NEWS

S&P 500 increased +6.2%, the Nasdaq rose +9.6%, whilst in

the UK, the FTSE was up +3.3%.

16 Jun 2025 - Glenmore Asset Management - Market Commentary

|

Market Commentary - May Glenmore Asset Management June 2025 Globally equity markets rallied strongly in May. In the US, the S&P 500 increased +6.2%, the Nasdaq rose +9.6%, whilst in the UK, the FTSE was up +3.3%. Domestically, the AllOrdinaries Accumulation index also performed strongly, appreciating +4.2%. On the ASX, the top performing sectors were technology and energy. The worst performers were defensive sectors such as utilities and consumer staples, which lagged as investor risk appetite recovered. As was the case in April, growth stocks performed very strongly in May with numerous technology stocks posting double digit gains. In bond markets, the US 10-year bond yield increased +28 basis points (bp) to 4.44%, whilst its Australian counterpart rose +16 bp to close at 4.27%. The Australian dollar was flat in May, closing at US$0.643. Funds operated by this manager: |

13 Jun 2025 - Reframing Net Zero: Investing in a >2°C World

|

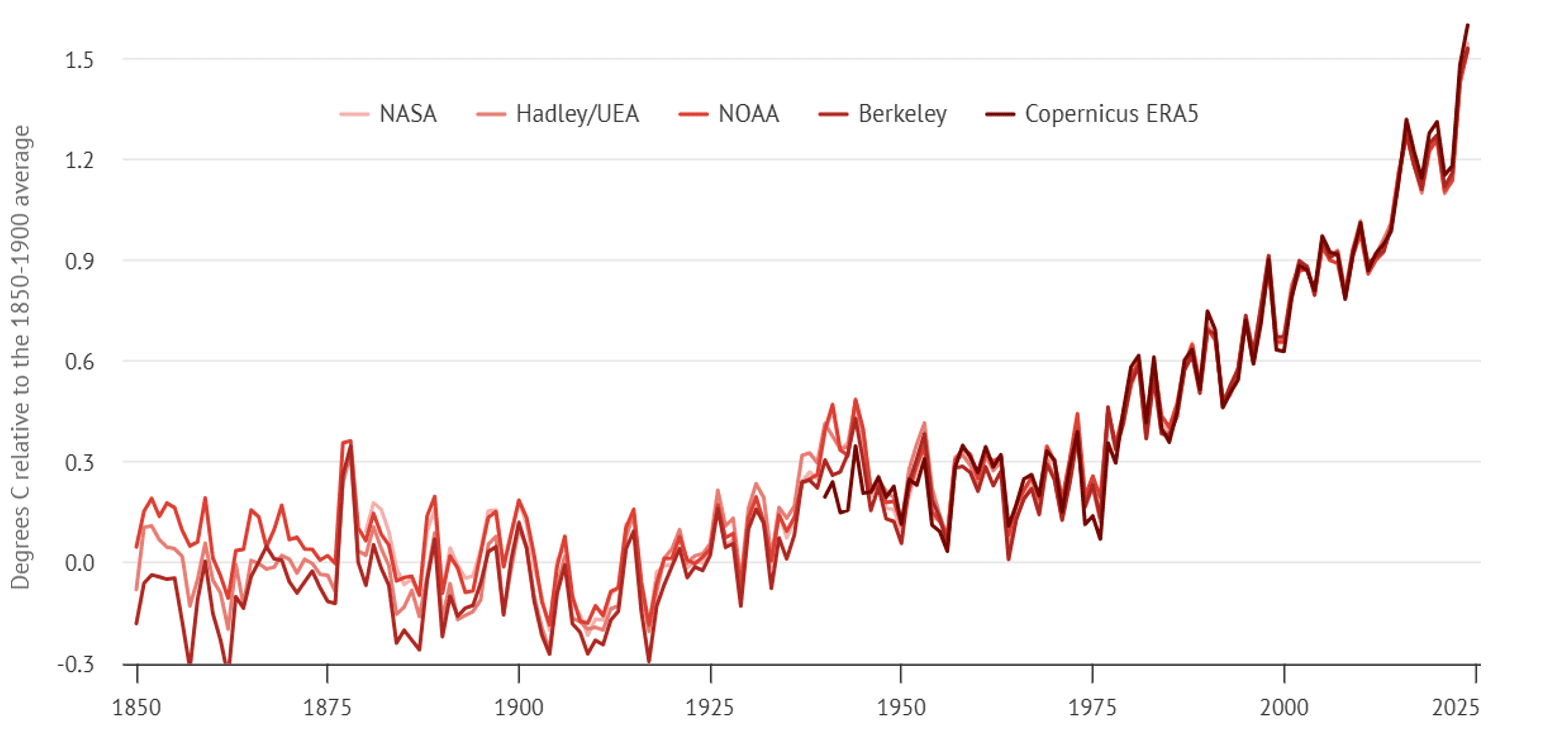

Reframing Net Zero: Investing in a >2°C World Yarra Capital Management May 2025 With warming very likely to exceed 2°C, investors face a radically altered investment landscape marked by intensifying physical risks, rising litigation and liability, evolving regulation and uneven progress in transition readiness. This paper outlines how we are recalibrating our research agenda and investment process in response to these profound structural changes. Our base case outcome driving our research approach now focuses on an adaptation and mitigation response rather than achieving a net zero outcome. To be clear, we believe we must continue to pursue net zero objectives. However, as fiduciaries, we must take a pragmatic approach to managing climate risks and opportunities. The New Climate RealityThe world has already surpassed 1.5°C of warming[1] (refer Figure 1), and current policy pathways suggest temperatures will surpass 2.4°C this century. Many physical climate events-heatwaves, wildfires, droughts and floods-are accelerating in frequency and severity[2]. The investible universe in Australia and globally is materially exposed to both direct and indirect consequences of this warming trajectory. Figure 1. Global surface temperatures over time relative to pre-industrial baseline

Source: Carbon Brief, Jan 2025. The Intergovernmental Panel on Climate Change (IPCC) 2023 AR6[3] report projects that our current policies and technological trend is pointing to well over 3°C warming by the end of the century, noting that we have already exceeded two-thirds of the global carbon budget to stay below 2°C. Indeed, the current Nationally Determined Contributions (NDCs) under the Paris Agreement[4] are insufficient to limit the world's warming to below 2°C and are now projected to lead to warming above 2.4°C. And in Australia, the growing recognition of this climate reality has led to the appointment of a new position, Special Envoy for Climate Change Adaption and Resilience following the May 2025 federal election,[5] and the recent release of the Australian Adaptation Database[6]. Investment Risks are on the RisePhysical risks are already driving financial losses. For example, Californian utility company Pacific Gas and Electric (PG&E) was forced to file for Chapter 11 bankruptcy in 2019, flagging over US$30 billion in liabilities after being held responsible for equipment failures and downed power lines that started the 2017/18 Californian wildfires, including one blaze which caused 84 fatalities. PG&E's share price is yet to recover and trades today some 3-4 times below its pre-wildfire levels (refer Figure 2). Figure 2. PG&E's share price fell 91% between Sept 2017 and Jan 2019

