NEWS

29 Oct 2025 - China's Energy Pivot: The Turning Point Investors Can't Ignore

24 Oct 2025 - European & Australian ABS: 2025 review and outlook for the remainder of the year

|

European & Australian ABS: 2025 review and outlook for the remainder of the year Challenger Investment Management October 2025 12-minute read Our expectations, laid out in the outlook for 2025, {European & Australian ABS: Rounding up 2024 and looking ahead to 2025}, included high issuance volumes across both European and Australian ABS and for asset performance of collateral to remain relatively stable - despite rates remaining higher for longer than market expectations. 2025 year to date Market review - were our expectations in line with reality? Focus themes: Tariff impacts and Macro economic uncertainty After a strong start to the year in Q1, markets faced uncertainty in Q2 given President Trump's tariff announcement. Although new issue markets did grind to a halt and spreads widened to levels comparable to early 2024, volatility in securitised credit was lower than corporate credit given lower credit spread duration and higher average ratings. This was further dampened in European and Australian securitised credit by the low exposure to rate volatility as assets are predominantly floating rate. See our review of this period here: {Lessons from Liberation Day: Is now the right time to consider diversifying into securitised credit?} As markets rebounded, European ABS primary markets saw a strong pick up in May with issuers keen to get deals priced before the annual Global ABS conference in Barcelona, early June. Despite increased supply, spreads retraced from April wides with the secondary market subdued by investor focus on new issue markets. Strong Technical demand and supply from less traditional sectors A continued lack of mezzanine issuance and strong demand from investors persisted during the first half of the year. As a result, post the April tariff-induced volatility, spreads have reached YTD tights across asset classes globally. This has encouraged not only repeat issuers to come to market but also some new sectors/collateral included in transactions. Examples are RMBS transactions including HELOC (Home Equity Line of Credit) mortgage collateral in the UK and issuers transitioning previously private platforms to public markets. The second half of July and August gave us the traditionally quiet pipeline in Europe. In Europe, it is worth noting deals were still being placed privately or preplaced in part due to the more atypical collateral financed such as equity release products and legacy mortgage pool securitisations. On the regulatory front, June saw the release of the new EU securitisation framework proposals where key themes include changes to capital and reporting requirements, the motivation of which is to lower barriers for both issuers and investors. It is noted that the implementation is on a long-time horizon, likely through to 2027, given continued consultation and lengthy legislative process. Further detail is provided towards the end of this note. Expectations to Year End 2025 The last few months of 2025 are expected to be shaped by a complex and evolving geopolitical and macroeconomic landscape. Political and geopolitical risks are front-of-mind for market participants and we expect this dynamic will persist into year-end and beyond. Investor sentiment remains highly sensitive to developments in global trade policy as well as the pace of Federal reserve rate cuts. Political developments in the U.S. and the potential escalation of the conflict in Ukraine add further layers of complexity to the investment environment. Notwithstanding this backdrop, technicals for the ABS market globally remain strong. Supply of new issue paper has held up well, with volumes similar to those seen in 2024, and spreads tightening as demand has held up. However, macroeconomic fundamentals do remain a concern for specific jurisdictions. We remain vigilant for any changes in performance of the underlying consumers, and we look to rating agencies to maintain appropriate performance assumptions to limit rating risk for our investors. Issuance Despite the markets facing uncertainty during Q2 and the inevitable stall in primary issuance across Europe and Australia, issuance volumes as at end September 2025 are at just over €71bn in European ABS, slightly lower than the issuance year to date in 2024. We expect issuers to capitalise on windows of market stability, leading to concentrated bursts of primary activity--September being a prime example with €14.6bn of transactions priced, the highest month of issuance since May 2024. Absent any macro shocks, we expect European ABS 2025 issuance to beat the annual record for post GFC issuance volume set in 2024. In Australia, YTD issuance volumes have been high at AUD50.9bn as at end September largely on par with last year's breakout year for issuance which had reached AUD$59.4bn for the equivalent period. September was also a post GFC record month for issuance. With a strong pipeline for October, we expect issuance volumes to remain at a strong cadence during October and November with issuers aiming to have deals priced before the annual Australian Securitisation Conference, late November. Asset Performance Performance of underlying collateral In European ABS has remained stable across most sectors aided by the decline in rates observed to date and continued resilience of employment statistics. In Australia, asset performance varied by receivable type and lender, but the lower interest rate environment is broadly viewed as supportive for borrowers. Generally, collateral performance has held up relatively well despite pressures on household servicing costs, helped by floating-rate structures and gradual policy easing. Spread Dynamics and Demand Given the continued supply demand dynamic for mezzanine issuance, we continue to see high subscription levels in primary and competitive BWIC auction processes in secondary for mezzanine investment grade bonds. For larger, more established platforms, denominated in EUR, we continue to see the placement of senior paper can be affected by bouts of large supply with newer issuers often less covered and at wider spreads. Australian ABS spreads have compressed significantly across the capital structure, with the single A and BBB rated tranches pricing similarly to European transactions during September. The credit curve is relatively flat compared to European issuance with the more senior parts of the capital structure still offering a significant basis to their European counterparts. Also, the breadth of issuers and emergence of new collateral types, structures and issuers across Europe and Australia continues to present opportunities for investors to earn a premium over more traditional platforms. We note that structured finance spreads across sectors and jurisdictions are testing on to post GFC tights but continue to hold that the benefits on holding securitised products which include; a pickup to similarly rated corporates, limited spread duration, and exposure to floating rate assets. We discuss structure finance as an alternative to corporate credit. Regulatory Activity continues to evolve Market participants were kept busy as always, with non-market related regulatory activity - in particular, the EU regulatory reform and UK autos ruling (see below) UK Auto Court Rulings: We covered the uncertainty that Court rulings provided UK auto lenders and ABS investors in our article here, "Uncertainty Weighs on UK Auto Lenders Due to Recent Court Rulings", at the start of the year. What did the Supreme Court decide? The Supreme Court overturned the Court of Appeal's decision and ruled that UK dealers did not owe a fiduciary or disinterested duty to the borrowers. This removed the spectre of widespread, large claims for compensation based solely on hidden commission arrangements. There is still some work being done by the FCA on a potential redress scheme focusing on Discretionary Commission Arrangements (DCAs), which were banned in 2021. Impact on UK Auto ABS? As we noted in our piece above, the impact on UK Auto Asset-Backed Securities (ABS) did remain limited, thanks to strong structural protections and credit enhancements, although secondary liquidity was more challenged until more clarity was reached. Publicly distributed issuance in UK Auto ABS across bank and non-bank lenders, was €3.6bn in 2024 compared to no issuance at all seen until September this year, in the space. Will UK Auto ABS issuance pick up? We do expect a pickup in issuance, as demonstrated by the first UK Auto ABS to price since the since the Supreme Court ruling. In mid-September, VW UK placed Driver 10 publicly with the senior class A spread at 60bp and 100bp above SONIA, on the Class B and with an increased deal size to just over €700mn due to demand. This compared very well to the previous Driver transaction price in September 2024, where the senior tranche also priced at 60bp over SONIA. The transaction placement is a positive signal for UK non-bank lenders and will have given them confidence in execution. That said we do note that given lower origination volumes, the funding needs of these lenders may be more muted in the near term. European Securitisation Regulation: A consultation was launched in Q4 2024 by the European Commission to gather feedback from the industry on a wide range of issues pertaining to the EU securitisation market. The legislative proposals were presented in June 2025 and overall, the reaction from market participants was positive regards proposed changes to the STS framework. We limit our discussion here on the proposed changes to high level comments as the final proposals come out next year but the aim on the proposals is stated as to reduce barriers to issuance and investment in EU securitisation. The expected changes include those we believe are most relevant, below:

