NEWS

19 Feb 2026 - Volatility providing fertile ground in active credit

|

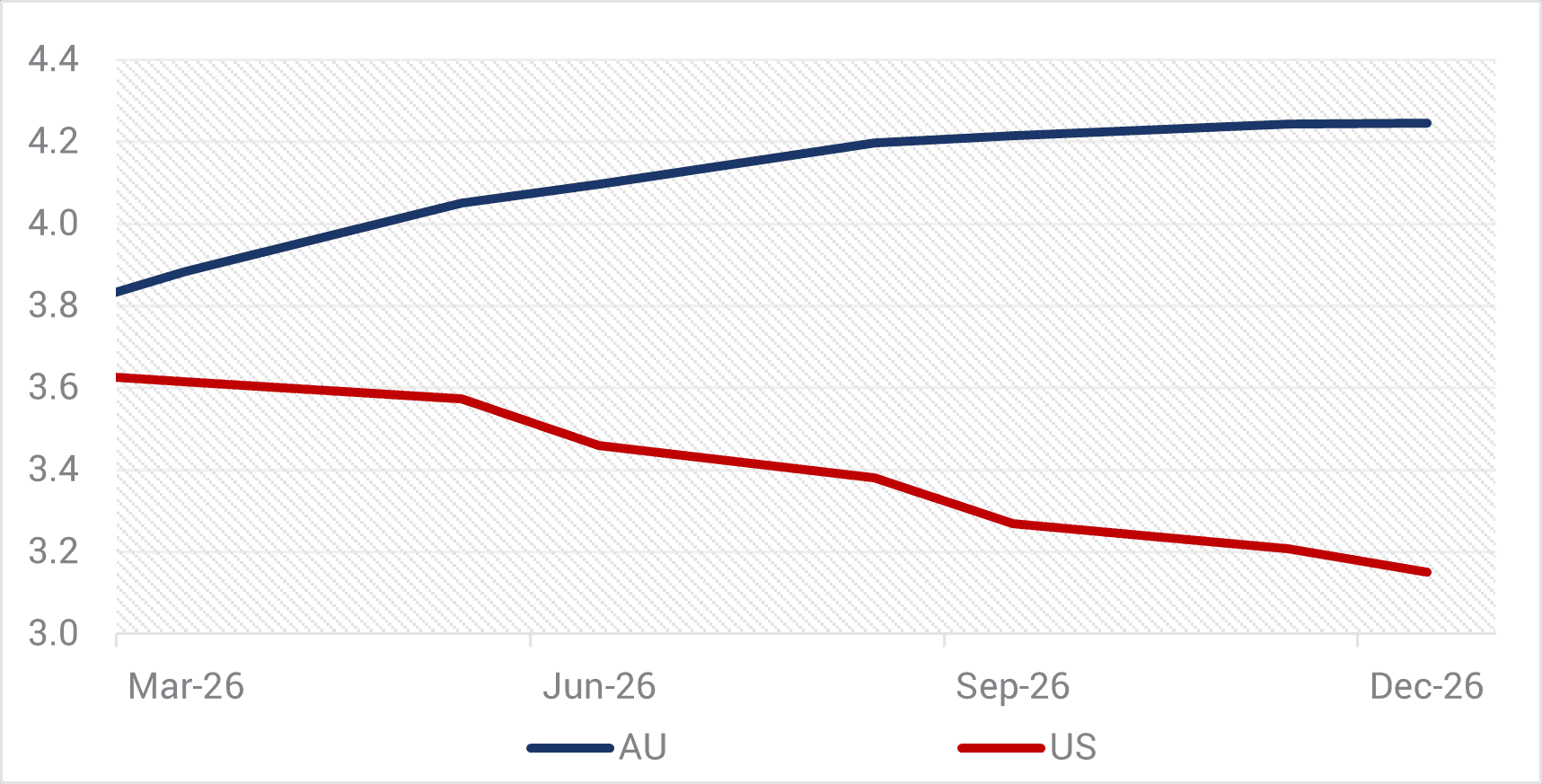

Phil Strano: Volatility providing fertile ground in active credit Yarra Capital Management February 2026 In this instance, the direction change is Australia's late 2025 bond selloff, culminating in a 25bp hike from the RBA this week and with the prospect of more hikes through 2026. Looking forward, current market pricing for 2026 shows a widening gap between the RBA cash rate and the FED funds rate, with the pricing of rate hikes in Australia in stark contrast to the US where easing appears virtually certain (refer Chart 1). Chart 1: Cash Rate Futures - US and Australia (%)

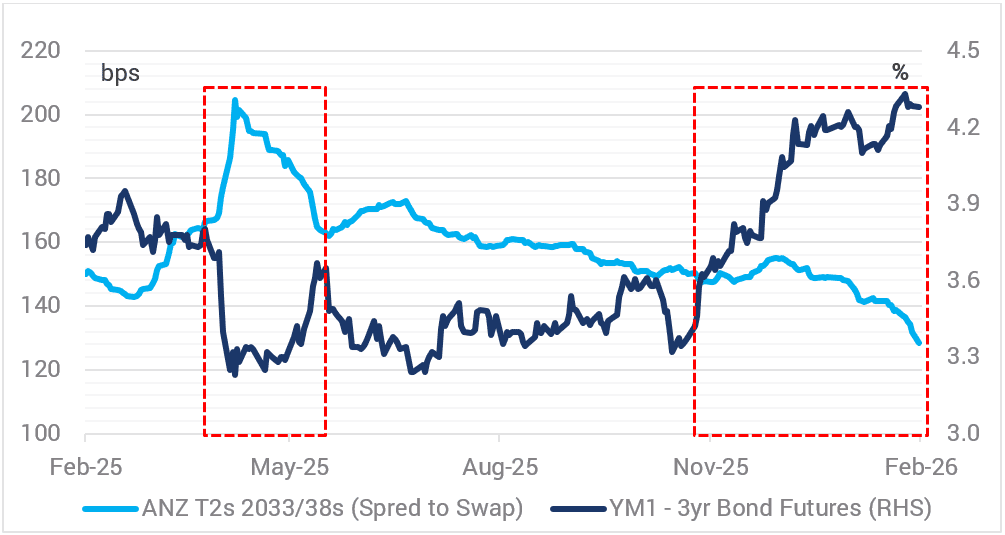

Source: Bloomberg, Yarra Capital Management Feb 2026.While the year ahead can pan out differently since actual movements in interest rates in some instances can bear little resemblance to the futures market at any point in time, pricing is always eventually reflected in security valuations across Australian credit and thus impacts investment decisions. For us, higher bond yields in the closing months of 2025 enabled a rebuild of strategic duration at ~1.7 years across both our Enhanced Income and Higher Income strategies. While market timing is never perfect, this duration positioning - where we have a skew to the front end - should help limit any drawdowns from risk offs in 2026. This period reminds us of April 2025, where both strategies generated positive performance despite credit spreads moving materially wider. We believe a similar scenario can play out in 2026 (refer Chart 2). Chart 2: Australian 3-year Interest Rates and ANZ 2033/38 T2 Credit Spreads

