NEWS

27 Oct 2021 - Stock Story: Seven Group

|

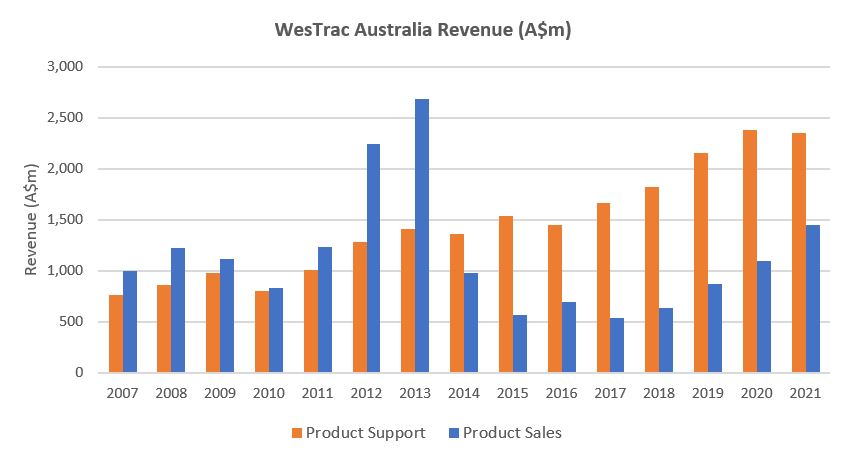

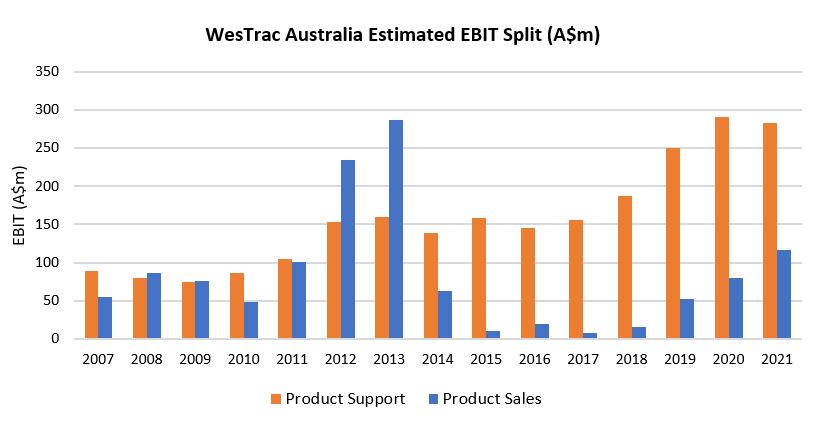

Stock Story: Seven Group Joe Wright, Airlie Funds Management 18 October 2021 Hiding in plain sight? At Airlie, we look to invest in quality companies that we believe are undervalued by the market. Often these opportunities emerge when a great business sits within an otherwise mediocre sector, or when the market assigns an arbitrary discount to a type of business. For us, Seven Group Holdings (SVW) falls into both categories. Seven is a conglomerate of industrial businesses. Two of these businesses sit in sectors often unloved by investors for their volatile returns and capital intensity - mining services (WesTrac) and equipment rental (Coates). Furthermore, in listed equities 'conglomerate' is a dirty word. It can imply complexity, opacity and bloat, where the corporate structure of the company sits at odds with interest of the shareholders, and many investors choose to avoid conglomerates for these reasons. In our mind, WesTrac and Coates are quality businesses sitting within mediocre industries, pushed further out of sight by the conglomerate structure of Seven. While investors digest the highly publicised on-market takeover of Boral or lament the decline of the namesake Free To Air TV business (Seven West Media), WesTrac and Coates quietly demonstrate their quality and form the majority of our valuation of Seven. WesTrac - Less cyclical than it appears?WesTrac is the authorised Caterpillar dealer in Western Australia, New South Wales and the Australian Capital Territory, providing heavy equipment sales and support to customers. Caterpillar employs an independent dealership sales model for its heavy machine sales and support services. Caterpillar thinks this model fosters a stronger relationship between dealers and local customers (acknowledging the importance of high-quality after-sales service and support) and allows Caterpillar to focus its capital allocation on product development and innovation. WesTrac sales are given in two segments - product sales (i.e. machine sales) and product support. Product sales have been reasonably cyclical, tied to future production volumes and the fleet replacement cycle of the tier-1 and tier-2 miners (and at a second derivative, commodity prices and miner profitability). Product support sales have been far more steady, growing at a 10-year rate of 7.0%, as new sales enter the maintenance program and old equipment sees parts intensity increase and its life extended.

Finally, Caterpillar has an internal target of doubling its revenue from product services (via the dealership network) by 2026, as it looks to take advantage of fleet-replacement cycle extensions and expanded product lifecycle offering.

