NEWS

22 Jul 2019 - New Funds on Fundmonitors.com

|

New Funds on Fundmonitors.com |

|

|

||||

| Ellerston Australian Micro Cap Fund | ||||

|

||||

| View Profile |

|

||||

| Watermark Absolute Return Fund | ||||

|

||||

| View Profile |

|

||||

| The Navis Jockey Fund | ||||

|

||||

| View Profile |

|

||||

| Fairlight Global Small & Mid Cap (SMID) Fund | ||||

|

||||

| View Profile |

|

||||

| TAMIM Small Cap Income Fund | ||||

|

||||

| View Profile |

| Want to see more funds? |

|

Subscribe for full access to these funds and over 400 others |

22 Jul 2019 - Performance Report: Bennelong Australian Equities Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | The Bennelong Australian Equities Fund seeks quality investment opportunities which are under-appreciated and have the potential to deliver positive earnings. The investment process combines bottom-up fundamental analysis with proprietary investment tools that are used to build and maintain high quality portfolios that are risk aware. The investment team manages an extensive company/industry contact program which helps identify and verify various investment opportunities. The companies within the portfolio are primarily selected from, but not limited to, the S&P/ASX 300 Index. The Fund may invest in securities listed on other exchanges where such securities relate to the ASX-listed securities. The Fund typically holds between 25-60 stocks with a maximum net targeted position of an individual stock of 6%. |

| Manager Comments | Over the June quarter the Fund rose +5.83%. Key detractors included Reliance Worldwide, Corporate Travel Management, Costa Group and Treasury Wine Estates. The Fund's main positive contributor was Aristocrat Leisure after the company reported strong half year financial results in May, above the market's expectations. Bennelong's view is that the market is largely being driven by macro factors at present, however, their belief is that ultimately stock prices won't be able to ignore longer term fundamental drivers of valuations, earnings and growth. |

| More Information |

19 Jul 2019 - Hedge Clippings | 19 July 2019

|

||||

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday

|

19 Jul 2019 - Performance Report: Wheelhouse Global Equities Income Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | To pursue this objective, the Investment Manager is responsible for actively managing, monitoring and tailoring the integration of derivative contracts alongside the Morningstar Portfolio, while taking into account changing market and stock specific conditions. The Investment Manager is responsible for maximising the structural benefits of short option positions (lowered Volatility, improved capital preservation, higher income generation), whilst mitigating, minimising and monitoring the structural negatives (variable market exposure, option expiries, collateral management and asymmetric return profiles). In addition, long derivatives positions are also used to enhance the capital preservation characteristics of the Fund in more extreme market movements. As a consequence of the integration of Derivatives, returns of the strategy, intra-cycle, are expected to vary from the underlying Morningstar Portfolio due to these characteristics. For example in weak markets, or in extended sideways markets, the Fund is expected to outperform relative to the Morningstar Portfolio. Conversely in strong positive markets the Fund is expected to underperform. |

| Manager Comments | The Fund's 12-month returns showcase the objectives of Wheelhouse's approach, which is to deliver a consistent high yield, plus protect and grow the capital base. Wheelhouse believe over time this will lead to equity rates of return delivered mostly in yield rather than capital appreciation. Wheelhouse observe that global share markets are setting record highs against a backdrop of weakening economic data. They believe the share market's huge focus on Fed policy, as opposed to fundamental economic activity, can only be temporary; at some point markets will reflect current economic reality, with prices responding accordingly. |

| More Information |

19 Jul 2019 - Fund Review: Bennelong Twenty20 Australian Equities Fund June 2019

BENNELONG TWENTY20 AUSTRALIAN EQUITIES FUND

Attached is our most recently updated Fund Review on the Bennelong Twenty20 Australian Equities Fund.

- The Bennelong Twenty20 Australian Equities Fund invests in ASX listed stocks, combining an indexed position in the Top 20 stocks with an actively managed portfolio of stocks outside the Top 20. Construction of the ex-top 20 portfolio is fundamental, bottom-up, core investment style, biased to quality stocks, with a structured risk management approach.

- Mark East, the Fund's Chief Investment Officer, and Keith Kwang, Director of Quantitative Research have over 50 years combined market experience. Bennelong Funds Management (BFM) provides the investment manager, Bennelong Australian Equity Partners (BAEP) with infrastructure, operational, compliance and distribution services.

For further details on the Fund, please do not hesitate to contact us.

