NEWS

24 Jan 2025 - The Advantages Of Being A Small Investor

|

The Advantages Of Being A Small Investor Marcus Today January 2025 |

|

I have never liked the expression "Smart money". It is demeaning to individual investors and used by the finance industry to imply they are smart and the rest of you are by implication "Dumb". But a lot of supposedly smart professionals do some very dumb things, and a lot of non-professional investors (you guys) do some very clever things. What Big Investors Can Do That You Can't There are a few "Smart Money" activities available to institutional investors that most individual investors can't access. These include: Access to IPOs and Placements Big institutions often get priority access to IPOs, share issues, and placements. They get it because the brokers controlling the issue want to suck up to them to get their secondary market business. Inside Information There's an old broker's saying--"If you're not on the inside, you're on the outside." Many private investors assume that institutional investors have access to inside information and that the market is rigged against them. But this isn't the case. I once stood in a lift with a very experienced professional trader who overheard two brokers discussing an inside tip. In his gravelly voice of experience, he said, "If I'd never been told any inside information, ever, I'd be a million dollars better off." While inside information might exist, it's neither legal nor common, even among professionals. The misconception that everyone else has it is simply not true. That's not the game. Writing Options for Incremental Gains Wealthy investors sometimes write out-of-the-money call options against existing holdings. While this strategy can generate small, incremental returns, it doesn't provide substantial gains. It's also not practical for most individual investors. Why Being a Small Investor Is an Advantage Despite the perks available to big investors, small investors enjoy significant advantages that professionals can only envy. Liquidity Isn't an Issue Institutional investors often face liquidity problems, struggling to enter or exit positions without affecting share prices. Small investors can buy and sell quickly without influencing the market. Despite the perks available to big investors, small investors enjoy significant advantages that professionals can only envy. Freedom to Adapt Unlike fund managers who must follow strict mandates, small investors can shift strategies whenever they like. You're free to act without needing approvals or explanations. The Ability to Hold Cash Fund managers often can't hold cash even when markets drop. Small investors can exit the market and wait for better opportunities, avoiding unnecessary losses. No Need for Over-Diversification Fund managers must diversify to meet benchmarks, even if it means including underperforming stocks. Small investors can focus on a few high-quality opportunities instead. No Reporting Requirements Professionals deal with compliance regulations, financial services guides, and audits. Small investors avoid these headaches, saving time and money. Minimal Costs Running a self-managed portfolio means avoiding the overheads that come with managing large funds. There are no compliance fees, licensing costs, or administrative burdens. Instant Decisions Small investors can react to market events in real-time. Fund managers, on the other hand, face internal approvals that delay decisions. The Downsides of Being a Small Investor Of course, small investors do miss out on some perks available to institutional players: No Broker Perks Big investors enjoy access to IPOs, discounted placements, and premium research. Brokers often court them with lunches and events. Limited Research Support Institutions have teams of analysts hunting for investment opportunities. Individual investors typically rely on their own research. No Excuses for Losses While fund managers can justify losses by pointing to market-wide downturns, small investors face personal accountability for their results. Why Flexibility Beats Big Money Sure, big investors get the perks--lunches, research, and IPOs but they're also stuck in a system full of rules, reports, and restrictions. Small investors, on the other hand, have the freedom to move quickly, cut costs, and make decisions without answering to anyone. And let's be honest when it comes to investing, freedom is worth more than a free lunch. Author: Marcus Padley |

|

Funds operated by this manager: |

23 Jan 2025 - Trump nominated a vaccine sceptic for health secretary. What does that mean for investors?

|

Trump nominated a vaccine sceptic for health secretary. What does that mean for investors? Redwheel December 2024 |