Challenger IM Credit Income Fund , Challenger IM Multi-Sector Private Lending Fund For Adviser & Investors Only Disclaimer: The information contained in this publication has been prepared solely for solely for the addressee. The information has been prepared on the basis that the Client is a wholesale client within the meaning of the Corporations Act 2001 (Cth), is general in nature and is not intended to constitute advice or a securities recommendation. It should be regarded as general information only rather than advice. Because of that, the Client should, before acting on any such information, consider its appropriateness, having regard to the Client's objectives, financial situation and needs. Any information provided or conclusions made in this report, whether express or implied, do not take into account the investment objectives, financial situation and particular needs of the Client. Past performance is not a guide to future performance. Neither Fidante Partners Limited ABN 94 002 895 592 AFSL 234 668 (Fidante Partners) nor any other person guarantees the repayment of capital or any particular rate of return of the Client portfolio. Except to the extent prohibited by statute, Fidante Partners or any director, officer, employee or agent of Fidante Partners, do not accept any liability (whether in negligence or otherwise) for any errors or omissions contained in this report. |

23 Oct 2025 - One Theme That Can Make You Rich

|

One Theme That Can Make You Rich Marcus Today October 2025 4-minute read

|

|

Back in 2005, I had a client who became quite famous at Bell Securities because he was very good at investing. He was a fairly young guy who had inherited $500,000, and he lived in Bali. He had no stock market experience, but he had a lot of time in Bali. He turned his hand to the stock market, found me as a broker (I think I was in the media at the time), and used me for information. He didn't really want advice. If I rang him up with my lame morning meeting ideas -- that he should buy Leighton Holdings because our analysts thought it was cheap -- he would say, "Look Marcus, what's the drive? Are its fundamentals changing for the better?" And I would say, "I don't know." He ended up not asking for advice, just using me for execution. But he was so good at what he was doing, despite a low level of knowledge, that everybody at Bell started following him in the back office admin system. You would hear people talking over lunchtime and in the lift -- "What's Bali Boy doing?" (as we used to call him). People would track his trades, and he was very successful. 2005 was the resources boom era -- it ran from around 2002 to 2008. What he was doing was investing on thematics rather than stock picking. He parked most of that money in BHP and also bought Fortescue, which at the time was pretty much an explorer turning into a producer. He was terribly successful. He had other iron ore stocks too, and also bought into uranium. I think he had Paladin when it was still below 50 cents, and it went to $10. He was playing themes. If you play themes, the stocks pick themselves. He had read one line about China building "a Brisbane every three months." So they were going to need a lot of iron ore and steel, and that was going to come from Australia. All the iron ore stocks had fundamentals changing for the better. That was the key driver -- fundamentals changing for the better. The catalyst was China building Brisbane every three months. We kept seeing things happening in the iron ore stocks. The smaller ones were getting taken over. They were declaring special dividends. They were having share buybacks. They were reporting better than expected results. We thought, what does he know? Has he got inside information? Truth is, he knew nothing more than us -- but he did know there was a catalyst. China was driving the iron ore price, which was feeding into the fundamentals of every iron ore stock. And when companies are making money, they announce special dividends, they have better results, they take over other companies. That's what was happening in iron ore. The lesson from dealing with him was simple: you need fundamentals changing for the better. That takes a catalyst. You have to find something changing in the world, and good things will happen to stocks in good sectors. Another thing he was particularly good at was being in Bali, looking at Australia from a distance. We were too close. He was like the man in the moon, looking down and saying, "All that iron ore is going to come from Australia." We were looking at the fundamentals of BHP, the PEs and yields. He was looking conceptually, saying Australia was in the perfect spot to exploit China's economic revolution. Objectivity was his edge. So: objectivity, playing themes, and making sure fundamentals are changing for the better. Take that to today. One of the strongest themes in the world right now is AI. Companies are doing deals, taking each other over, announcing contracts, reporting better than expected results -- all driven by the investment in cloud infrastructure to facilitate AI, and the demand for computing power. Objectively, Australians can look at the US and say: yep, that's happening. Objectively, we can also see it's all getting overvalued. Objectively, we can see that at some point it's sentiment-driven and that might change. But for now, that is the theme. It's a great template for any investing: ask, what's the catalyst? Are the fundamentals changing for the better? If you get that right, the stocks pretty much pick themselves. And the events that surprise on the upside will just happen. Good things happen to stocks in good sectors. DISCLAIMER: This content is for general information purposes only and does not constitute personal financial advice. Please consider your own circumstances or seek professional advice before making investment decisions. |

