NEWS

24 Aug 2018 - Hedge Clippings, 24 August 2018

Where's the leadership we deserve?

At a time when the government needed leadership, unity and stability, the combination of personal ambition and the desire for revenge delivered exactly the opposite. Irrespective of who one believed should be in the top job, the country deserved better, and only time will tell if it gets it.

Personalities, and personal ambition, and in our view a misreading of the mood of the majority of people in the street, has resulted in the running of the country put to one side, while a bunch of self-centered politicians have indulged themselves, in just the same way as their predecessors did.

The real tragedy is that the economy, while not booming, is sound and growing, employment is growing, inflation and interest rates are low (probably too low) and taxation, except for the "big" end of town, is coming down. The federal budget is forecast to make it back to a surplus way ahead of forecast, and given the potential change of government at the next election, that's probably now in doubt.

If there's one good (?) thing to come out of the debacle in Canberra it's probably that the chief destabiliser and those pulling the strings didn't win, although they'll no doubt be happy enough they've dispatched the one person - now the previous PM - they didn't want to win. The question is will they now be satisfied and pull their heads in, or will they work to destabilise another moderate?

If there's one good (?) thing to come out of the week's media focus it is that the Hayne Royal Commission wasn't on the front pages.

Meanwhile AMP's appointment gets out thumbs up - experience and ability, and hopefully prepared to make the changes necessary - or enforced by the HRC and future legislation. Hedge Clippings has previously been critical of both AMP and David Murray, but this is a good and smart move. However, there's still a long, long way to go.

17 Aug 2018 - Hedge Clippings - 17 August 2018

Hayne Royal Commission - the ongoing revelations are taking their toll on so many reputations:

ANZ, NAB, IOOF, and Ric Allert from AMP Trustees were enlightening this week at the HRC, but for all the wrong reasons.

AMP Trustees simply haven't been doing what they should have - namely looking after other peoples' money. Rather it seems they're simply looking after themselves and AMP.

Meanwhile, IOOF's board notes are akin to a second former's (not sure if in junior or senior school).

NAB played with ASIC, and indulged in some cute information timing.

ANZ played with the rules, and played with …. Other peoples' money!

It seems not to matter if it occurs at "Industry" or "For Profit" funds. Of course Hostplus need to spend hundreds of thousands of dollars taking prospective clients to the Australian Open tennis. Oops, 'so I had to take the wife and kids as well to fill a few spare seats'. What, no fund members could be found at short notice and invited along?

And it's a great use of members' funds to sponsor the footy - but I wonder which team the Hostplus CEO barracks for? Oh! Surprise, Surprise, the Richmond Tigers. And who sponsors the Tigers (and admittedly some other clubs)? Hostplus! I'm sure there are always a few seats in the sponsor's box at the MCG reserved for Hostplus' super members.

And a staff lunch? Forget the local restaurant across the road from the Hostplus offices in Melbourne's William Street. We'll just pop up the road to the Flower Drum at the Paris end of town.

Full marks to Hostplus for being a top performing fund. But that should be enough to get employers and others to park their retirement savings with them. Not for taking family to the tennis, CEO's of employers to the footy, or staff to the "Drum" for a not inexpensive Chinese meal (trust me, I've had a few there in days gone by) .

Remember, it's other peoples' money. That's taking the old adage of "looking after it as if it is your own" just a tad too far!

10 Aug 2018 - Hedge Clippings, 10 August, 2018

Are we becoming immune to poor corporate governance?

It would be unfair to call it boring, but the Hayne Royal Commission (HRC) is becoming so repetitive it's almost predictable, so much so that it's losing its shock factor.

Misdeeds at the big end of the financial system? So what? We all either knew that, or suspected it, and by now we have heard it all (or much the same) before. No wonder the banks fought so hard against the RC being established in the first place.

In any other area, the charging of fees for no service would be called for what it is - a SCAM. If perpetrated by an individual advisor they'd be struck off in quick time. But at executive and board level different rules obviously apply. The key point going forward is not how much financial pain is inflicted on executives via lost or reduced bonuses, or penalties on the banks themselves (which of course flow on to shareholders), but the potential for criminal charges to be laid.

That, to excuse the pun, might help to arrest the problem.

Whilst this might seem extreme, the reality is that theft has occurred, deliberately, knowingly, and frequently - and worse still more often than not at the expense of those most vulnerable, both as a result of their lack of financial interest or knowledge, or those least likely to be able to afford it in terms of their financial security in the future.