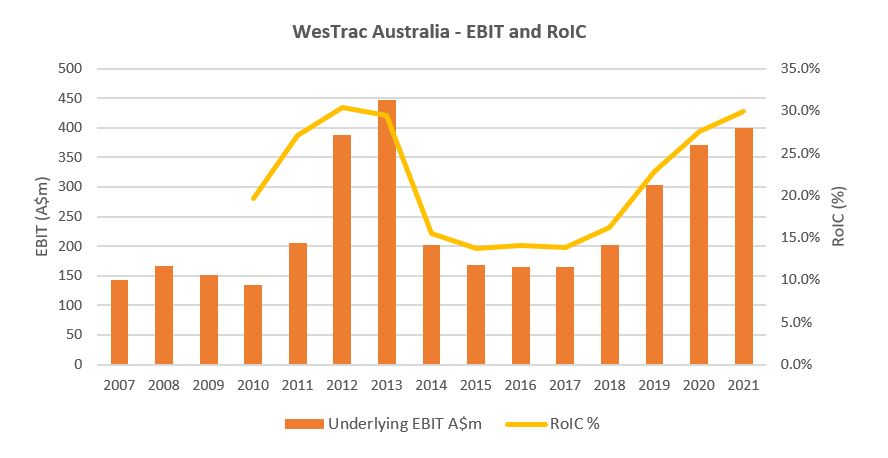

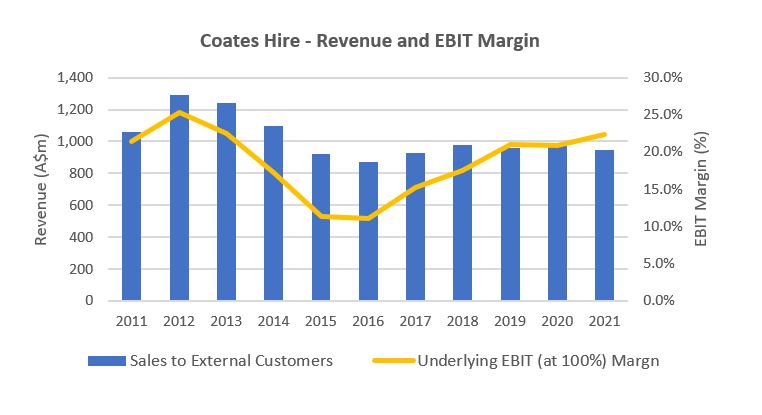

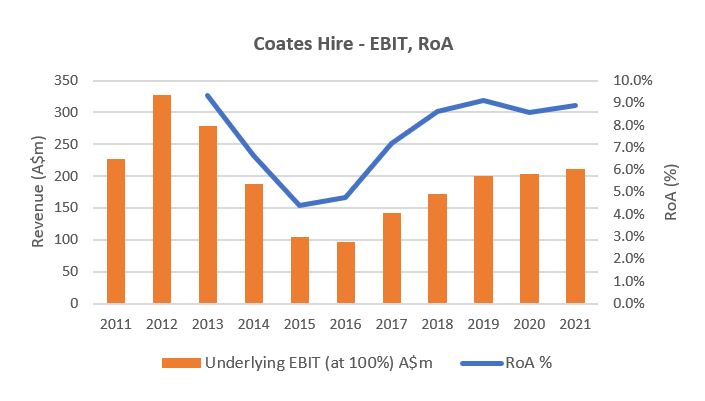

The net of this is that we believe WesTrac is far less cyclical than typical mining-services businesses, and earns stronger returns through the cycle, and should be valued as such. Coates - Impressive transformation ahead of a revenue inflection?Coates Hire is Australia's largest general equipment hire company and provides a range of general and specialist equipment to a variety of markets including engineering, building construction and maintenance, mining and resources, manufacturing, government and events. The business is primarily exposed to east coast infrastructure, industrial and residential projects, as well as resources activity. The Coates business is thriving. Following the resources boom earlier in the decade, Coates' margins slumped from about 25% to about 11% as revenue fell from about A$1.3 billion to A$870 million (-32%) from FY12 to FY16. Management has since undertaken a material cost-out, transformation program that has been delivered incredibly successfully:

For FY22, management has guided to high single-digit EBIT growth. Looking further out, management is driving the business towards the internal 'Team25' project goals. Team25 is a continuation of the existing transformation strategy within Coates with the business targeting A$1.25 billion of revenue and a 25% EBIT margin. Part of the success of the Team25 targets will rely on revenue growth driven from increased market share and east coast infrastructure spend, however cost-out initiatives still form part of the strategy. Were management to successfully execute on the Team25 targets, Coates would deliver about $313 million of EBIT, versus A$212 million in FY21 (+48% overall, or a 10% CAGR to FY25). The takeaways for us are two-fold:

Coates' margins and returns sit in the top-quartile of the global equipment rental sector, and there remains the potential for considerable earnings growth over the next two to three years (on top of that delivered steadily since 2016). Both of these factors suggest to us that the business is of higher quality than most would expect of typical rental equipment companies. ValuationOf course, Seven does not just consist of WesTrac and Coates. Within the conglomerate also sit stakes in listed companies Boral (70%), Beach Energy (30%) and Seven West Media (40%), as well as unlisted energy, media and property holdings. Of these investments, the recently acquired 70% stake in Boral is the most material (and where valuation is arguably most up for debate). Including the Boral investment, we estimate Seven is trading on a P/E multiple of sub 14x FY22 earnings, which is a about a 25% discount to the S&P/ASX 200, and in our mind an undemanding valuation. In our 'sum of the parts' analysis of the business, we see upside to the current share price when taking a more mid-cycle view of the earnings of WesTrac and Coates, and before including any material valuation upside to the Boral business, should management successfully execute the transformation program and unlock additional value in the non-core property portfolio. Finally, our confidence in the conglomerate structure comes back to ownership. Seven remains 60% owned by the Stokes family, with Kerry Stokes in the chairman role and his son Ryan as CEO. In our view this gives shareholders significant alignment with the board and management, and we have found that through time founder-led businesses tend to consistently outperform the broader index. Sources: Company filings and website |

|

Funds operated by this manager: Airlie Australian Share Fund |

27 Oct 2021 - Why consistency wins the race

|

Why consistency wins the race Magellan Asset Management October 2021

|

|

Timestamps: 01:10 - Fund objective 09:10 - Investment outlook 16:30 - Microsoft 21:58 - Netflix 28:11 - Why invest in China? Consumption / GDP Australia vs China Funds operated by this manager: Magellan Global Fund (Hedged), Magellan Global Fund (Open Class Units) ASX:MGOC, Magellan High Conviction Fund, Magellan Infrastructure Fund, Magellan Infrastructure Fund (Unhedged), MFG Core Infrastructure Fund |