|

Funds operated by this manager: |

22 Oct 2025 - Skin in the game

|

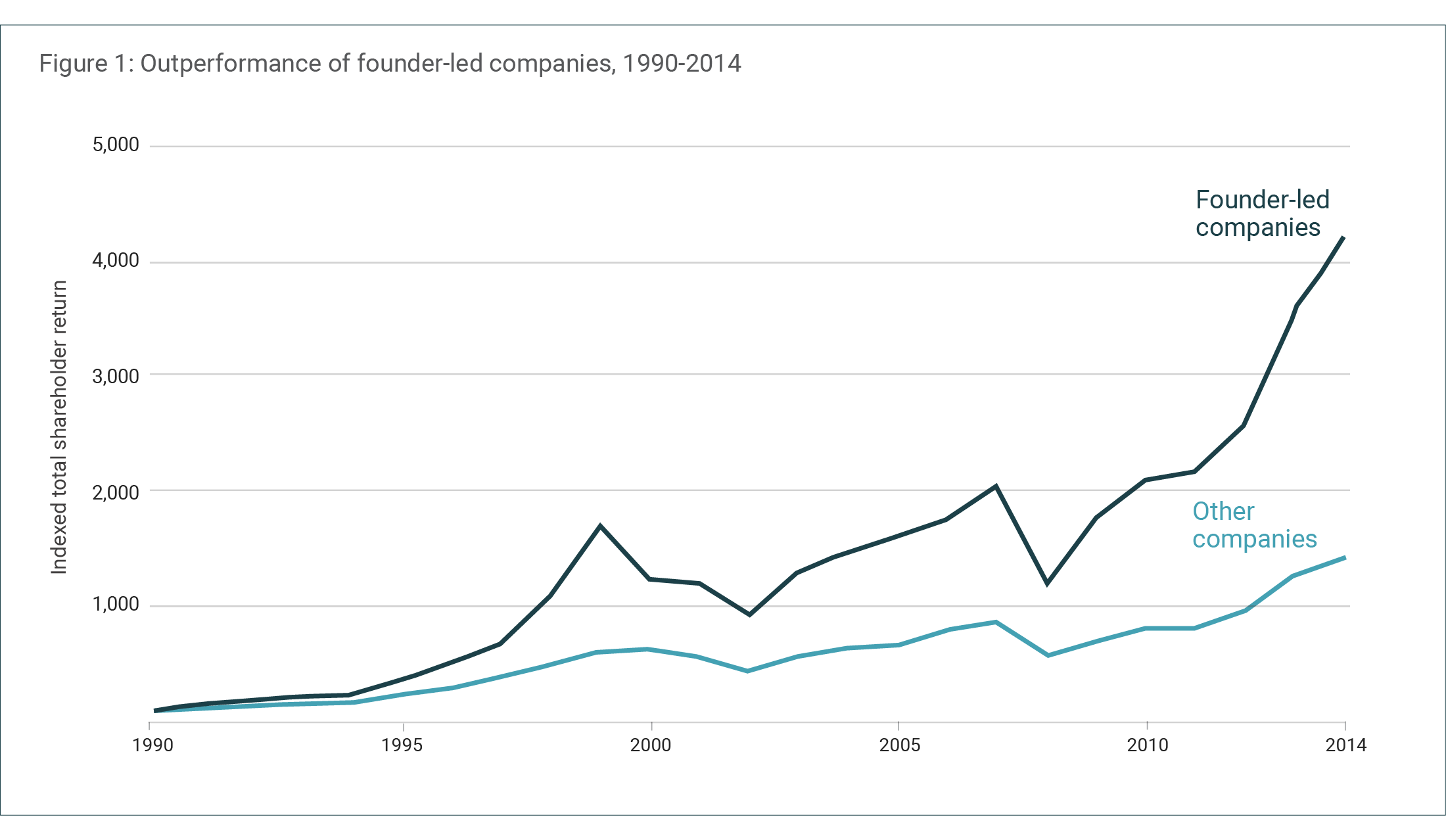

Skin in the game Canopy Investors October 2025 5 min read 'Show me the incentive and I'll show you the outcome.' Investing in a company means putting your capital in the hands of managers who decide how it's used. Managers have access to information you don't, and their personal incentives may differ from yours. Since people naturally act in their own self-interest, ensuring managers' interests align with yours is critical. At Canopy, we believe the most effective alignment comes through meaningful ownership, whether from founder-operators, family-controlled businesses, or executives with substantial equity positions. Historical out performance of aligned managementCompanies with aligned management consistently outperform their peers. Bain & Company's analysis of S&P 500 firms from 1990 to 2014 showed that founder-led companies delivered cumulative total shareholder returns 3.1 times greater than other companies over this period, as shown in Figure 1 below.

Source: Bain & Company. One might argue this simply reflects the exceptional performance of technology companies over this period, many of which happen to be founder-led. However, even when technology firms were excluded from the analysis, founder-led companies still delivered 1.8 times the returns of their peers. Academic research suggests this outperformance stems partly from differences in how founder-led companies allocate capital and innovate. Fahlenbrach's 2009 study of 2,327 firms from 1992-2002 showed founder-led companies invested 22% more in R&D and 38% more in capital expenditures than their non-founder-led peers, and delivered annual share price outperformance of 8.3% even adjusting for risk factors. This combination - higher investment and superior returns - demonstrates that founder-CEOs don't just spend more on growth, they're better at selecting which investments will create value. Lee, Kim, and Bae's study of S&P 500 companies from 1993 to 2003 showed founder-led companies generated 31% higher citation-weighted patent performance (a measure of innovation impact) versus non-founder-led companies. The advantage remained at 23% even after controlling for higher R&D spending, indicating they innovate more efficiently. The study also found that founder-led companies tend to produce more breakthrough innovations (patents in the top 5% by citations). However, alignment does not universally drive optimal outcomes. Morck, Shleifer, and Vishny's 1988 study of 371 Fortune 500 firms revealed an inverted U-shaped relationship between management ownership and firm value. The study found firm performance improved substantially when managers increased their ownership positions above 5%, but then declined again as ownership levels increased beyond 20%, potentially indicating entrenchment and value destruction. This entrenchment effect is particularly pronounced in family-controlled firms. The Morck study found evidence that older firms run by founding family members underperformed compared to those led by unrelated officers. As family ownership stakes increase beyond optimal levels, concentrated voting control can insulate management from market discipline and traditional governance mechanisms. Entrenchment risk may manifest through nepotism in senior appointments, excessive compensation, retention of underperforming family executives, resistance to strategic changes that threaten control, and conservative financial policies that prioritise stability over growth. The ownership mindsetWe believe companies with properly aligned management teams outperform for several fundamental reasons:

|

|

Funds operated by this manager: |

20 Oct 2025 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

||||||||||||||||||||||

| MA Prime Logistics Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Wingate Investment Partners Trust No. 3 | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

Wingate Property Senior Debt Holding Fund |

||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Global X Physical Gold Structured (GOLD) | ||||||||||||||||||||||

|

||||||||||||||||||||||

|

Want to see more funds? |

||||||||||||||||||||||

|

Subscribe for full access to these funds and over 900 others |

17 Oct 2025 - Quarterly State of Trend report - Q3 2025

|

Quarterly State of Trend report - Q3 2025 East Coast Capital Management October 2025 3-minute read In this update, we present the quarterly State of Trend report for Q3, 2025. Our report covers the performance of Trend Following systems compared with traditional investments such as the S&P/ASX 200 Total Return index, and the Australia "60/40" portfolio. Trend Following provides exposure to a diverse pool of underlying instruments, and implements trading strategies systematically and without emotional biases. Tariff turmoil impacts global markets In Q3 2025, markets remained turbulent as inflation pressures, shifting rate expectations and ongoing geopolitical friction shaped sentiment. Trend following systems have rebounded from drawdown, benefitting from sustained moves in precious metals, cattle, and technology-linked equity indices, significantly outperforming the ASX200 and 60/40 portfolio. Key market movements in Q3 2025

