NEWS

Manager Insights | East Coast Capital Management

Chris Gosselin, CEO of FundMonitors.com, speaks with Simone Haslinger, Chief Executive Officer at East Coast Capital Management.

Read more...

How are active ETFs reshaping the European investment market?

With the active ETF market in Europe set to hit US$1 trillion by 2030, driven by the adoption of innovative "active core" and "high-conviction active" ETFs, Michael John (MJ) Lytle, Head of Product Innovation, outlines the importance of...

Read more...

Performance Report: Equitable Investors Dragonfly Fund

The Equitable Investors Dragonfly Fund rose by +1.67% in August, driven by gains in Spectur and Wrkr, while MedAdvisor detracted from performance. Equitable remains focused on company-specific catalysts amid ongoing market volatility,...

Read more...

Investment Perspectives: Riding the silver tsunami

The aging population presents a powerful investment theme, but as the recent legal setback for Lifestyles Investment Communities (ASX: LIC) shows, execution matters. LIC's plights highlight the risks of complex structures in thematic investing.

Read more...

Performance Report: Skerryvore Global Emerging Markets All-Cap Equity Fund

The Skerryvore Global Emerging Markets All-Cap Equity Fund rose by +0.76% in August, outperforming the MSCI Emerging Markets (MMEF) AUD benchmark by +1.13%. Since inception in August 2021, the fund has returned +5.01% per annum, a...

Read more...

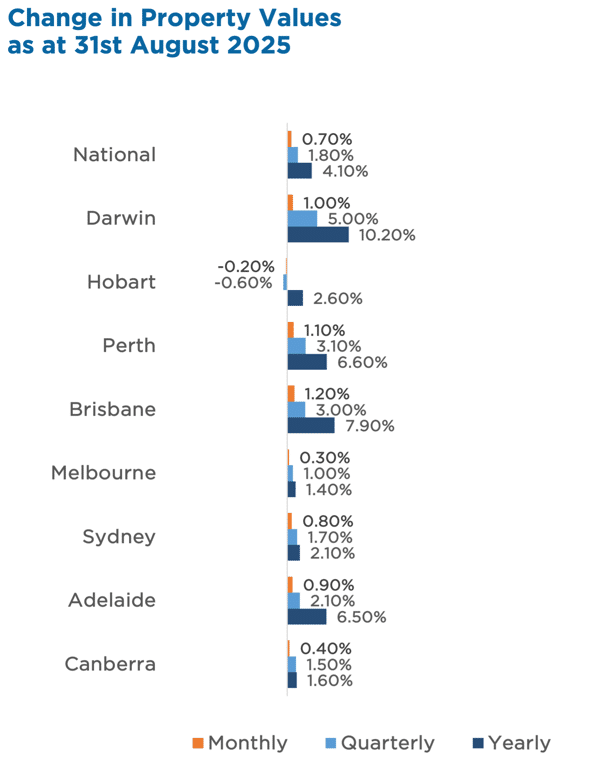

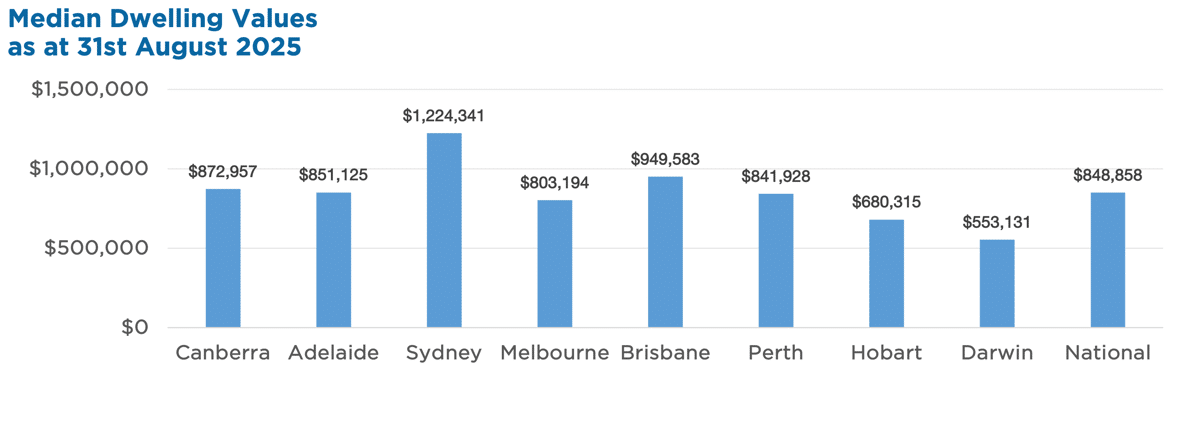

Australian Secure Capital Fund - Market Update

Australia's housing market extended its run in August, with values up 0.7%. This is strongest monthly gain since May 2024. Annual growth now sits at 4.1%.

Read more...

Performance Report: DAFM Digital Income Fund (Digital Income Class)

The DAFM Digital Income Fund (Digital Income Class) rose by +1.21% in August, outperforming the RBA Cash Rate + 3% benchmark by +0.68%. Since inception in May 2021, the fund has returned +22.58% per annum, an outperformance of +16.77%...

Read more...

New Funds on Fundmonitors.com

Here are some of the latest additions to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research,...

Read more...

Hedge Clippings |19 September 2025

The US Federal Reserve did what markets had been anticipating - and Donald Trump has been crying out for - cutting rates by 25 bps and flagging that two more are on the way. Trump will claim the credit no doubt, and his new FED appointee...

Read more...

Performance Report: Canopy Global Small & Mid Cap Fund

The Canopy Global Small & Mid Cap Fund rose by +4.26% over the past 12 months. In August, Spirax, Autozone and STERIS were the top contributors while Gartner, Tradeweb and Hemnet detracted, and Canopy remains constructive on medium-term...

Read more...