26 Oct 2021 - Performance Report: Premium Asia Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | The Fund is managed by Value Partners using a disciplined value-oriented approach supported by intensive, on-the-ground bottom-up fundamental research resulting in a portfolio of individual holdings, which are, in the view of Value Partners, undervalued and of high quality, on either an absolute or relative basis, and which have the potential for capital appreciation. The Fund will primarily have exposure to the equity securities of entities listed on securities exchanges across the Asia (ex-Japan) region, however, the Fund may also gain exposure to entities listed on securities outside the Asia (ex-Japan) region which have significant assets, investments, production activities, trading or other business interests in the Asia (ex-Japan) region as well as unlisted instruments with equity-like characteristics, such as participatory notes and convertible bonds. The Fund may also invest in cash and money market instruments, depositary receipts, listed unit trusts, shares in mutual fund corporations and other collective investment schemes (including real estate investment trusts), derivatives including both exchange-traded and OTC, convertible securities, participatory notes, bonds, and foreign exchange contracts. |

| Manager Comments | Since inception in December 2009 in the months where the market was positive, the fund has provided positive returns 89% of the time, contributing to an up-capture ratio for returns since inception of 160.89%. Over all other periods, the fund's up-capture ratio has ranged from a high of 151.55% over the most recent 36 months to a low of 139.5% over the latest 48 months. An up-capture ratio greater than 100% indicates that, on average, the fund has outperformed in the market's positive months over the specified period. The fund has a down-capture ratio for returns since inception of 90.03%. Over all other periods, the fund's down-capture ratio has ranged from a high of 101.21% over the most recent 12 months to a low of 79.83% over the latest 24 months. A down-capture ratio less than 100% indicates that, on average, the fund has outperformed in the market's negative months. |

| More Information |

26 Oct 2021 - Performance Report: Bennelong Twenty20 Australian Equities Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | The Fund is managed as one portfolio but comprises and combines two separately managed exposures: 1. An investment in the top 20 stocks of the markets, which the Fund achieves by taking an indexed position in the S&P/ASX 20 Index; and 2. An investment in the stocks beyond the S&P/ASX 20 Index. This exposure is managed on an active basis using a fundamental core approach. The Fund may also invest in securities expected to be listed on the ASX, securities listed or expected to be listed on other exchanges where such securities relate to ASX-listed securities.Derivative instruments may be used to replicate underlying positions and hedge market and company specific risks. The companies within the portfolio are primarily selected from, but not limited to, the S&P/ASX 300 Accumulation Index. The Fund typically holds between 40-55 stocks and thus is considered to be highly concentrated. This means that investors should expect to see high short-term volatility. The Fund seeks to achieve growth over the long-term, therefore the minimum suggested investment timeframe is 5 years. |

| Manager Comments | The fund's returns over the past 12 months have been achieved with a volatility of 7.86% vs the index's 9.42%. The annualised volatility of the fund's returns since inception in November 2009 is 13.67% vs the index's 13.2%. Over all other periods, the fund's returns have been more volatile than the index. Since inception in November 2009 in the months where the market was positive, the fund has provided positive returns 97% of the time, contributing to an up-capture ratio for returns since inception of 128.82%. Over all other periods, the fund's up-capture ratio has ranged from a high of 142.43% over the most recent 24 months to a low of 125.68% over the latest 60 months. An up-capture ratio greater than 100% indicates that, on average, the fund has outperformed in the market's positive months over the specified period. The fund's down-capture ratio for returns since inception is 96.16%. |

| More Information |

26 Oct 2021 - Investment Perspectives: Don't fear the taper

|

Investment Perspectives: Don't fear the taper Quay Global Investors October 2021 |