|

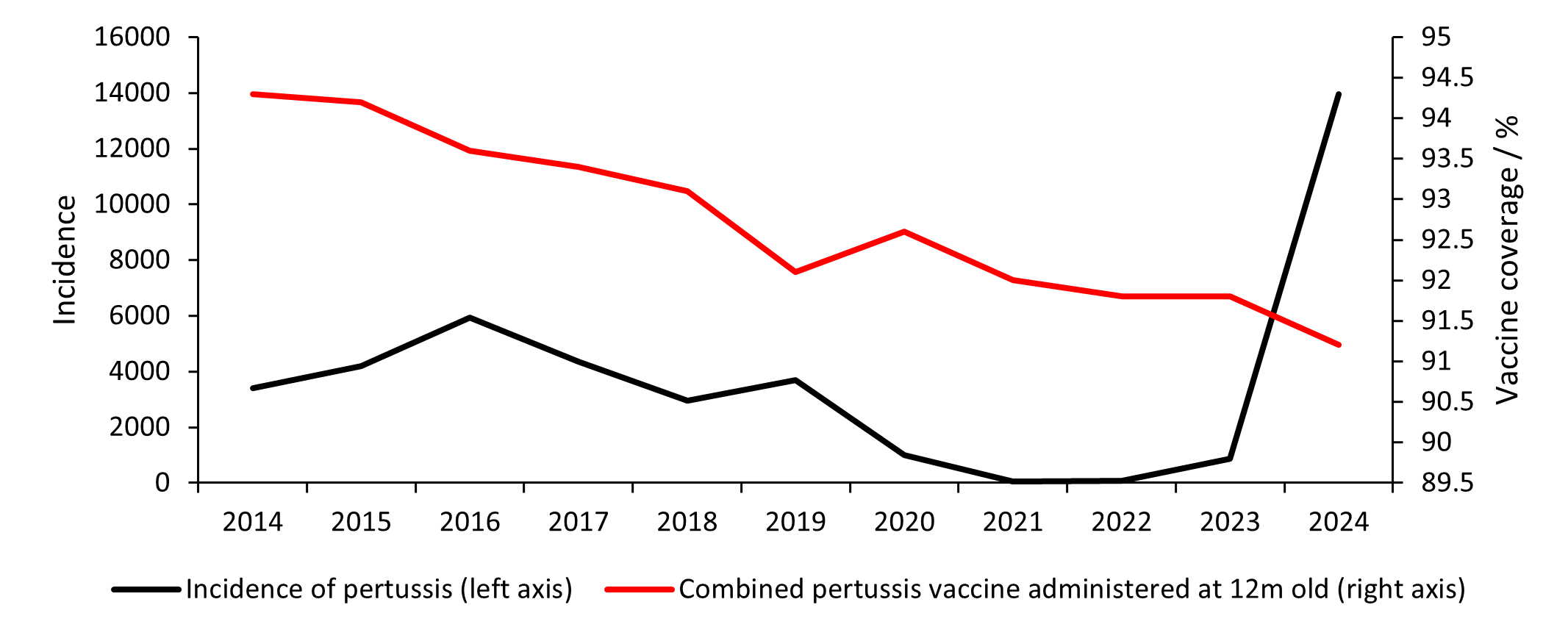

Vaccines are among the most impactful medical inventions in history.[i] Globally, vaccines exist to prevent more than 20 life-threatening diseases.[ii] New estimates suggest that global immunisation efforts over the past 50 years have prevented 154 million deaths from diseases like diphtheria, tetanus, pertussis, yellow fever, and measles.[iii] Despite worldwide immunisation success, the COVID-19 outbreak and resulting vaccination race brought into focus the global prevalence of vaccine hesitancy and appeared to trigger a further decline of trust in vaccinations.[iv] A US survey found that the proportion of surveyed adults who do not think approved vaccines are safe rose by 6% to 16% between 2021 and 2023.[v] Similarly, a survey in Germany shows that public vaccine scepticism increased from 21% in 2022 to 25% in 2024.[vi] As a result of decreasing vaccine uptake and concerns over the prevalence of preventable diseases, the World Health Organisation has declared vaccine hesitancy as one of the top global health challenges.[vii] Whooping cough (pertussis) in England shows the concerning effect of increasing vaccine scepticism, declining vaccination rates, and consequent rising incidence of the disease. Although historically associated with lower-income countries where there is greater mistrust of vaccines, Figure 1 demonstrates how growing scepticism can have a marked impact on disease prevalence in higher-income countries too[viii]. In 10 years, the infant pertussis vaccine coverage in England fell from 94% to 91%, meanwhile the maternal pertussis vaccine coverage fell from 75% to 59% from 2017 to 2024[ix]. Incidence of the disease has more than tripled over the same time-period.

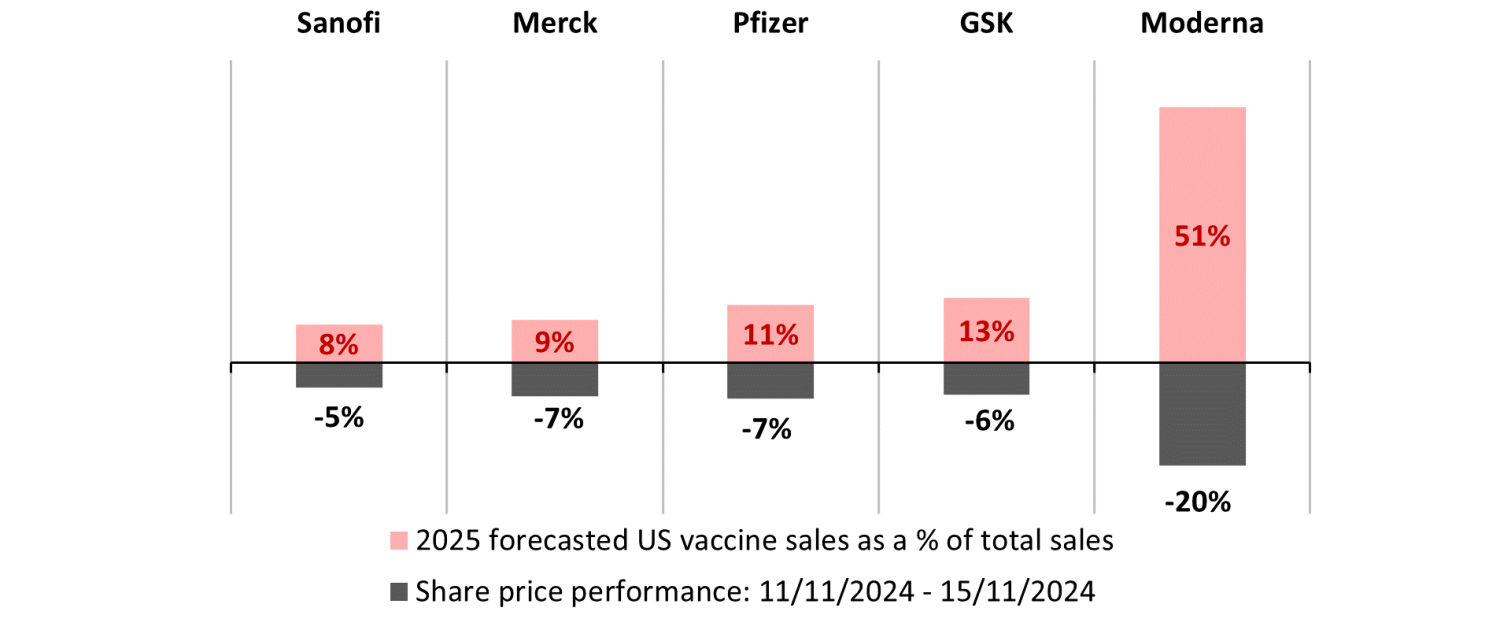

A similar trend can be detected with measles, where misguided concerns over a link with autism in children have led to declining vaccination rates[x]. 2023 saw a 20% rise in global cases compared to 2022[xi], while nearly 60 countries experienced outbreaks in the past year. Globally, only 83% of children received a first dose of the measles vaccine in 2023 and only 74% received the recommended second dose, despite national coverage of 95% or greater being necessary to prevent outbreaks of the contagious disease.[xii] During the COVID-19 pandemic it was found that antivaccine messages from authority figures were a common reason for vaccine hesitancy.[xiii] Now that President-elect Donald Trump has nominated Robert F Kennedy Jnr. (RFK Jnr.) - who has been skeptical of vaccines in the past - to head up the Health and Human Services Department, there are increasing concerns of an even greater erosion of people's willingness to get vaccinated in the US.[xiv] How does this impact investors? RFK Jnr.'s nomination as Head of Health and Human Services (HHS) precipitated a sharp sell-off in healthcare stocks. Sanofi, Merck, Pfizer, GSK, and Moderna have greater exposures to the US vaccine market and hence were punished most by the market in the week of his nomination.