18 Jul 2019 - Crazy Bankies Misread APRA

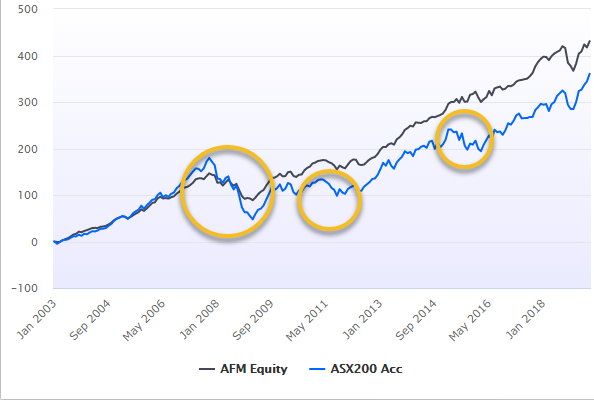

18 Jul 2019 - Fund Review: Bennelong Kardinia Absolute Return Fund June 2019

BENNELONG KARDINIA ABSOLUTE RETURN FUND

Attached is our most recently updated Fund Review. You are also able to view the Fund's Profile.

- The Fund is long biased, research driven, active equity long/short strategy investing in listed ASX companies with over ten-year track record.

- The Fund has significantly outperformed the ASX200 Accumulation Index since its inception in May 2006 and also has significantly lower risk KPIs. The Fund has an annualised return of 9.29% p.a. with a volatility of 7.06%, compared to the ASX200 Accumulation's return of 6.34% p.a. with a volatility of 13.22%.

- The Fund also has a strong focus on capital protection in negative markets. Portfolio Managers Mark Burgess and Kristiaan Rehder have significant market experience, while Bennelong Funds Management provide infrastructure, operational, compliance and distribution capabilities.

For further details on the Fund, please do not hesitate to contact us.

17 Jul 2019 - Fund Review: Bennelong Long Short Equity Fund June 2019

BENNELONG LONG SHORT EQUITY FUND

Attached is our most recently updated Fund Review on the Bennelong Long Short Equity Fund.

- The Fund is a research driven, market and sector neutral, "pairs" trading strategy investing primarily in large-caps from the ASX/S&P100 Index, with over 16-years' track record and an annualised returns of 14.81%.

- The consistent returns across the investment history highlight the Fund's ability to provide positive returns in volatile and negative markets and significantly outperform the broader market. The Fund's Sharpe Ratio and Sortino Ratio are 0.89 and 1.43 respectively.

For further details on the Fund, please do not hesitate to contact us.

16 Jul 2019 - Auto Trader: Finding opportunities amongst the Brexit wreckage

16 Jul 2019 - Performance Report: Cyan C3G Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | Cyan C3G Fund is based on the investment philosophy which can be defined as a comprehensive, clear and considered process focused on delivering growth. These are identified through stringent filter criteria and a rigorous research process. The Manager uses a proprietary stock filter in order to eliminate a large proportion of investments due to both internal characteristics (such as gearing levels or cash flow) and external characteristics (such as exposure to commodity prices or customer concentration). Typically, the Fund looks for businesses that are one or more of: a) under researched, b) fundamentally undervalued, c) have a catalyst for re-rating. The Manager seeks to achieve this investment outcome by actively managing a portfolio of Australian listed securities. When the opportunity to invest in suitable securities cannot be found, the manager may reduce the level of equities exposure and accumulate a defensive cash position. Whilst it is the company's intention, there is no guarantee that any distributions or returns will be declared, or that if declared, the amount of any returns will remain constant or increase over time. The Fund does not invest in derivatives and does not use debt to leverage the Fund's performance. However, companies in which the Fund invests may be leveraged. |

| Manager Comments | Cyan noted there were a couple of wins this month that helped drive the Fund higher. Their IPO investment in co-working space provider Victory Offices listed at a 10% premium; Cyan have since added to their initial position. The Fund's best performer in June was Kelly Partners (+25%). The other win they had this month was the revaluation of some escrowed Atomos shares Cyan purchased back in March at 60c. Atomos closed at $1.03 but has traded higher again in July having raised $7.5m in new capital and completed a sell-down. Cyan reiterate in this month's report that, whilst month-to-month volatility can be expected, they have a firm view of long-term opportunity and remain confident in the outlook for the Fund into the future. |

| More Information |