NEWS

13 Mar 2026 - Beyond 'Quality at any price'

12 Mar 2026 - Performance Report: ECCM Systematic Trend Fund

[Current Manager Report if available]

12 Mar 2026 - When Geopolitics Moves Markets, Most Portfolios Aren't Ready

|

When Geopolitics Moves Markets, Most Portfolios Aren't Ready East Coast Capital Management March 2026 3-minute read There is a particular kind of market risk that doesn't show up cleanly in a spreadsheet. It doesn't follow earnings seasons or central bank calendars. It arrives through a headline, a border dispute, a sanctions announcement - and by the time most investors have processed it, the repricing has already begun. Geopolitical risk is not new. But the current environment has a different character to it. What we are seeing is not a series of isolated shocks, but an accumulation of structural pressures: fractured supply chains, sustained conflict, and policy unpredictability operating simultaneously across multiple geographies. That combination has a way of staying in markets longer, and running deeper, than a single event. The question for investors is not whether this will eventually resolve. It's whether their portfolios are positioned to navigate the period before it does. What Markets Are Actually Signalling In periods of genuine geopolitical stress, the signal tends to show up in commodities and currencies before it surfaces in equities. Energy markets become a key transmission mechanism: oil price volatility doesn't just reflect supply anxiety, it flows directly into inflation expectations, corporate cost structures, and consumer sentiment. We have seen exactly this dynamic play out. Supply disruptions have kept energy markets volatile and directional. Currency markets have repriced on shifting capital flows and policy divergence. These are not peripheral markets - they sit at the centre of how geopolitical stress propagates through the real economy. Systematic trend following is well-suited to precisely this environment. Not because it predicts geopolitical outcomes (it doesn't) but because it is built to detect and follow the price trends that geopolitical stress tends to produce. When energy trends, it captures energy. When currencies move on safe-haven flows, it captures that too. The strategy doesn't need to know why a trend is happening. It needs to know that it is. The Diversification Assumption Worth Re-examining Most portfolios carry an implicit assumption: that diversification across asset classes will provide protection when conditions deteriorate. In stable regimes, this assumption generally holds. In stress regimes, it often doesn't. When a single macro force - geopolitical risk, an energy shock, a sudden policy reversal - moves through markets simultaneously, assets that appeared uncorrelated begin moving together. The diversification that looked sound on paper compresses exactly when it needs to expand. This is not a flaw to be corrected with more asset classes. It is a feature of how modern markets behave under stress, and it requires a different solution: exposure to return streams that are structurally independent of traditional beta, rather than just spread more widely across it. "True diversification isn't about just holding more assets," says Simone Haslinger, CEO of East Coast Capital Management. "It's about holding assets that behave differently when conditions become difficult. That's a higher bar -- and it's the bar that matters." A Framework Built for Uncertainty, Not Despite It At ECCM, we are often asked how trend following performs in "normal" markets. The reality is that trend following is designed for the full range of market conditions, but it tends to earn its keep most visibly in environments like the current one. Geopolitical stress produces the extended, directional moves across commodities, currencies, and rates that trend following is built to capture. Elevated volatility, far from being a headwind, is the raw material the strategy works with. And because our approach is rules-based, it doesn't require us to take a view on how a conflict resolves, which policy will be enacted, or how long uncertainty will persist. The price action tells us what we need to know. This matters in practice. When uncertainty is high, discretionary decision-making is most prone to error: anchoring to prior regimes, hesitating at inflection points, or seeking safety in familiar assets regardless of what the trends are telling them. A systematic process removes that vulnerability. Conclusion Geopolitical uncertainty is not a phase to be endured while waiting for markets to normalise. For investors with the right framework in place, it is a productive environment - one that generates the kind of clear, sustained trends that systematic strategies are built to capture. At ECCM, our ECCM Systematic Trend Fund is designed to do exactly that: to respond to what markets are doing, wherever the opportunity arises, and to deliver return streams that remain genuinely uncorrelated to traditional portfolios through periods of stress and stability alike. Wholesale clients can find more information on ECCM and the ECCM Systematic Trend Fund at Australian Fund Monitors and ECCM's website. Funds operated by this manager: |

12 Mar 2026 - Performance Report: Altor AltFi Income Fund

[Current Manager Report if available]

11 Mar 2026 - Performance Report: Airlie Australian Share Fund

[Current Manager Report if available]