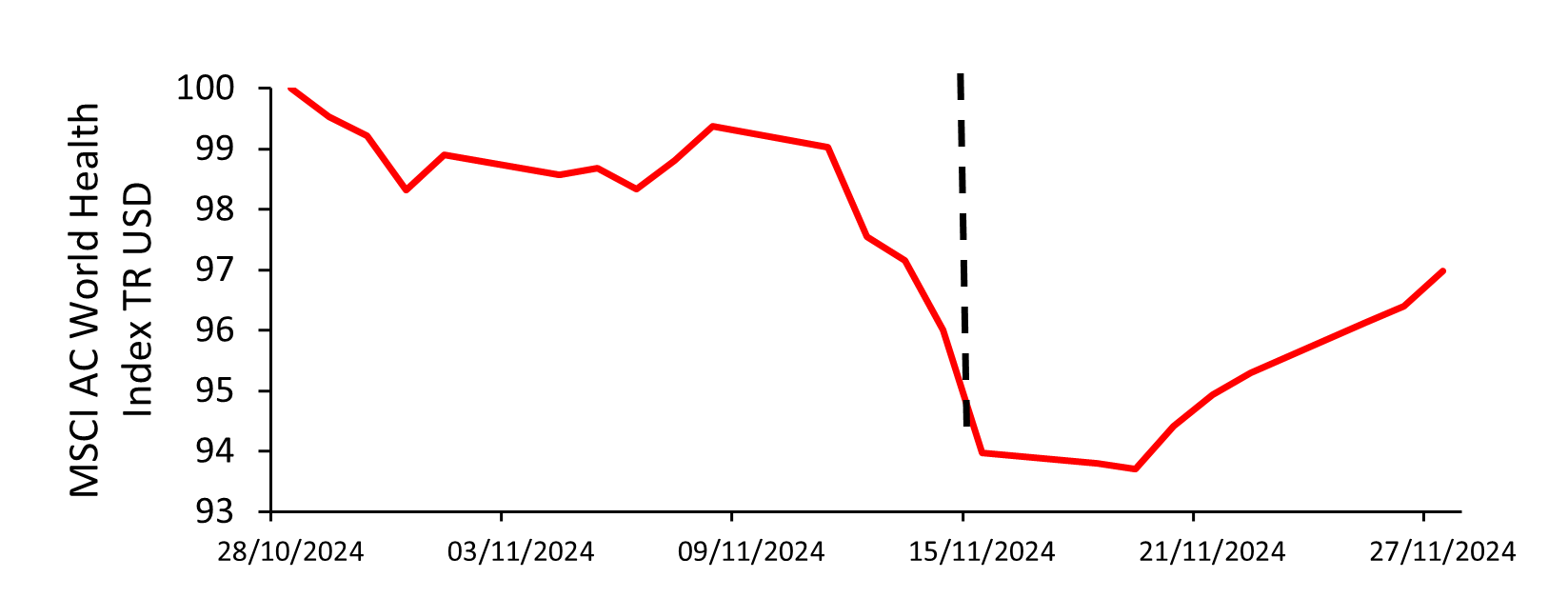

Although there is very little clarity over the shape of future US health policy, there is a presumption in the investment community that RFK Jnr.'s vaccine stance may lead to larger and longer clinical trials, stricter labels for approved products, lower vaccination rates, and therefore lower revenues for vaccine makers. Further, with Republican control of both chambers of Congress and the White House, a hawkish health department could seek to repeal the National Childhood Vaccine Injury Act of 1986 which protects vaccine makers from litigation due to injury. An increase in lawsuits - even if not successful - may increase costs for manufacturers. Ultimately, if significant legislative changes were to occur then investing in vaccine makers could be riskier. However, whilst commentators have focussed largely on RFK Jnr.'s more harmful rhetoric, not all news has been entirely negative. RFK Jnr. has stated that vaccines were 'not going to be taken away from anybody'[xv], while Vivek Ramaswamy - who will co-lead the newly created Department of Government Efficiency (DOGE) - confirmed that the new US healthcare leadership 'understand innovation is a key part of the solution.'[xvi] And it is interesting to note that Ramaswamy has made comments suggesting that he wants DOGE to reduce regulatory burden on pharma, biotech and medical device companies that require US Food and Drug Administration (FDA) approval. He recently posted on X, "My #1 issue with FDA is that it erects unnecessary barriers to innovation", so it could be argued that the FDA under the Trump administration may be supportive of getting treatments to patients more quickly, which would most likely be a net positive for manufacturers. Further, it is our view that despite potential disruption in US healthcare, many treatments will continue to have a life-changing impact on patients' lives, and hence, best-in-class businesses will keep their competitive advantage. In the week of RFK Jnr.'s nomination, the MSCI AC World Health Index declined by more than 5%[xvii], which included companies with no exposure to vaccines. With that discount, we believe there are significant opportunities for us to invest in these life-changing solutions at compelling valuations.

|

|

Funds operated by this manager: Redwheel China Equity Fund, Redwheel Global Emerging Markets Fund |

|

Sources: [i] UN, 2024 [ii] WHO, 2024 [iii] WHO, 2024 [iv] Larson et al., 2022 [v] Annenberg Public Policy Center, 2023 [vi] Statista, 2024 [vii] WHO, 2019 [viii] RACGP, 2024 [ix] GOV UK, 2024 [x] Hviid et al., 2019 [xi] Reuters, 2024 [xii] CDC, 2024 [xiii] Griffith et al., 2021 [xv] NPR interview, 06/11/2024. [xvi] Vivek Ramaswamy's push for FDA changes could boost his wealth - The Washington Post, accessed 27/11/2024. [xvii] Bloomberg, November 2024 Key Information |