What is astounding is that, like at AMP, the senior ranks of the banks such as CBA and NAB knew of the theft, and did nothing to fix it - even worse, NAB did whatever they could to obfuscate to protect their position, including asking Mr Hayne to keep it confidential.

Nothing will focus their minds more than the prospect of some quiet, reflective time in a green uniform, with set meal times, and limited visiting hours.

CEO's and chairmen (and women, although there's been little apology we can recall from AMP's previous Chair) may apologise' but saying sorry is one thing. Changing the systemic cultural and operational problems are another.

By contrast, Australian Super's Mr Silk gave a "smooth as" performance, partly as a result of what seemed to be a less severe interrogation, itself quite possibly because there have been fewer misdemeanours uncovered on his watch. We'd still like to see the HRC delve into where the fees behind industry super flow - over and above purchasing shares in the New Daily. That problem's unlikely to resolved while the boards and trustees of industry funds are not required to have independent members.

Unfortunately the superannuation pie is so large, so opaque, and in many respects so distant from the majority of contributors and beneficiaries that it is going to take some serious government intervention to change the current malpractices. And while talking of change, with an election looming in less than a year from now, it's likely the "for profit" sector is likely to be firmly in Canberra's sights, while the "industry" sector will remain as opaque as ever.

Pity the poor punter!

3 Aug 2018 - Hedge Clippings, 3 August 2018

David Murray takes (yet another) tilt at ASIC

David Murray's antipathy towards ASIC goes back a long way so it was always going to be interesting to see if he would temper his comments once he took the chair at AMP.

Far from being conciliatory, this week he upped the argument considerably, whilst conveniently forgetting, or more correctly ignoring, the fact that AMP's track record with the regulator is less than exemplary.

For example, the chairman and board lying to ASIC is not something one would really like to have on one's corporate tombstone - or CV.

Neither is charging investors for services not received, nor consistently favouring in-house and underperforming products, and thereby making a mockery of the term "independent financial advice".

One presumes that David Murray's approach to ASIC follows the line that the best form of defence is "attack, attack, attack", or that other well tried defence, "deny, deny, deny".

There's no doubting that the level of compliance and regulation required by ASX listed companies (and unlisted ones if it comes to that) is significantly greater than it once was, but how each one implements ASIC's guidance can vary from company to company. What is quite obvious is that AMP's previous chair and the board took a very detailed and hands-on approach to management, and as the record shows, quite simply failed in the execution.

Going forward expect more entrenched criticism of ASIC from David Murray, but what will now be interesting will be who he appoints as CEO, and how they both manage to change the culture, practice and business model at AMP (assuming Murray intends to do so).

The market and the AMP share price will no doubt tell the story over time.

Meanwhile, next week sees a resumption of the Hayne Royal Commission, this time around focusing on the Superannuation sector. No one is likely to be surprised (although they might be shocked) at the revelations that will no doubt be exposed.

27 Jul 2018 - Hedge Clippings, 27 July 2018

The Royal Commission and the Boiling Frog

Hedge Clippings is reminded of the old adage of the boiling frog - which for those not familiar with it went as follows: If you put a frog into a pot of cold water and put it over a low flame for a long time, the frog would eventually end up "poached". However, if the frog was dropped into a pot of already boiling water it would instantly react by jumping out, and be saved.

In financial services parlance the industry has been on a long slow journey towards being poached, although maybe the Hayne Royal Commission has arrived just in time to create a "boiling frog" moment which will result in it being saved - although not without a severe scorching, and only if the powers that be, and those in charge at the big end of town, take the opportunity to change.

The (long overdue) Hayne Royal Commission has shone - or is shining - a welcome (depending on where one stands) torch on every aspect of the financial services sector. This has now been followed by the Productivity Commission's 500+ page report into Superannuation, particularly focusing on fees and poor performance, and with suggestions of a Top Ten "Best in Show" default system. Now, not surprisingly, ASIC is going to give added focus on the sector, whilst Treasury has also weighed into the debate.

Why has this been able to occur?

Simply because the majority of consumers are not financially literate, and of those that are many have the knowledge to be "self-directed". Meanwhile, most (although not all) of those heading up the industry are very financially literate, and stand, or stood, to make a motza out of the system, the lack of real scrutiny, and a lack of ethics.

Whilst easy to point the finger at the financial advisor actually providing advice to the consumer, the reality is that the real cause is the problem is the systematic and conflicted structure of the industry - be it banking, superannuation, mortgage broking or financial advice. The vast majority of advisors would prefer to give their clients independent financial advice - as evidenced by the significant numbers choosing to do so by moving to an independent AFS licensee.