|

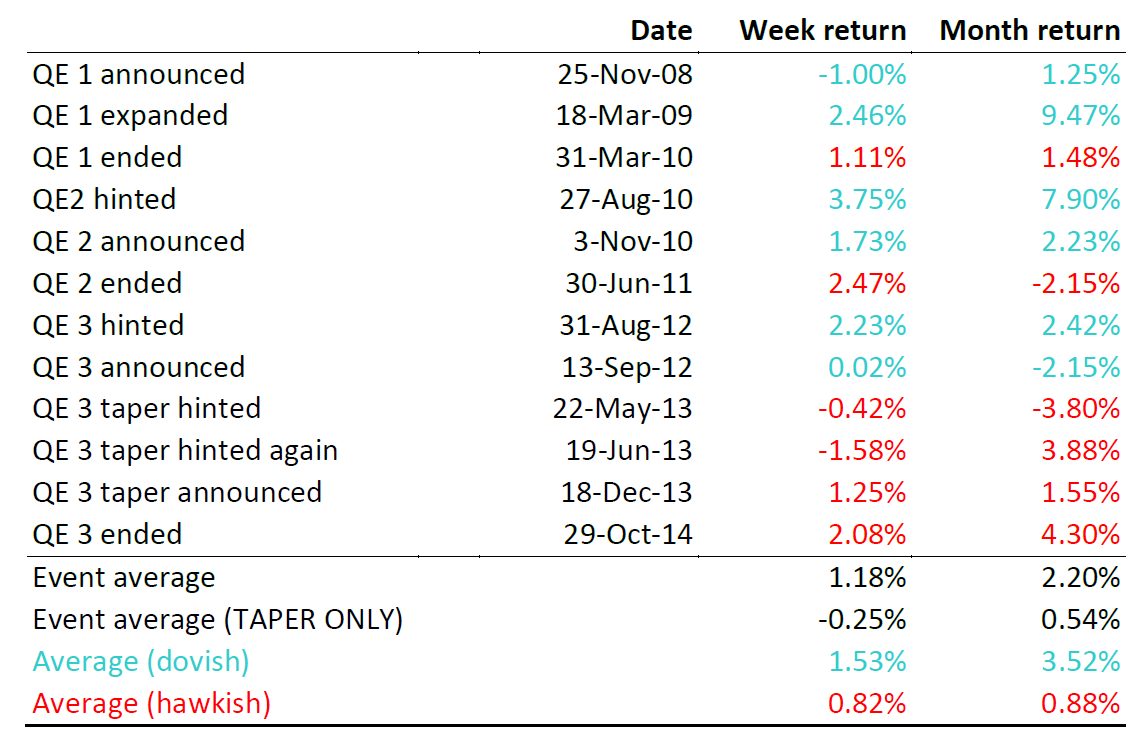

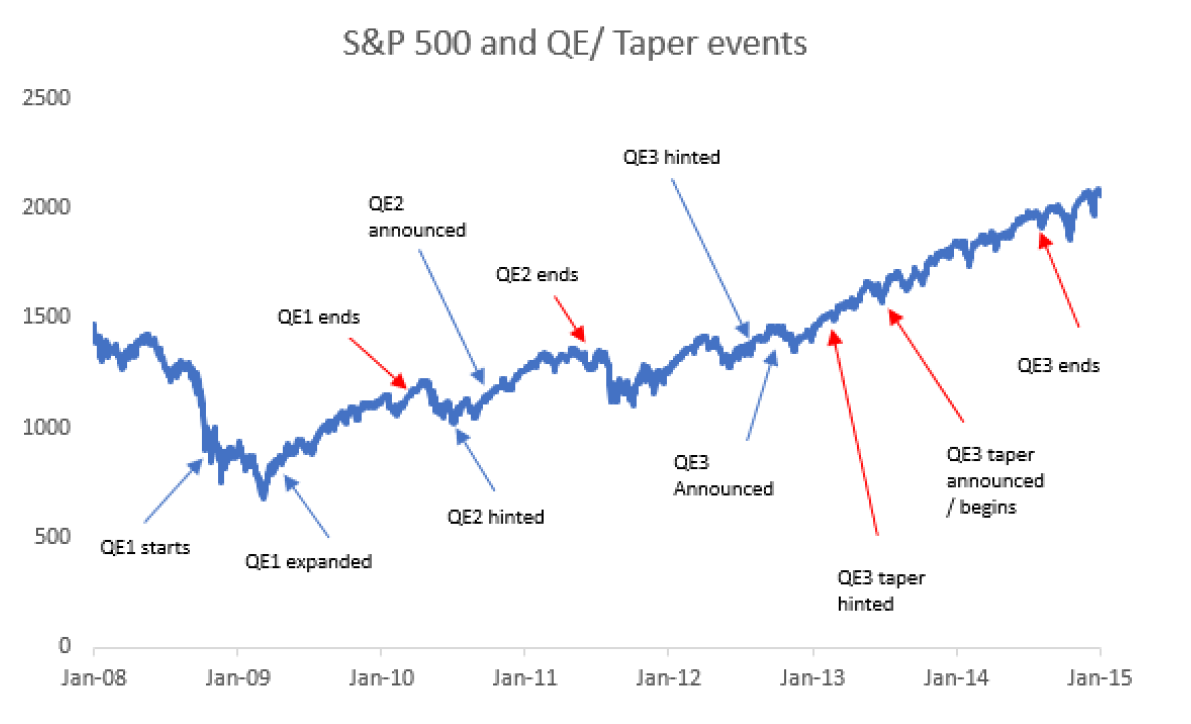

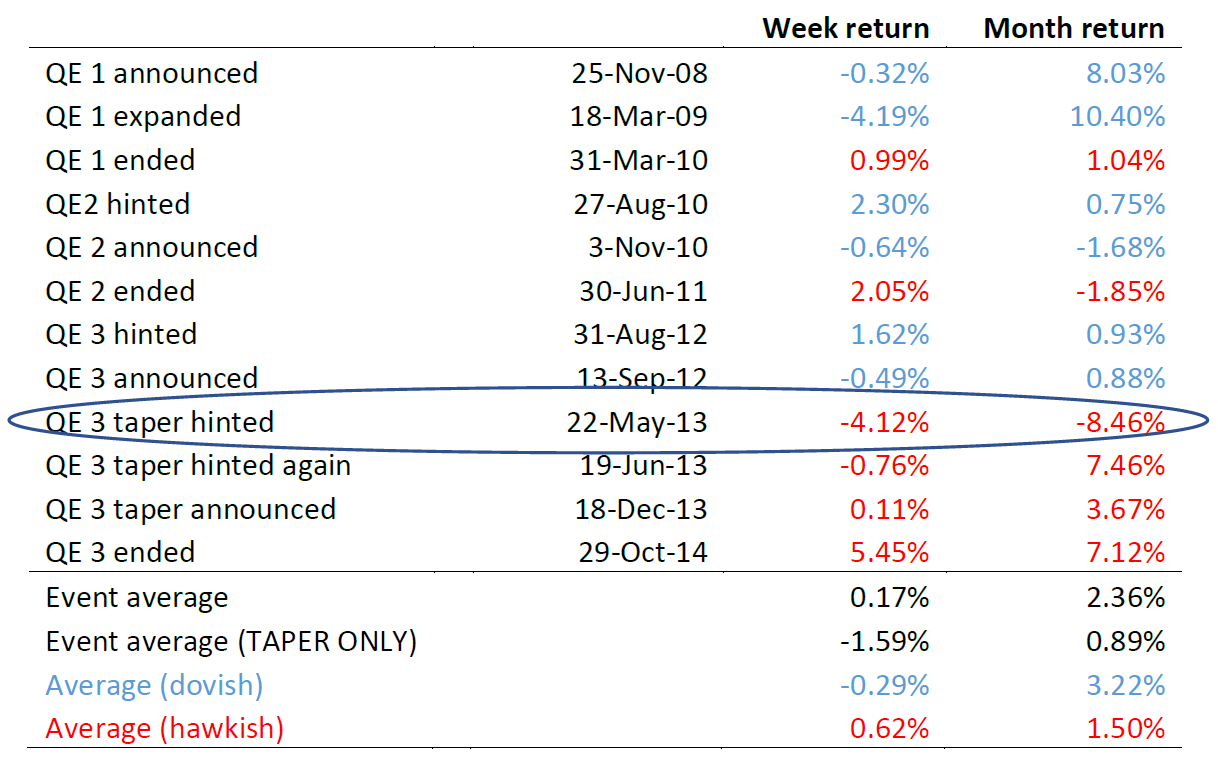

As vaccination rates increase around the world and we (hopefully) return to some normality in our daily lives, world economies appear to be stabilising. Economic output is near or above pre-pandemic levels, and signs of inflation and wage pressure have become a theme of 2021. As a result, many investors and commentators are now keeping a close watch on the US Federal Reserve and any change in current monetary policy: specifically, the quantitative easing program (QE) and the potential that the monthly asset purchases (US$120bn per month) will begin to slow, or 'taper'. Some investors have bad memories from the last time the US Fed tapered, and as such there appears to be some anxiety over the next central bank move. Indeed, in the minutes from last month's meeting, the committee stated, "Most participants noted that, provided the economy were to evolve broadly as they anticipated, they judged that it would be appropriate to start reducing the pace of (asset) purchases this year".[1] Should investors fear the taper? Some historic perspectiveSince the great financial crisis of 2008/2009, there have been three QE programs in the United States: two of which ended abruptly, and the third via taper (a gradual reduction in monthly asset purchases). The following table highlights the dates of each announcement (or signalling) of these policies, and measures the performance of the S&P500 Index in the week and month following these announcements.[2]