22 Jan 2025 - Long-term Investing

|

Long-term Investing Airlie Funds Management December 2024 |

|

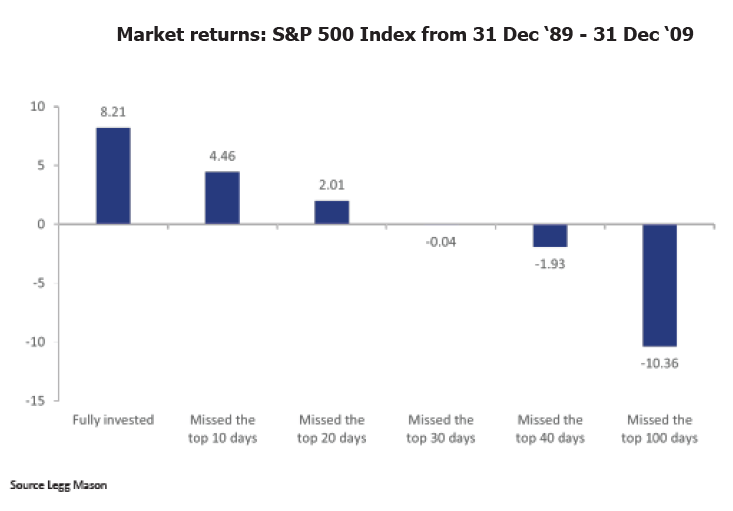

Investing in Australian listed companies with a long-term outlook entails retaining investments for a minimum of five years or longer. While the exact time frame for long-term investing can differ, the core principle is dedication, regardless of market turbulence and fluctuations in asset prices. We delve into key strategies tailored for those investors keen on harnessing the potential of Australian listed companies for long-term wealth accumulation. Objectives, risk tolerance and investment horizonLong-term investing begins with a clear understanding of your financial objectives, risk appetite, and investment time frame. Whether your aim is to secure your retirement, finance education expenses or a dream property, clearly defining your goals is essential. Assessing your risk tolerance, which means finding out if your risk level is conservative, moderate or aggressive, helps you understand the level of risk you're willing to accept in pursuit of your investment objectives. Generally, investors with longer horizons can afford to embrace higher risks compared to those nearing retirement. It's important to consider your investment time horizon, as this is when you'll need access to money to achieve your financial objectives. Some of the factors that influence your time horizon include your financial goals, income, age and risk tolerance. Tailoring your investment strategy to align with your unique circumstances is foundational for long-term success in the Australian market. Diversify your portfolioThe Australian investment landscape, like any other, is prone to unpredictability and market fluctuations. Spreading your investments across different industry sectors can potentially help to mitigate risk. Diversification may help reduce the potential negative impact of any single asset's downturn on your overall portfolio. This approach helps in balancing out the performance, as when one asset or sector underperforms, another may outperform, stabilising the portfolio's returns. It's important to align diversification with your individual risk tolerance and investment goals, ensuring a well-rounded and resilient investment strategy. Stay committedEmotions often run high during market downturns, tempting investors to deviate from their chosen investment strategies. However, succumbing to fear-driven decisions can jeopardise long-term returns. Resist the urge to time the market, as consistently predicting market movements is exceedingly challenging. Long-term investing requires discipline and resilience, where investors are encouraged to adhere to their investment strategies even amidst turbulent market conditions. Avoid falling into the trap of chasing short-term profits, as maintaining investment during market cycles can be essential for realising the full potential of the market. It's easy to feel drawn to timing the markets, aiming to choose tomorrow's winners from yesterday's winners. However, evidence suggests that market timing is a tough game. Take the buy low, sell high approach, for instance; it hinges on predicting when a stock will rise or fall, a task fraught with complexity. Successful long-term investing, on the other hand, demands a commitment to staying invested, resisting the urge to constantly chase the next big thing. The chart below illustrates the risks of trying to time the market.

Leverage expertise and regular reviewAchieving success in investing requires a thorough understanding of market dynamics and investment strategies. Consider investing in managed funds where investment experts are actively researching and managing a portfolio, aiming for optimal diversification with continued dedicated oversight. Review your investment strategy regularly to ensure it remains aligned with your long-term objectives. Rebalancing your portfolio and adjusting the weightings of your portfolio helps to ensure alignment with your intended long-term goals. Over time, some investments may perform better than others, causing your portfolio to shift from its original strategy. Rebalancing brings your portfolio back to its original plan, ensuring it continues to reflect your investment goals and risk tolerance. Long-term investing in Australian-listed companies entails a strategic approach tailored to your unique financial goals and risk tolerance. By embracing diversification, maintaining discipline, and leveraging expert guidance, investors may have greater confidence in navigating the dynamic Australian market landscape. Funds operated by this manager: Airlie Australian Share Fund, Airlie Small Companies Fund Important Information: This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 trading as Airlie Funds Management ('Airlie') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision about whether to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to an Airlie financial product or service may be obtained by calling +61 2 9235 4760 or by visiting www.airliefundsmanagement.com.au. Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of an Airlie financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. Airlie makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Airlie. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. No representation or warranty is made with respect to the accuracy or completeness of any of the information contained in this material. Airlie will not be responsible or liable for any losses arising from your use or reliance upon any part of the information contained in this material. Any third party trademarks contained herein are the property of their respective owners and Airlie claims no ownership in, nor any affiliation with, such trademarks. Any third party trademarks that appear in this material are used for information purposes and only to identify the company names or brands of their respective owners. No affiliation, sponsorship or endorsement should be inferred from the use of these trademarks. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Airlie. |

21 Jan 2025 - Glenmore Asset Management - Market Commentary

|

Market Commentary - December Glenmore Asset Management January 2025 Globally, equity markets were broadly weaker in December. In the US, the S&P 500 declined -2.5%, the Nasdaq rose +0.5%, whilst in the UK, the FTSE fell -1.4%. December saw the US Federal Reserve cut interest rates (as expected), however guidance from the Fed regarding further rate cuts in 2025 was tempered, due to stubbornly high inflation and a strong US employment market. There is also potential for US president Donald Trump's "pro growth" policies to result in higher inflation over the next 12-24 months, which may have been a factor in the monetary policy guidance. Domestically, in line with its offshore peers, the ASX All Ordinaries Accumulation index declined, falling -3.1%. On the ASX, the top performing sectors were staples and utilities, with real estate being the main underperformer (impacted by higher bond yields). Resources also lagged due to weak sentiment towards the outlook for the Chinese economy. Bond markets saw yields increase in December as forward guidance for the number of interest rate cuts from the US based Federal Reserve was reduced. The US 10 year government bond yield climbed +30 basis points (bp) to close at 4.52%, whilst its Australian counterpart was flat +2bp to end the month at 4.37%. Funds operated by this manager: |

20 Jan 2025 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

||||||||||||||||||||||

| HOPE Housing Investment Trust | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

| HOPE Housing Residential Property Trust | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Fairlight Global Small & Mid Cap (SMID) Fund - Hedged | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Labassa Capital Australian Real Estate Debt Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Capstone Income Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