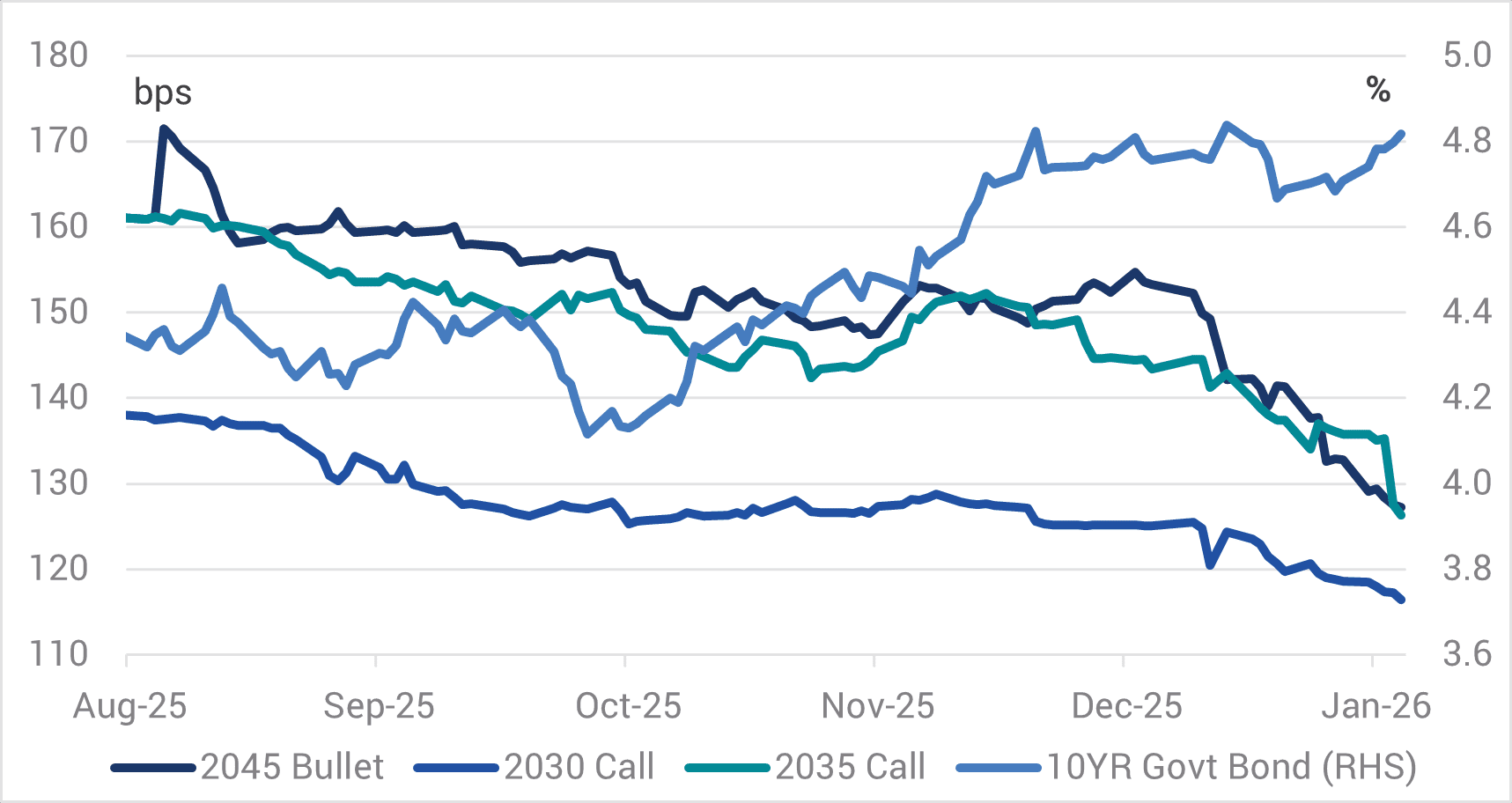

Source: Bloomberg, Yarra Capital Management Feb 2026.Another key theme through 2025 was the 6%+ "mania" which appears to be back with gusto. A pool of investors attracted to higher outright yields, especially longer dated major bank T2s, appear to be forgoing adequate credit spread compensation and happily accepting higher spread and interest rate duration risk to achieve their 6%+ yield objectives. Our analysis of the ANZ T2 credit curve illustrates the poor credit spread compensation that is currently on offer for the longer dated 2035 (call) and 2045 (bullet) maturities (refer Chart 3). Chart 3: ANZ T2 $A Securities Credit Spreads and Government Bond 10-year Yields

Source: Yarra Capital Management Feb 2026.Unsurprisingly, the significant contraction in the credit spreads on longer dated T2s is closely correlated with the rise in government bond yields and ANZ's T2 credit curve, as with the other major banks, is unattractively flat. We have taken this opportunity to rotate out of these longer-dated T2s given the inadequate spread compensation, preferring instead to be invested in shorter dated T2s such as the 2030s which are paying comparable credit spreads but with much less risk. While we are rotating out of longer-dated T2s, we remain comfortable investing in longer dated securities provided the credit spread compensation is commensurate to the risk assumed. In early February, we invested in the 5 and 10-year BBB rated Aroundtown bonds. While these securities are more off Broadway than the major bank T2s, the 10-year securities priced at an attractive 200bps credit spread and a yield of 6.72%. This deal provided ~70bps additional compensation for two notches lower credit quality (i.e. approximately double the normal compensation over A- rated major bank T2s). |

|

Funds operated by this manager: Yarra Australian Bond Fund , Yarra Australian Equities Fund , Yarra Emerging Leaders Fund , Yarra Income Plus Fund , Yarra Enhanced Income Fund , Yarra Australian Smaller Companies Fund , Yarra Ex-20 Australian Equities Fund , Yarra Global Small Companies Fund , Yarra Higher Income Fund |

18 Feb 2026 - Performance Report: DS Capital Growth Fund

[Current Manager Report if available]