Featured chart - Platinum

See the full report at our website. Funds operated by this manager: |

16 Oct 2025 - Australian economic view - October 2025

|

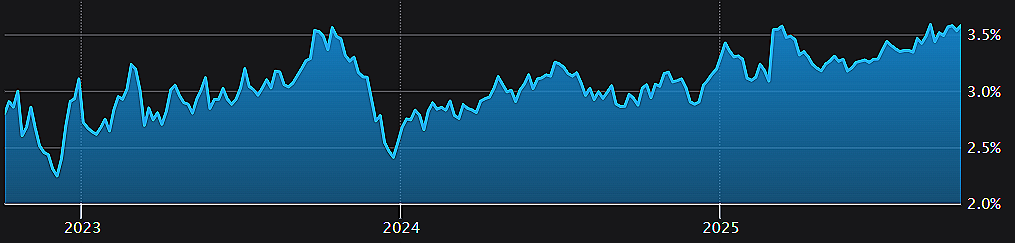

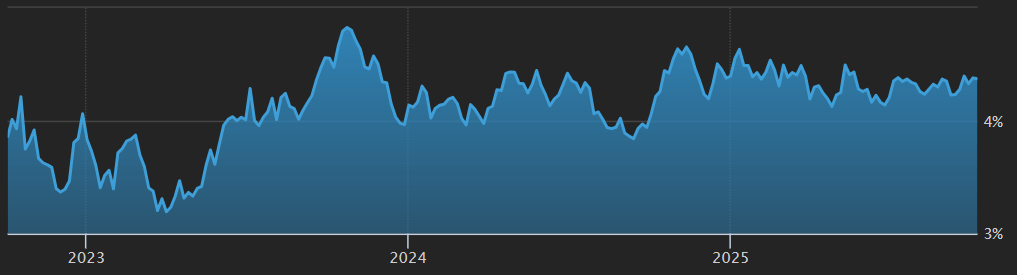

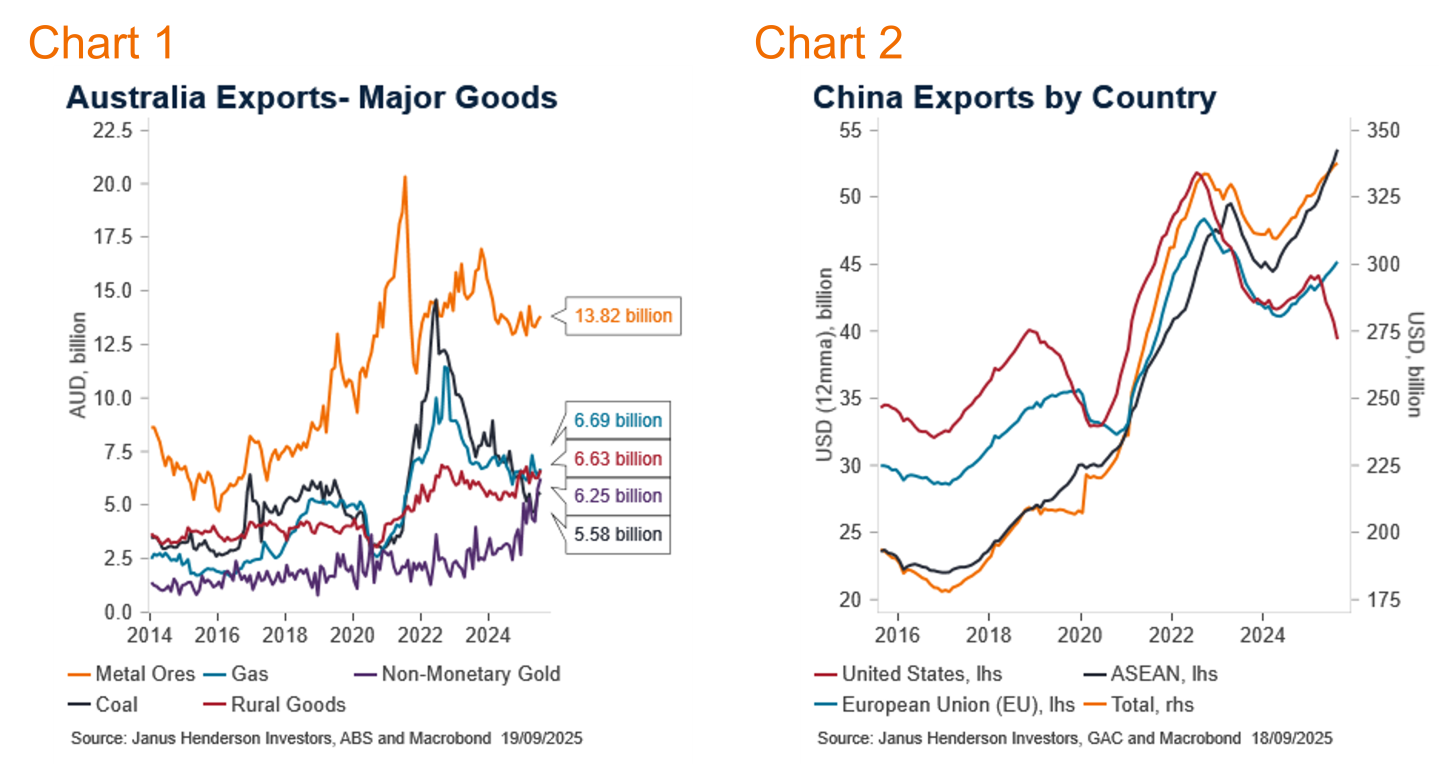

Australian economic view - October 2025 Janus Henderson Investors October 2025 (Originally published by Janus Henderson Investors on 1 October 2025) Emma Lawson, Fixed Interest Strategist - Macroeconomics in the Janus Henderson Australian Fixed Interest team, provides her Australian economic analysis and market outlook. Market reviewAustralian bond markets saw a repricing of the Reserve Bank of Australia (RBA) in September. The Australian bond market, as measured by the Bloomberg AusBond Composite 0+ Yr Index, rose 0.1%. The RBA maintained the cash rate at 3.60%, as was expected. Three-month bank bills were steady at 3.58% by month end. Six-month bank bill yields rose 9 basis points (bps) to 3.66%. Australia's three-year government bond yields ended the month 15bps higher, at 3.55%, while 10-year government bond yields were 2bp higher at 4.30%. While global ructions continued in the background, it was the local data that drove the big moves in local yields. Second quarter GDP was a touch higher than expected, with a pick-up in household consumption. There are continued concerns around the transition between a softer public sector and a better off household sector, so better than expected spending news was welcome. That transition isn't entirely guaranteed, with employment growth dropping again. Although, with the unemployment rate steady, through lower participation, the RBA is less concerned about a softening labour market. The inflation side of the RBA's mandate captured more attention, with the volatile monthly series precipitating renewed inflation concerns. The headline series was higher than expected, at 3%yoy, returning to the top of the RBA's target band. In the details, market services, strongly related to the labour market, was higher and led to the RBA's heightened inflation awareness in their recent press conference. This cloudy picture has the RBA returning to a highly data dependent stance. The global backdrop shows a slowing US economy, countered by the renewed Federal Reserve easing cycle. The Chinese economy remains lacklustre, while global trade continues to be uncertain. High government debt levels remain a concern for bond markets in the UK, parts of Europe and Japan. Market outlookRenewed inflation concerns have seen a repricing of the RBA's expected path higher, with a low in the cash rate at 3.30% in August 2026. This is higher than our base case for the RBA to ease a further 75bps to 2.85%. Our low case reflects a weaker economic outcome and the RBA easing by a total of 250bps. We allocate a modest weight to the low case. We hold a small, long duration position to take advantage of some of the lift in yields, while we remain vigilant through the volatility to take advantage of two-way mispricing. Monthly focus - Global trade still to play outThe US implemented decades high and comprehensive tariffs across the globe throughout the last six months. The global economy has absorbed these thus far, seemingly defying initial concerns. There are increasing signs of a slowing in global trade and adjustments in existing trade relationships. We expect the transition to a new set of trading relationships to slowly continue. Australia's direct tariffs from the US are at the low end of the range, at 10%, and our trade with the US is a small proportion of total trade. As such, the direct impacts from the US' policy were always expected to be limited. Concerns centre on the indirect impact of trade with our largest trading partners including China, Japan, South Korea, Taiwan and India. Thus far, all is well. Australian exports are tracking comfortably. Goods exports have been solid, while services recover from Covid era weakness. However, there are signs that global policies have not yet been fully absorbed by the global economy, and the time to relax, considering these fundamental changes, has not yet arrived. Australian exports are a function of broad global economic growth. The stop-start and uncertain nature of the global tariff implementation has pushed back the expected impact they will have on global economic growth, but not fully eliminated it. The tariff pressure has now started to build, and we see global demand levels easing off. China's GDP is slowing, due to tariff impacts but also domestic factors, and demand for iron ore and coal are slowing along with it. Nominal trade values have picked up as prices have improved, but volumes are lower. This bodes poorly for the future as demand is easing at the point where global competing sources of iron ore are about to rise. One bright export light is non-monetary gold. Gold exports have risen sharply, along with the rise in prices, to make it a major export good, besting coal. Rural goods are also holding well. Services exports have partially recovered from their pandemic slump. Net personal travel remains soft, albeit off its recent lows. Education services exports lifted to above pre-pandemic highs but have now stalled. Changing global education demand and regulation have tempered additional growth. A loosening of domestic policy and reinvigoration of Chinese and Indian student demand are required to elicit a resumption of higher growth from current levels.