Want to see more funds? |

||||||||||||||||||||||

|

Subscribe for full access to these funds and over 900 others |

17 Jan 2025 - The Australian: Economic uncertainty driven by a Trump guessing game

|

The Australian: Economic uncertainty driven by a Trump guessing game JCB Jamieson Coote Bonds November 2024 The year 2025 is shaping up to be one of great uncertainty, with global politics driven by the incoming Trump administration likely leading significant market gyrations and increased asset class volatility. Trump US exceptionalism is expected, but the actual policies used to generate "make America great again" are still the source of debate only a week from the presidential inauguration. Many permutations and combinations for policy are possible and the medium-term impacts may be quite different to the "shoot first and ask questions later" moves of modern markets as we are seeing with US equities back towards election day valuations. Expectations for continued earnings and growth are high after two exceptional years for risk assets, while longer-dated US fixed income yields have increased despite the US Federal Reserve and many other global central banks cutting interest rates in 2024. This is historic in and of itself (usually rates fall as funding rates are lowered), driven by concerns about US fiscal spending and inflation impacts that continue an unsustainable pathway. Will the change in the US government generate any fiscal prudence? Will the Department of Government Efficiency succeed in curbing excessive fiscal spending to reduce inflation fuelled by excessive government spending? And what could be the growth implications of this withdrawal of government support from the economy? These remain key questions for bond yields which, if they rise, could dampen the outlook for all asset markets by increasing the global cost of funding. Australia finds itself heavily influenced by these global trends yet uniquely positioned between contrasting economic realities. In the US, bond yields are increasing, with 10-year Treasury yields rising 66 basis points in 2024 to 4.57 per cent, reflecting expectations of pro-business policies, tax cuts and a market-friendly administration. Meanwhile, in China, 10-year bond yields fell 89 basis points across the same period to just 1.67 per cent as the economy continues to struggle with low growth and disinflation. This divergence has continued in the opening days of 2025, further highlighting the US exceptionalism of the times. Away from US markets, global growth looks tepid - no longer will a raising US tide lift all boats, meaning investors will need to place their bets selectively as asset performance across geographies will likely diverge significantly in similar asset markets. In 2025, the volume of corporate debt requiring refinancing is set to increase significantly. After locking in low rates during the Covid period, a significant proportion of loans and bonds now face repayment or rollover. This dynamic has the potential to add some spice to markets this year, as there will be some bad refinancing stories in the credit space after such a dramatic shift in the interest rate environment since the pandemic. Private credit issues already are emerging in Australia, with a number of high-profile private credit investment managers citing issues around the sector. However, the inherent lack of transparency within private credit means these challenges often remain hidden until the damage is done. In some cases, junior or subordinated lenders in local deals have already faced complete losses. As interest rates continue to exert pressure and delinquencies rise, we anticipate more such stories to surface, reflecting the sustained impact of a restrictive rate environment. Private credit is a highly attractive asset class but its rapid growth has attracted many new participants who promote high returns with minimal perceived risk (and low market volatility because of infrequent asset revaluation). This can be misleading, as high returns typically involve substantial risks that may not be immediately apparent. Investors require significant skill to identify who they are lending to, where they sit in the capital stack, who might run the workouts on distressed assets if required and how long this process may take. These products typically require long lockups of capital, which increasingly will need to ride through heightened uncertainty. Returns must be exceptionally high to compensate for these factors. The question is whether these challenges will escalate into a systemic tipping point, triggering broader market repercussions, or whether they will remain isolated incidents, wiping out the few unfortunate folks who didn't do their homework or ran the risk regardless. The answer will likely depend on the scale and interconnectedness of the issues as they unfold. The year looks set to be full of surprises. We expect the Reserve Bank will cut interest rates early in 2025, as inflation continues to moderate with a significant lag to the rest of the world, and we expect other jurisdictions will continue cutting rates as economies slow. Calibrating all of that with such significant policy uncertainty is difficult; investors will need to ride the developments and adjust accordingly. As always, we think portfolio diversification is prudent into such uncertainty, as bold bets will likely be as lucky as they are smart. Charlie Jamieson, Chief Investment Officer Funds operated by this manager: CC Jamieson Coote Bonds Active Bond Fund (Class A), CC Jamieson Coote Bonds Dynamic Alpha Fund, CC Jamieson Coote Bonds Global Bond Fund (Class A - Hedged) |

16 Jan 2025 - 2024 In Review & 2025 Outlook

|

2024 In Review & 2025 Outlook Alphinity Investment Management January 2025 |

|

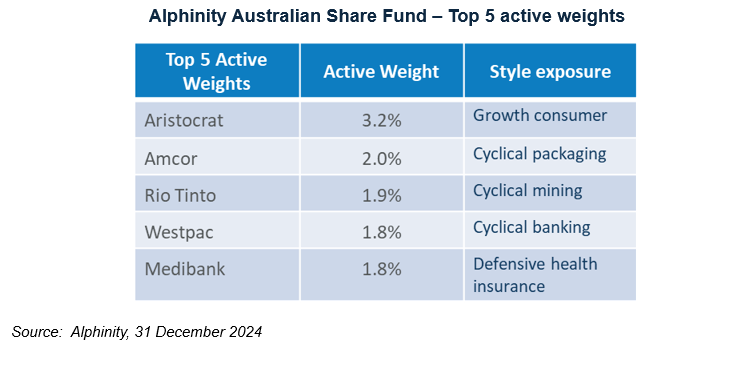

If 2024 was the year of Elections, Economics, Evolutions and Earnings, what is in store for Australian equities in 2025? The year 2024 proved to be a remarkable one, both in absolute terms and relative to expectations. As the year unfolded, it brought numerous surprises and developments that shaped the global economic and political landscape. From election outcomes (and associated geopolitics), diverging economic growth (and interest rate changes), to the AI evolution (and associated ripple effects) and finally the return of earnings revisions as a key relative individual stock performance driver. Elections, economics, evolutions and earnings - a fitting summary of some of the primary forces behind the global equity rally as 2024 draws to a close. Below we explore these themes in more detail, share our outlook for 2025 and how the Alphinity Australian Funds are positioned going into the New Year. 2024 in review: As we entered 2024 a year ago, there were widespread expectations of significant rate cuts in the United States. However, as the year progressed, only a handful materialised, accompanied by a soft landing for the economy. In Australia, the Reserve Bank maintained a resolute stance against rate cuts, though some cracks in this position began to appear towards the year's end. The U.S. presidential election was a focal point of 2024, filled with twists and turns. The outcome, with Donald Trump's victory, is likely to usher in policies and a political and regulatory environment perceived as pro-business and pro-market. Meanwhile, China's attempts at economic stimulus, while showing some much-needed strong intent, fell short of expectations in the detail, failing to provide the anticipated boost to global growth just yet. In the financial markets, the U.S. stock indices continued their upward trajectory, propelled by the "Magnificent Seven" tech giants and artificial intelligence advancements. This momentum had a positive spillover effect on the Australian market, with the technology sector the highest contributor to returns despite the pullback in December (+49% YTD). Outside of the tech sector, the strong performance in the US had a broader positive impact in the Australian market through the year, despite quite different economic and earnings outcomes. For Australian investors, the strength of major banks, particularly Commonwealth Bank and Westpac, was also noteworthy, driven by small but persistent earnings upgrades. With earnings upgrades few and far between elsewhere (the market in total having net downgrades), financials continued to be well supported, almost regardless of valuations. From a portfolio and process perspective, it was encouraging to see the re-emergence of earnings revisions as a key individual stock driver and alpha generator over the last 12 months, something that went temporarily missing for much of 2022 and 2023 as large top down thematics and swings took precedence. This trend allowed for consistent momentum to be a key driver, which assisted all the Alphinity funds to capture positive alpha for our clients this year. The outlook for 2025: Looking ahead to 2025, the outlook appears more nuanced. A repeat of the robust absolute returns seen in 2024 seems less likely, given the high valuations and elevated expectations that now form a more challenging starting point. Unlike 12 months ago, everyone appears positioned for a "no-landing" or at worst a "soft-landing" already, with very little wall-of-worry to climb. However, a precipitous decline is not anticipated either. Several positive factors remain that could continue to drive the market forward. The U.S. economy continues to show resilience, and the new Trump administration is expected to implement pro-business, growth-oriented policies and a market friendly environment, at least initially. There's potential for more rate cuts in international markets (even though less than hoped for initially) including, but perhaps toto a lesser extent, in Australia. China, while still facing challenges, has demonstrated strong intent and retains some levers to stabilise its economy, potentially becoming less of a drag on global growth and sentiment. We have our own election here in Australia that is likely to lead to more fiscal stimulus promises from the major parties, and a focus on 'cost-of-living' pressures. Nevertheless, earnings expectations in the U.S. are already quite high, (less so here in Australia), making further PE expansion as the main market driver less likely unless we have a material change in interest rate view. The focus will need to shift to actual earnings outcomes. Uncertainties surrounding U.S. trade policies, inflation trajectories, interest rate movements, and geopolitical tensions add complexity to the outlook. While material growth in market indices may be harder to achieve in 2025, there is enough positive momentum to sustain current levels for some time. A period of market consolidation wouldn't be surprising however after the strong run in 2024, though a more significant correction would likely require catalysts beyond just high valuations (such as an economic, earnings or interest rate policy surprise). It is likely that rather than the level of the market, the key question for 2025 will revolve around potential sector and stock rotation. Will the current market leaders maintain their dominance, or will we see new market leadership emerge? For example, changes in monetary policy, such as rate cuts in Australia, could benefit domestic and consumer cyclical stocks. A recovery in China or more forceful policy might boost commodities, as would improved US and global economic growth. In a flatter or weaker market environment, defensive stocks might get their time in the sun yet again. Ultimately, whatever the market environment it is likely to be earnings driven. Market leadership will be driven by those companies that can produce better earnings outcomes than expected, which is what we saw eventuate in 2024. The key will be the flexibility to move to where earnings leadership is as the year unfolds. How are we positioned? Given these considerations, a relatively balanced portfolio approach seems prudent to start 2025, focusing on likely earnings outcomes in individual stocks rather than trying to second guess broader macro drivers. Some increased defensive positioning is likely advisable due to high market valuations, but maintaining some exposure to domestic interest rate-sensitive sectors could be beneficial for example if rates decrease. Our portfolios continue to be positioned in stocks with better earnings outlooks than the market expects, as per our investment process. While we do focus on earnings momentum and the quality of those earnings primarily, we also care about valuation. Valuation rarely tells you when a stock or market is going to turn, but it does tell you when risk is increasing. As such, without a better earnings outlook for the market overall, risks in the market have by definition increased alongside those higher valuations. So, the portfolio needs to be very vigilant around investing in stocks that are showing earnings leadership and delivering earnings upgrades. As the year unfolds and new earnings trends become clearer, we will continue to adjust our portfolios to align with new earnings leaders. |