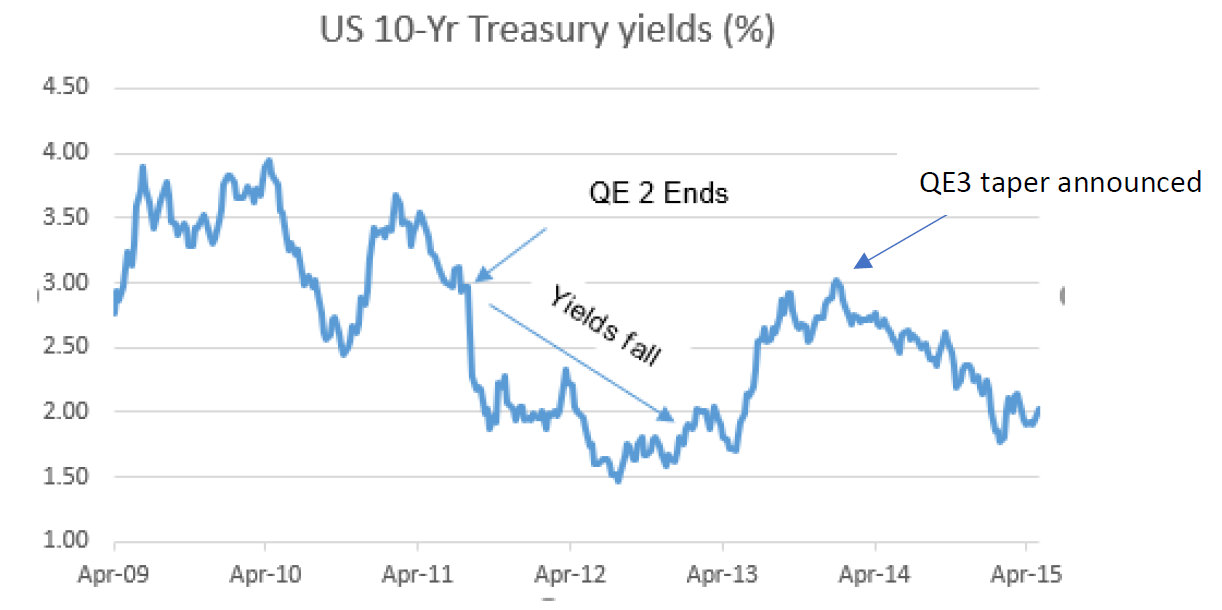

Source: Calculated Risk, Bloomberg, Quay Global Investors To assist our analysis, we have colour-coded each 'QE event' depending whether the policy announcement was dovish (supportive of the economy and more QE) in blue, or hawkish (restrictive and less QE) in red. The taper - which was first hinted at in a speech by Ben Bernanke on 22 May 2013 - set a clear path to the end of QE and led to the first post-GFC rate increase in December 2015. The data clearly shows a 'dovish' Federal Reserve tended to be good for stocks over the following week and month (on average up +1.53% and +3.52% respectively). However, it is also clear the end of QE (on average) is not necessarily bad for equities (on average up +0.82% and +0.88%). Most of the taper angst appears to be derived from the May 2013 statement to US congress by then-Chairman Ben Bernanke, when the concept of gradually reducing asset purchases was first suggested.[3] Unlike the end of the first two QE programs, this signalled a change in policy, and introduced 'the taper' for the first time. Yet in the current environment, this moment has already passed as per the September minutes. And based on historic performance, the idea that we should worry about any taper carries very little historic weight. Moreover, for investors not concerned with short-term performance, the best strategy post-GFC was to ignore the taper/QE noise entirely and simply stay invested.

