NEWS

1 Sep 2025 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

|

||||||||||||||||||||||

| Wilson Asset Management Leaders Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

||||||||||||||||||||||

| La Trobe Australian Credit Fund - 12 Month Term | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

||||||||||||||||||||||

| RMC Enhanced Income Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Remara Investment Grade Credit Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Remara Credit Income Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

| Remara Credit Opportunities Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

| Remara Opportunistic Development Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

Want to see more funds? |

||||||||||||||||||||||

|

Subscribe for full access to these funds and over 900 others |

29 Aug 2025 - Hedge Clippings |29 August 2025

|

|

||

|

Hedge Clippings | 29 August 2025

News | Insights New Funds on FundMonitors.com The art of the comeback | Magellan Asset Management Recognising a stumble from a fall | Canopy Investors July 2025 Performance News Equitable Investors Dragonfly Fund DAFM Digital Income Fund (Digital Income Class) |

||

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday |

29 Aug 2025 - Performance Report: TAMIM Fund: Global High Conviction Unit Class

[Current Manager Report if available]

28 Aug 2025 - Performance Report: ASCF High Yield Fund

[Current Manager Report if available]

28 Aug 2025 - Are you sure about that? The folly of forecasting

27 Aug 2025 - Performance Report: Insync Global Quality Equity Fund

[Current Manager Report if available]

