NEWS

Why collaborating is key to climate change

Collective action is essential for addressing global challenges like climate change, food security, and pandemic risks.

Read more...

Performance Report: Bennelong Twenty20 Australian Equities Fund

The Bennelong Twenty20 Australian Equities Fund has returned +9.04% per annum since its inception in November 2009, an outperformance of +0.69% relative to the ASX 200 Total Return benchmark which has returned +8.35% on an annualised basis...

Read more...

Performance Report: Argonaut Global Gold Fund

The Argonaut Global Gold Fund rose by +10.18% in December, outperforming the S&P Global Natural Resources AUD (TR) benchmark by +8.73%. Since inception in November 2022, the fund has returned +39.15% per annum, an outperformance of +31.48%...

Read more...

Performance Report: Bennelong Long Short Equity Fund

The Bennelong Long Short Equity Fund has returned +11.59% per annum since its inception in February 2002, an outperformance of +3.22% relative to the ASX 200 Total Return benchmark which has returned +8.37% on an annualised basis over the...

Read more...

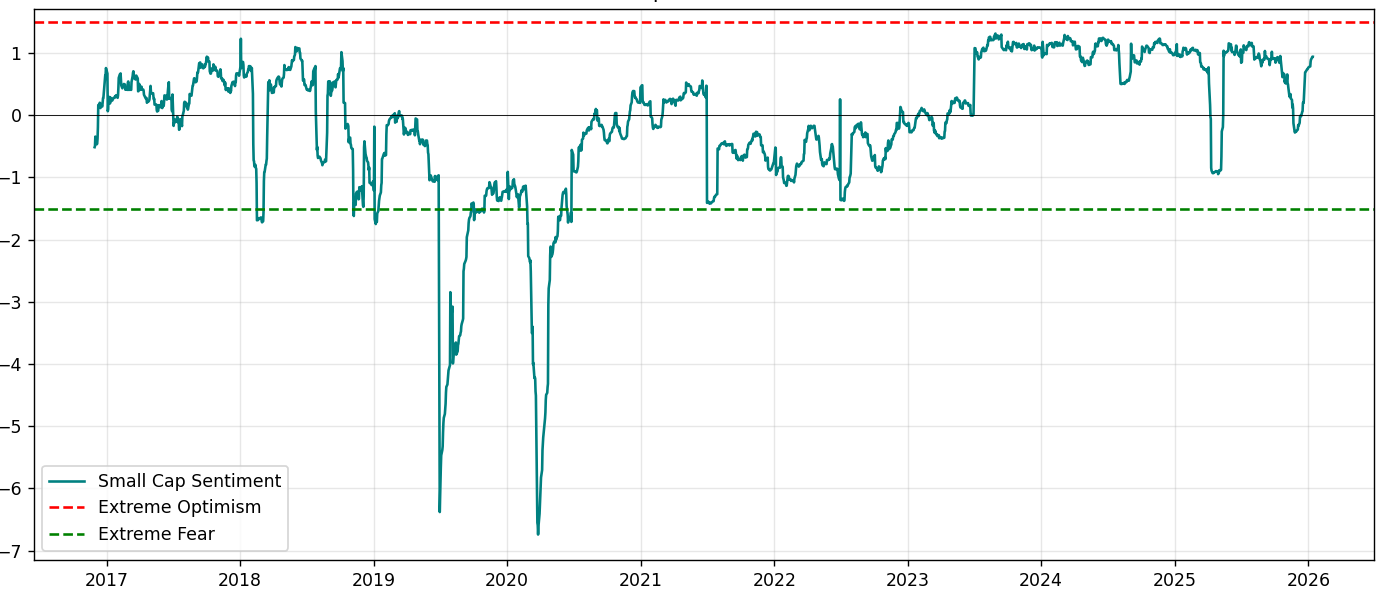