|

Funds operated by this manager: Alphinity Australian Share Fund, Alphinity Concentrated Australian Share Fund, Alphinity Global Equity Fund, Alphinity Global Sustainable Equity Fund, Alphinity Sustainable Share Fund |

15 Jan 2025 - 10k Words | January 2025

|

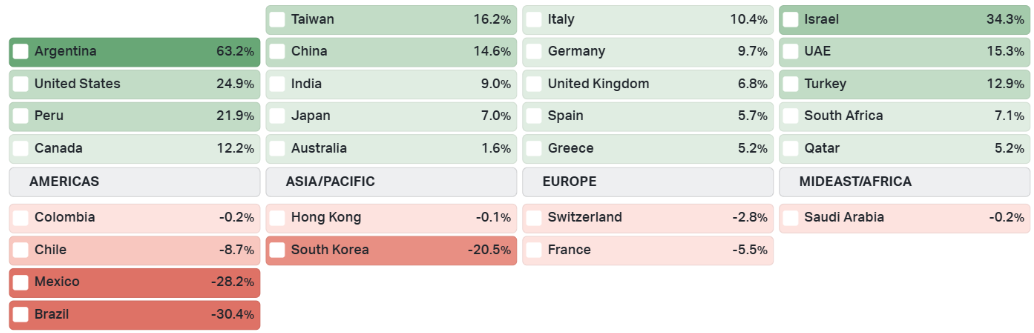

10k Words Equitable Investors January 2025 Only Argentina's sharemarket outpaced the US in CY2024, with a mediocre performance from Australia; 10-year bond yields expanded despite the Federal Reserve's rate cuts; the AUD battled while the USD went from strength-to-strength; while natural gas was the commodity of choice. We can't help but highlight the concentration in the US market once again; while its pricing is dependent on a resurgence in earnings outside the tech sector. The thing about high multiples for the S&P 500 is that they tend to be followed by low 10-year returns. Maybe that is why money flowed out of active equities funds in CY2024. We take a look at the implications of volatility on small cap returns and the severity of drawdowns that have been seen across asset classes through the decades. Then we see just how big a part of the global investment pie equities have become. Finally, we look at the increased role government borrowing has played in the US and government spending has played in Australia. Global equity ETF total returns for 2024 (in USD)