27 Aug 2025 - Recognising a stumble from a fall

|

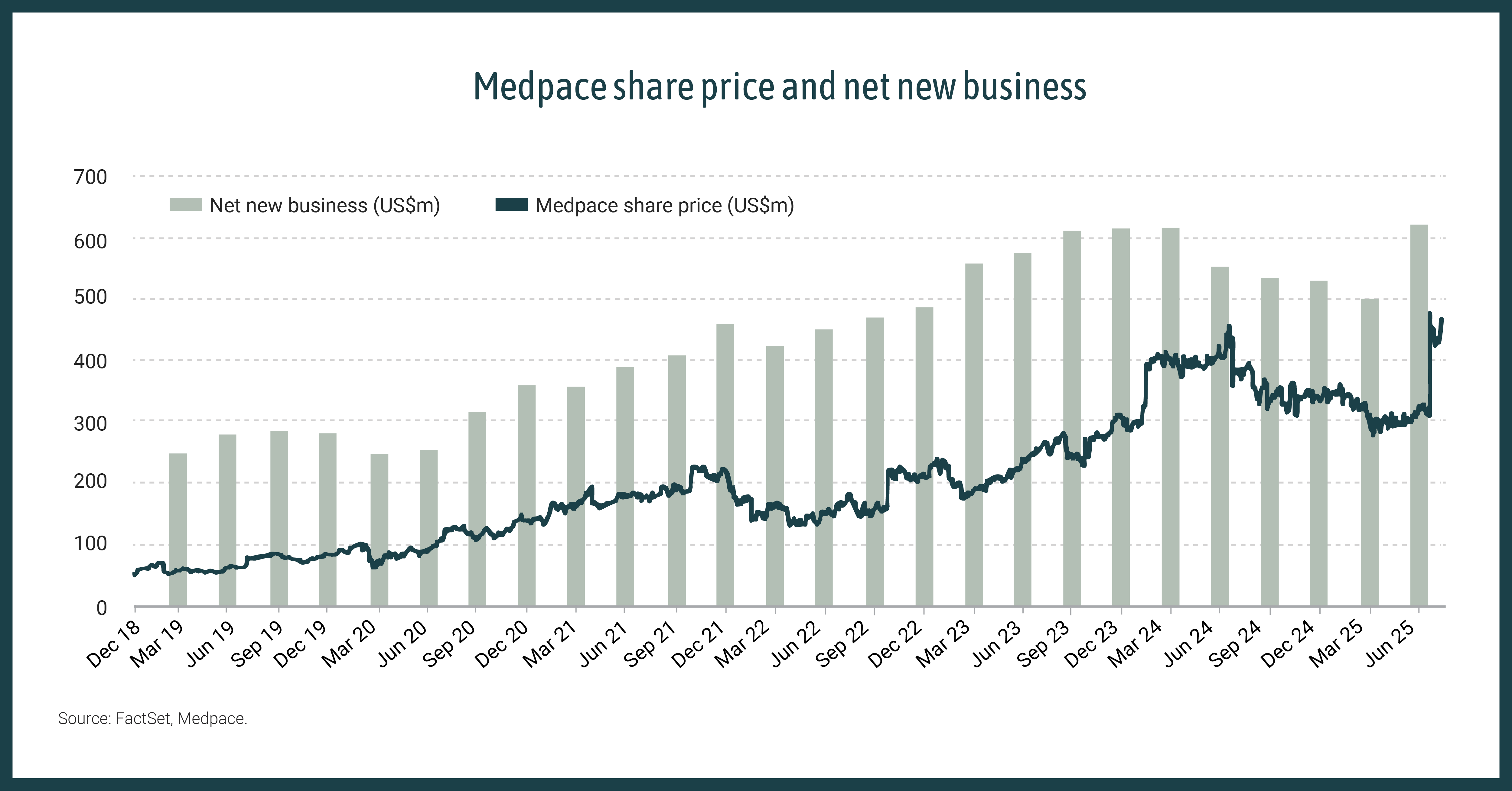

Recognising a stumble from a fall Canopy Investors August 2025 Quality companies typically trade at premium valuations, but when cyclical headwinds are conflated with secular falls, even the best businesses can be dismissed by the market. When heroes stumble excessive negativity can present opportunities to buy quality at a discount. Quality companies are often not hard to spot. The best are well known and trade at a premium valuation as a result. Despite their appeal, quality companies can be risky investments if the price paid is too high. Yet there are times when investors have the opportunity to buy quality at a discounted price, often when cyclical headwinds are conflated with secular concerns, fuelling negative sentiment and fear that the stock is 'dead money' with limited near-term upside. Medpace (MEDP)Take Medpace, for example, an investment in the Canopy Global Small & Mid Cap Fund. This founder-led clinical research organisation focuses on small biotechs and boasts an enviable track record: many years of sales growth exceeding 20%, expanding margins and returns, high cash conversion, and no debt. Its sales represent less than 5% of an addressable market expected to grow 10% pa over the long term. However, from mid-2024 Medpace disclosed lower net new business wins for four consecutive quarters, due to an unexpected increase in trial cancellations by its clients, blamed mostly on a weak funding environment. A litany of additional concerns piled on: potential negative impacts from US drug pricing policy changes, cuts to FDA and NIH funding under the new Secretary of Health and Human Services, and pricing pressure from larger competitors. Despite no fundamental change in the scale of unmet medical need addressed by small biotech, or to Medpace's ability to capture this long-term opportunity, the stock was dismissed by many as 'dead money' with no obvious near-term catalysts, and its share price declined by one-third over the course of a year. At Canopy, we believe investing in high-quality companies at the moment of maximum market pessimism can deliver high returns with relatively low risk. Our Fund holds positions in several companies at various points in their dead money journey. In this instance, we increased our investment in Medpace as investor concerns mounted and the share price fell, improving its return potential, even as the recovery timing remained uncertain. Eventually, the fundamentals reasserted themselves. In Q2, Medpace delivered a surprisingly strong result, with cancellations reverting to normal levels, driving higher net new business growth, which should support higher revenue growth over the coming years. When a positive surprise occurs in a so-called dead money stock, the reaction can be dramatic: Medpace's share price increased 50% the day after the Q2 result. While there was probably no way of predicting the result in advance, the Medpace experience highlights how long term investors can recognise a stumble, as opposed to a fall, and with conviction in the company's long-term prospects, buy quality at a discount.

Source: FactSet, Medpace |

|

Funds operated by this manager: |

26 Aug 2025 - Performance Report: DAFM Digital Income Fund (Digital Income Class)

[Current Manager Report if available]