Global patterns are showing signs of slowing goods exports, particularly to the US. China, for example, has seen a sharp slowing of exports to the US, but a concomitant pick-up in exports to its Asian neighbours. The sustainability of these redirected flows may be challenged if found to be re-exports and thus attracting even higher tariff rates. For now, the flows are in flux, and yet to find a new equilibrium. History tells us that higher tariff rates will always reduce trade volumes, and in turn global growth. What we have learnt this time, is that the process can take significantly longer to flow through due to the uncertain and inconsistent nature of the implementation. It would be premature to ignore the historical experience of poorer macro-outcomes in the face of higher trade restrictions. We anticipate an easing in iron ore exports over the coming year, and a generalised moderation in broad export growth, based on lower global economic activity. As domestic consumption improves, and the stated defence spending increase is delivered, import growth is expected to rise. As a result, we forecast a deterioration in Australia's net trade position, which will be a net detractor for GDP through 2026 and into 2027. |

|

Funds operated by this manager: Janus Henderson Australian Fixed Interest Fund , Janus Henderson Conservative Fixed Interest Fund , Janus Henderson Diversified Credit Fund , Janus Henderson Global Natural Resources Fund , Janus Henderson Tactical Income Fund , Janus Henderson Australian Fixed Interest Fund - Institutional , Janus Henderson Conservative Fixed Interest Fund - Institutional , Janus Henderson Cash Fund - Institutional , Janus Henderson Global Multi-Strategy Fund , Janus Henderson Global Sustainable Equity Fund , Janus Henderson Sustainable Credit Fund Disclaimer: This article reflects the views of the author(s) at the date of publication and does not necessarily represent those of FundMonitors.com. It is provided for general information only and does not constitute investment advice or a recommendation to buy or sell any security. Market data, views, and forward-looking statements were current as at 1 October 2025 and may change without notice. Past performance is not indicative of future results. Readers should consider their own objectives and obtain professional advice before making investment decisions. All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect. The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested. Whilst Janus Henderson believe that the information is correct at the date of publication, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson to any end users for any action taken on the basis of this information. |

15 Oct 2025 - Europe: The centre of Europe's global arms race, in power, defence and AI

|

Europe: The centre of Europe's global arms race, in power, defence and AI Ausbil Investment Management October 2025 Reading time 15mins SummaryFor years, the US market has led global equity growth, but soaring valuations now suggest much of the upside is already included in prices. Meanwhile, Europe, having been in the growth doldrums, is stepping into the spotlight with fresh government spending and attractive valuations, fuelling new opportunities. Ausbil's Global Small Cap Team argues that shifting focus to select European companies could unlock unrecognised earnings growth. Key Points

The US marketThe US market has been the clear winner for many years, both after the Global Financial Crisis (GFC) and more recently since the COVID-19 pandemic. The low-interest rate environment of the 2010s supported the US market, particularly US technology. Following COVID, significant fiscal spending programs were introduced in the US, including the Infrastructure and Jobs Act (2021), the Inflation Reduction Act (2022), and the CHIPS Act (2022). These initiatives injected substantial fiscal support into the US economy, underpinning investment themes such as US onshoring, artificial intelligence and data centre capital expenditure, and the expansion and upgrading of electricity grids. A shift in direction: Europe reawakeningAusbil's view of the US economy is that tariffs will have a downward drag on growth in the near term before growth begins to build again at the end of 2025, and into 2026. We think that the chance of a US recession is lower than the market is ascribing given the mitigating factors discussed below. With the hard monetary tightening undertaken by global central banks in 2022 and 2023, monetary authorities have significant room to stimulate should this be needed. Of course, we will keep a watchful eye on this and make any necessary adjustments as events unfold. Transition from Unrecognised to Recognised Earnings GrowthOver the last few quarters, however, valuations in the US have risen to elevated levels relative to both the rest of the world and their own historical averages. While we continue to anticipate robust earnings growth in the US, we now see significantly more potential for unrecognised earnings growth emerging from the European region. For instance, Price-to-Sales valuations for the S&P 500 are near all-time highs (Chart 1), suggesting that much of the robust earnings growth is already priced into US large-cap stocks. Global large caps are also elevated in valuation, both MSCI World and the S&P 500 priced well in excess of MSCI World Small Caps on price-to-sales valuations. Shifting from the US to EuropeToward the end of last year and earlier this year, we began trimming positions and taking profits in US companies that had performed well over recent years. The capital freed up was redeployed into several European companies with strong projected earnings growth. Europe appears compel- ling when compared to the US for several reasons. First, valuations in the European Union and the UK remain comparatively attractive, especially as US valuations have continued to climb (Chart 1). Second, European governments are now making clear and quantifiable commitments to increase fiscal spending, a significant shift after many years of conservative fiscal policy. This includes sig- nificant increases in defence spending, and in related areas like energy, information technology and industrials. Opportunities in an emergent EuropeGiven the macro backdrop, the outlook for stronger growth in Europe, and more fiscal and defence spending, sees Europe at the centre of a global arms race in power, defence and AI. Increases in fiscal and defence spending will have a multiplier effect, delivering positive impacts on the wider European economy and on some European companies in particular. Industrial sectors such as engineering, aerospace, shipbuilding, electronics, logistics and IT stand to benefit significantly. Furthermore, much of the fiscal spending is mandated to remain within European borders wherever possible, which should boost local industries such as steel production, truck manufacturing, and logistical engineering. Logistics and warehousing in environment of rising growthWarehouses De Pauw (WDP) is a real estate investment trust, which engages in the development and leasing of logistic and semi-industrial real estate properties across Europe (Belgium, The Neth- erlands, France, Germany, and Romania). Real estate investment trusts had a punishing 2022-2024 with restrictive monetary policy and slow growth, however, with the European Central Bank in an easing cycle and the economy rebounding, leaders in logistics like WDP are set to capture upside in business activity and investment. Moreover, lower rates correspond with tighter cap rates which is an additional tailwind for valuations for companies like WDP. Power and AI driving secular investmentThe EU is witnessing major investment in the electrical transmission network across Europe, with capex investment in the coming five years (2025-2029) at multiples of the level undertaken in the last five years (2020-2024), ranging from 2x to 7x the amount invested previously (Chart 4). This capex spend by EU transmission system operators (TSOs) will benefit companies across the value chain in electrical engineering, services, transformers, transmission and technology. |