18 Feb 2026 - Australian economic view - February 2026

|

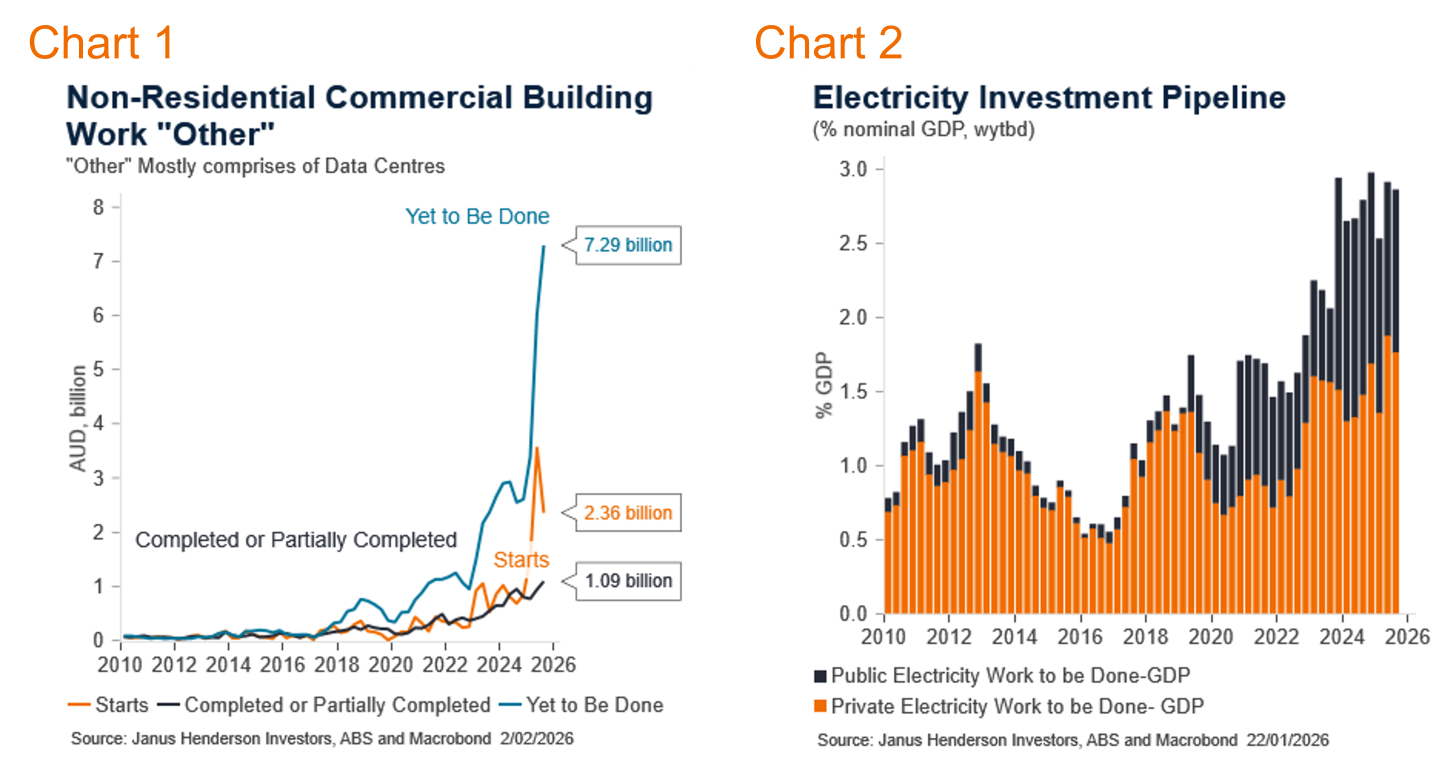

Australian economic view - February 2026 Janus Henderson Investors February 2026 (7-minute read) Market reviewSolid domestic data contributed to reinforcing near term lift in yields. The Australian bond market, as measured by the Bloomberg AusBond Composite 0+ Yr Index, rose 0.21%. The Reserve Bank of Australia (RBA) did not meet in January, therefore the cash rate remained at 3.60%. Three-month bank bills rose 10 basis points (bps) to 3.84% by month end. Six-month bank bill yields fell 3bps to 4.09%. Australia's three-year government bond yields ended the month 13bps higher, at 4.27%, 10-year government bond yields were 7bps higher at 4.81%. January was an extraordinary month in terms of global, geopolitical events and central bank uncertainty. From the US demanding Greenland, to ousting the Venezuelan leader, and instigating a criminal probe into Federal Reserve Chair Powell. What is more remarkable is the market's mostly benign response to the newsflow. Amid a general level of uncertainty, demand for assets continues to outweigh any potential global blowback. Peripheral markets are showing the impacts, volatility in gold and silver prices and a weakening US dollar are key indicators of that unease. While these broad events are ongoing, providing a backdrop to the domestic market, at this point, they are not driving them. The local economy shows elevated inflation, with the RBA's main measure, the trimmed mean quarterly series, at 3.4%yoy. The new monthly headline series remains at 3.8%. A series of administrative prices and one-offs have driven the headlines. Underlying this is steadying energy and rent prices, proving some degree of comfort ahead. The labour market remains highly volatile, with large changes month-to-month. The unemployment rate has dropped to 4.1%, but employment growth is low. Consumer confidence has dropped on the prospect of higher interest rate increases, while major city house prices are similarly subdued. A case for RBA hikes can be made this year. The upcoming artificial intelligence (AI) related capital expenditure cycle is expected to contribute significantly to demand and come up against supply constraints. Much of this comes in H2 and beyond. Initially, the household sector remains sensitive but should stabilise. Risk markets continued their solid momentum into 2026. Domestically, corporate and structured credit primary markets opened strongly with a range of issuers issuing bonds. Against a broadly constructive background for credit, the Australian iTraxx Index closed 2bps wider at 66bps, while the Australian fixed and floating rate credit indices returned +0.32% and +0.46% respectively. Market outlookWe have updated our RBA base case, looking for a series of hikes through 2026, into 2027. While our hikes are later than current market pricing, they move higher than that priced into 2027. Our high case is one where inflation remains elevated and the RBA are forced to raise interest rates more than expected in H1 2026, continuing higher through the year and into 2027. This has a 10% weight. Our low case reflects a weaker economic outcome, if global uncertainties are renewed and the labour market deteriorates. We hold a modest long duration position, targeted on the curve, and remain vigilant to take advantage of market mispricing. Monthly focus - Make way for AI InvestmentThe AI investment boom is upon us, we knew it was coming but the third quarter of 2025 showed that its appearance was perhaps sooner than expected. The trajectory is by no means guaranteed. There is a desire by policy makers, and players alike, to facilitate progress but some perspective on quantum, and constraints, provide a useful guideline to the path ahead. The AI sector influence on the economy initially shows up in investment. The productivity enhancements come later. Australia is seen as having a comparative advantage in terms of global geopolitics, economic conditions and availability of renewable energy sources. Given this, it is reported that the build and placement of data centres (DC) in Australia is higher than in comparative countries. Australia will benefit from setting up DC in Australia that service both local and non-Australian clients. The rise in DC building has been dramatic. This captured economist's attention in the third quarter data set, surging ahead. To Q3 2025, per quarter, actual building steadily rose at A$1.1bn, starts have surged to A$2.4bn but all eyes on the work yet to be done (WYTBD) at A$7.3bn. WYTBD are committed, approved developments that are expected to proceed in the next year. While not all will go through, a significant proportion is expected to be developed. The Q3 data for starts is also indicative of the possible pathways. It may not be a smooth process; delays can be expected. These represent a powerful rise in the sector. Mapped against the overall economy though, it may be smaller. The datacentre WYTBD is around 0.25% of nominal GDP at this stage. There have been numerous announcements regarding the pipeline for DC build commitments that will not be in the official ABS data.