Source: YCM, Bloomberg, May 2025. Beyond being impacted by physical events, companies are also increasingly likely to be held liable for their contributions to physical events. Climate litigation is expanding. A recent model[7] attributes over US$8.5 trillion in damages globally to top fossil fuel producers. This research extended to Australia's five largest fossil fuel producers over this same period, with an estimated US$682 billion in economic damages directly attributable to these companies. Shareholders, clearly, will be impacted by rising corporate accountability for climate change. Attribution of cost implications of physical events to specific companies will be important to watch. In Table 1 (refer Appendix), we summarise the impacts on companies from physical disruptions as well as the potential liabilities associated with causing physical events. A detailed list of sector-specific considerations is also included in Table 2 (refer Appendix). We are actively analysing these risks to every company that we research, and it now forms a key pillar in our engagement agenda. Portfolio Implications for a Warming WorldAs investors, understanding (i) the portfolio implications of a likely delayed transition; and (ii) the higher physical impacts resulting from climate change are critical. Our process is also evolving. Whereas like many investors we have historically worked to understand the path to targets and the associated risks, our focus has shifted to focus acutely on mitigation and adaptation. We are moving beyond 'net zero pathways' to model how climate outcomes - not just targets - affect value and risk. Our analysis now focuses on physical exposure mapping, litigation trends and adaptive capacity across sectors. Key opportunities include companies enabling climate adaptation, resilient infrastructure, diversified and adaptive supply chains, and carbon removal technologies. We expect to observe: 1. Climate Adaptation

2. More Resilient Infrastructure

3. Increasingly Diversified and Adaptive Supply Chains

4. Greater Investment in Carbon Removal Technologies

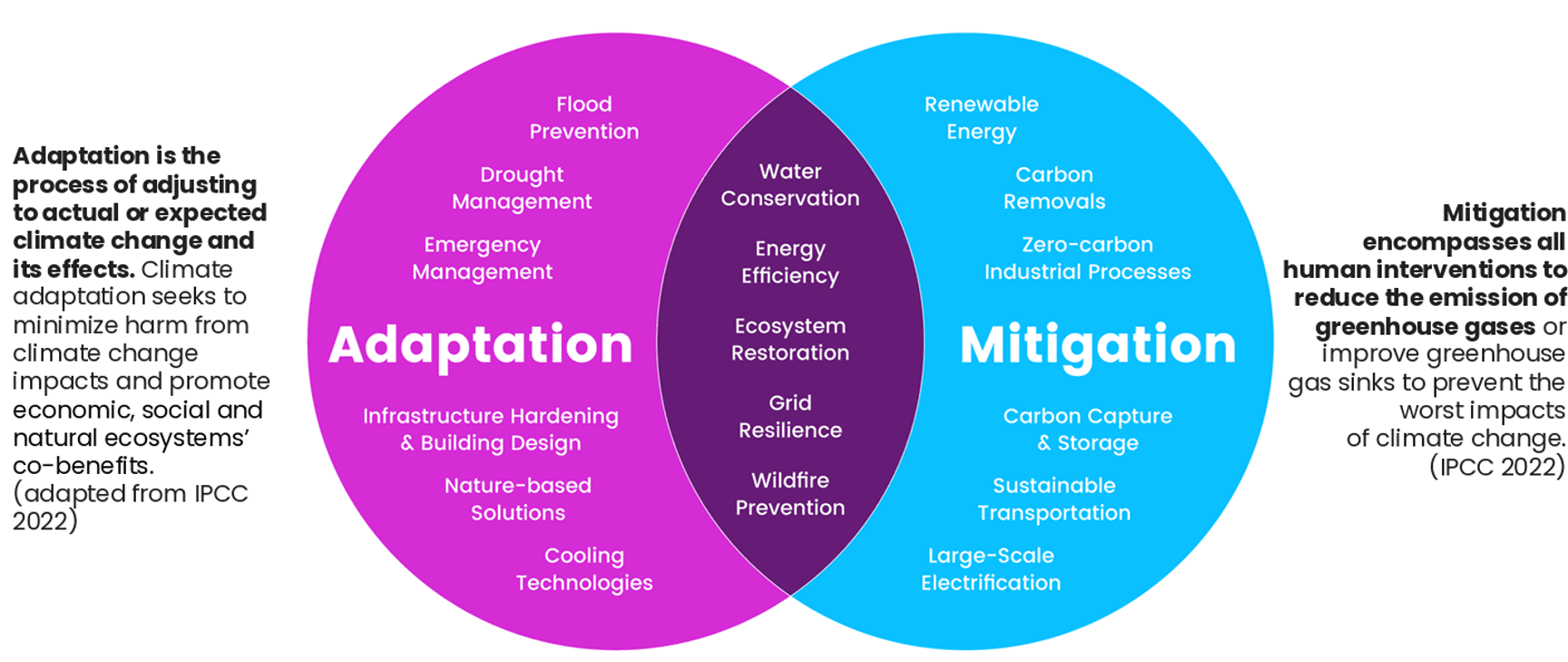

Mitigation and adaptation strategies also include specific initiatives to slow down or reverse the effects of global warming (refer Figure 3). Figure 3. Adaptation and mitigation opportunities

Source: Tailwind Climate Adaptation Finance Primer. What We're Doing DifferentlyWith the world on a trajectory beyond 2°C, understanding and navigating the risks associated with this emerging reality is crucial. In particular, we are: 1. Reassessing Portfolio Risks and Implications 2. Refining our Stewardship and Engagement Priorities 3. Positioning for Opportunities The climate investment narrative has shifted from 'if' to 'how much' and 'how fast'. Portfolio resilience now requires a forward-looking understanding of both climate impacts and adaptation dynamics. We are sharpening our research to reflect this new reality and to ensure we continue to deliver value in an era of accelerating environmental change. +++ [1] Source: https://wmo.int/news/media-centre/wmo-confirms-2024-warmest-year-record-about-155degc-above-pre-industrial-level. [2] Source: https://soe.dcceew.gov.au/overview/pressures/climate-change-and-extreme-events; We note that some physical events may have uneven impacts across regions, including some regions, such as Queensland, projected to experience potentially decreasing frequency and increasing severity of cyclones; whereas other risks, in particular, chronic risks are projected to increase in both frequency and severity. [3] Source: https://www.ipcc.ch/assessment-report/ar6/. [4] Source: https://unfccc.int/. The Paris Agreement is a legally binding international treaty that aims to limit global warming to well below 2°C with efforts to limit it to 1.5°C through national commitments to reduce greenhouse gas emissions, enhance climate resilience and provide support for developing countries. In 2015, 195 countries signed this agreement; and as of March 2025, there are currently 196 countries and the European Union who are signatories, representing an estimated 85-90% of global greenhouse gas emissions (following the withdrawal of the United States - which accounts for an estimated 15% of global emissions - by executive order in January 2025). In 2018, the Intergovernmental Panel on Climate Change (IPCC) published a special report noting that limiting the global temperature increase to 1.5°C above pre-industrial levels would significantly reduce the risks and impacts associated with climate change compared to an average increase of 2°C. This included lower levels of biodiversity loss, sea-level rise and extreme weather events such as heatwaves and more frequent and severe storms. [5] Source: https://www.pm.gov.au/media/press-conference-canberra-12may25. [6] Source: https://australianadaptationdatabase.unimelb.edu.au/. [7] Source: https://www.nature.com/articles/s41586-025-08751-3. |

|

Funds operated by this manager: Yarra Australian Bond Fund , Yarra Australian Equities Fund , Yarra Emerging Leaders Fund , Yarra Income Plus Fund , Yarra Enhanced Income Fund , Yarra Australian Smaller Companies Fund , Yarra Ex-20 Australian Equities Fund , Yarra Global Small Companies Fund , Yarra Higher Income Fund |