|

Funds operated by this manager: Ausbil 130/30 Focus Fund , Ausbil Australian Active Equity Fund , Ausbil MicroCap Fund , Ausbil Australian Geared Equity Fund , Ausbil Active Sustainable Equity Fund , Ausbil Global SmallCap Fund , Ausbil Active Dividend Income Fund , Ausbil Australian Concentrated Equity Fund , Ausbil Australian Emerging Leaders Fund , Ausbil Australian SmallCap Fund , Ausbil Balanced Fund , Ausbil Global Essential Infrastructure Fund (Unhedged) , Ausbil Global Resources Fund , Ausbil Long Short Focus Fund , Candriam Sustainable Global Equity Fund , Ausbil Global Essential Infrastructure Fund (Hedged) , Ausbil Active Dividend Income Fund - Active ETF (ASX: DIVI) , Ausbil Active Sustainable Equity Fund Active ETF (ASX:ASUS) , Ausbil Global Small Cap Active ETF (ASX:GSCF) , Ausbil Global Essential Infrastructure FUnd (Hedged) Active ETF (ASX:GHIF) , Candriam Sustainable Global Equity Fund Active ETF (ASX:GSUS) This article represents the views and opinions of the author(s) at the time of publication and does not necessarily reflect those of FundMonitors.com. It is provided for general information purposes only and does not constitute investment advice or a recommendation to buy or sell any security. The information contained herein is based on sources believed to be reliable at the date of publication, but its accuracy or completeness cannot be guaranteed and may change without notice. Past performance is not indicative of future results. Readers should consider their own investment objectives and seek professional advice before making any financial decisions. This commentary includes forward-looking statements and references to market conditions current as of October 2025, which may no longer be valid after that date. |

