NEWS

Performance Report: Seed Funds Management Hybrid Income Fund

The Seed Funds Management Hybrid Income Fund rose by +0.74% in August. Since inception in October 2015, the fund has returned +6.43% per annum, an outperformance of +1.58% relative to the Solactive Australian Hybrid Securities (Net)...

Read more...

Turning Turbulence into Triumph: Two Stocks Mastering Market Themes

Five powerful themes are reshaping the investment landscape, creating winners and losers across global markets. The AI revolution stands as the defining narrative, driving fundamental shifts in capital allocation and valuation frameworks.

Read more...

Performance Report: Altor AltFi Income Fund

The Altor AltFi Income Fund rose by +0.93% in August, outperforming the RBA Cash Rate + 5% benchmark by +0.24%. Since inception in April 2018, the fund has returned +11.43% per annum, an outperformance of +4.44% relative to the benchmark...

Read more...

Performance Report: 4D Global Infrastructure Fund (Unhedged)

The 4D Global Infrastructure Fund (Unhedged) rose by +1.72% in August, outperforming the S&P Global Infrastructure TR (AUD) benchmark by +1.63%. Since inception in March 2016, the fund has returned +9.90% per annum, a difference of -0.56%...

Read more...

The investment case for Anta Sports: Who'd have thought Fila was alive and...

As global equity income investors, our job is to purchase good businesses when they are troubled by an investment controversy.

Read more...

Performance Report: Glenmore Australian Equities Fund

The Glenmore Australian Equities Fund rose by +5.24% in August, outperforming the ASX 200 Total Return benchmark by +2.14%. Since inception in June 2017, the fund has returned +19.44% per annum, an outperformance of +9.69% relative to the...

Read more...

Performance Report: Airlie Australian Share Fund

The Airlie Australian Share Fund rose by +0.93% in August. Since inception in June 2018, the fund has returned +10.52% per annum, an outperformance of +0.76% relative to the ASX 200 Total Return benchmark which has returned +9.76% on an...

Read more...

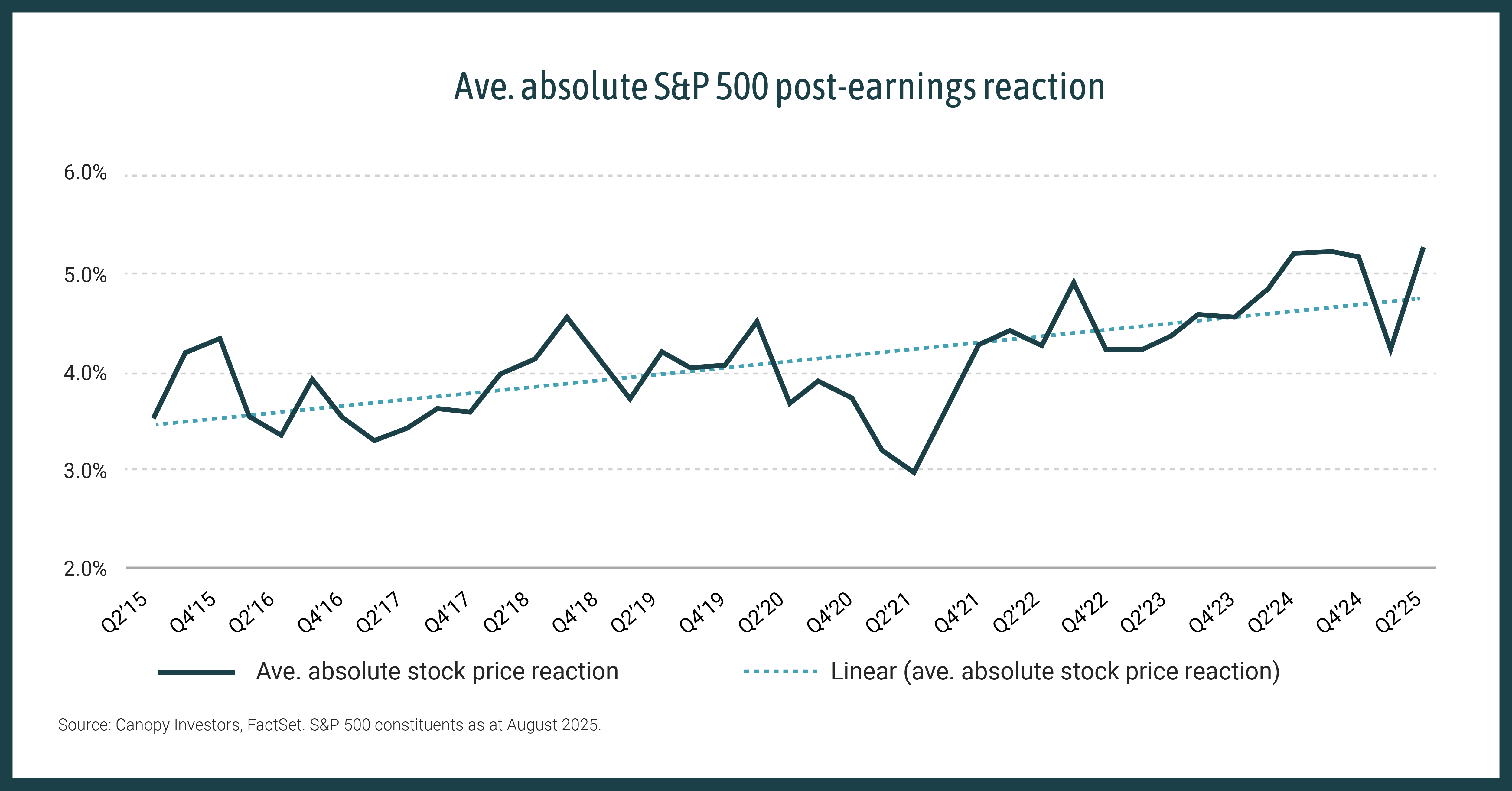

Volatility insights

If you think share prices are becoming more volatile during earnings season, you're not imagining it.

Read more...

Performance Report: Bennelong Concentrated Australian Equities Fund

The Bennelong Concentrated Australian Equities Fund has returned +12.47% per annum since inception in February 2009, an outperformance of +2.18% relative to the ASX 200 Total Return benchmark which has returned +10.29% on an annualised...

Read more...

Performance Report: ASCF High Yield Fund

The ASCF High Yield Fund rose by +0.64% in August, outperforming the Bloomberg AusBond Composite 0+ Yr benchmark by +0.31%. Since inception in March 2017, the fund has returned +8.12% per annum, an outperformance of +6.04% relative to the...

Read more...