NEWS

Cyan Investment Management | Market Perspective & Fund Overview

In this video Dean Fergie (Founding Director and Portfolio Manager) gives Cyan's perspective on the market's activity towards the end of 2018 and the rebound seen in the first quarter of 2019. He then discusses how the Cyan C3G...

Read more...

Performance Report: Bennelong Emerging Companies Fund

The Bennelong Emerging Companies Fund rose +14.03% in April, outperforming the ASX200 Accumulation Index by +11.66% and taking 12-month performance to +22.21% versus the Index's +10.41%.

Read more...

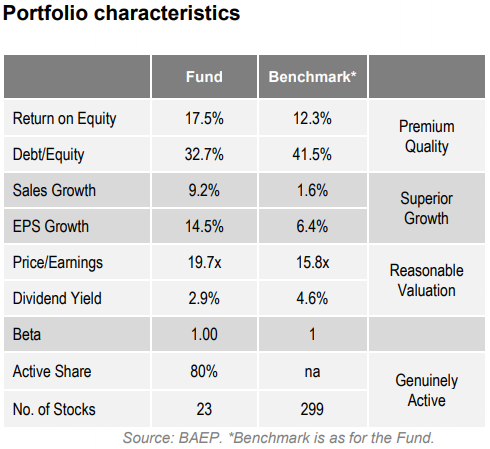

Performance Report: Touchstone Index Unaware Fund

The Touchstone Index Unaware Fund returned +3.57% in April, outperforming the ASX200 Accumulation Index by +1.2% and taking annualised performance since inception in April 2016 to +11.23%.

Read more...

Performance Report: KIS Asia Long Short Fund

The KIS Asia Long Short Fund returned -0.41% in April. Since inception in October 2009, the Fund has returned +11.76% p.a. with an annualised volatility of 5.16%.

Read more...

Performance Report: Bennelong Concentrated Australian Equities Fund

The Bennelong Concentrated Australian Equities Fund rose +3.40% in April, outperforming the ASX200 Accumulation Index by +1.03% and taking annualised performance since inception in February 2009 to +16.34% versus the Index's +10.65%.

Read more...

Performance Report: Insync Global Capital Aware Fund

The Insync Global Capital Aware Fund rose +7.24% after fees and protection in April, outperforming AFM's Global Equity Index by +3.15% and taking annualised performance since inception in October 2009 to +10.78%.

Read more...

Bipartisanship - an Albatross for Congress

As we watch the US and China heading enthusiastically into a full-scale trade war, it is worth taking a step back from President Trump's daily squabbles via the Twittersphere with the rest of Planet Earth, and focusing on the policy areas...

Read more...

Loftus Peak | Market Update (April 2019)

Alex Pollak (CIO & Founder) discusses Loftus Peak's performance and portfolio composition as at April 2019. Alex points out that the net debt to equity ratio of the companies in their portfolio as group is negative, meaning they don't have...

Read more...

Hedge Clippings | The excitement's over, now back to work!

After all the expectations and then, depending on one's political leanings, the excitement or disappointment of the final result, it's now back to normal. Or as near normal as life ever seems to be.

Read more...

Loftus Peak | Auto Industry Disruption

Alex Pollak, Loftus Peak's CIO & Founder, expects electric vehicles to cause significant disruption to the auto industry. In this video, Alex details Loftus Peak's views on the disruption being caused to the industry and how they're taking...

Read more...