12 Jun 2025 - One Year On: Responsible AI engagement examples and reflections

|

One Year On: Responsible AI engagement examples and reflections Alphinity Investment Management May 2025 |

|

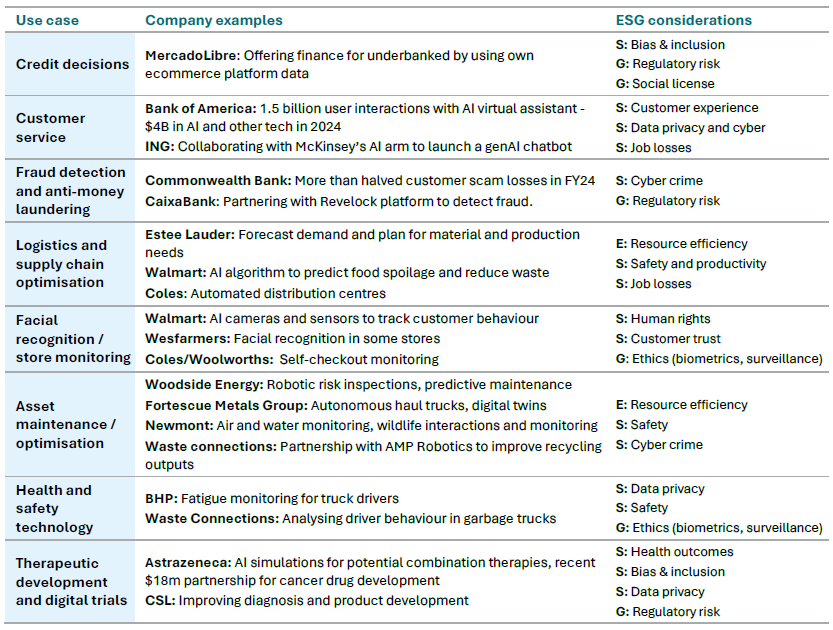

Artificial Intelligence (AI) is fast becoming a powerhouse for individuals and businesses, offering automation, data-led insights and boosted efficiency. With this huge opportunity, however, comes challenges and risks that need to be carefully considered. With AI uptake moving quicker than many expected, Responsible AI needs to match the pace. Alphinity has been digging into the ethics of AI technologies for quite some time, considering the potential risks to companies, society and the environment. This curiosity led to an exciting collaboration with Australia's premier national science research agency, Commonwealth Scientific and Industrial Research Organisation (CSIRO), in 2023. We co-developed a landmark Responsible AI Framework which was released in 2024. Now, after a year of use, we have some reflections to share. This article highlights AI use cases that we see companies adopting, some of the related ESG risks, and notable company engagements that were driven by applying the framework to our investments. Spotlight: Responsible AI FrameworkIn May 2024, Alphinity and CSIRO released a Responsible AI Framework (RAI Framework) to assist both investors and companies navigate the flourishing AI opportunity. The framework is a practical, three-part toolkit that bridges the gap between emerging responsible AI considerations and existing ESG principles such as workforce, customer, data privacy and social license. The framework is designed to set a standard in responsible AI and can be used flexibly depending on the investor's scope and needs. It is also intended to help companies understand investor expectations around responsible AI implementation and disclosure. The report and toolkit can be explored here: A Responsible AI Framework for Investors - Alphinity Why should investors care about responsible AI today?AI holds significant potential but also presents various environmental and social risks. For instance, the reliance on data centres leads to increased greenhouse gas emissions, which may result in climate change-related risks, including carbon pricing. Additionally, their high water usage could need to be restricted during droughts, or be subject to future regulations as recently proposed in Europe. The business stability of entities within the AI value chain could be adversely affected if these issues are not promptly identified and managed. These risks are prevalent throughout the AI value chain, from semiconductor producers to software providers, but are particularly significant in the short-term for hyperscalers such as Microsoft, Alphabet, and Amazon. AI can help drive automation, supercharge productivity and assist with the performance of repetitive tasks. But what happens when workers are displaced, or when the AI tool hallucinates or malfunctions? Employees and unions could react, creating social tension and affecting customer service. Wider operational disruptions and/or cybersecurity issues are also possibilities. A consideration in the healthcare industry is to balance the cost and timing benefits around clinical trials and product development, with the potential risks to data quality, bias and real-world validation of AI-lead drug discovery. We believe that in order for AI opportunities to be realised, the governance, design, and application of the AI needs to be undertaken in a responsible way, considering any environmental, social, and evolving regulatory considerations of AI and mitigating these impacts wherever possible. To help us think through these implications, we take a use case first approach. That is, we identify the relevant use cases by sector or company, then assess the relevant ESG considerations including the company specific mitigation efforts. This has supported more proactive and targeted research and engagement with companies and has enabled us to better identify and integrate the various risks and considerations into our ESG assessments. This approach has been illustrated in the table below. It presents some of the more common use cases, some company examples and the relevant ESG threats and/or opportunities.

