NEWS

Performance Report: Insync Global Quality Equity Fund

The Insync Global Quality Equity Fund has returned +12.43% per annum since its inception in October 2009, an outperformance of +0.24% relative to the All Countries World (AUD) benchmark which has returned +12.19% on an annualised basis...

Read more...

Performance Report: Cyan C3G Fund

The Cyan C3G Fund rose by +0.09% in November, outperforming the ASX Small Ordinaries Total Return benchmark by +1.57%. Over the past 12 months, the fund rose by +26.85%, an outperformance of +7.42%, compared with the benchmark, which has...

Read more...

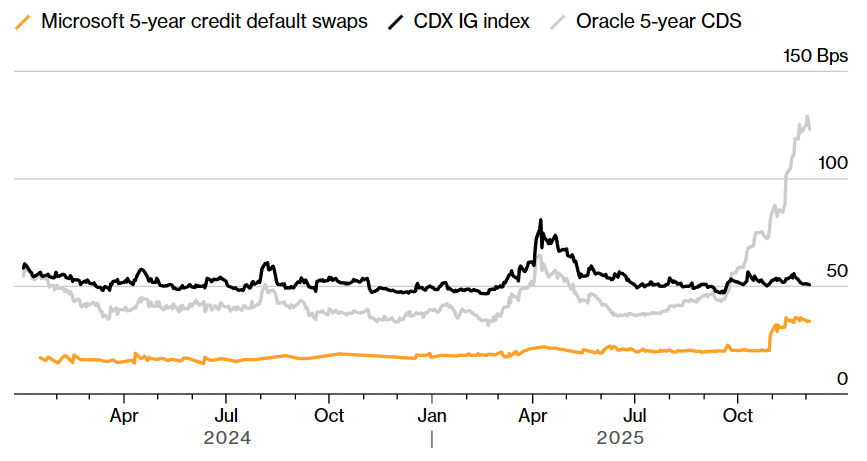

AI's debt binge draws European telco parallels

In 2025, 'hyperscalers' including Amazon, Google, Meta and Microsoft are fuelling an unprecedented surge in equity and debt issuance to bankroll massive AI-driven capital expenditure. While their credit ratings remain pristine today,...

Read more...

Performance Report: Argonaut Natural Resources Fund

The Argonaut Natural Resources Fund rose by +0.90% in November. Since its inception in January 2020, the fund has returned +28.57% per annum, an outperformance of +18.30% relative to the S&P/ASX 300 Resources TR benchmark which has...

Read more...

Performance Report: Glenmore Australian Equities Fund

The Glenmore Australian Equities Fund has returned +18.70% per annum since its inception in June 2017, an outperformance of +9.65% relative to theASX 200 Total Return benchmark which has returned +9.05% on an annualised basis over the same period.

Read more...

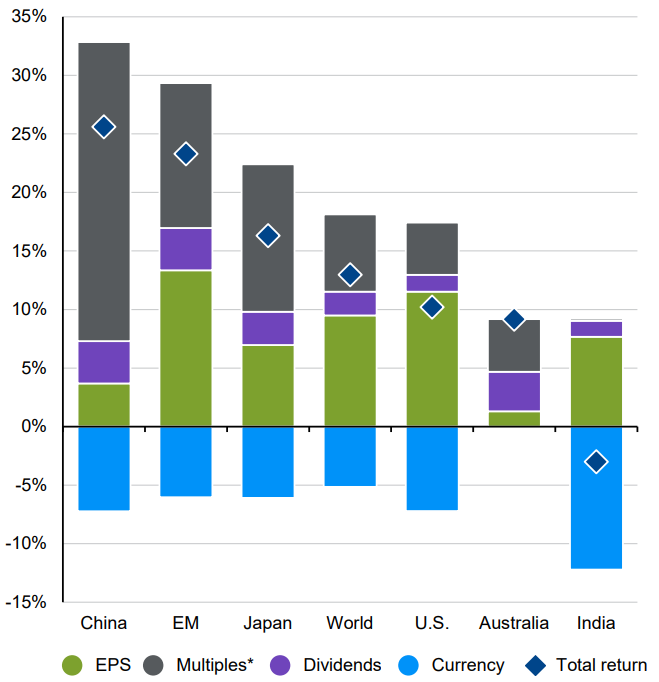

10k Words | December 2025

There is a chasm in the return drivers of Australian equities v. US equities in CY2025. Large cap (ASX 200) EPS has been soft (and there has been few new ASX listings to spur growth on). (2-minute read)

Read more...