If we assume the A$7.6bn increase, then deflate by target inflation, the rise in real private non-residential capital expenditure is an admirable 20%. Assuming it isn't implemented all at once and smooth the spend over multiple years, this would imply an approximate 0.4 percentage point rise in the contribution to real GDP per year. This is not to be ignored, but equally it doesn't suggest another boom period. However, if the media announcements are to be believed, there is a long-term pipeline of around A$150bn. If, and this is a big assumption, this comes about, then there could be a significant contribution to real GDP over a decade. This includes spending on the inputs, such as energy and water, as well as software. There are challenges to the projected implementation of datacentre construction. There has been a crowding out of construction as the public sector utilised available labour and inputs to building, creating roadblocks to rapid build out in the private sector. This will ease as the public build moderates. Energy and Transmission Energy is significant for DC and AI. DC are energy intensive and have huge energy, and thus transmission, needs. Increasingly, DC are saying they will provide their own energy, predominantly through renewables. The electricity building on WYTBD is larger than that of DC, and while AI and DC are a large part of this, the changing needs of the entire energy sector is also behind the ramp up. The WYTBD now equates to just shy of 3% of GDP on a nominal basis. Much of the acceleration since 2024 has been in the public sector, while private plans have been flat, after a sharp rise though 2022-2023. That will need to change if private energy generation is to be used to meet the new AI needs. Given the increasing focus on the social aspect of energy, and water, usage, often referred to as the energy trilemma of reliability, affordability and sustainability, combined with tight supply and rising costs, it should be expected that heavy users such as DC, and others, will meet their energy needs outside of the public provision. This can be represented as a capital expenditure tailwind, or an investment headwind. It is likely there is a bit of both. Some investors will be able to go ahead with private access to their energy, and water, needs. Others will see the costs, delays and social license as too high a barrier. Spending on actual AI itself will likely increasingly factor into the equation. Overall software spend has already surpassed the late 1990's boom and should further increase. As AI becomes cheaper per user, and other versions appear, this growth may slow. The generalised rise in overall spend thus far is also likely to represent the increased digitisation of lives and workforces that was already underway. AI adds to this. We would consider the contribution to growth to maintain on a steady path from here. Views as at 1 February 2025. |

|

Funds operated by this manager: Janus Henderson Australian Fixed Interest Fund , Janus Henderson Conservative Fixed Interest Fund , Janus Henderson Diversified Credit Fund , Janus Henderson Global Natural Resources Fund , Janus Henderson Tactical Income Fund , Janus Henderson Australian Fixed Interest Fund - Institutional , Janus Henderson Conservative Fixed Interest Fund - Institutional , Janus Henderson Cash Fund - Institutional , Janus Henderson Global Multi-Strategy Fund , Janus Henderson Global Sustainable Equity Fund , Janus Henderson Sustainable Credit Fund All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect. The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested. Whilst Janus Henderson believe that the information is correct at the date of publication, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson to any end users for any action taken on the basis of this information. |

17 Feb 2026 - Performance Report: 4D Global Infrastructure Fund (Unhedged)

[Current Manager Report if available]

fashion, driven by geopolitical concerns over Greenland,

Venezuela and Iran. (2-minute read)

17 Feb 2026 - Glenmore Asset Management - Market Commentary

|

Market Commentary - January Glenmore Asset Management February 2026 (2-minute read) Global equity markets kicked off the new year in volatile fashion, driven by geopolitical concerns over Greenland, Venezuela and Iran. This provided a boost to Resources, which drove the ASX All Ordinaries Accumulation Index up +1.6% for the month. This represented a slight outperformance vs the S&P 500, which rose +1.4%. However, the NASDAQ underperformed most global benchmarks (+0.9%), as fears over disruption caused by Artificial Intelligence (AI) weighed upon the Tech sector. Outside of the US, the FTSE 100 and Euro Stoxx 50 continued their strong run, rising +2.9% and +2.7%, respectively. The ASX experienced a particularly volatile month, which was more pronounced in the small-cap segment of the market. Energy and Gold were the strongest performing sectors, whilst Technology was the weakest performer, impacted by concerns about AI disruption. During the month, the ASX Small Ordinaries Accumulation Index rose +6.0% at its peak, before falling over -3% in the final week of the month, to finish +2.7% higher. In addition to the factors noted above, we believe the small-cap segment was disproportionately impacted by two events, being (1) stronger-than-expected Australian inflation data, which supported the RBA's subsequent February 2026 rate increase, and (2) a sharp reversal in commodity prices following the appointment of Kevin Warsh as the new Governor of the US Federal Reserve. Regarding monetary policy in Australia, the market expects 1- 2 more RBA rate hikes over the next 12 months. In bond markets, the US 10-year bond yield rose +7 basis points (bp) to 4.24%, whilst its Australian counterpart rose +7bp to 4.81%. The Australian dollar had a strong month, rising +4.4% to US$0.70, implying an increase of 2.9 cents. Funds operated by this manager: |

16 Feb 2026 - Performance Report: Glenmore Australian Equities Fund

[Current Manager Report if available]