40+ company meetings: Continued engagement on responsible AISince publishing the framework, our focus has been on assessing responsible AI risks and opportunities within our investments. Building on the 28 company interviews conducted in 2023 for the research project, our engagement with portfolio companies and prospects has continued. These discussions not only shed light on how AI use cases are evolving, they also help us to assess how responsible AI practices are progressing. Since publishing the report in May last year, we've undertaken a further 15 engagements where insights from our RAI Framework guided the discussions. We shared our framework with organisations such as Wesfarmers, Medibank, AGL, Origin, Aristocrat Leisure, Netflix, Intuitive Surgical, Novonesis, Mercadolibre, Thermo Fisher, CaixaBank and Schneider Electric. The RAI framework has been a practical way to communicate the types of information investors seek to evaluate AI-related risks. Pleasingly, companies like Medibank and MercadoLibre have said that the resource has been helpful to guide internal responsible AI practices. Insights and examples from these engagements are categorised into: Financial services, Healthcare, Technology products and platforms, and Industrials and energy services. Financial servicesCaixaBank: AI Investment Guided by Governance Framework CaixaBank, a prominent Spanish bank, is investing €5 billion in AI to benefit millions of customers. The bank has seen early success with AI in customer service claims, call centre operation, and code generation. There are regulations in the European AI Act that require additional controls and governance mechanisms to ensure the quality of AI outputs in the banking sector. We spoke with the Head of Data Governance to explore the bank's responsible AI approach, confirming preparedness for AI regulation. The company's AI Governance Framework ensures oversight of AI applications and adhered to principles like cybersecurity, fairness and reliability. We recommended that CaixaBank publish a responsible AI policy and disclose more on AI implementation to further enhance its leading approach. Commonwealth Bank of Australia (CBA): Advanced Technology and Responsible AI Strategy CBA's responsible AI strategy is globally recognised, leveraging the company's advanced technological background and ethical AI programs since 2018. Ranked first in the Evident AI Index for leadership in Responsible AI, CBA collaborates to manage regulatory and reputational risks. The bank introduced a Responsible AI Toolkit in 2024 and completed 15,000 modules on Generative AI and Deep Learning. We view CBA's approach as leading and are supportive of its ongoing disclosures to shareholders. In 2023, we provided feedback to CBA that it should consider publishing its Responsible AI Policy. The Bank published this policy later the same year and is presently one of the only Australian companies with a publicly disclosed position. HealthcareMedibank: Leveraging AI for customer service and healthcare analytics In early 2024, we engaged with health insurer Medibank to explore AI opportunities in healthcare and the way in which it considers related implications such as data privacy, bias and customer trust. The company has been using AI to support customer call experiences and to improve healthcare analytics. Medibank has established an AI Governance Working Group that evaluates each AI use case before implementation, to consider aspects such as customer, reputation and data risks. We are pleased to share that Medibank has adopted our Responsible AI Framework to benchmark its own practices. Medibank is also considering our feedback on publishing a responsible AI policy and disclosure on AI governance implementation. Intuitive Surgical: Enhancing minimally invasive surgery and patient outcomes with AI US medical device company Intuitive Surgical is a pioneer in health technology and has moved to improve robotic surgery processes through machine learning and predictive analytics. We engaged with the company to better understand these exciting use cases and explore its responsible AI strategy. For instance, postoperative recommendations have become more effective as they combine surgery indicators, such as blood loss or operating time, with patient outcomes like pain levels and recovery. Future opportunities point to AI being used within surgery, for example staplers using AI to measure and adjust tissue compression in real-time to help with precision and patient recovery. The company manages cybersecurity and data privacy to high standards, and we suggested that publishing a responsible AI policy that outlines governance - including its management of important risks like bias and quality control - would be useful to investors. Thermo Fisher: Enhancing healthcare through AI, overseen by a bioethics committee US healthcare company Thermo Fisher Scientific has been using AI and machine learning for many years to streamline internal operations and improve productivity, especially in clinical trials where AI can support disease detection, drug discovery and diagnostics. We engaged with the company to learn more about these AI applications and responsible AI considerations. Thermo Fisher highlighted the role of its bioethics committee, which was established in 2019 and has subject matter experts developing a policy commitment, in guiding its responsible AI activities. We provided information on our Responsible AI Framework and encouraged the publication of the policy in line with best practices. Technology products and platformsNvidia: Launched an AI Ethics Committee and customer KYC process Nvidia is a renowned AI enabler which supplies more than 40,000 companies, including 18,000 AI startups. Early in 2025, we had a meeting in which we discussed the balance between sustainability solutions which could be brought by AI, with the energy and water needed to power these tools. Nvidia highlighted that AI provides many exciting solutions like advanced weather modelling for adaptation and resilience, enhanced maintenance practices via digital twins, and automation and route optimisation to lessen carbon emissions in manufacturing and transport. The company is working to disclose these different end-markets, along with energy and water use, which will offer greater insight into Nvidia's sustainability contributions. Nvidia also established an AI ethics committee in 2024 to oversee the development of AI with an emphasis on trust and ethics. The committee's initial focus was to identify new AI use cases and develop a framework to recognise potential risks in product development and customer use. For instance, the committee recommended additional testing and the implementation of guardrails for a specific product, which subsequently increased due diligence requirements for sales to certain customers. These were subsequently adopted by the development and sales teams. We feel this demonstrates a good level of responsible AI integration through the business. Aristocrat Leisure: Balancing innovation with responsible AI We conducted a responsible AI assessment utilising our framework and engaged with Aristocrat Leisure to understand the AI use cases across its business. We learned that the more recent generative AI use cases include coding, creative development, marketing and general employee productivity. The company has an AI governance program which includes regular use case reviews by a central AI Working Group. This is a good structural model and the Board receives updates at least semi-annually. Aristocrat has also engaged external advisors to provide additional guidance on responsible AI. Workforce impacts and employee sentiment are being considered through employee surveys that measure the impact of AI tools. Overall, we observed that Aristocrat is adopting new AI tools, had a good level of workforce adoption and is building a good foundation in responsible AI. We provided feedback that a responsible AI policy would be a good next step. Industrials and energy servicesSchneider Electric: Enhancing AI and industrial automation Since 2021, French electrical parts company Schneider Electric has expanded AI hubs in India, France, and the US to improve electrification, energy efficiency, and automation. It plans to invest more than $700 million in the US to enable AI growth, domestic manufacturing and energy security, creating 1,000+ new jobs and boosting digital capabilities. In December 2024, we engaged with the company and discussed AI opportunities and responsible practices. Its AI solutions follow strict governance and ethics standards, managing bias and discrimination through a responsible AI program. A broader AI strategy for 2025-2030 is in development, and we provided our research report as feedback. We also recommended publishing an AI policy to enhance confidence in managing AI risks and opportunities. AGL: AI in energy networks AGL Energy has been using AI for some time in various areas, including energy generation, network maintenance and in the electricity retailing part of the business. AGL introduced a relatively recent technology strategy in which AI is one of the four key pillars, and one of the significant use cases discussed was in predictive maintenance. AGL is on the journey to embed responsible AI practices into its operations and are considering suitable governance structures. Reflections and conclusionAs companies continue to invest in AI, the transformative business impacts are becoming increasingly clear. As described in the company engagement examples above, AI's potential is evident in areas such as healthcare, industrial automation, energy management, and improving general productivity through processes like coding, customer service and marketing. From a responsible AI perspective, we have noticed an increase in cross-functional governance structures and policy commitments, as well as a growing awareness of the legal, ethical and ESG risks that come with AI deployment. In terms of external benchmarking, there has been some progress including the finalisation of the ISO27001 AI Safety Standard, which indicates a trend towards verified AI systems. Important disclosure metrics related to responsible AI, however, as detailed in the deep-dive component of our framework, are still in early stages. We would like to see metrics such as the number of AI-related incidents, energy usage from applying AI, cost savings from AI, the number and outcomes of AI audits, and the number and types of complaints related to AI. With 'agentic AI' now the next frontier, we are aware this will bring another level of complexity to AI decisions. We feel that responsible AI governance structures, such as those outlined in our framework, can help organisations to harness AI opportunities, while steering away from some of the risks. Therefore, the three main engagement priorities for portfolio companies are:

Regulatory developments continue to progress (for example, the EU AI Act and the recent AI Action Summit where a joint declaration on inclusive and sustainable AI was signed by 58 countries) but we have observed that no significant or compelling regulations have emerged recently. As such, we continue to monitor resources such as the World Benchmarking Alliance's Digital Benchmark as well as newer benchmarks like the Evident AI Index, which offer useful insights. We have also been broadening our research scope to benchmark and evaluate the ESG risks within the AI value chain, including emissions, energy, and water usage in data centres. We hope to be able to share more on this in future. |

|

Funds operated by this manager: Alphinity Australian Share Fund , Alphinity Concentrated Australian Share Fund , Alphinity Sustainable Share Fund , Alphinity Global Equity Fund , Alphinity Global Sustainable Equity Fund

This material has been prepared by Alphinity Investment Management ABN 12 140 833 709 AFSL 356 895 (Alphinity). It is general information only and is not intended to provide you with financial advice or take into account your objectives, financial situation or needs. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. Any projections are based on assumptions which we believe are reasonable but are subject to change and should not be relied upon. Past performance is not a reliable indicator of future performance. Neither any particular rate of return nor capital invested are guaranteed. |