Back to the Royal Commission. Round 5 is due to start on 6th August, focusing on superannuation, and will run for 2 weeks.

Round 6, slated for 10 September, will cast its eye on Insurance, while Round 7 on the 19th November will focus on policy questions arising from rounds 1-6. In between time the CEO's from the big end of town will get their time in the witness box, and anecdotal evidence suggests their minions are putting in long hours beavering away to make sure it won't be too uncomfortable for them.

Some hope.

Talking of hope, Hayne's preliminary report is/was due no later than 30 September, and the final report due by 1 February (2019). Happy Christmas holidays to Mr Hayne and his team trying to meet that deadline.

20 Jul 2018 - Hedge Clippings, 20 July 2018

It seems fund rankings are in the news in the past couple of days, whether it be super funds, or managed funds available outside super.

Taking super funds first, there seem to be two schools of thought, each not surprisingly probably dependent where the self-interest of the thinker lies.

Super Ratings tables clearly show that industry super funds have outperformed the bank and for-profit sector funds, and while they will understandably promote their performance and claim that it is due to lower fees, they will also rightly claim that asset allocation plays a significant part in their success.

On the other hand Colonial has argued that it is not a simple comparison and the options available, along with the demographics of the fund members, are significant. What is relevant is that the massive number of options and alternatives available make it incredibly difficult not only to compare funds and the returns, but also for the investor to choose the appropriate option.

Whatever the arguments the logic and argument from the Productivity Commission that across the board fees be reduced to match those available in comparable products and jurisdictions overseas, but that there should be a simple default option of the top 10 performing funds.

The complexity of the current array of choices simply makes it impossible for the average person to make an informed choice.

Moving on to managed funds outside superannuation, the tables in today's Financial Review, supplied by Mercer, make interesting reading and will equally no doubt be promoted by each of the relevant funds.

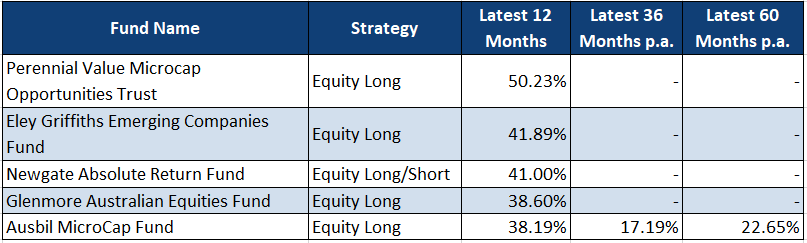

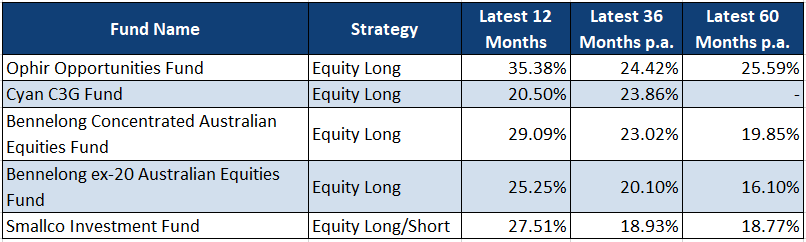

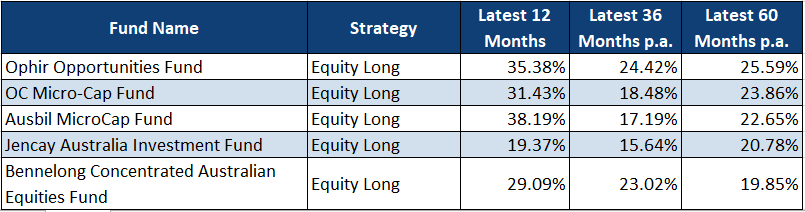

What is interesting is that when Australian Fund Monitors analyses results to the end of June (bearing in mind not all funds have reported as yet) for the past one, three and five years, there are some significantly interesting trends:

- Firstly when it comes to 12 month performance Australian equity funds (whether long only or long short), four out of the top five were early stage managers who do not yet have a three or five year track record.

- The emerging or micro-cap sector dominates, having been particularly strong over the past 12 to 24 months, particularly with the Banks and Telstra taking a battering.