14 Oct 2025 - Investment Perspectives: Data Centres - An update is required

13 Oct 2025 - 10k Words | October 2025

|

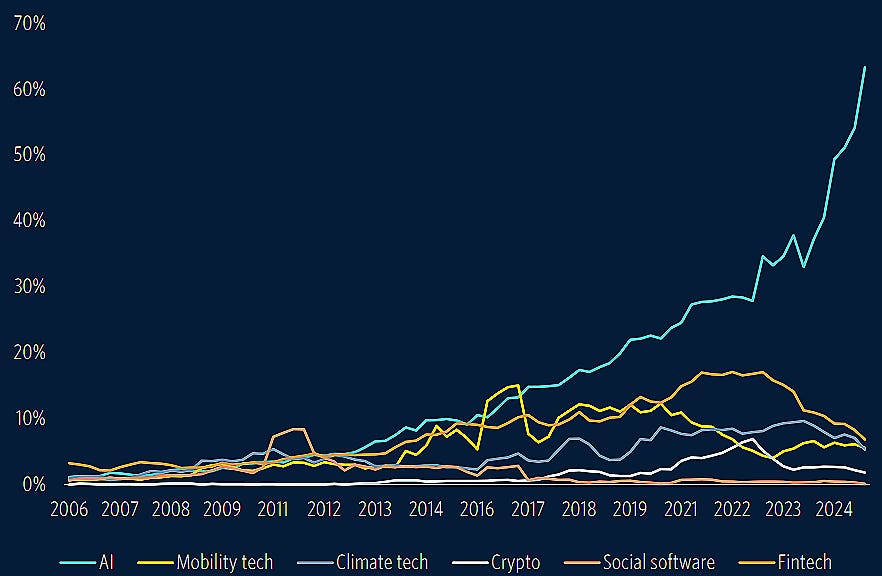

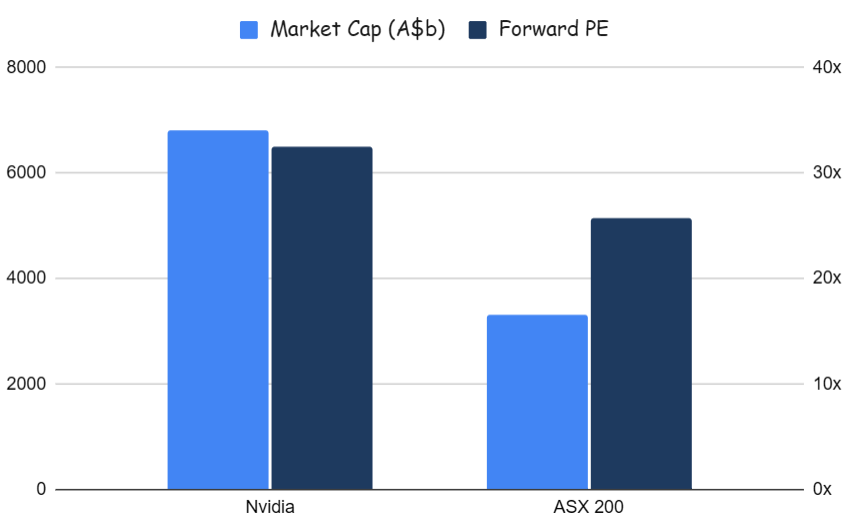

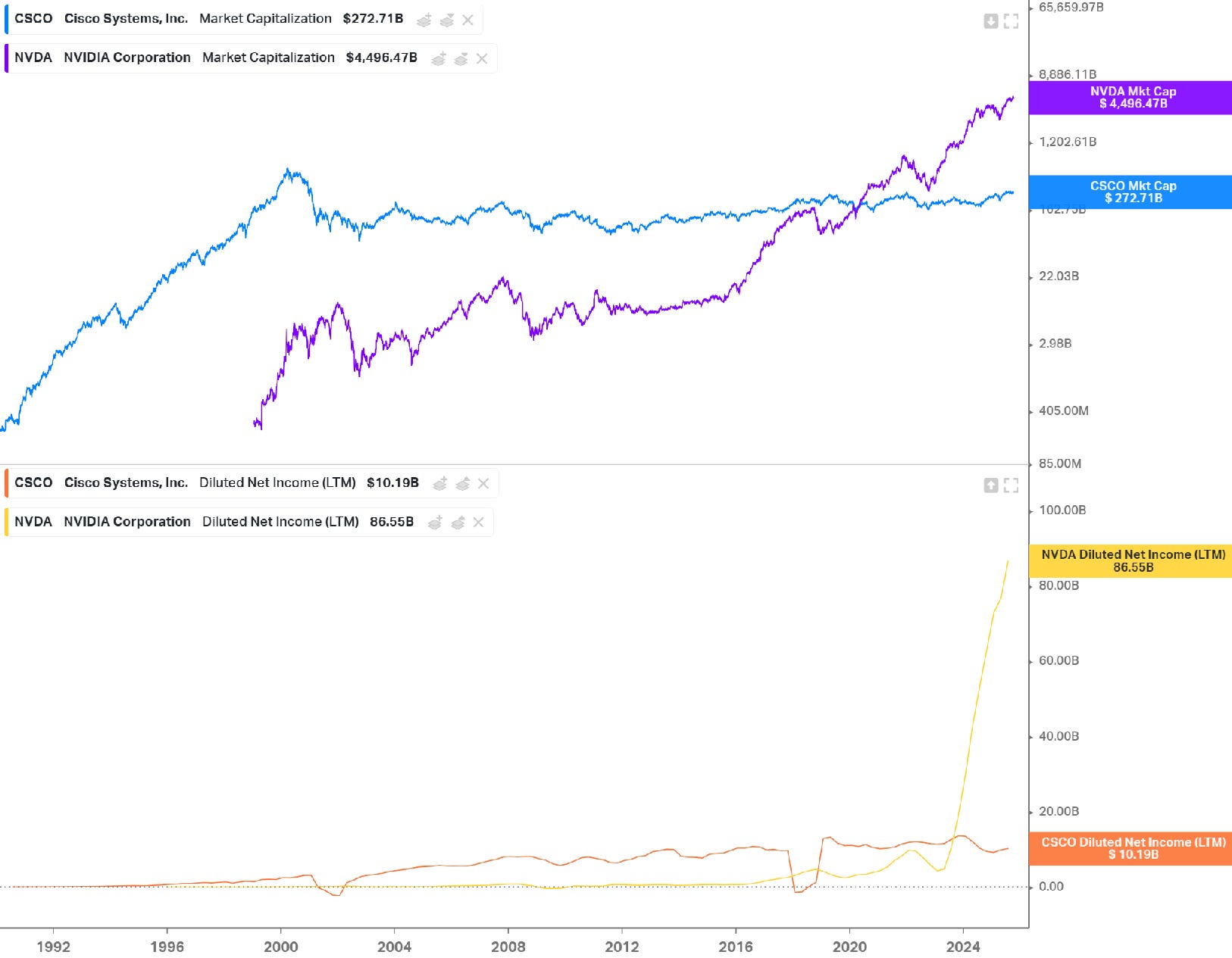

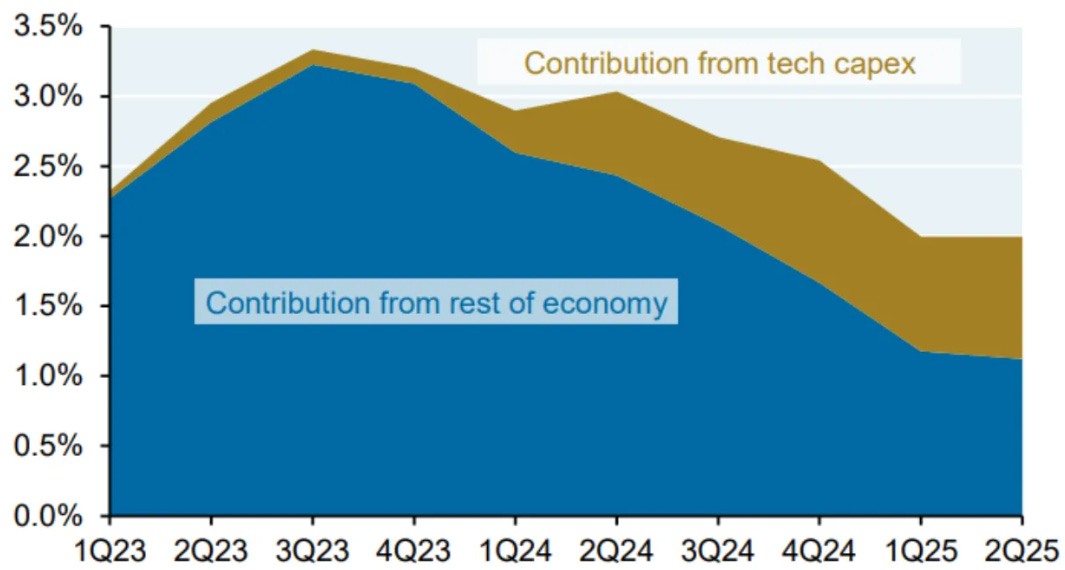

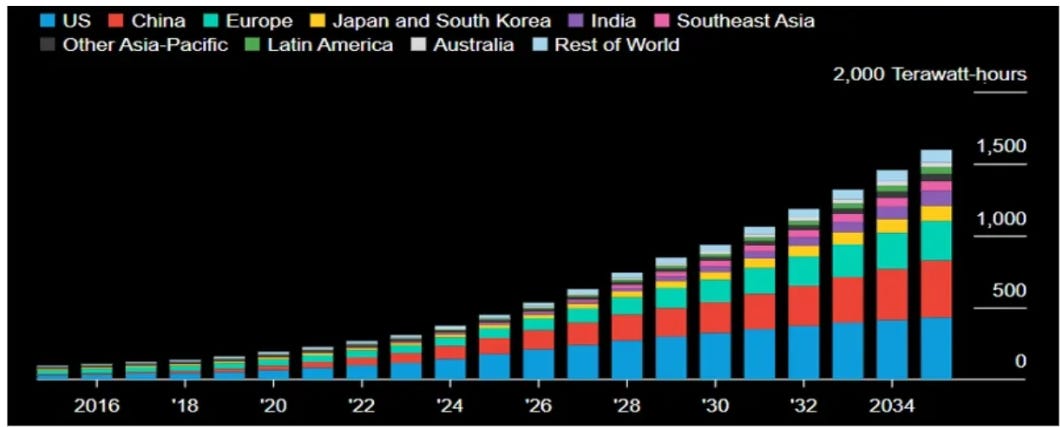

10k Words Equitable Investors October 2025 Small stocks are making up some lost ground with investor interest returning. Size has been the key factor on the ASX over the past 12 months, whereas in the US it has only come to the fore in the past three months. Australian 10 year bond yields have been pretty stable for the past few years but political turmoil in Japan and France shows up in their equivalent bond yields. The extent to which AI is dominating venture funding is unprecedented. But so is the extent to which Nvidia dominates the total value of Australia's top 200 companies. Surging earnings is the difference when comparing Nvidia's valuation to that of Cisco during the dot com boom. The economy is certainly relying more heavily on tech sector capex - and anticipating 4x growth in power demand from AI data centres over the next 10 years. Finally, we still have over 1,000 companies a month entering external administration in Australia, compared to just over 500 a month between FY2020 and FY2023. Record weekly value of trade in S&P/ASX Emerging Companies stocks (5 highest weekly amounts since 2004 v averages)