11 Jun 2025 - Canopy Highlights - insights from our global research

|

Canopy Highlights - insights from our global research Canopy Investors May 2025 With quarterly results now in for most of the companies we follow, we've compiled the latest Canopy Highlights-insights from our global research. Just as investors have faced heightened volatility, business leaders are navigating a similarly complex environment. According to The New York Times and FactSet, 87% of corporate earnings calls this season referenced the word "uncertainty," up from 38% in the previous three months-a theme echoed by many of the companies we look at. Tariffs front and centre While many businesses had already begun diversifying manufacturing and sourcing in response to US tariffs introduced during the previous Trump administration, renewed uncertainty is accelerating those efforts. Take Floor & Décor, a US hard surface flooring retailer: in 2018, ~50% of its products were sourced from China. By the end of FY25, that figure is expected to fall to the low- to mid-single-digits, though most of its sourcing will remain outside the US. Another example is Yeti, which sells drinkware and coolers. While ~80% of its drinkware was produced in China as at the end of FY24, it is targeting a reduction to ~10% by the end of FY25, with most of that capacity being relocated elsewhere in Asia. However, for many, shifting production remains impractical, with most companies indicating plans to pass on tariffs through price increases. Bigger ripple effects? The larger impacts may be indirect: falling consumer confidence, delayed capital decisions, and a general pause in big-ticket spending were cited across sectors-from global luxury to US industrial spending to housing. Much of this stems from a lack of US policy certainty and high interest rates. As Assa Abloy, a global supplier of locks and doors put it: "The challenge with the tariffs is a little bit that it changes every day...So, the answer I can give you is only the answer as it is today, as the tariffs stand...this morning, because perhaps they change this afternoon". Some tailwinds too Not all companies are struggling. Discount retailer Dollar General is benefitting from trade-down by lower-income consumers. Fixed income trading platform MarketAxess is seeing gains from increased market volatility, with average daily credit trading volumes up >30% in April-an improvement from flat growth in the two quarters to March. And some international companies we've spoken with have cited rising anti-American sentiment as a potential commercial tailwind.