26 Aug 2025 - The art of the comeback

|

The art of the comeback Magellan Asset Management August 2025 |

|

The investment world often prizes consistency and upward momentum--but some of the most compelling returns come from companies that have temporarily lost their way. In a recent Magellan In The Know podcast, Investment Analysts Hannah Dickinson and Emma Henderson shed light on how discerning investors can tap into turnaround stories in the consumer sector and, more importantly, how to separate real opportunity from value traps. What makes a turnaround worth it?At Magellan, a turnaround doesn't mean betting on distressed companies or moonshot startups. Instead, it refers to high-quality businesses facing temporary setbacks--strategic or operational missteps that lead to material share price declines but are fixable. The rewards for identifying a true turnaround early can be significant. Successful recoveries can often result in share price rallies of 50% or more. However, the risks are just as real: historical studies show that only 20-30% of corporate turnarounds actually succeed. That's why we maintain a high bar, filtering only a few Four pillars of turnaround investingThe Magellan investment team apply a disciplined framework to assess whether or not a company genuinely has turnaround potential. The framework is built on four pillars: 1. Fundamentals: Is the business still high quality?Before diving into a company's recovery strategy, we ask ourselves whether or not the business still retains its core strengths. For example, Nike, despite recent setbacks, continues to operate in an attractive industry (sportswear) and retains global brand equity and competitive advantages. Similarly, Kering's challenges On the other hand, companies like Pepsi face more ambiguous issues, such as structural health concerns and policy shifts. These situations, while not necessarily doomed, are harder to categorise as classic turnarounds. 2. Leadership: Who is at the helm?Successful turnarounds often depend on the right CEO. Ideally, this is someone new--an outsider with full autonomy and a mandate to make bold changes. Starbucks offers a telling case: after several underwhelming leadership transitions, the company brought in Brian Niccol from Chipotle, whose track record and However, we would warn that even a celebrated CEO appointment doesn't guarantee success. If governance structures are weak or the leadership lacks experience in managing complexity, execution can flater. 3. Strategy and complexity: Is the plan credible?We look for turnaround strategies that focus on reinforcing a company's core competitive strengths rather than cost-cutting for short-term gains. Estée Lauder, for instance, operates in a highly attractive beauty market and has new leadership but its current plan leans too heavily on easy wins like headcount reduction and Amazon partnerships. We are cautious here, citing concerns regarding innovation, outdated IT systems and supply chain complexity. Nike, by contrast, has a more straightforward strategy: refresh its product innovation pipeline and rebuild damaged retail relationships. These are fixable issues that don't require reinvention of the business model. 4. Timing: Where are we in the recovery cycle?Rather than trying to 'time the market', we assess whether the company is early, mid, or late in its turnaround phase. Has a credible CEO been appointed? Is the strategy clearly communicated? Have investor expectations been reset? Nike again stands out as a case where much of the heavy lifting has occurred already. Product pullbacks have been made, reinvestment is underway, and green shoots in innovation are expected in the next 12-18 months. Conversely, Kering's turnaround is still in its early days with leadership in place, but Valuation and portfolio disciplineValuation is particularly tricky in turnarounds, where near-term earnings are often depressed. We move beyond simple metrics like P/E ratios and instead focus on scenario analysis, assessing a range of possible outcomes and the probability distribution of returns. Position sizing and diversification are critical. Turnarounds typically enter the portfolio as small allocations, with the Magellan investment team continually monitoring signs of progress closely. If the share price falls, we revisit the evidence: is the thesis still intact? If so, we may average down; if not, we remain disciplined in selling. It's not for the faint-hearted, but worth the effortTurnarounds are rarely smooth. They require patience, rigorous analysis, and a clear-eyed view of both risk and reward. However, when done correctly, anchored by strong fundamentals, capable leadership, credible strategy and well-timed execution, they may unlock unique, outsized returns. That said, these opportunities don't come easily. They demand deep sector knowledge, disciplined valuation work, ongoing monitoring, and the ability to separate short-term noise from meaningful signals. For individual investors, that level of commitment and emotional resilience can be difficult to sustain. That's why turnaround investing is often best approached with a disciplined framework and the resources to dig deep. It takes experience to cut through the noise, the analytical firepower to deeply understand what's truly going on inside a company, and the ability to avoid behavioural traps and know when the risk-reward equation truly stacks up. For investors willing to do the work, turnarounds could be one of the most rewarding corners of the market. |

|

Funds operated by this manager: Vinva Global Alpha Fund - Active ETF (ASX: V1AC) , Vinva Australian Equity Fund , Vinva Global Equity Fund , Vinva Australian Alpha Extension Fund , Vinva Global Alpha Extension Fund , Magellan Infrastructure Fund , Magellan Global Opportunities Fund No.2 , Magellan Infrastructure Fund (Unhedged) , Magellan Core Infrastructure Fund , Magellan Global Opportunities Fund Active ETF (ASX:OPPT) Important Information: Copyright 2025 All rights reserved. Units in the funds referred to in this podcast are issued by Magellan Asset Management Limited ABN 31 120 593 946, AFS Licence No. 304 301 ('Magellan'). This material has been delivered to you by Magellan and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision about whether to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to a Magellan financial product may be obtained by calling +61 2 9235 4888 or by visiting www.magellangroup.com.au. The opinions expressed in this material are as of the date of publication and are subject to change. The information and opinions contained in this material are not guaranteed as to accuracy or completeness. Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward looking' statements and no guarantee is made that any forecasts or predictions made will materialise. No representation or warranty is made with respect to the accuracy or completeness of any of the information contained in this material. Magellan will not be responsible or liable for any losses arising from your use or reliance upon any part of the information contained in this material. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Magellan. Further important information regarding this podcast can be found on the Insights page on our website, www.magellangroup.com.au. |

25 Aug 2025 - Performance Report: Argonaut Global Gold Fund

[Current Manager Report if available]