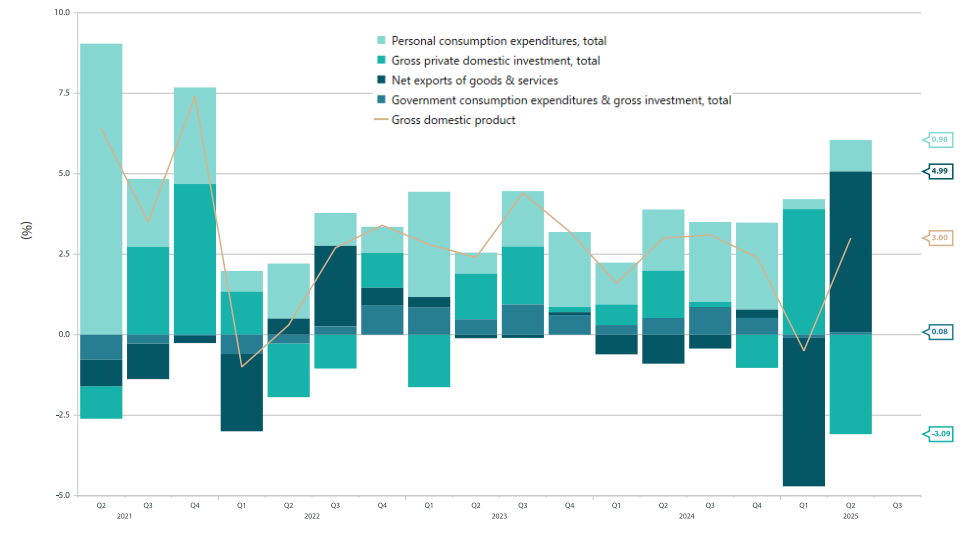

Investment Perspectives: 10 charts shaping our thinking

Deep-dive company research is central to Quay's investment process. This month we unpack six key themes - both emerging and ongoing - that stood out from over 30 in-person meetings with prospective and existing investees across Europe, the...

Read more...

Performance Report: Canopy Global Small & Mid Cap Fund

The Canopy Global Small & Mid Cap Fund rose by +1.90% in July, driven by strong gains from Medpace, PTC and Trex, while Brown & Brown, Gartner and Tradeweb detracted from returns. Canopy remains constructive on the market, noting easing...

Read more...

Performance Report: Altor AltFi Income Fund

The Altor AltFi Income Fund rose by +0.81% in July, outperforming the RBA Cash Rate + 5% benchmark by +0.10%. Since inception in April 2018, the fund has returned +11.43% per annum, an outperformance of +4.45% relative to the benchmark...

Read more...

Manager Insights | Digital Asset Funds Management

Chris Gosselin, CEO of FundMonitors.com, speaks with Clint Maddock, Director and Co-Founder at Digital Asset Funds Management, about the firm's Digital Income Fund and its market-neutral arbitrage strategy in the cryptocurrency space.

Read more...

Hedge Clippings |15 August 2025

This week, the Reserve Bank of Australia made headlines with a 25 basis point rate cut, bringing the cash rate down to 3.60% -- the third move in the current easing cycle.

Read more...

Performance Report: DS Capital Growth Fund

The DS Capital Growth Fund rose by +2.21% in July. Since inception in January 2013, the fund has returned +13.09% per annum, an outperformance of +3.60% relative to the ASX 200 Total Return benchmark which has returned +9.49% on an...

Read more...

Performance Report: Cyan C3G Fund

The Cyan C3G Fund rose by +18.51% over the past 12 months, outperforming the ASX Small Ordinaries Total Return benchmark by +6.97%. In July, strong performances from Beforepay, Bioxyne and Alcidion were offset by a sharp pullback in Locate...

Read more...

Fed, BOJ and China navigate uncertain growth and inflation paths

The Federal Reserve (Fed) kept rates on hold on 30 July, maintaining the policy rate in a range between 4.25% and 4.5%, following stronger-than-expected US Q2 GDP data.

Read more...