|

|

Funds operated by this manager: |

10 Jun 2025 - Australian Secure Capital Fund - Market Update

|

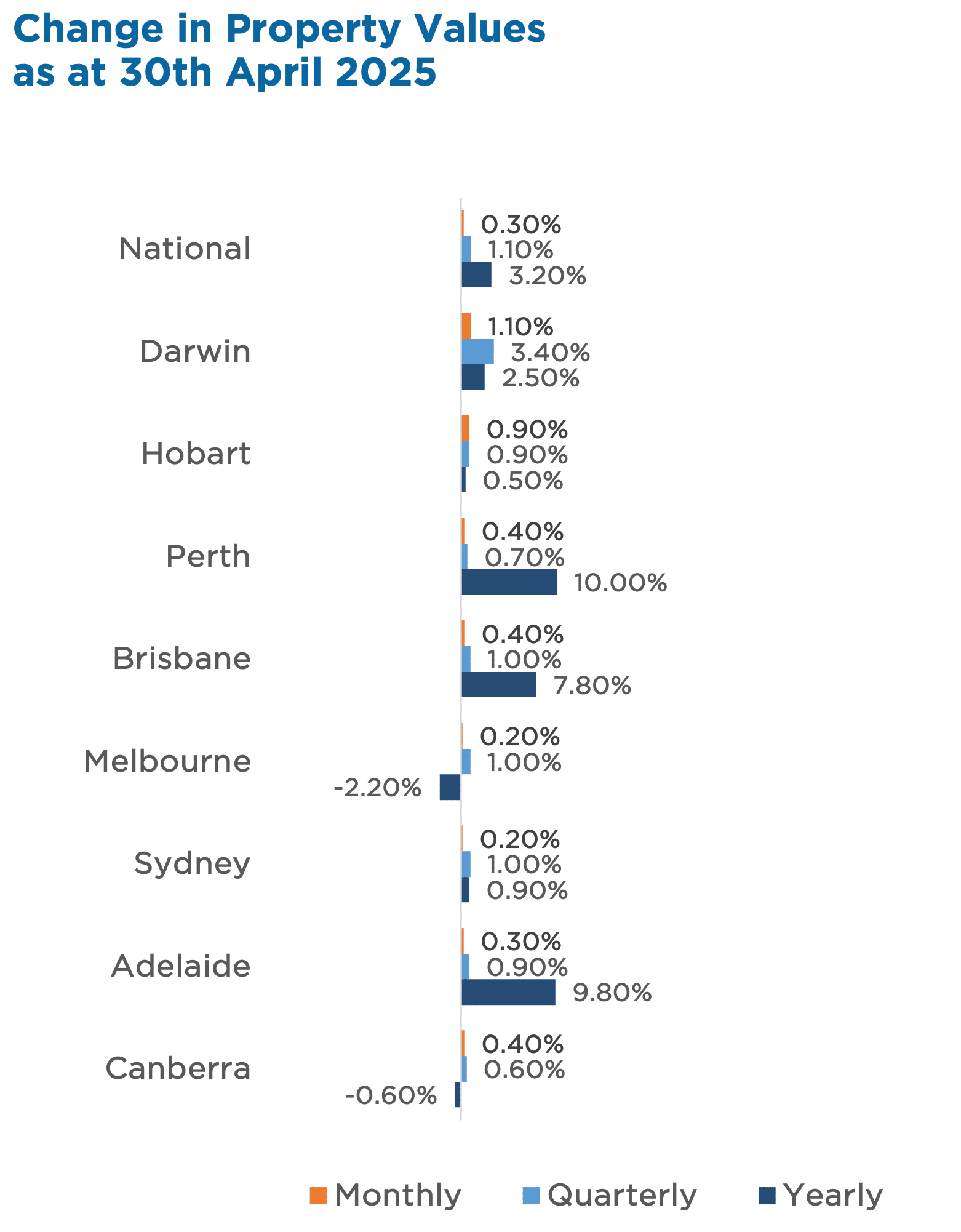

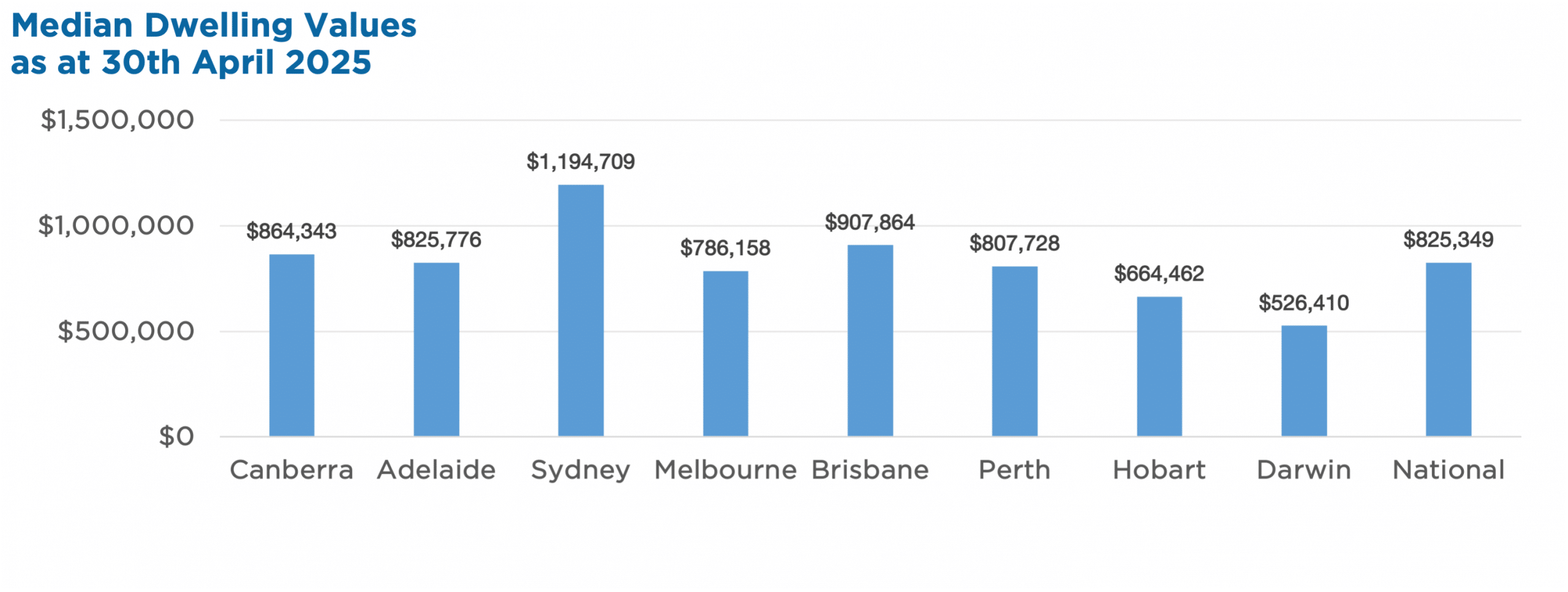

Australian Secure Capital Fund - Market Update Australian Secure Capital Fund May 2025 National home values rose for the third month in a row, with CoreLogic's Home Value Index up 0.3% in April, adding roughly $2,720 to the median Australian dwelling. Growth was recorded across all capital cities, though the pace slowed slightly from March. While mid-sized capitals and regional markets led the charge, Sydney and Melbourne remain below previous highs. Annual growth eased to 3.2%, reflecting last year's broader slowdown despite a recent rebound since February's rate cut. Key Highlights:

Property Values

|

6 Jun 2025 - Trump's first 100 days: a new economic regime takes shape

|

Trump's first 100 days: a new economic regime takes shape Nikko Asset Management May 2025 Tariffs bring global uncertaintyDonald Trump's second term in office has now passed the symbolic 100-day mark, and his most significant action this far was his announcement of global tariffs on 2 April. Trump's "Liberation Day" triggered a market sell-off in anticipation of a global supply shock, but after he subsequently announced a 90-day pause, global equity indices recovered, ending the month broadly where they began. The pause should give the US administration time to negotiate with its closest allies, but if no meaningful progress is made, particularly with countries like South Korea and Japan, by the end of May, it could signal a prolonged impasse. That would reinforce concerns that this is not simply a short-term negotiating tactic, but the beginning of a more entrenched trade rift. Therefore, while investors who avoided panic selling in April may have found themselves emerging relatively unscathed, the tariff shock continues to justify a higher risk premium across global equities. US economic concerns at the foreThis not the first time the world has faced a severe supply chain disruption. But unlike the pandemic, for example, the current shock is self-inflicted, driven by Trump's idiosyncratic approach to trade policy rather than external forces. We're already starting to see the effects ripple through the US economy. Logistics data shows a sharp drop in goods moving from China to the US. Container bookings are significantly lower than a year ago. The Port of Los Angeles, the main entry point for Chinese goods, expects arrivals in early May to be down by a third. Airfreight bookings are also falling. According to Vizion, container bookings for standard 20-foot boxes from China to the US were 45% lower year-on-year by mid-April. As John Denton of the International Chamber of Commerce noted, many businesses are delaying decisions while they wait to see whether the US and China can reach a deal. China-US relations remain keyAs discussed last year, Trump's approach to tariffs has been to target China most aggressively. But political headwinds may force him to take a more conciliatory approach than he would like. With mid-term elections in November 2026, the Republican Party needs a quick win with allies, ideally leading markets towards new highs before then. China's President Xi Jinping, of course, faces no such political pressure. The tariff strategy appears designed to create what economists might call a "separating equilibrium", pushing allies to side with the US in isolating China, while also testing China's response. Trump's approach leaves little room for Xi to save face, effectively forcing Beijing into tit-for-tat measures. That lack of an off-ramp increases the risk of a drawn-out standoff, with economic data releases ratcheting up the pressure. Looking ahead, we expect more anecdotal evidence of supply disruption to emerge by the end of May, followed by harder economic data shortly after. The potential inflationary effect is notable. Based on trade volumes of around USD 425 billion and tariff rates that could eventually settle around 50%, we estimate the direct impact on US inflation could be around 1 percentage point, assuming no offsetting effects. Depending on how much of the cost is absorbed by importers and exporters, the range could be anywhere from 30 to 70 basis points. In short, the trade war's economic effects are already becoming visible. The longer it persists, the greater the risk that it drags on US growth and complicates the Federal Reserve (Fed)'s task of managing inflation expectations. Threats to Federal Reserve impartiality: are Powell's days numbered?Early in his second term, Trump appeared to be testing the legal ground for removing the Fed Chair Jerome Powell before the end of his term, with suggestions he could do so without needing to show cause. Trump has recently softened his public stance on Powell, but questions remain over future Fed independence. At the heart of this issue is Wilkins v. United States, a Supreme Court case expected to be decided in June. The case could effectively challenge the precedent set by Humphrey's Executor in 1935, which limits a president's ability to remove the heads of independent agencies without cause. Should the Supreme Court side with the Trump administration, it could strip away key legal protections that shield the Fed Chair from political interference. Even if the court offers a more limited ruling, the legal precedent could still be weakened, clearing the way for greater executive control over independent agencies. In the most extreme outcome, Trump would have the authority to dismiss Powell, or any other agency head, at will. Such a move would undermine the institutional integrity of the Fed and draw comparisons to the erosion of central bank independence seen in countries like Turkey, where politically driven monetary policy has contributed to economic instability. Powell's current term ends in May 2026, and it is unlikely he will be reappointed, and his successor could be announced well before then. Trump will likely nominate a more dovish candidate willing to cut rates aggressively in support of his policy agenda. This puts the Fed in a difficult position. Even if political pressure builds to ease policy, the Fed must remain vigilant about the risk of re-accelerating inflation. A premature or politically motivated pivot could risk repeating the mistakes of the 1970s, when monetary policy missteps allowed inflation to spiral. For now, this uncertainty may push the Fed to maintain its current pause for longer, as it waits for greater clarity on both inflation and the political landscape. Has the tariff risk premium already been priced in?In fixed income markets, some degree of tariff-related risk premium has already been priced into the long end of the US rates curve. However, when comparing US long-term yields with those of other developed markets, the relative value is starting to look more compelling. Global bond market scepticism, often described as bond vigilantism, can only stretch so far. At a certain point, investors recognise they are being adequately compensated for bearing tariff-related inflation risks. When that happens, US long bonds may start to attract stronger demand, offering not just a yield premium but also a degree of protection in a potentially slower growth environment. With the European Central Bank moving onto an easing path, the spread between US and European long-end rates is likely to widen further in the near term. That divergence supports the case for US duration, especially as the risk premium embedded in Treasury yields becomes more attractive. Downward pressure on the dollarWhile credit markets also weakened during April, the more pressing concern is the US dollar. The dollar index fell to a three-year low in the month, and the currency is currently looking technically oversold, even when assessed relative to interest rate differentials. Fundamentally, there appears to be an incentive for the US to maintain a weaker dollar in order to reduce its export deficit. What we are seeing is the emergence of a new economic regime. Previously, foreign exchange moves were largely driven by interest rate differentials. But under Trump's policies, those drivers appear to be shifting. Trade dynamics and political strategy are taking a more central role in currency movements. In this new environment, we expect continued downward pressure on the dollar. Slowing economic data, which we anticipate will materialise soon, could reinforce this trend. We also believe that at its upcoming June meeting the Fed is more likely to ease policy, which the markets have currently priced in at only around 50%. Thoughts on volatilityThe start of April brought a spike in market volatility that unsettled many investors. In today's markets, risk premiums are priced in far more quickly than they were two decades ago, and we saw this in action with the volatility index (VIX) briefly surging above 50 following Liberation Day. Such levels are rare and typically short-lived. While similar spikes occurred during the Global Financial Crisis and the early days of pandemic, volatility above 50 historically tends not to persist. It creates an environment where selling volatility becomes attractive, quickly pulling the index back down. This pattern appears to be playing out again. The initial equity sell-off seemed to bottom shortly after the Liberation Day announcement, in a manner not dissimilar to the bottom reached in March 2020 at the onset of the pandemic. Back then, valuations fell to around 16 times forward earnings. This time, we've only seen multiples contract to roughly 19 times, and credit markets have experienced far less severe dislocation. While macro risks remain, current conditions do not yet point to a systemic crisis. From a market positioning perspective, the worst may now be behind us. What happens next largely depends on the pace and direction of trade negotiations, both with Washington's allies and, further down the line, China. Ultimately, we expect US-China tariffs to settle in the mid-double-digit range, depending on how far both sides are willing to compromise. Crucially, Trump will need to make at least a symbolic concession to allow Xi Jinping to save face. Without that, a sustainable off-ramp becomes much harder to achieve. For now, based on historical patterns and current valuations, we think it's likely the market has found a near-term bottom, unless trade tensions escalate significantly from here. In our view, now is an opportune time to consider an active global fixed income approach to navigate what is likely to be a prolonged period of uncertainty and for those seeking diversification. With bond yields and geopolitical risks remaining elevated, this environment presents unique opportunities in fixed income, particularly as markets adjust to lower inflation expectations. Funds operated by this manager: Nikko AM Global Share Fund , Nikko AM ARK Global Disruptive Innovation Fund , Nikko AM NZ Cash Fund , Nikko AM NZ Corporate Bond Fund , Nikko AM Core Equity Fund (NZ) , Nikko AM Global Shares Hedged Fund (NZ) , Nikko AM KiwiSaver Scheme Balanced Fund (NZ) , Nikko AM ARK Disruptive Innovation Fund (NZ)