Performance Report: Insync Global Capital Aware Fund

The Insync Global Capital Aware Fund rose by +4.79% over the past 12 months. In November, the fund saw strong contributions from Alphabet, while Tencent detracted, and Insync maintains a constructive outlook as global equities continue to...

Read more...

Performance Report: Bennelong Twenty20 Australian Equities Fund

The Bennelong Twenty20 Australian Equities Fund has returned +9.11% per annum since its inception in November 2009, an outperformance of +0.80% relative to the ASX 200 Total Return benchmark which has returned +8.31% on an annualised basis...

Read more...

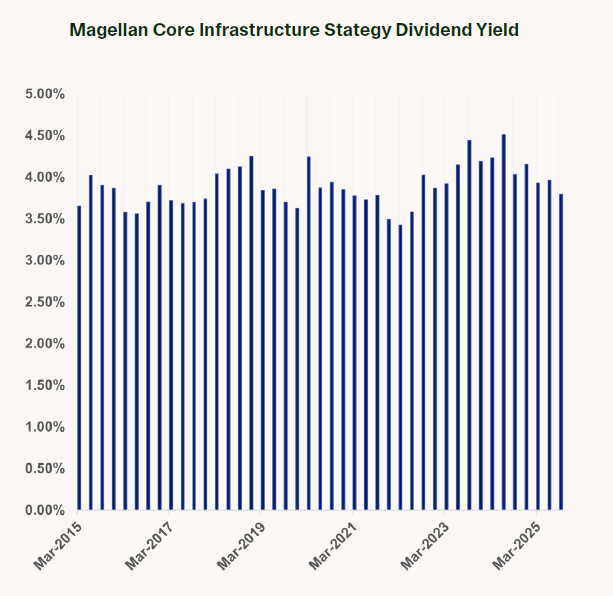

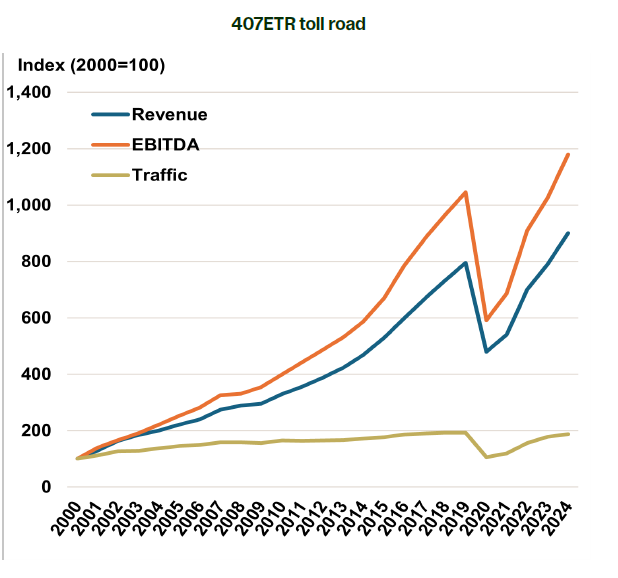

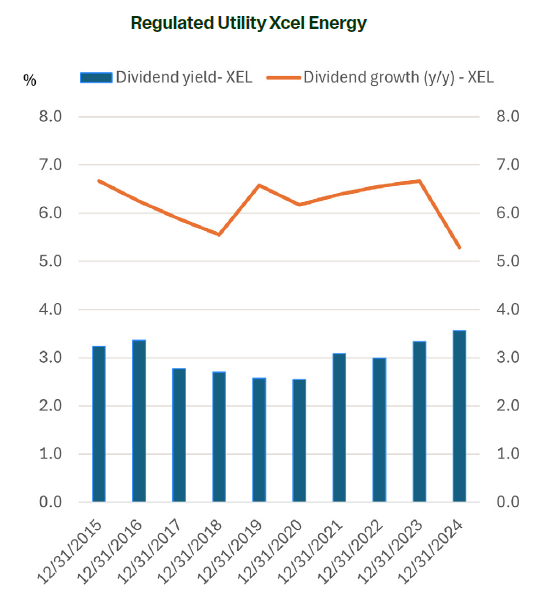

What investors should expect when investing in infrastructure: yield

Dependable earnings growth is a core characteristic of the high-quality listed infrastructure companies in which we invest. Throughout past cycles, we have seen consistent, solid returns. (10-minute read)

Read more...

Performance Report: Altor AltFi Income Fund

The Altor AltFi Income Fund rose by +0.80% in November, outperforming the RBA Cash Rate + 5% benchmark by +0.11%. Since inception in April 2018, the fund has returned +11.43% per annum, an outperformance of +4.38% relative to the benchmark...

Read more...