16 Feb 2026 - 10k Words | February 2026

|

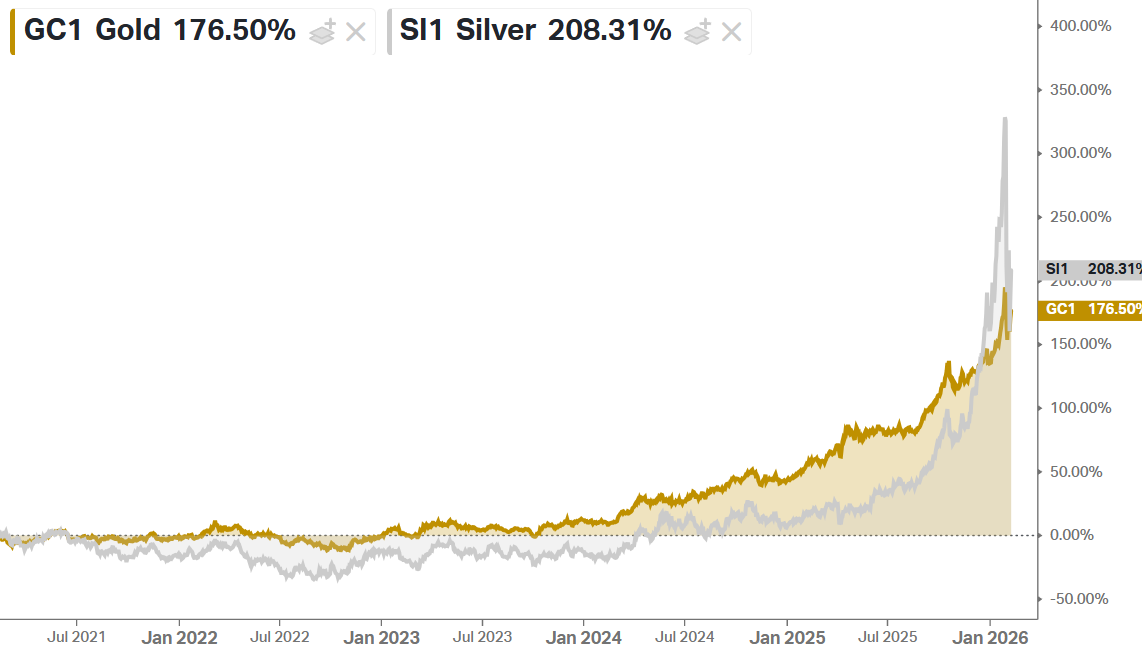

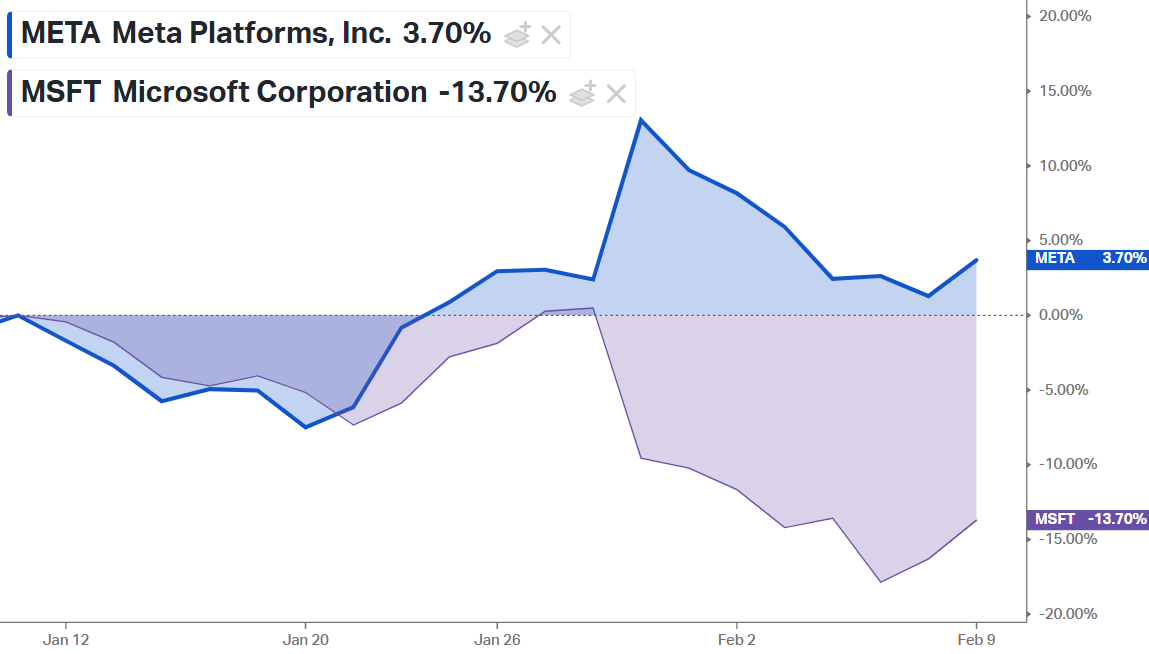

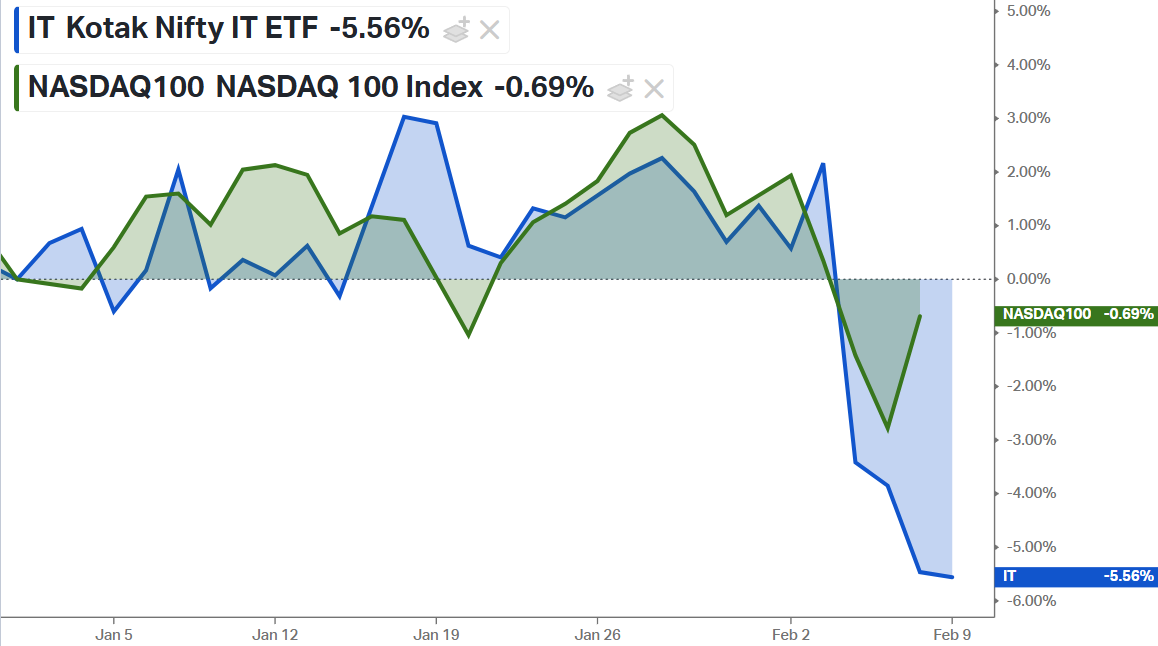

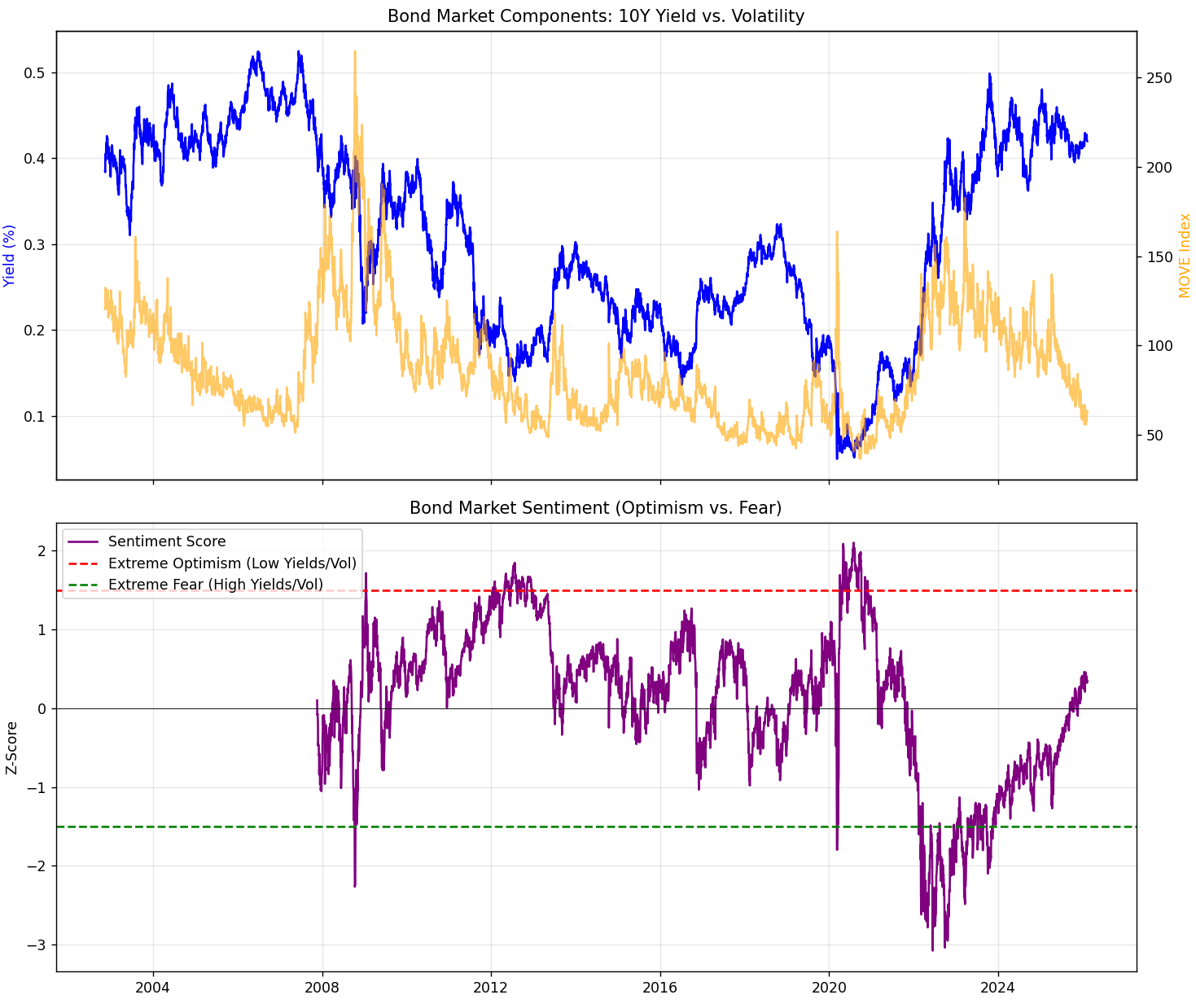

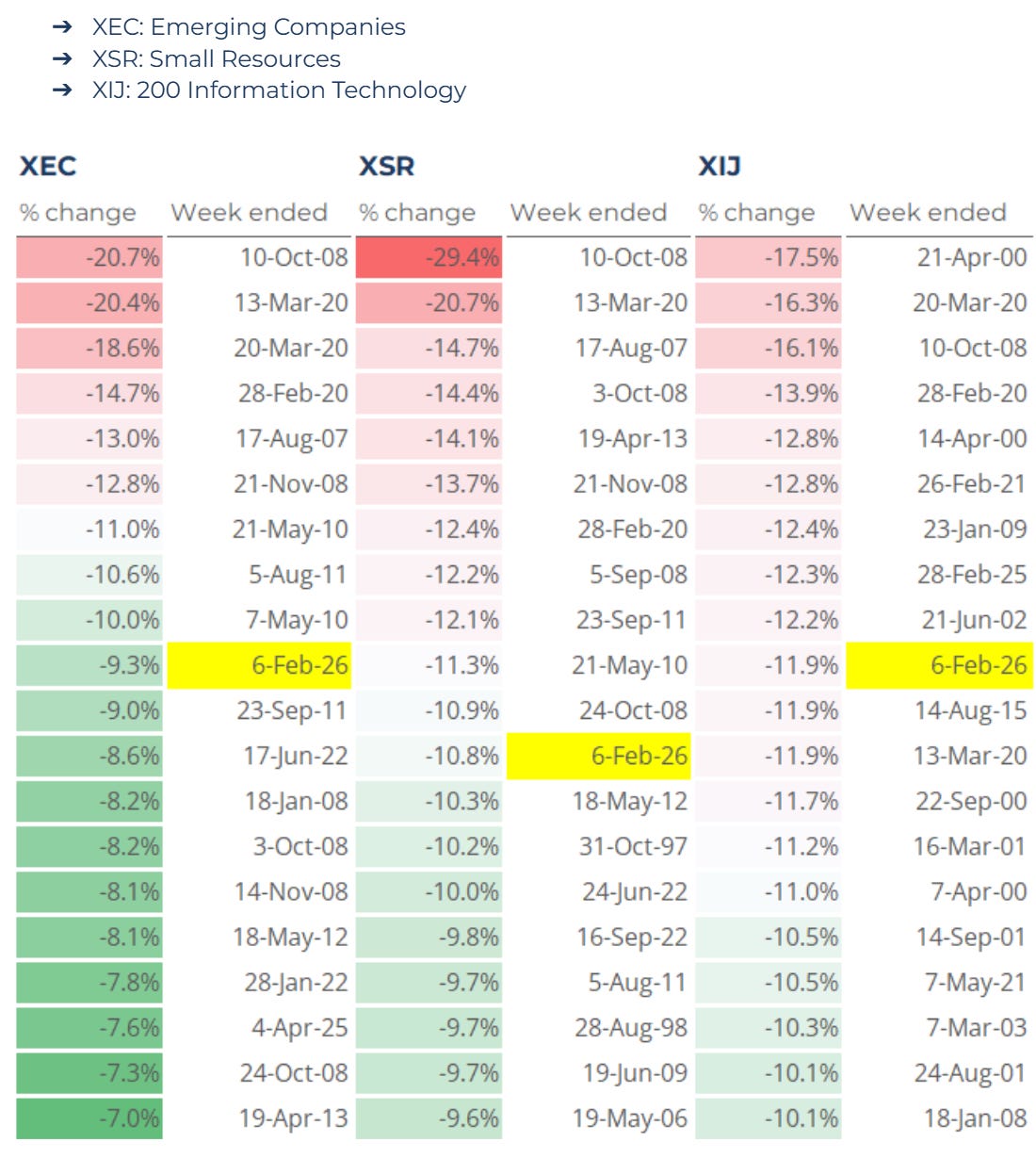

10k Words Equitable Investors February 2026 (2-minute read) Precious metals reacted savagely on the Kevin Warsh Fed Chair nomination. The "AI" capital drain bites for hyperscalers at the same time AI's rapidly improving capabilities bites for technology services. Government bond yields have been rising with low volatility amid broader market gyrations. Those gyrations were most apparent in the worst week since Covid-19 rocked markets in 2020 for Australia's small resources and large IT stocks. Valuation metrics in US tech - and software in particular - have taken a haircut. Regime change is apparent with the majority of stocks outperforming rather than the market being led by a few key stocks - both in the S&P 500 and among Australia's small caps. There is a huge dispersion in valuations among small caps to play with. Finally, US Office CMBS delinquency rate spiked to a record 12.3%! The "Warsh Effect" dents Gold and Silver price performance over past five years

Source: Equitable Investors, Koyfin "AI" divergence - market punishing MSFT for high capex

Source: Equitable Investors, Koyfin Capex as % of operating cash flow for "hyperscalers" (MSFT, AMZN, GOOGL, META, ORCL)

Source: Bank of America Global Research Hyperscaler's combined capital expenditure in US dollars

Source: Bloomberg India's IT services giants sold off on fears of IT disruption

Source: Equitable Investors, Koyfin US 10 year bond yield relative to MOVE Index of implied bond market volatility; and Equitable Investors' Bond Market Sentiment indicator