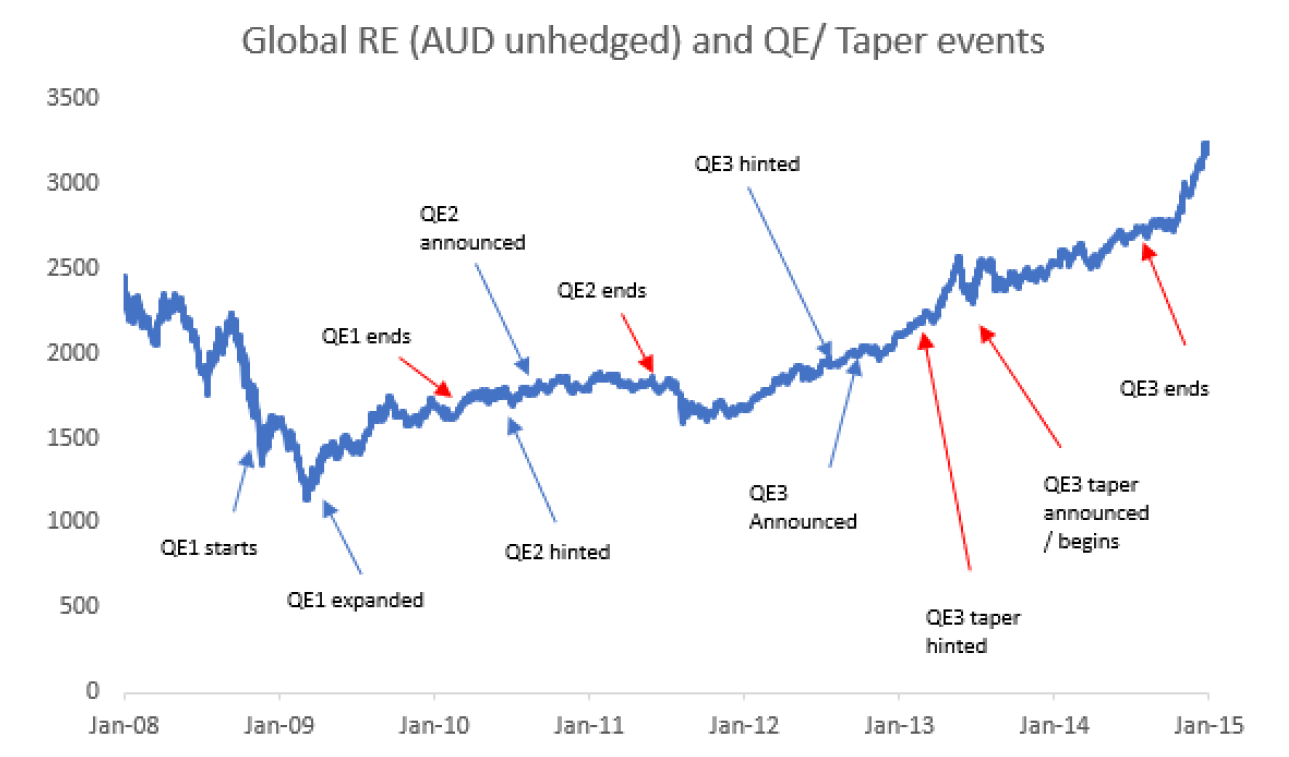

What about real estate?Listed real estate was not immune to the volatility caused by various quantitative easing announcements. However, the data again suggests there is little to fear with respect to any end to the QE program - although admittedly, there was more volatility. It would probably surprise some investors that global real estate did worse over the week after the Fed was dovish (-0.29%), compared with when it was hawkish (+0.62%). And like the S&P500, on average global real estate actually performed well in the month following the various taper announcements (+0.89%), and following hawkish statements (+1.50%) .

Again, as the following chart shows, long-term investors in global real estate that ignored the noise were rewarded over time. We also make the observation that global listed real estate performed best during and after the Fed became consistently hawkish following the initial taper hint in May 2013. This again should remind investors that real estate does best when the economy is good, not when interest rates are low (or central banks are dovish). For more on this, refer to our 2019 article 30 years of investment lessons from Japan.

Source: Bloomberg, Calculated Risk, Quay Global Investors Why QE has less impact on equity markets than most thinkA common narrative post financial crisis was that various central banks (across the world) influenced equity markets directly or indirectly with their various monetary programs - especially quantitative easing. Throwaway lines such as "flooding the market with liquidity" or "artificially reducing interest rates" or "forcing investors into risky asset" played well with the CNBC/Zero hedge crowd, but rarely are these comments scrutinised for the detail. The reality is that central bank influence on equity markets valuations is minimal at best, for the following reasons.