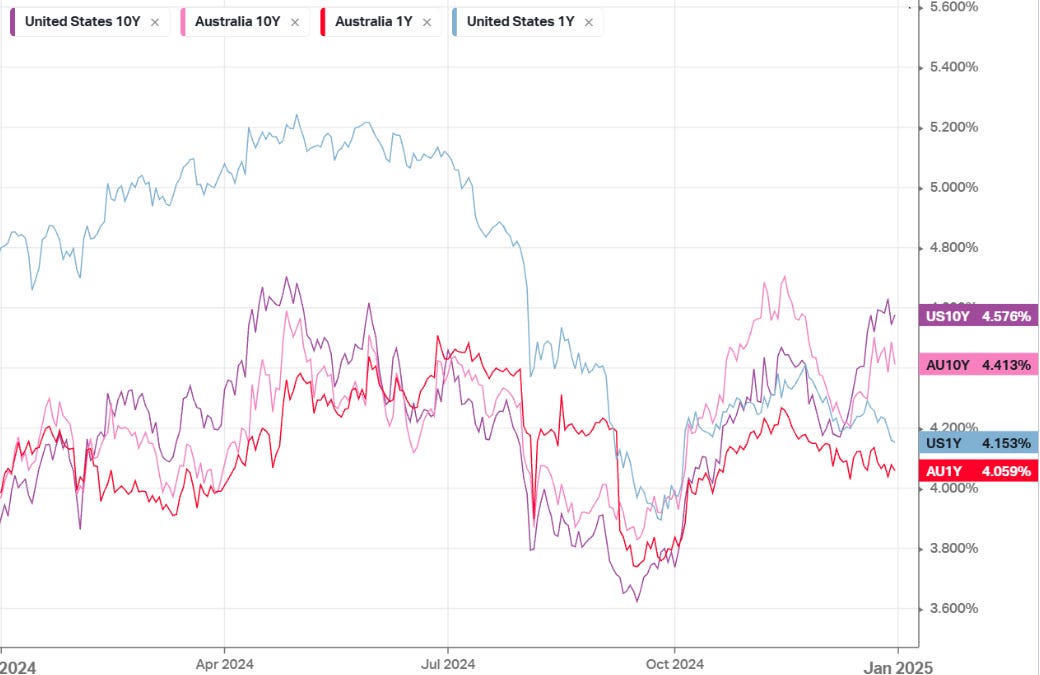

Source: Koyfin, Equitable Investors Government bond yield movements in CY2024

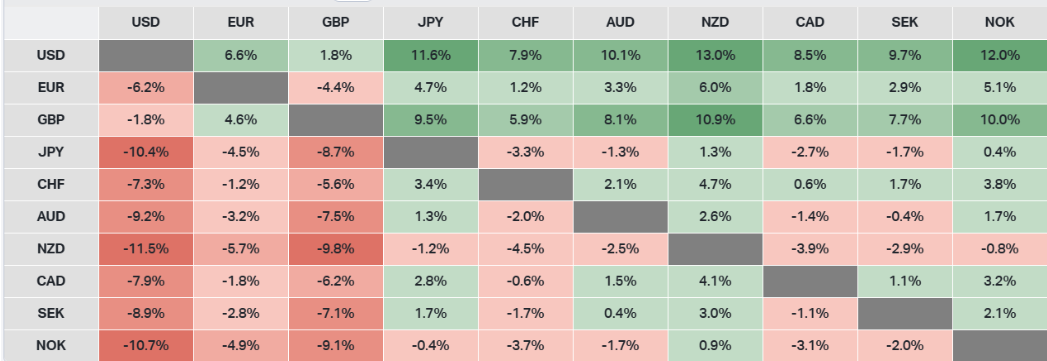

Source: Koyfin, Equitable Investors Currency performance in CY2024

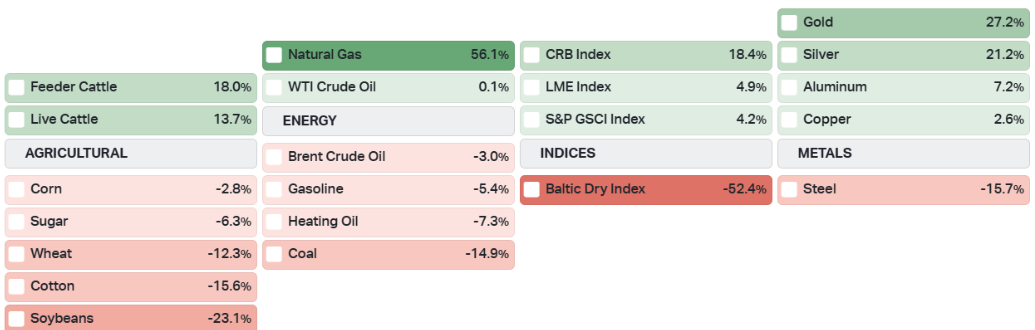

Source: Koyfin, Equitable Investors Commodities performance in CY2024

Source: Koyfin, Equitable Investors Share of total S&P 500 market cap held by 5 largest stocks

Source: Bianco Research Year-on-year S&P 500 earnings growth - historical and projected

Source: Callie Cox Media, Bloomberg S&P 500 forward P/E and subsequent 10-year returns

Source: @thejoshviljoen Active equities fund outflows in 2024

Source: Financial Times Percentage of trading days with moves of 1% or more in the Russell 2000 over the last 25 years

Source: Royce & Associates Drawdowns - the latest prices in relation to the previous all-time high

Source: Topdown Charts Composition of the global market portfolio

Source: State Street Global Advisors Evolution of the composition of the global market portfolio

Source: State Street Global Advisors US debt growth breakdown

Source: @TheKingCourt Data demand growth driving a surge in data centre power use

Source: @AvidCommentator January 2025 Edition Funds operated by this manager: Equitable Investors Dragonfly Fund Disclaimer Past performance is not a reliable indicator of future performance. Fund returns are quoted net of all fees, expenses and accrued performance fees. Delivery of this report to a recipient should not be relied on as a representation that there has been no change since the preparation date in the affairs or financial condition of the Fund or the Trustee; or that the information contained in this report remains accurate or complete at any time after the preparation date. Equitable Investors Pty Ltd (EI) does not guarantee or make any representation or warranty as to the accuracy or completeness of the information in this report. To the extent permitted by law, EI disclaims all liability that may otherwise arise due to any information in this report being inaccurate or information being omitted. This report does not take into account the particular investment objectives, financial situation and needs of potential investors. Before making a decision to invest in the Fund the recipient should obtain professional advice. This report does not purport to contain all the information that the recipient may require to evaluate a possible investment in the Fund. The recipient should conduct their own independent analysis of the Fund and refer to the current Information Memorandum, which is available from EI. |

14 Jan 2025 - The door for rate cuts opens further

|

The door for rate cuts opens further Pendal December 2024 |

|

THE Australian economy grew by only 0.3% in the September quarter, once again falling behind population growth. We managed only 0.8% growth for the year, yet the RBA still thinks demand outstrips supply. The September quarter GDP numbers were always going to be more interesting than most. Tax cuts and government subsidies were hitting consumer pockets and the big question was whether they would be spent or saved. For now, it appears consumers have been happy to pocket the extra money. Spending by business and consumers once again flatlined and per capita consumption fell by 2% over the year. The only growth we could find was, once again, the government - which now comprises almost 28% of GDP, up from around 23% for most of the past 50 years. The graph below, courtesy of Westpac, highlights this extraordinary return of big government.  Source: Westpac Economics Source: Westpac Economics

Source: Wages grow 3.5 per cent for the year | Australian Bureau of Statistics The national accounts also provided more information around wage pressures. As the high wage outcomes of 2022 and 2023 have faded from view, these are easing quickly. Average earnings per hour moderated to 3.2%yr, from 6.5%yr in the June quarter. This is consistent with recent wage data at 3.5%. We have weak growth, moderating inflation, wages under control and global easing cycles - so why the hesitation from the RBA? The central bank remains focused on the idea that the labour market remains too tight, as it believes that 4.5% - not the current 4.1% - to be full employment. The data is now suggesting otherwise. OutlookIt will be an interesting few upcoming meetings for the RBA board. February will likely be the last monetary policy board decision for three of the six independent directors. And March or April will see a split into governance and monetary policy boards. Whether this influences thinking remains to be seen, but the current spirit of caution may yet stop a rate cut in February. However, I think the RBA may do a short sharp pivot in the next few months, and view two cuts (in February and May) as still on the cards. The Q4 inflation data at the end of February will be another low number, with even underlying inflation likely to print 0.6%, or annualised at the RBA midpoint. While bond investors will be cheering for a cut, the Labour government will be desperate for one ahead of the "cost-of-living" election. Time will tell if the RBA delivers for them. Author: Tim Hext |

|

Funds operated by this manager: Pendal Global Select Fund - Class R, Pendal Horizon Sustainable Australian Share Fund, Pendal MicroCap Opportunities Fund, Pendal Multi-Asset Target Return Fund, Pendal Sustainable Australian Fixed Interest Fund - Class R, Pendal Sustainable Australian Share Fund, Regnan Credit Impact Trust Fund, Regnan Global Equity Impact Solutions Fund - Class R |