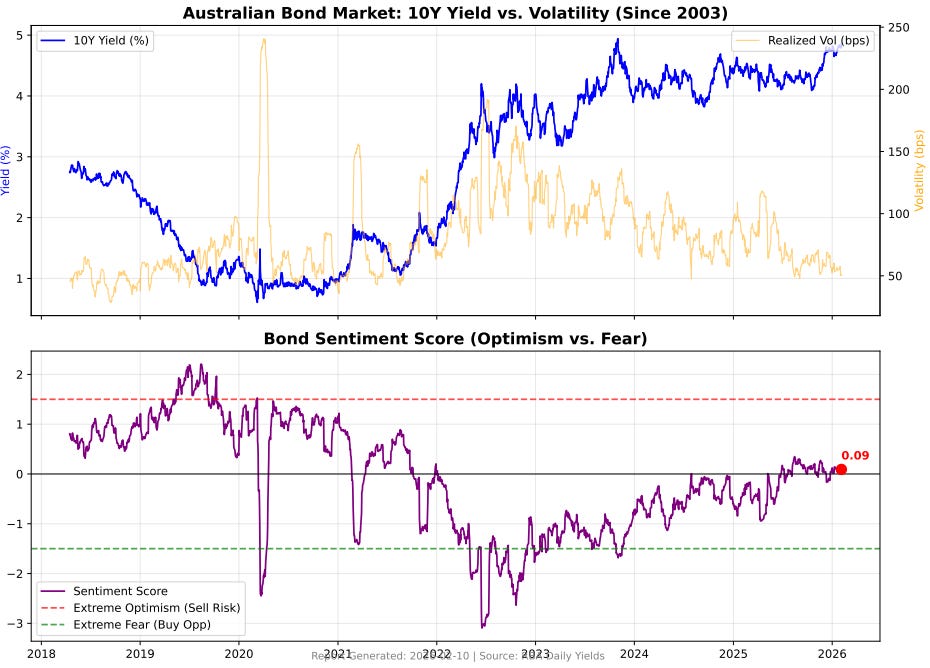

Source: Yale, Equitable Investors Aus 10 year bond yield relative to realised volatility; and Equitable Investors' Bond Market Sentiment indicator

Source: RBA, Equitable Investors Largest weekly precentage falls for three S&P/ASX indices

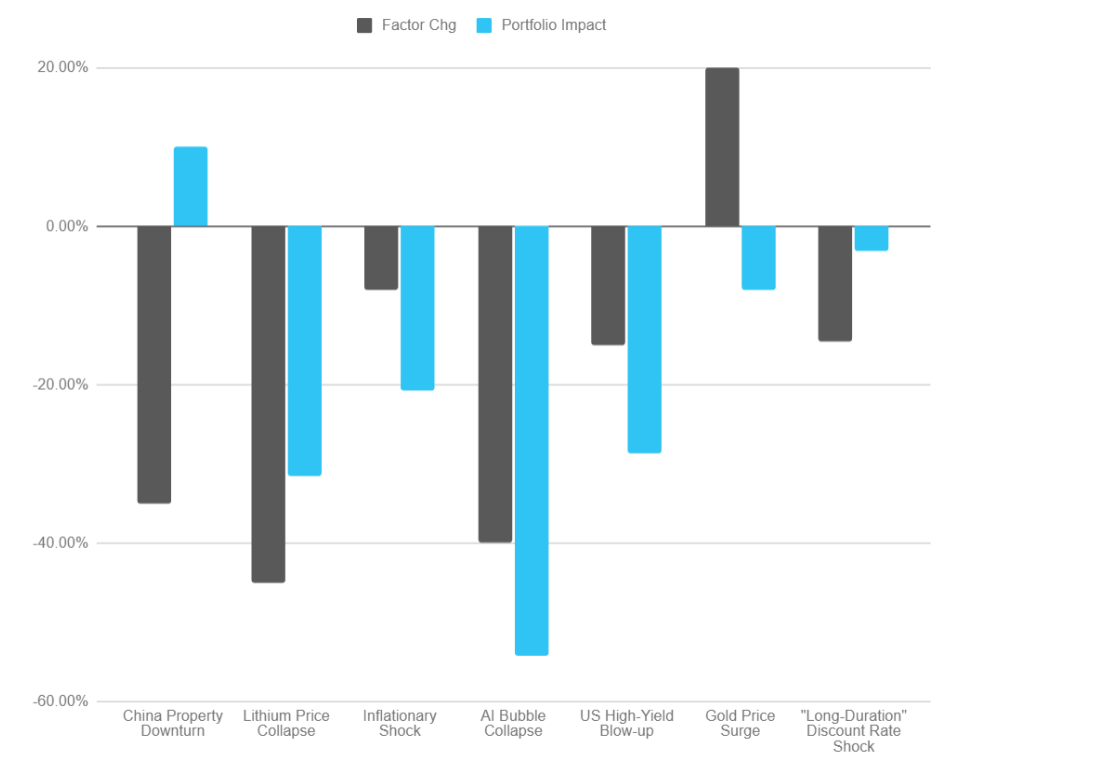

Source: Iress, Equitable Investors Impact on ASX small caps from factor shocks - implied by historical performance relative to proxy ETFs