Important disclaimer information Please note that much of the content which appears on this page is intended for the use of professional investors only. |

5 Jun 2025 - Is the idea of a sustainable Earth a farce?

|

Is the idea of a sustainable Earth a farce? Janus Henderson Investors May 2025 Viewing the Earth as an "island" with limited resources underscores the importance of evaluating the systemic risks of overconsumption, considering the environment in long-term investment strategies, and investing in firms committed to sustainable practices. When contemplating if a sustainable Earth is possible, utilising some fundamental concepts from science and economics provides an interesting perspective for insight into investment opportunities, starting first with the ecology concept of carrying capacity. Carrying capacity sets out to answer the question for a single species in a defined space: is there a maximum number of individuals for that species that can be supported by its surrounding environment? One of the most often cited examples is the moose population on Isle Royale. The island in Michigan, United States, is a designated wilderness environment that can only be accessed by boat. Analysis of the moose population shows that its size is directly connected to vegetation and predator levels of the island. The idea of environmental sustainability expands on this island view of carrying capacity by viewing the Earth, from outer space, as an island. Earth: an island in spaceViewing the Earth as an island then implies it has limited resources to support a maximum population. If that's the case, then one might wonder how life persists with limited resources available. This is best answered by considering a fundamental scientific principle - The Law of Conservation of Mass, which states that mass is neither created nor destroyed in a chemical reaction, only converted. Based on this principle, it means all matter needed to live on Earth must come from something on Earth. So, we must, therefore, recognise as a collective society that the Earth has a finite amount and fixed number of resources (e.g., mass) to share amongst all living things. These resources form a common-pool that everyone can use, but once consumed, they are unavailable for others. If resources are only taken from this pool and not replenished, they would eventually run out. However, Earth has natural recycling processes like the water cycle, carbon cycle, oxygen cycle, and other biogeochemical cycles that help make used resources reusable, although these processes require time to complete. On the surface, this makes it seem like sustainability is possible. For Earth to be sustainable, the rate of resource consumption must not exceed the rate at which they can be recycled. This balance is crucial for sustainability, but it becomes complicated by the 'Tragedy of the Commons'. This economic theory describes how individuals, if given unregulated access to a shared resource, tend to overuse it, depleting the resource at a rate faster than it can regenerate. A classic example is overgrazing of a village's common, shared grassland. If too many sheep were placed in the field by each villager resulting in the grass being eaten faster than it could grow back, it would ultimately result in a sheep population that could not be supported by the field. The 'Tragedy of the Commons' highlights that if a common resource is left unregulated then the potential for it to be overconsumed is highly likely. The challenge of sustainability, therefore, lies in finding ways to ensure that consumption of a common resource does not surpass Earth's or technological ability to recycle these resources, ensuring they are available for future use. The investment case for sustainabilitySo, what does viewing the Earth as an island with a common-pool of resources mean for an investor? Investors should:

A clear investment case emerges for companies thoughtfully considering the use and reuse of common-pool resources. Saint-Gobain, a global building materials company, aims to become the worldwide leader in light and sustainable construction. Operating in 76 countries with 160,000 employees and generating revenues close to €50 billion, the company is driven by its mission to "make the world a better home". It is particularly influential in the realm of low-cost homebuilding and renovation, addressing the needs of expanding populations. Saint-Gobain's integrated solutions offer numerous environmental and social advantages, such as enhancing energy efficiency, reducing embedded carbon, optimising the use of natural resources, and improving the thermal, acoustic, and safety features of homes, all while maintaining affordability. In the context of circularity, the construction industry is notorious for its substantial environmental footprint, responsible for 40% of solid waste and nearly 50% of natural resource consumption. Saint-Gobain is actively working to mitigate these impacts with several initiatives aimed at enhancing sustainability. The company has adapted its factories and manufacturing processes to utilise recycled inputs and collaborates with governments to improve the collection of recycled materials. A significant portion of its products, including plasterboard, glass wool, and flat glass, are infinitely recyclable, reinforcing its commitment to sustainable practices. Saint-Gobain not only adheres to best practices in the building materials sector but also gains a competitive edge as sustainability becomes a more integral factor in consumer decisions. The company has noted a rising customer interest in Environmental Product Declarations (EPDs). Utilising EPDs, which rely on Life Cycle Analysis, Saint-Gobain can benchmark its products against competitors and establish itself as a leader in sustainable construction. By issuing EPDs, Saint-Gobain Glass supports clients such as architects, engineering firms, and general contractors who aim to secure building certifications like Leadership in Energy and Environmental Design (LEED), Building Research Establishment Environmental Assessment Method (BREEAM), Deutsche Gesellschaft für Nachhaltiges Bauen (DGNB), among others. With an eye to the future, Saint-Gobain is also designing its products and construction solutions to be easily separated in the event of deconstruction. It has a 2030 target to reduce non-recoverable waste by 80% and reduce virgin material consumption by 30%, and currently more than 50% of sales are generated by products covered by verified life-cycle assessments and environmental product declarations with a 2030 target of 100%.1 This forward-thinking approach not only enhances its investment appeal but also solidifies its role in promoting sustainable practices in high-impact sectors like construction. This is exactly the type of strategy that we look for in companies that we consider having strong investment appeal. We find that companies that solidify their role in promoting sustainable practices have strong, long-term potential to deliver financially material advantages to investors. |