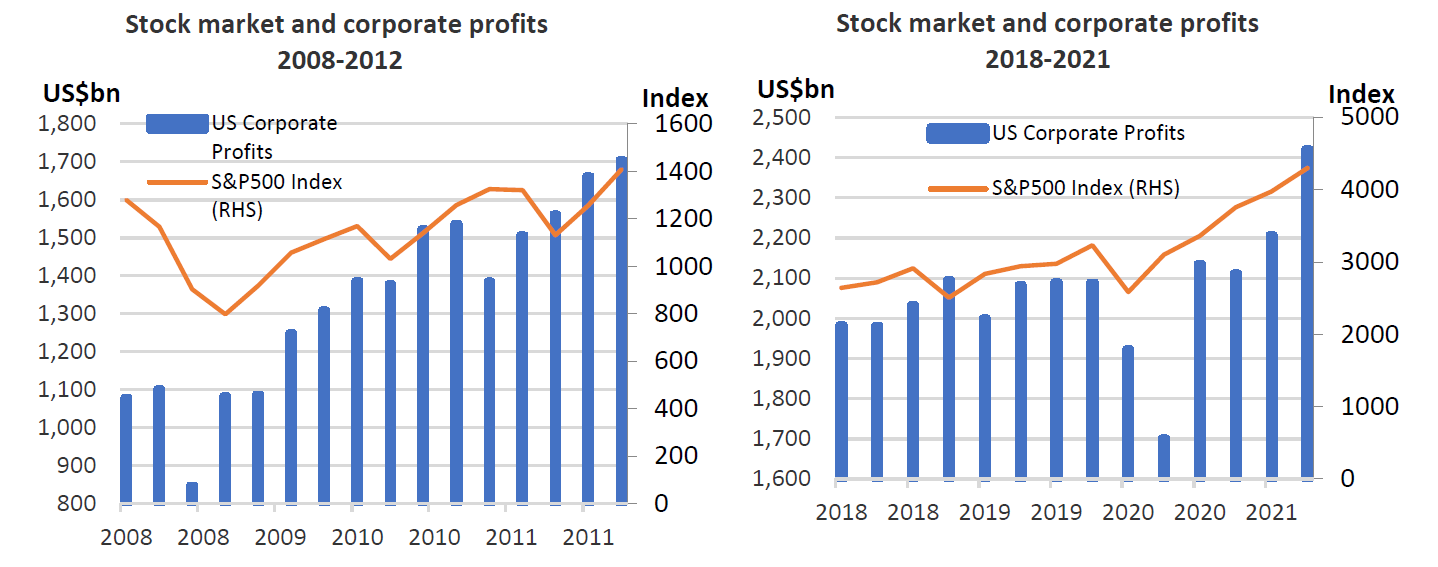

It's all about profitsAs we have stated in previous articles, what drives long-term equity returns are profits. And while some investors blame (or credit) central banks for share market performances, on most occasions equity performance is supported by rising earnings. As we highlighted in our June 2021 article checking in on Kalecki, the macroeconomic source of company profits is more closely aligned to fiscal policy (spending and taxing), not monetary policy.

Concluding thoughtsAt Quay, we are unapologetic in our bottom-up approach. This does not mean we ignore macroeconomic data or various government policy. The key is understanding which macroeconomic issues matter. The US has now enacted various forms of QE over the past 12 years - and not unlike the Japanese experience (now 20 years of QE), the data suggests worrying about central bank policy and actions is not productive for long-term investors. That's not to say equity markets are not overvalued; but if they are, it has more to do with animal spirits than the Fed. Our observation is investors should spend less time worrying about central bank actions that have very little impact on equity markets beyond a placebo effect - and more time remaining invested in high quality companies that grow cashflows sustainably over time. |

|

Funds operated by this manager: Quay Global Real Estate Fund |

26 Oct 2021 - The Winter of Discontent

|

The Winter of Discontent Arminius Capital 12 October 2021 The winter of 1978-1979 was disastrous for the UK economy. A combination of freezing weather, rising inflation, union wage demands, and public and private sector strikes caused fuel shortages, food shortages, and essential services failures. The press christened the period "the winter of discontent", borrowed from the first line of Shakespeare's Richard III. Not surprisingly, Margaret Thatcher won the May 1979 election. The coming winter of discontent will affect much of the northern hemisphere, but particularly the UK and China. The US is all but self-sufficient in energy, although it will continue to suffer supply chain disruptions. The EU has sufficient spare generating capacity and cross-border electricity transmission to mitigate the power problems, and Russia has promised to step up gas supply. India has managed to create its own coal shortage without having a Communist Party or a Conservative Party to make mistakes, but very few global investors have any exposure to the Indian share market. Boris Johnson doesn't have to face a general election until May 2024, but the winter of 2021-2022 is shaping up as a major public relations disaster for his government. Rising oil, gas, and commodity prices are exacerbated by higher transport costs, not to mention labour shortages in essential functions such as truck drivers, butchers, and process workers. Lack of truck drivers has forced the government to use the army to deliver petrol to service stations, and supermarkets are already suffering stock-outs of basic items such as eggs, milk, pasta, and canned fruit. The shortages have been blamed on COVID-19, Brexit, EU bloody-mindedness, UK government incompetence, private sector inadequacies, and global supply disruptions. What is clear is that there are no quick solutions. Xi Jinping is facing the same types of problems in China: power cuts and supply disruptions. The nationalistic (State-owned) media has blamed these on the usual suspects - corrupt officials, foreign saboteurs, counter-revolutionaries, and "bad elements" generally - but in China's case the true causes are well-documented. Demand for Chinese goods surged in 2021 as the global economy recovered. This meant that demand for electricity surged. But more than half of China's electricity comes from coal-fired plants, and since 2016 the central government had been forcing the closure of small coal mines, not in a quest for net zero emissions, but because of the very high levels of local pollution and industrial accidents in these small mines. Alex Turnbull makes a persuasive argument that part of the shortage was caused by the disruptive effects of anti-corruption campaigns in Inner Mongolia - see https://syncretica.substack.com/p/rectification-campaign-to-energy. So China needed more electricity than it had the coal to produce. The obvious next step was to import more coal. Unfortunately, the rest of the world wanted more coal too, so prices had already risen sharply. To complicate matters, in 2019 the central government had unofficially halted thermal coal imports from Australia, and the spare Australian coal had been sold to other countries. By mid-2021 it was clear that many Chinese provinces did not have enough electricity to power their economies. Yunnan, for example, has built an aluminium industry on cheap and abundant power from its hydro stations. But in 2021 low rainfall reduced hydro power supply, so Yunnan was forced not only to shut down alumina smelters, but also to reduce electricity exports to the neighbouring province of Guangdong. What made matters worse is that, because two-thirds of China's provinces had missed their targets for reducing energy consumption and energy intensity, the central government told cities which were home to major polluters to shut down the worst offenders for several hours a day or a few days each week. This means heavy industries such as steel, cement, glass, and paper manufacturers. Another complication: local power prices are set by the government, usually for the benefit of industrial and residential users. When higher coal prices pushed coal-fired power stations into losses, most governments would not agree to any power price rises. In response, generating companies stopped buying expensive coal and temporarily shut down their unprofitable power stations. Xi Jinping and his Politburo are several management levels above the grassroots, and bureaucrats are never keen to bring bad news to their bosses, so the extent of the problems did not become obvious until September. The eventual response shows that - unlike Boris Johnson - Xi Jinping took matters very seriously indeed.