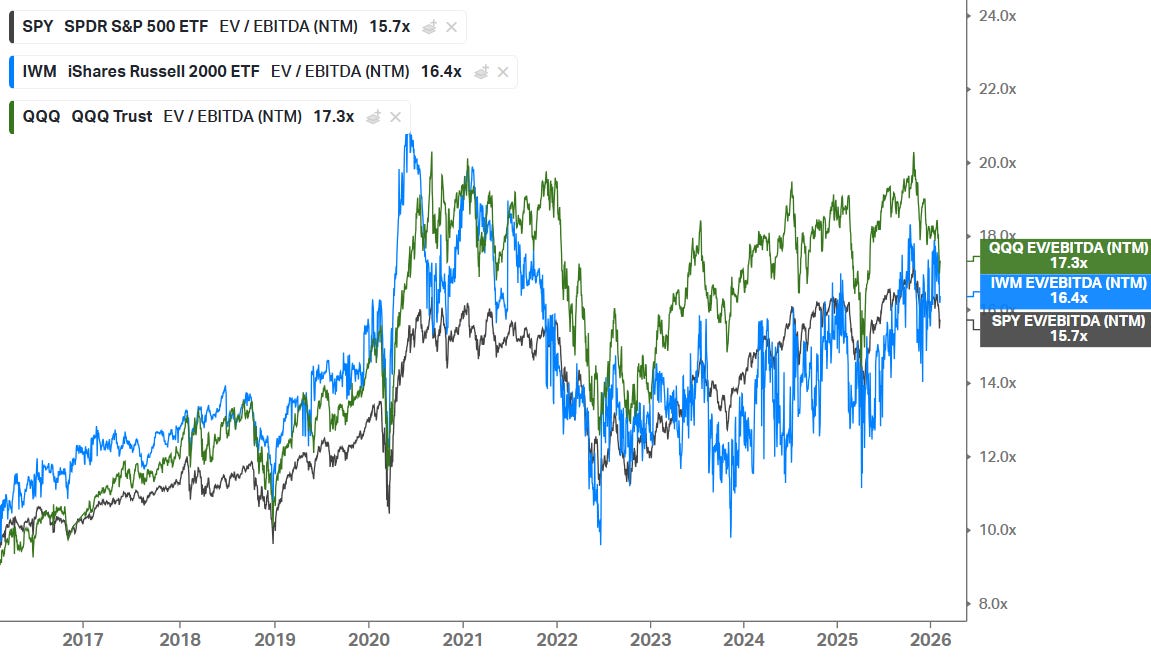

Source: Equitable Investors Recent pull-back in US tech EV/EBITDA multiples

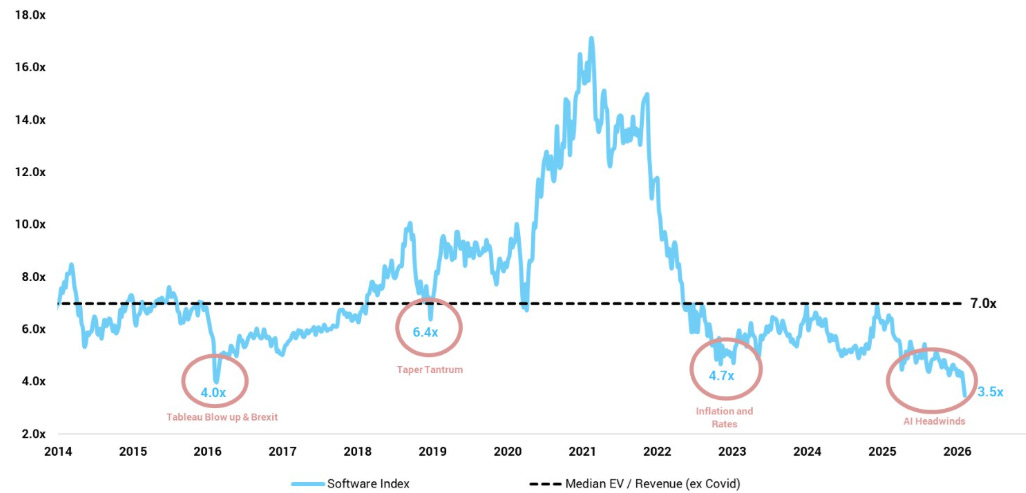

Source: Koyfin, Equitable Investors US Software sector median EV/Revenue multiple

Source: Altimeter Surge in % of S&P 500 companies beating the index

Source: Ned Davis Research via The Kobeissi Letter A regime shift with a surge in the percentage of stocks in the S&P/Small Ordinaries Index that outperformed the market cap weighted average return

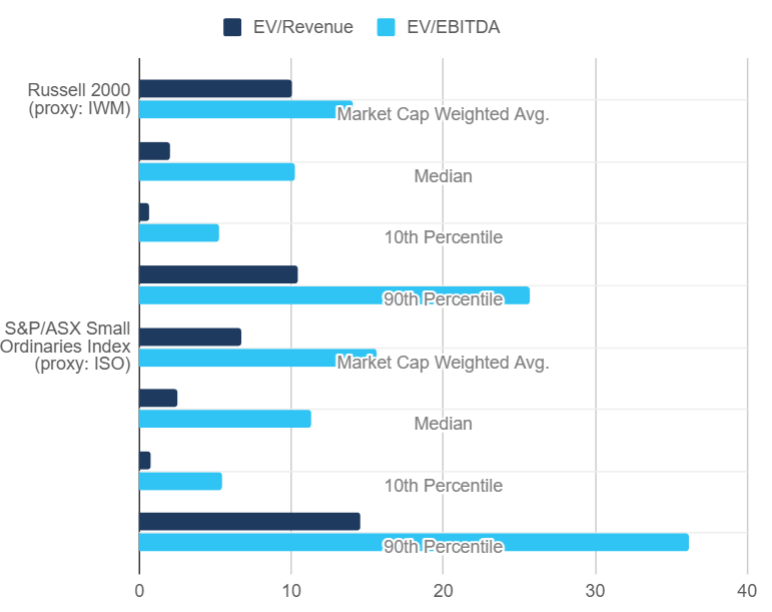

Source: Koyfin, Equitable Investors Dispersion of valuation multiples among US and Australian small caps

Source: Koyfin, Equitable Investors US Office CMBS delinquency rate spikes to record 12.3%

Source: Trepp via WOLFSTREET.com Funds operated by this manager: Equitable Investors Dragonfly Fund Disclaimer Past performance is not a reliable indicator of future performance. Fund returns are quoted net of all fees, expenses and accrued performance fees. Delivery of this report to a recipient should not be relied on as a representation that there has been no change since the preparation date in the affairs or financial condition of the Fund or the Trustee; or that the information contained in this report remains accurate or complete at any time after the preparation date. Equitable Investors Pty Ltd (EI) does not guarantee or make any representation or warranty as to the accuracy or completeness of the information in this report. To the extent permitted by law, EI disclaims all liability that may otherwise arise due to any information in this report being inaccurate or information being omitted. This report does not take into account the particular investment objectives, financial situation and needs of potential investors. Before making a decision to invest in the Fund the recipient should obtain professional advice. This report does not purport to contain all the information that the recipient may require to evaluate a possible investment in the Fund. The recipient should conduct their own independent analysis of the Fund and refer to the current Information Memorandum, which is available from EI. |

13 Feb 2026 - Hedge Clippings |13 February 2026

|

|

|

|

Hedge Clippings | 13 February 2026 The normally calm and rational exterior persona of RBA Governor Michele Bullock was rattled this week when her integrity was questioned during a heated Senate estimates hearing, when she was accused by Nationals senator Matt Canavan of "gaslighting" Australians when describing the economy as doing "okay". Given the current state of the Federal coalition, it is no wonder that Canavan tried to distract attention away from both the on-again-off-again shambles within the opposition, or the fact that they have been incapable of landing a blow on either Chalmers or Albanese, in spite of the opportunity, or need, to do so. However, it caused Hedge Clippings to turn to the dictionary (via Google) to clarify the term "Gaslighting", which wasn't a term with which we were overly familiar. It turns out it was the Merriam-Webster Dictionary "Word of the Year" in 2022, and is defined as "the act or practice of grossly misleading someone, especially for one's own advantage". No wonder that Canavan, and no doubt most politicians we can think of, are familiar with and use the term, given how well versed they must be in its implementation. And no wonder that Michele Bullock was so quick to refute the allegation. The RBA may well have jumped too quickly when cutting rates three times last year, only to see inflation start to nudge back up again, but to consider their statement and Bullock's media conference post meeting as "misleading" was bound to elicit a swift rebuttal. What obviously irked Canavan was that Bullock refused to pin the blame for rising inflation on Jim Chalmers and government spending, instead noting that while it contributed, there were other factors involved, including private demand, which had been stronger than expected. She also raised one of the major issues for the economy, namely stagnant productivity, which she termed "Australia's non-inflationary speed limit", and that unless productivity lifts, the economy may struggle to grow sustainably above 2% without fueling inflation further. Unfortunately, we can't see productivity suddenly changing, and if that's the case, it's likely that inflationary pressures will continue to rise, as will interest rates. News | Insights Magellan Global Equities Quarterly update | Magellan Investment Partners Market Update | Australian Secure Capital Fund January 2026 Performance News Bennelong Concentrated Australian Equities Fund |

|

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday |

13 Feb 2026 - Performance Report: Bennelong Long Short Equity Fund

[Current Manager Report if available]

13 Feb 2026 - Performance Report: Airlie Australian Share Fund

[Current Manager Report if available]