- All are concentrated - it is simply impossible to provide these kind of returns when the ASX accumulation index returned 13% without significant stock picking skills (as opposed to Super, where asset allocation is a primary driver of performance).

Finally, in a rising market, with the exception of Newgate and Smallco, Long Only funds dominated.

Taking the top five performing funds over three years, the table looks like this:

Then taking the best performers over five years, the results are as follows:

Before we receive a raft of complaints from those managers with better returns in a specific year than those listed, we applied a consistency filter, which with the exception of the earlier stage funds in the one and three year tables, took out any fund with a performance of less than 15% over either one, three or five years. Equally, the above tables only include equity based funds with a geographic mandate of Australia and New Zealand, so Asian and Global funds were excluded.

Methodology is always important when ranking and filtering funds, and purely selecting the top performing funds based on returns is always risky, simply because looking at returns, without looking at risk factors such as volatility , Sharpe ratios, draw downs and up and down capture ratios, doesn't tell the whole picture.

And of course the overall disclaimer that "past performance is no guarantee of future returns" applies - although we consider it to be highly relevant.

13 Jul 2018 - Hedge Clippings, 13 July 2018

Last week's deadline for - and subsequent introduction of - the tit for tat trade tariffs on $34 billion of goods between the US and China seem to have come and gone without the end of the economic world as we've come to know it, but to be fair it is probably much too early to tell how this will play out. It may only be 0.1% of their respective GDP's, but the fact that the so-called "Chimerica Trade" is estimated to approach 40% of the global total puts it into perspective.

Meanwhile The Donald has moved on to Europe, using his "stable genius" negotiation approach to resolve NATO's funding future, before hopping across the English Channel to give some (we imagine unwelcomed) advice to Theresa May, while adding that he "gets along with her nicely" and thinks she's "a nice person".

At this point in time we haven't heard her response - on or off the record - and we're also not sure if Donald has yet worked out why he feels unwelcome in the "London he used to love".

Meanwhile back at home the Hayne Royal Commission has advised it will shortly be turning its attention to superannuation funds which must fill the 30 or so lucky directors due to take the stand come August 6th with trepidation. Hayne will be looking at such uncomfortable aspects as "acting in the best interest of members, not unions, employer groups or shareholders", and has requested they provide papers of board meetings and sub-committees stretching back five years.

Leading up to this, Commissioner Hayne will no doubt be getting to know the Productivity Commission's 570 page report on the $2.6 trillion superannuation sector, which itself was pretty scathing, but with his added powers and the glare of the lights on the witness box, there should be more headlines in store.

Not, however, too many surprises! The "for profit" sector funds consistently underperform, and lest the "industry funds" think they're going to be getting off lightly, there will no doubt be all sorts of uncomfortable questions around cosy deals with unions, a lack of appropriate knowledge and expertise at board level, not to mention their ongoing refusal to appoint independent directors. We wonder why?

It is inconvenient timing therefore that an unfair dismissal case against Australian Super, alleging conflicts of interest and cosy related-party deals, is currently making the news. Or the report we saw recently that estimated that with lower fees the $2.6 trillion currently in super would be worth closer to $3.4 trillion.

No wonder the SMSF sector is so popular, even if some funds with lower balances are uneconomic. At least their trustees get to make their own decisions, and pay for their own mistakes.

6 Jul 2018 - Hedge Clippings, 6 July 2018

Trying to predict the eventual outcome of the looming trade war between the US and China is about as difficult as trying to predict Donald Trump's next policy announcement. However, a reasonable prediction would be that neither side enjoys losing face, and therefore is unlikely to back down at the first hurdle.

For those that have missed it at 2 PM today America is due to slap a 25% duty on $34 billion worth of Chinese imports, ranging from machinery to electronic parts. As night follows day Tit is liable to follow Tat, meaning that China will immediately respond with equivalent tariffs focused on American farm goods.

While $34 billion seems a fair chunk to Hedge Clippings, they only represent about 0.1% of GDP for both the Titter (the US) and the Tatter (China). However the real risk lies in the Donald's approach to negotiation, and we would imagine China's approach to backing down. Assuming both parties perform as expected by most pundits, as opposed to how each hopes the other will react, it seems pretty likely that tensions, the damage to each country's economy, will increase.

However the US economy is in a very different place to China's, with a strong stock market, improving growth, and bond rates that in spite of dire predictions, and inevitable Fed tightening, seems not to have upset the apple cart (yet). Growth in the second quarter of the year is likely to exceed 3.5% annually, and unemployment is falling. Apart from the trade war, the major risk seems to be that there will in fact be an eventual outbreak of inflation, currently just above the FED's target of 2%.