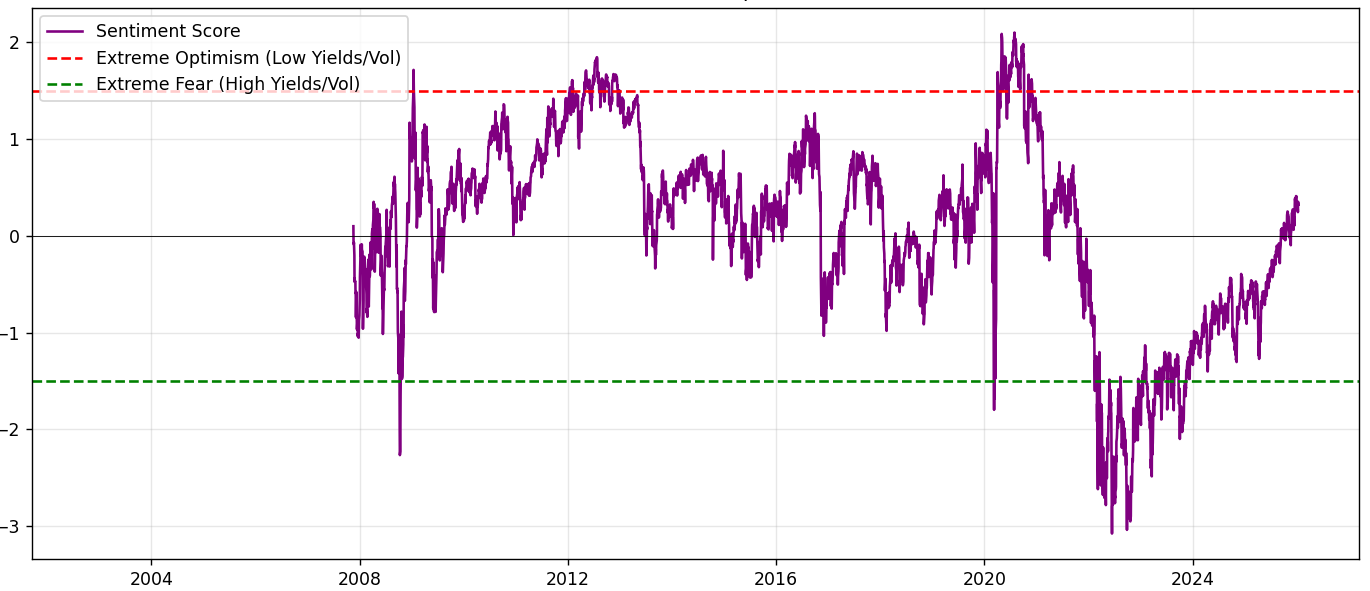

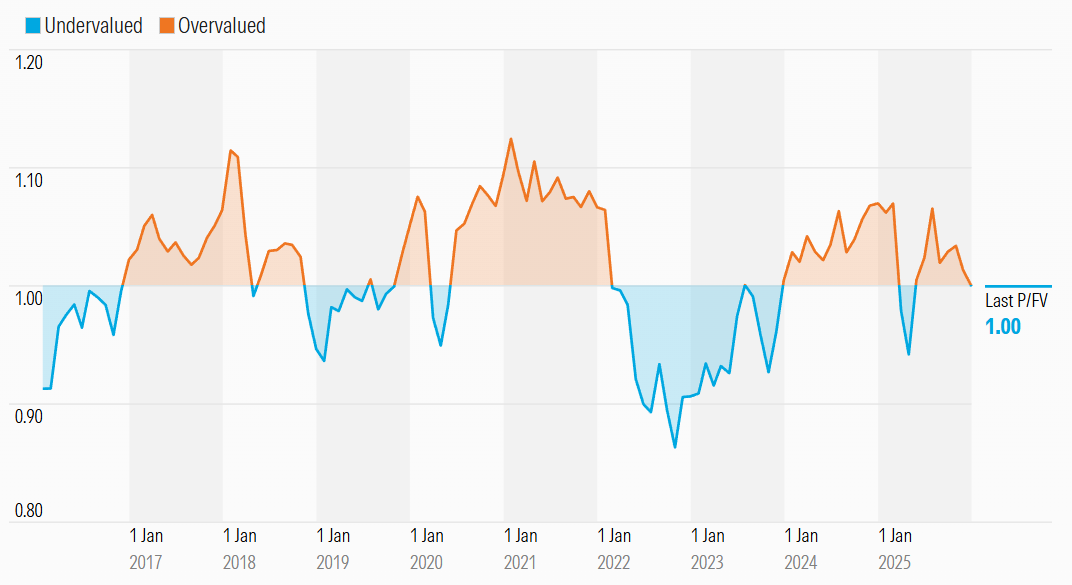

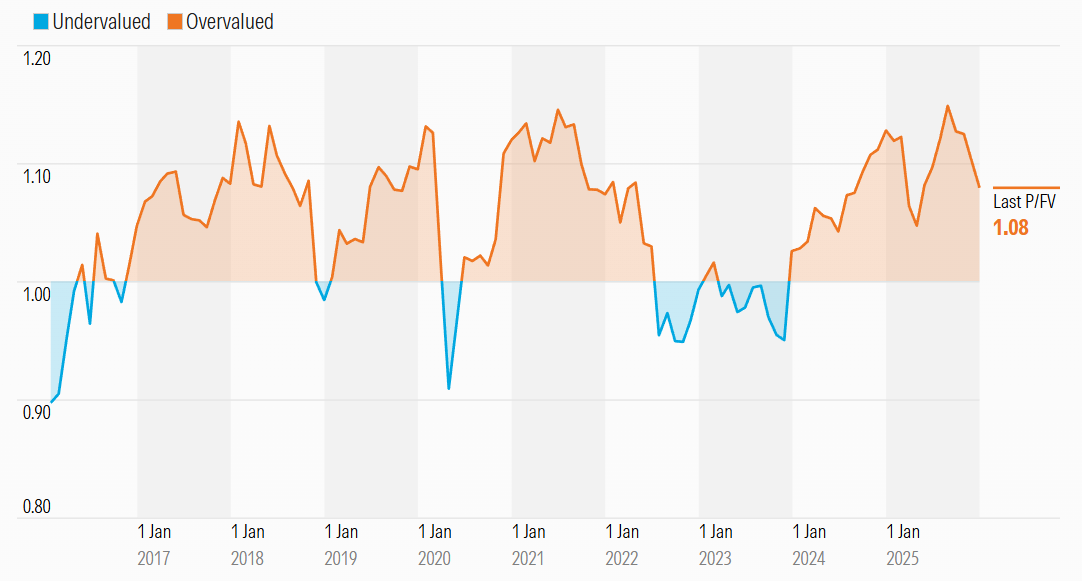

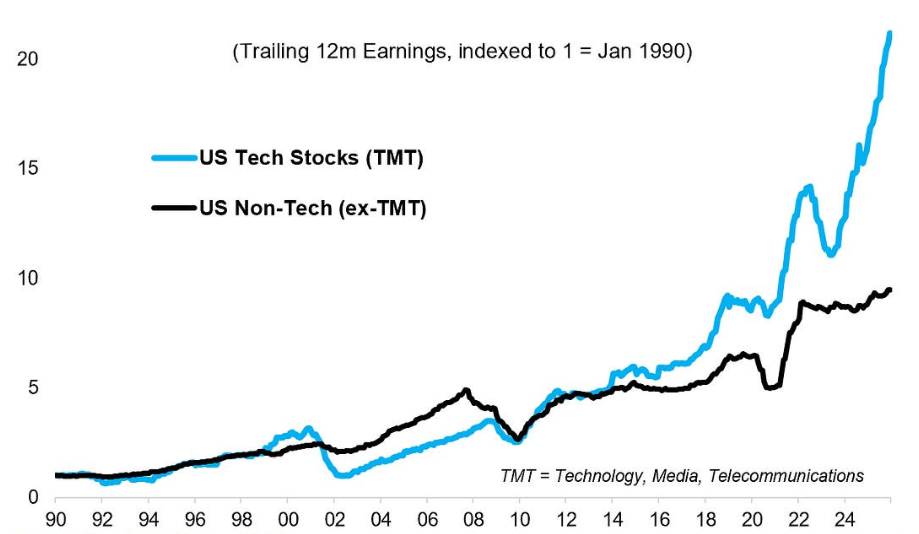

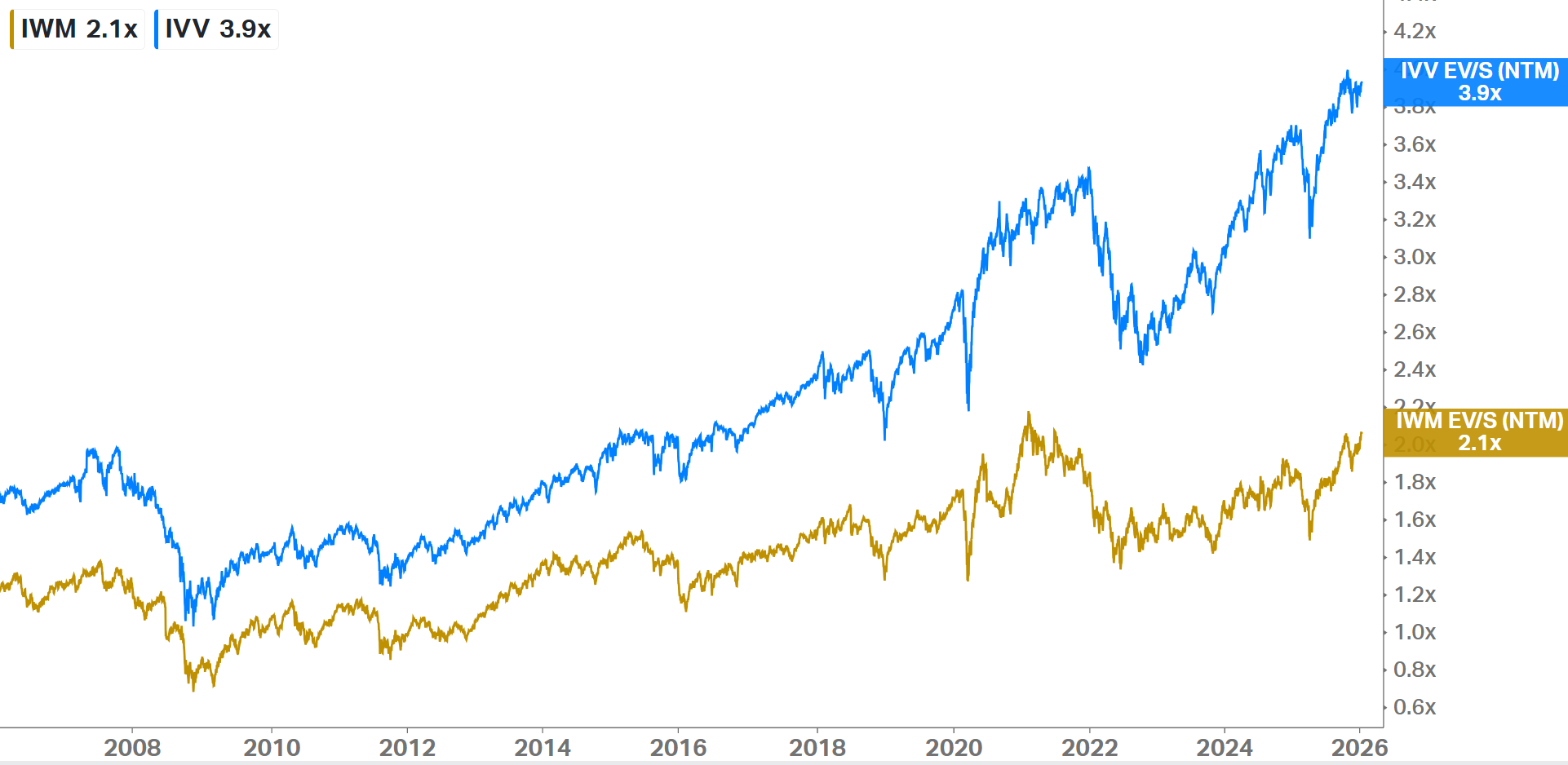

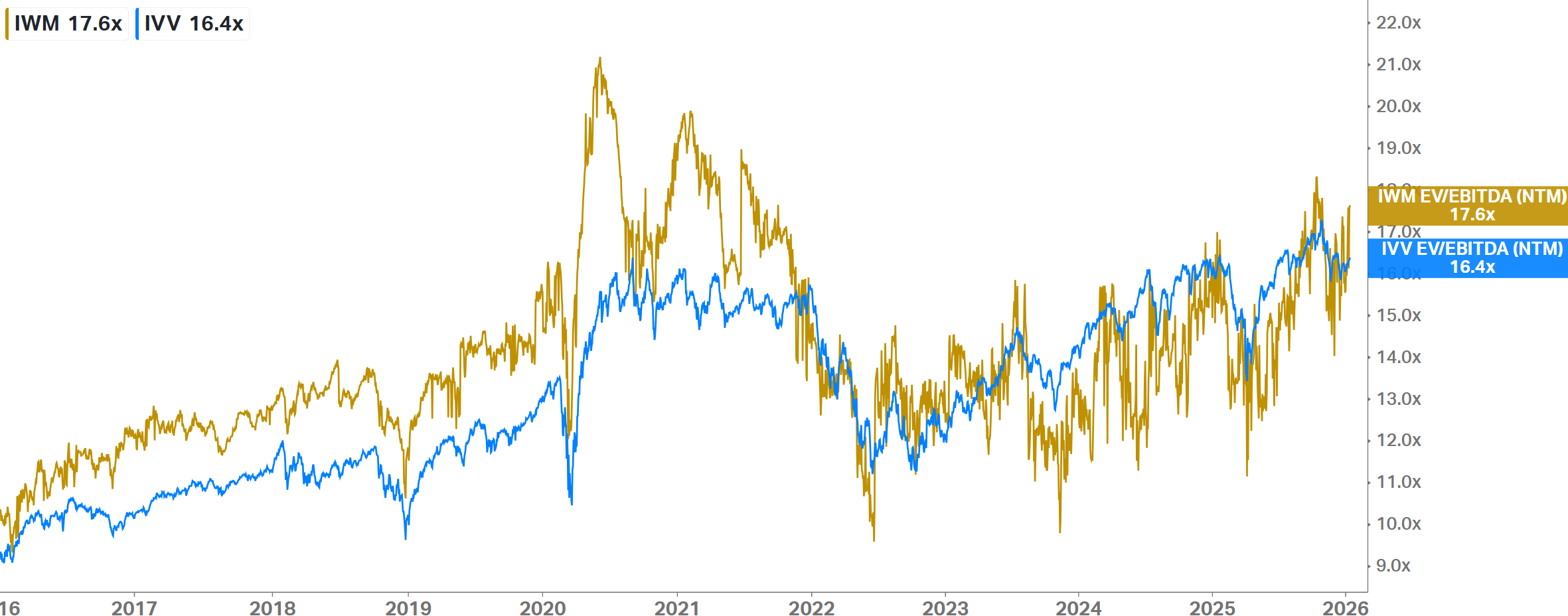

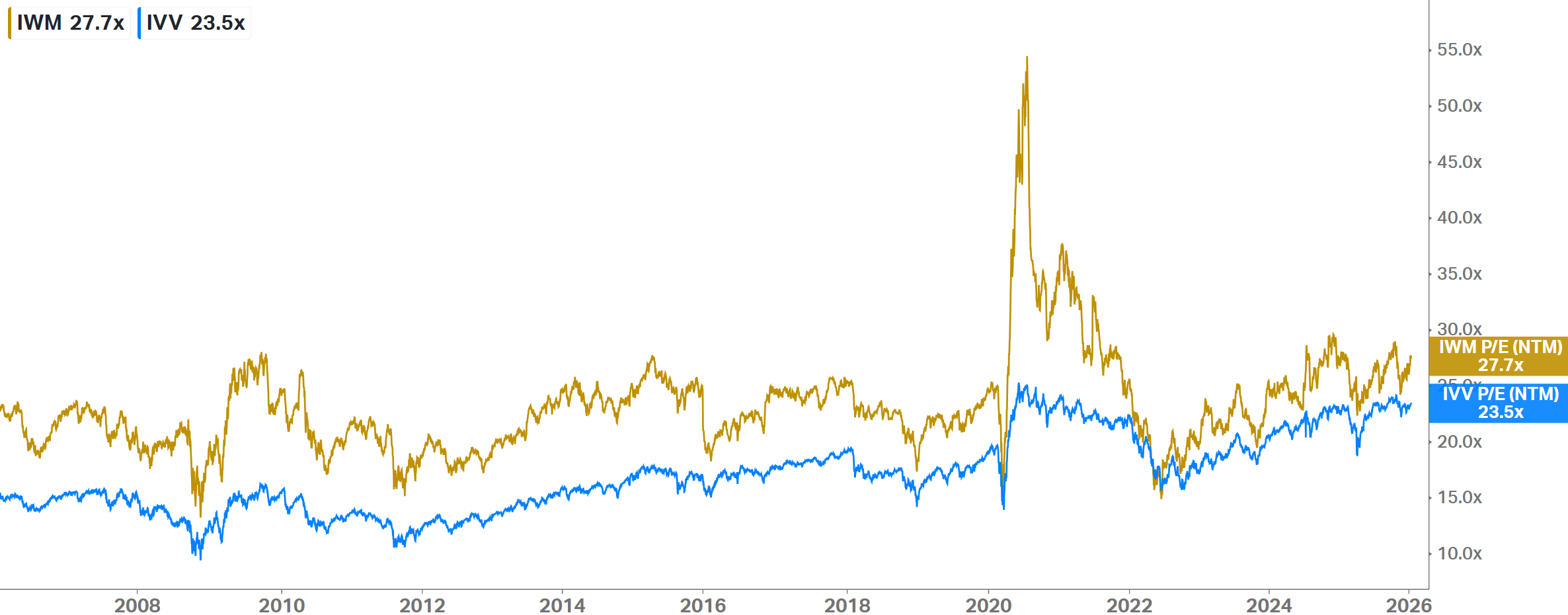

10k Words | January 2026

We kick off calendar 2026 by trying our hand at our own sentiment indicators - combining valuation and implied volatility for the US equity and bond markets, the Aus equity market and ASX small caps. (2-minute read)

Read more...