INVESTMENT IMPLICATIONS Whatever happens in the UK will have very little impact on Australian investors. As a trading partner, the UK is slightly more important to us than Thailand. Ever since the Brexit vote in June 2016, the UK share market has traded at a 20% discount to other developed markets, so a lot of bad news is already priced in. By contrast, the power cuts in China are globally important, reinforced with the property market turmoil caused by the Evergrande default. The net effect will be to reduce China's GDP growth rate below 4% annualized over the next six months. Chinese imports of Australian iron ore will fall by 10% over this period, but Chinese imports of Australian thermal coal will rise unobtrusively. The Chinese factory shutdowns will add to the world's supply shortages and keep commodity prices weak until the Chinese economy is visibly back to normal - probably by March 2022. China's power outages will worsen global supply chain disruption, but the key factor which will end the US import shortages is consumers reducing their spending on goods and switching to spending on services. For China's share markets, the impact of the power cuts is negative, but it is far smaller than the damage done to China's tech giants already by the central government's regulatory crackdowns. Because Australia is already on the receiving end of China's unofficial trade war, the downside for us is minimal. Lost iron ore exports are offset by record coal exports. But Australian investors need to watch the Chinese economy, just in case it doesn't recover within six months. If so, there will be more negative consequences for the global economy. Funds operated by this manager: |

25 Oct 2021 - Performance Report: Frazis Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | The manager follows a disciplined, process-driven, and thematic strategy focused on five core investment strategies: 1) Growth stocks that are really value stocks; 2) Traditional deep value; 3) The life sciences; 4) Miners and drillers expanding production into supply deficits; 5) Global special situations; The manager uses a macro overlay to manage exposure, hedging in three ways: 1) Direct shorts 2) Upside exposure to the VIX index 3) Index optionality |

| Manager Comments | Since inception in July 2018 in the months where the market was positive, the fund has provided positive returns 80% of the time, contributing to an up-capture ratio for returns since inception of 217.49%. Over all other periods, the fund's up-capture ratio has ranged from a high of 398.65% over the most recent 24 months to a low of 145.19% over the latest 12 months. An up-capture ratio greater than 100% indicates that, on average, the fund has outperformed in the market's positive months over the specified period. The fund has a down-capture ratio for returns since inception of 104.06%, indicating that it has typically not fallen significantly more than the market during the market's negative months. |

| More Information |

25 Oct 2021 - Fund Review: Bennelong Twenty20 Australian Equities Fund September 2021

BENNELONG TWENTY20 AUSTRALIAN EQUITIES FUND

Attached is our most recently updated Fund Review on the Bennelong Twenty20 Australian Equities Fund.

- The Bennelong Twenty20 Australian Equities Fund invests in ASX listed stocks, combining an indexed position in the Top 20 stocks with an actively managed portfolio of stocks outside the Top 20. Construction of the ex-top 20 portfolio is fundamental, bottom-up, core investment style, biased to quality stocks, with a structured risk management approach.

- Mark East, the Fund's Chief Investment Officer, and Keith Kwang, Director of Quantitative Research have over 50 years combined market experience. Bennelong Funds Management (BFM) provides the investment manager, Bennelong Australian Equity Partners (BAEP) with infrastructure, operational, compliance and distribution services.

For further details on the Fund, please do not hesitate to contact us.

25 Oct 2021 - Manager Insights | Laureola Advisors

|

Damen Purcell, COO of Australian Fund Monitors, speaks with John Swallow, Director at Laureola Advisors. The Laureola Australia Feeder Fund has a track record of 8 years and has consistently outperformed the Bloomberg AusBond Composite 0+ Yr Index since inception in May 2013, providing investors with a return of 15.4%, compared with the index's return of 4% over the same time period. On a calendar basis, the fund has never had a negative annual return in the 8 years since its inception. The fund's largest drawdown was -4.9% lasting 10 months, occurring between December 2018 and October 2019.

|