Conversely, in China the equity market has fallen 20%, and the authorities are grappling to control credit. Over the past 20 years, having become the world's factory and having exported deflation as a result, a nasty trade war with the US could be the trigger to signal the end of the miracle.

Meanwhile, we assume the economy of all other countries, including Australia, caught in the crossfire will be considered collateral damage, although depending on who sides with whom, and who can negotiate what, will depend on the eventual outcome.

29 Jun 2018 - Hedge Clippings, 29 June 2018

David Murray's problems with ASIC go back a long way, but more recently he's upped the ante even further as he attempts to justify Vertical Integration within the financial services industry, and AMP in particular.

It is worth remembering that Murray (who prior to his soon to be current gig as AMP's chairman) had only ever worked at CBA. He was both the architect, engineer and implementer of their vertical integration model, taking the likes of Colonial, Aussie Home Loans, and Count Financial into the bank in his quest to gain a greater share of the customer's wallet. In a classic case of "if you can't beat 'em, buy, buy, and buy more of 'em" he added financial planning, accountancy, and mortgage broking to the product suite, while Colonial's investment platform created the perfect distribution model.

Except it wasn't perfect, as clients of Storm Financial and others have experienced, and as the Hayne Royal Commission has recently exposed. Leading the charge to take market share, and make profits at any cost, often leaves the client's best interest coming a long way third - if it features at all - in the process. As a result, CBA's incoming CEO Matt Comyn has wasted little time in announcing the demerger of "wealth" from "banking" and undoing much of Murray's work at CBA in the process.

Murray's previous run in with ASIC included him comparing the regulator to Hitler's Nazis, for which he was forced to apologise. Last week, just as he prepares to take the reins at AMP, he engaged in a little more ASIC bashing claiming the regulator had lost its way under Greg Medcraft, and wasn't focussed on its main job.

Meanwhile, ASIC is going after AMP's financial planning arm through the courts, so we'd like to be a fly on the wall when the regulator's new chairman James Shipton and David Murray first sit down for a quiet chat and a cup of tea. Just try typing David Murray and ASIC into Google to get a flavour of how the conversation might run.

In many ways, Murray, whose reputation and knowledge of the financial services is undoubted, makes him a perfect choice to head up the organisation which has managed to trash its reputation and decimated the ranks of its board and senior management.

In others he's probably the worst. The world has changed and vertical integration is on the nose, in decline. Not only has the AMP got to change, but Murray's got to learn a new game at the same time.

AMP's problem is that without vertical integration it has an uncertain future as it struggles to distribute its frequently uncompetitive products through a tied sales force. ASIC will be watching with interest.

22 Jun 2018 - Hedge Clippings, 22 June 2018

The government was understandably excited to get their personal income tax legislation through the Senate yesterday, but the fact that it came down to such a knife edge decision is of concern. It remains to be seen whether they will now be able to get the proposed company tax changes through the Senate next week, but with the second highest company tax rate amongst OECD countries, how can Australia compete on the world stage unless they do?

Australia needs to be competitive, and needs a competitive taxation system to be able to do so. Not only is it not competitive, it remains excessively complex, with a GST rate way below most other countries, and only levied on half the economy. It reinforces RBA Governor Phillip Lowe's comments a week ago that the Australian population had no stomach for tax reform.

It was interesting to see the governor of the RBA weigh into the debate, noting that the personal income tax cuts were only the "first step" in the right direction, saying that they were merely incremental, and falling short of "that kind of first-order tax reform that will make a fundamental difference" to productivity growth.

Hedge Clippings believes that the Australian population has, in general, plenty of stomach for tax reform, but the combination of a political process which results in both parties automatically opposing the other's policy, political expediency which encourages negativity (not to mention happily lying in the process), and the inability of either party to successfully prosecute a policy change, leave the Australian population with an overly complex and uncompetitive taxation system.

If the RBA Governor was prepared to speak up, maybe it is time for both the population and the politicians to listen. What is disappointing is that previous governments have had their chance, but didn't have the stomach for tax reform. Ken Henry's 2010 review of the taxation system (excluding the GST which he wasn't allowed to include in the final report) proposed 9 broad themes (still applicable today) covering 138 recommendations, of which the then government implemented only three.

So full marks to the current government for progress to date, but there's an awfully long way to go yet. As the Chinese proverb states, "A journey of a thousand miles begins with a single step."