Hedge Clippings |16 January 2026

Looking forward, Looking back, Welcome back!

In 2025, there were a number of major themes that dominated markets and the news, and which in turn influenced returns of the various peer groups and the managed funds operating within them.

In 2025, there were a number of major themes that dominated markets and the news, and which in turn influenced returns of the various peer groups and the managed funds operating within them.

Read more...

Performance Report: Airlie Australian Share Fund

The Airlie Australian Share Fund rose by +0.91% in December. Since inception in June 2018, the fund has returned +9.31% per annum, an outperformance of +0.26% relative to the ASX 200 Total Return benchmark which has returned +9.05% on an...

Read more...

Performance Report: Bennelong Emerging Companies Fund

The Bennelong Emerging Companies Fund has returned +18.69% per annum since its inception in November 2017, an outperformance of +9.72% relative to the ASX 200 Return benchmark which has returned +8.97% on an annualised basis over the same period.

Read more...

Performance Report: Glenmore Australian Equities Fund

The Glenmore Australian Equities Fund has returned +18.42% per annum since its inception in June 2017, an outperformance of +9.30% relative to the ASX 200 Total Return benchmark which has returned +9.12% on an annualised basis over the same period.

Read more...

Performance Report: Bennelong Concentrated Australian Equities Fund

The Bennelong Concentrated Australian Equities Fund has returned +10.71% per annum since its inception in February 2009, an outperformance of +0.75% relative to the ASX 200 Total Return benchmark, which has returned +9.96% on an annualised...

Read more...