|

This information has been prepared by Pendal Fund Services Limited (PFSL) ABN 13 161 249 332, AFSL No 431426 and is current as at December 8, 2021. PFSL is the responsible entity and issuer of units in the Pendal Multi-Asset Target Return Fund (Fund) ARSN: 623 987 968. A product disclosure statement (PDS) is available for the Fund and can be obtained by calling 1300 346 821 or visiting www.pendalgroup.com. The Target Market Determination (TMD) for the Fund is available at www.pendalgroup.com/ddo. You should obtain and consider the PDS and the TMD before deciding whether to acquire, continue to hold or dispose of units in the Fund. An investment in the Fund or any of the funds referred to in this web page is subject to investment risk, including possible delays in repayment of withdrawal proceeds and loss of income and principal invested. This information is for general purposes only, should not be considered as a comprehensive statement on any matter and should not be relied upon as such. It has been prepared without taking into account any recipient's personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation. The information may contain material provided by third parties, is given in good faith and has been derived from sources believed to be accurate as at its issue date. While such material is published with necessary permission, and while all reasonable care has been taken to ensure that the information is complete and correct, to the maximum extent permitted by law neither PFSL nor any company in the Pendal group accepts any responsibility or liability for the accuracy or completeness of this information. Performance figures are calculated in accordance with the Financial Services Council (FSC) standards. Performance data (post-fee) assumes reinvestment of distributions and is calculated using exit prices, net of management costs. Performance data (pre-fee) is calculated by adding back management costs to the post-fee performance. Past performance is not a reliable indicator of future performance. Any projections are predictive only and should not be relied upon when making an investment decision or recommendation. Whilst we have used every effort to ensure that the assumptions on which the projections are based are reasonable, the projections may be based on incorrect assumptions or may not take into account known or unknown risks and uncertainties. The actual results may differ materially from these projections. For more information, please call Customer Relations on 1300 346 821 8am to 6pm (Sydney time) or visit our website www.pendalgroup.com |

13 Jan 2025 - Understanding Bridging Loans: A Comprehensive Guide

|

Understanding Bridging Loans: A Comprehensive Guide Australian Secure Capital Fund December 2024 In the world of finance, the term "bridging loan" often comes up in conversations about short-term funding solutions. Bridging finance may seem complex, but understanding its key features can help clarify its benefits and risks. In this article, we'll explore what a bridging loan is, how it works, its advantages and disadvantages, and when it might be the right choice for you.

What is a Bridging Loan?A bridging loan is a type of short-term financing that is designed to "bridge" the gap between a financial need and a long-term financing solution. These loans are typically used when an individual or business needs to access funds quickly, often for a specific purpose, such as purchasing a new property before selling an existing one. Bridging loans are usually secured against an asset, often real estate, and can be arranged relatively quickly compared to traditional loans. Types of Bridging LoansThere are two main types of bridging loans: 1. Open Bridging Loans: These loans do not have a fixed repayment date, meaning they can be paid back at any time. They are usually used in situations where the borrower has not yet sold their existing property or is unsure when they will be able to repay the loan. 2. Closed Bridging Loans: These loans have a specific repayment date, typically aligned with the sale of a property. They are ideal for borrowers who have already exchanged contracts on a property and have a clear timeline for repayment. How Does Bridging Finance Work?Bridging finance operates on a straightforward premise: it provides quick access to funds that can be used for various purposes. The process generally involves the following steps: 1. Application: The borrower submits an application for a bridging loan, providing necessary documentation such as proof of income, details of the property being used as security, and information about the intended use of the funds. 2. Valuation: The lender will conduct a valuation of the property to ensure it is worth the amount being borrowed. This step is crucial, as the property serves as collateral for the loan. 3. Approval and Funding: If the application is approved, the lender will issue the funds, usually within a matter of days. This quick turnaround is one of the main advantages of bridging finance. 4. Repayment: The borrower will repay the loan either upon the completion of the intended project (e.g., selling a property) or on the agreed-upon repayment date for closed loans.

Advantages of Bridging LoansBridging loans come with several benefits that make them an attractive option for many borrowers: 1. Speed: One of the most significant advantages of bridging loans is their speed. Traditional loans can take weeks or even months to process, while bridging finance can be arranged in a matter of days. 2. Flexibility: Bridging loans offer flexibility in terms of repayment options. They can be tailored to fit the borrower's specific needs, whether it's a short-term loan for a few weeks or a few months. 3. Access to Funds: Bridging finance can provide access to funds that might not be available through traditional lending routes, especially for borrowers with less-than-perfect credit histories. 4. No Early Repayment Penalties: Many bridging loan providers do not impose penalties for early repayment (depending on the terms), which can be a crucial factor for borrowers looking to reduce their overall interest costs. Disadvantages of Bridging LoansWhile bridging loans offer many benefits, they also come with some drawbacks that should not be overlooked: 1. Higher Interest Rates: Bridging loans typically have higher interest rates compared to traditional mortgages. This is due to their short-term nature and perceived risk associated with bridging loans. Borrowers should compare options to find a product that fits their circumstances. 2. Fees: Borrowers may encounter various fees associated with bridging loans, including arrangement fees, valuation fees, and legal fees, which can add to the overall cost. 3. Risk of Repossession: Since bridging loans are secured against an asset, failure to repay can result in the lender repossessing the property used as collateral. 4. Short-Term Solution: Bridging loans are not meant to be a long-term financing solution. Borrowers need to have a clear plan for repayment, as these loans usually need to be settled within a few months. When to Consider a Bridging LoanBridging loans may be a suitable financial tool in specific situations, depending on your circumstances and the terms provided by the lender. Here are a few scenarios where bridging finance might make sense: 1. Property Transactions: If you are in the process of buying a new home but have not yet sold your current property, a bridging loan can provide the funds needed to make the purchase without the stress of timing the two transactions perfectly. 2. Investment Opportunities: Investors might use bridging loans to seize opportunities that require quick financing, such as auction purchases or real estate investments that need renovation before resale. 3. Business Funding: Businesses may need immediate capital for various reasons, such as purchasing new equipment or covering operational costs during a slow period. Bridging finance can provide that necessary cash flow. Bridging loans may offer a short-term financial solution for those who meet the lender's criteria and have a clear repayment strategy. While they come with higher interest rates and various fees, their speed and flexibility make them an attractive option for many borrowers. Whether you're looking to purchase a new home, invest in real estate, or fund a business need, understanding bridging finance can help you make informed decisions about your financial future. As with any financial product, it's essential to weigh the pros and cons carefully and consult with a financial advisor if needed. Bridging loans can be an excellent tool in your financial arsenal -- just ensure you know how to use them wisely. Author: Mikaela Gladden Funds operated by this manager: ASCF High Yield Fund, ASCF Premium Capital Fund, ASCF Select Income Fund The content on this page is intended solely for general informational and educational purposes and should not be interpreted as financial advice. Although we make every effort to ensure the accuracy and relevance of the information, it may not always reflect the latest legal or financial changes. We strongly recommend seeking guidance from a qualified financial advisor or professional before making any financial decisions. Use the information at your own discretion. |