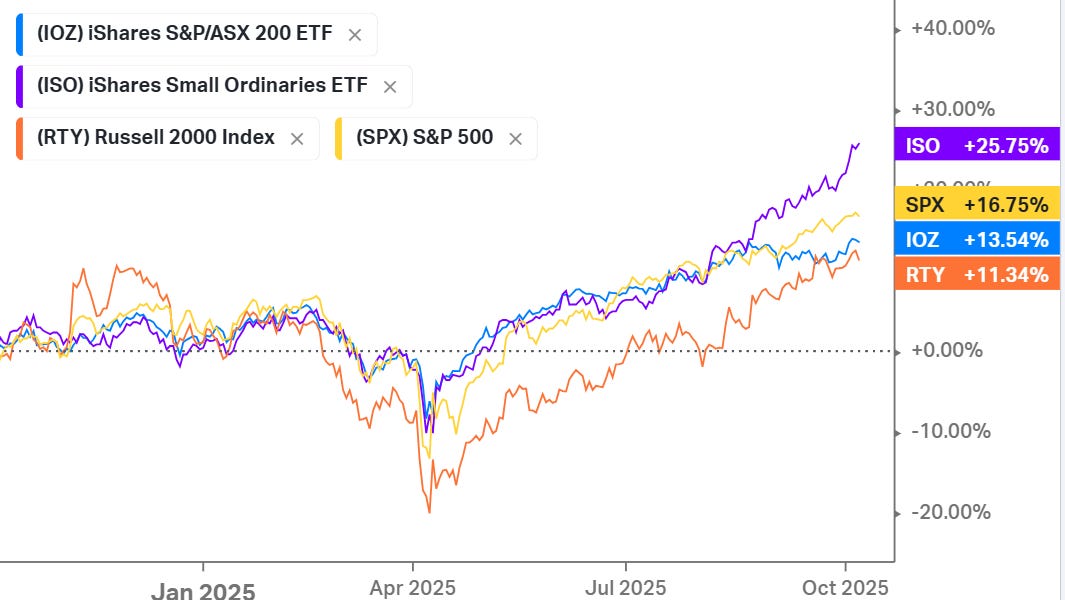

Source: Equitable Investors, Iress One year returns - Australian small caps leading large caps in Aus and US

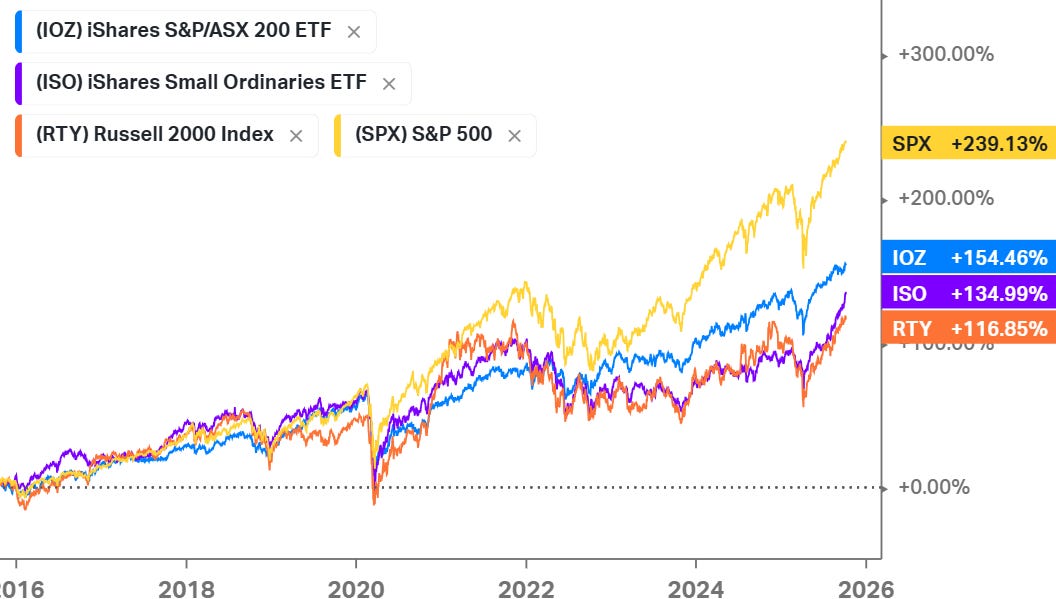

Source: Koyfin Ten year returns - small caps still lagging

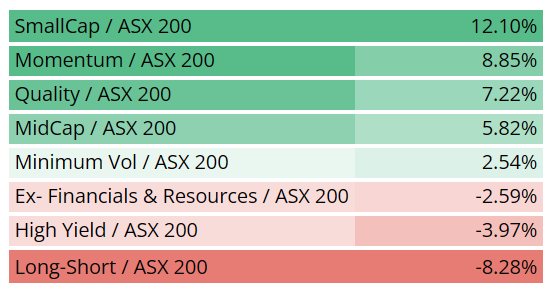

Source: Koyfin ETF-based factor analysis highlgiths size as the key on the ASX over the past 12 months

Source: Equitable Investors US factor ETF performance / S&P 500 ETF performance over past 3 months

Source: Koyfin 10 year Japanese government bond yield

Source: WSJ.com 10 year French government bond yield

Source: WSJ.com 10 year Australian government bond yield

Source: WSJ.com AI's share of value of venture deals over trailing 12 months

Source: PitchBook Nvidia's market cap and PE multiple relative to the S&P/ASX 200

Source: Equitable Investors, Koyfin Cisco v Nvidia in terms of market cap and net income (net profit)

Source: Koyfin US real GDP growth contribution from tech capex

Source: JP Morgan Bridgewater Power demand from AI data centres to quadruple in 10 years according to Bloomberg

Source: Bloomberg NEF The first time an Australian company enters external administration or has a controller appointed - monthly

Soure: ASIC Funds operated by this manager: Equitable Investors Dragonfly Fund Disclaimer Past performance is not a reliable indicator of future performance. Fund returns are quoted net of all fees, expenses and accrued performance fees. Delivery of this report to a recipient should not be relied on as a representation that there has been no change since the preparation date in the affairs or financial condition of the Fund or the Trustee; or that the information contained in this report remains accurate or complete at any time after the preparation date. Equitable Investors Pty Ltd (EI) does not guarantee or make any representation or warranty as to the accuracy or completeness of the information in this report. To the extent permitted by law, EI disclaims all liability that may otherwise arise due to any information in this report being inaccurate or information being omitted. This report does not take into account the particular investment objectives, financial situation and needs of potential investors. Before making a decision to invest in the Fund the recipient should obtain professional advice. This report does not purport to contain all the information that the recipient may require to evaluate a possible investment in the Fund. The recipient should conduct their own independent analysis of the Fund and refer to the current Information Memorandum, which is available from EI. |