|

Funds operated by this manager: Janus Henderson Australian Fixed Interest Fund , Janus Henderson Conservative Fixed Interest Fund , Janus Henderson Diversified Credit Fund , Janus Henderson Global Natural Resources Fund , Janus Henderson Tactical Income Fund , Janus Henderson Australian Fixed Interest Fund - Institutional , Janus Henderson Conservative Fixed Interest Fund - Institutional , Janus Henderson Cash Fund - Institutional , Janus Henderson Global Multi-Strategy Fund , Janus Henderson Global Sustainable Equity Fund , Janus Henderson Sustainable Credit Fund Definitions and footnotes BREEAM (Building Research Establishment Environmental Assessment Method) is a widely used sustainability assessment method for buildings and infrastructure, designed to improve environmental performance and promote sustainable practices. It evaluates buildings across various criteria, including energy, water, materials, waste, and more, to achieve a holistic approach to sustainability. Carrying capacity is defined as the maximum number of individuals from a particular species that an environment can support indefinitely without harming its natural resources and ecosystem functions over time. This principle is commonly applied in ecological studies to determine the sustainable population limit of an environment, ensuring that ecological harm or resource exhaustion is avoided. Common-pool resources are resources that are available to everyone in a community or society but are finite in quantity. These resources are difficult to restrict access to, and their use by one person diminishes their availability to others. Examples of common-pool resources include fisheries, forests, groundwater reserves, and pasturelands. Effective management and preservation of these resources are crucial to avoid overexploitation, which is often referred to as the Tragedy of the Commons. This requires diligent regulation to avert excessive use and subsequent depletion. DGNB (Deutsche Gesellschaft für Nachhaltiges Bauen), which translates to the German Sustainable Building Council, is a non-profit organisation that promotes and certifies sustainable buildings and urban districts in Germany and internationally. The DGNB system evaluates buildings based on their environmental, economic, and sociocultural impact throughout their lifecycle, from planning to demolition. LEED (Leadership in Energy and Environmental Design) is a globally recognised green building rating system developed by the U.S. Green Building Council (USGBC). It provides a framework for designing, constructing, and operating buildings that are more environmentally responsible, energy-efficient, and healthy. LEED certification is awarded based on a project's performance across various categories like water efficiency, energy use, and indoor environmental quality. Life Cycle Analysis (LCA): This approach assesses the ecological effects of a product or service from the beginning of its life, starting with the extraction of raw materials, through to its ultimate disposal. It enables companies to comprehend the environmental consequences of their operations and make choices that minimise detrimental effects. 1Source: Stain-Gobain, 'Our Actions and Targets - Sustainability' All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect. The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested. Whilst Janus Henderson believe that the information is correct at the date of publication, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson to any end users for any action taken on the basis of this information. |

4 Jun 2025 - Instant Everything: The New Retail Revolution

3 Jun 2025 - Sports Investment: The New Frontier of Alternative Assets

Sports Investment: The New Frontier of Alternative AssetsAltor Capital May 2025 |

|

In an era where traditional investment vehicles are increasingly scrutinised for their volatility and limited returns, alternative assets have emerged as compelling diversification options for sophisticated investors seeking uncorrelated returns. Among these alternatives, sports franchises demonstrate remarkable potential for significant value appreciation and revenue generation that can outpace traditional market returns. Recent developments in the football world highlight this trend, with two particularly illuminating examples: Liverpool FC's commercial ascension and Wrexham AFC's meteoric valuation rise under celebrity ownership. The Liverpool Model: Commercial Excellence Driving Financial GrowthLiverpool Football Club has established itself as a masterclass in commercial strategy execution within the sports industry. According to the club's official announcement, Liverpool's commercial revenue has surged by an impressive 23% to £272 million for the 2022-23 season, propelling them past rivals Manchester United for the first time in Premier League history. This achievement reflects several key investment factors:

For investors, Liverpool represents the potential of established tier-one sports assets when operated with commercial excellence. The club's ability to grow revenues even during challenging economic periods underscores sports franchises' resilience as investment vehicles. The Wrexham Phenomenon: Value Creation Through StorytellingOn the opposite end of the spectrum, Wrexham AFC provides a fascinating case study in rapid value creation through innovative approaches to sports ownership. When Hollywood stars Ryan Reynolds and Rob McElhenney purchased the struggling fifth-tier club in November 2020 for approximately £2 million, few anticipated the extraordinary transformation that would follow. Industry analysis suggests the club could now be valued at nearly £300 million--a staggering 15,000% increase in just over four years. This remarkable appreciation stems from:

The Wrexham case illustrates the extraordinary potential for value creation in "undervalued" sports properties when combined with innovative marketing, content creation, and authentic storytelling. Key Investment Insights for Sports ConsiderationFor sophisticated investors and their financial advisors considering sports franchise investment as an alternative asset class, several key principles emerge from these case studies:

Our Approach to Sports Investment OpportunitiesWe recognise that sports investments represent a unique alternative asset class that combines exceptional financial return potential with prestige ownership and community impact. Our approach is built on three decades of experience navigating complex alternative markets:

Conclusion: The Evolving Investment Thesis for High Net Worth PortfoliosThe contrasting examples of Liverpool and Wrexham illustrate the breadth of opportunity within sports franchise investment. Whether through operational excellence at established clubs or transformational vision at undervalued properties, the potential for significant returns exists across the spectrum. For high-net-worth investors and family offices seeking genuinely differentiated return drivers, sports franchises offer a compelling alternative--one built on passionate fan engagement, diverse revenue streams, and the universal appeal of athletic competition. As traditional markets face continued uncertainty and higher correlations across conventional asset classes, sports franchises represent not just a diversification play but potentially a cornerstone of future portfolio growth for sophisticated investors. For financial advisors, introducing appropriately structured sports franchise investments to suitable clients can demonstrate value beyond traditional portfolio construction while potentially enhancing long-term returns. Funds operated by this manager: Altor AltFi Income Fund, Altor Emerging Growth Fund |

2 Jun 2025 - The big issues for investors coming out of Washington

|

The big issues for investors coming out of Washington Magellan Asset Management May 2025 |

|

The first 100 days of the second Trump administration have certainly been interesting for investors. And as the initial global tariff shock appears to be winding back, it's a good time to draw on the thoughts and the insights of a Washington insider. National Security Expert Michael Allen, who was a Special Assistant to former President George W. Bush shares his thoughts in a wide-ranging interview. Magellan Head of Global Equities and Portfolio Manager Arvid Streimann talks with Michael about tariffs, the US government deficit, the Democrats, the US's technological lead over China and the Chinese military buildup. |

|

Funds operated by this manager: Magellan Global Fund (Hedged), Magellan Core Infrastructure Fund, Magellan Global Fund (Open Class Units) ASX:MGOC, Magellan High Conviction Fund, Magellan Infrastructure Fund, Magellan Infrastructure Fund (Unhedged) Important Information: Copyright 2025 All rights reserved. Units in the funds referred to in this podcast are issued by Magellan Asset Management Limited ABN 31 120 593 946, AFS Licence No. 304 301 ('Magellan'). This material has been delivered to you by Magellan and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision about whether to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to a Magellan financial product may be obtained by calling +61 2 9235 4888 or by visiting www.magellangroup.com.au. The opinions expressed in this material are as of the date of publication and are subject to change. The information and opinions contained in this material are not guaranteed as to accuracy or completeness. Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward looking' statements and no guarantee is made that any forecasts or predictions made will materialise. No representation or warranty is made with respect to the accuracy or completeness of any of the information contained in this material. Magellan will not be responsible or liable for any losses arising from your use or reliance upon any part of the information contained in this material. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Magellan. Further important information regarding this podcast can be found on the Insights page on our website, www.magellangroup.com.au. |