11 Mar 2026 - Beyond scale: rethinking the engine room of European infrastructure

|

Beyond scale: rethinking the engine room of European infrastructure abrdn February 2026 (4-minute read) The prevailing narrative in infrastructure favours scale. Large funds, large assets, and large ambitions dominate the conversation. Yet, as Europe's energy transition continues and policy reforms reshape the investment landscape, it's increasingly clear that meaningful progress is being driven by the small- and mid-cap segments. Transactions below €500 million account for the majority of European infrastructure deals. This is the centre of gravity for new investment and innovation. Our experience over more than a decade - with around €3 billion invested across energy, transport and digital infrastructure - consistently points to the same conclusion. The lower mid-market is where policy ambition, operational delivery and investor returns align most effectively. There's less need for intermediaries, and it's materially less competitive. This gives space for genuine value creation, rather than simply financial engineering. Policy tailwinds and competitive advantageRecent reforms in the EU's market design for electricity, quicker permit approvals, and the Net-Zero Industry Act have shifted the balance in favour of assets that can adapt quickly and align with local policy priorities. Small- and mid-cap platforms have a structural advantage. In practice, this means utilities that work constructively with municipalities, transport assets embedded within national and regional strategies, and energy platforms that can adapt business models as subsidy regimes and security-of-supply priorities evolve. Large, centralised assets often struggle to respond at this pace. Risk, value and evidenceThe notion that smaller assets are riskier doesn't stand up to scrutiny. In regulated sectors, risk is defined far more by framework stability and governance quality than by asset size. Our utility investments in Finland, for example, operate under the same regulatory regimes as larger peers, yet benefit from more conservative capital structures and greater scope for hands-on asset management. Agility, local solutions and systemic changeSmall- and mid-cap assets move at a different pace. Development timelines are shorter, adaptation is faster, and innovation is less encumbered by bureaucracy. In Finland, this has enabled the rapid deployment of electric boilers to exploit periods of low-cost renewable power, the co-location of data centres to capture waste heat, and the diversification of fuel sources within district heating networks to improve resilience. These initiatives were delivered through close engagement with management teams and local authorities, and implemented within months rather than years. Final thoughts...The infrastructure required to support Europe's changing economy won't be delivered solely by megaprojects or flagship assets. It will be built incrementally, through thousands of local decisions across infrastructure systems. It will also be shaped by those who can combine agility, results, and local insight to deliver measurable outcomes - especially as policy and competitiveness trends continue to evolve. |

|

Funds operated by this manager: abrdn Sustainable Asian Opportunities Fund , abrdn Emerging Markets Equity Fund , abrdn Sustainable International Equities Fund , abrdn Global Corporate Bond Fund (Class A)

|

10 Mar 2026 - Performance Report: Quay Global Real Estate Fund (Unhedged)

[Current Manager Report if available]

10 Mar 2026 - Performance Report: Bennelong Concentrated Australian Equities Fund

[Current Manager Report if available]

10 Mar 2026 - Ben McVicar discusses the data centre effect

|

Ben McVicar discusses the data centre effect Magellan Investment Partners February 2026 (6-minute read) |

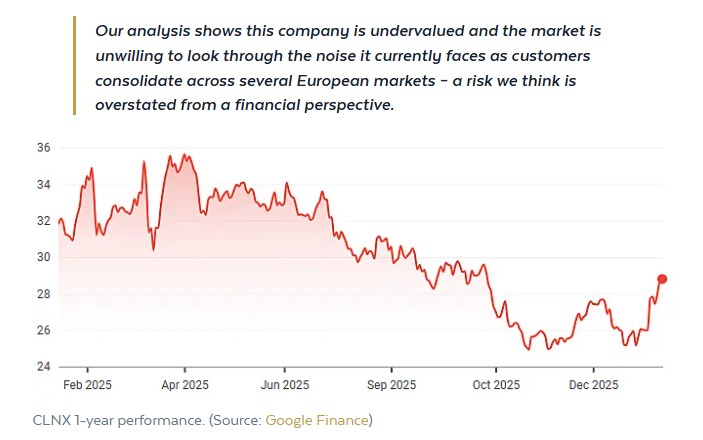

Power demand is rising again. And this time, it is not a short-term cycle.Ben McVicar, Co-Head of Infrastructure and Portfolio Manager at Magellan, sees a decisive shift underway. "There's an upswing in power demand that is data centre related." After more than a decade where electricity demand barely moved, data centres are changing the equation. Systems that once operated in a world of flat consumption are now under pressure to expand capacity and fund the next wave of build-out. That shift matters. In this Q&A, McVicar explains where he believes the market is misreading the landscape, how supply constraints are shaping investment decisions, and why patience remains a competitive advantage. What's your most recent investment and why?We operate a low-turnover portfolio, but one of the more substantial positions we have entered of late is Cellnex (BME: CLNX). The business is the largest mobile tower company in Europe.

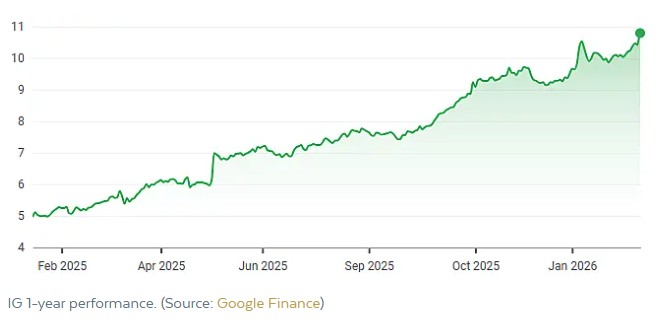

Which investment did you add to your watchlist this week?We have a universe of about 130-140 companies. It's a tightly defined list, so not a lot falls in and out often. These are all high-grade infrastructure companies that have met the quality thresholds we require. So the watch list doesn't change too much. But things move up and down on our radar. The companies highest on our radar are the mobile phone tower companies like Cellnex, but also its peers across the Atlantic. What is the most recent investment you have trimmed or sold and what drove this decision?We have trimmed our position in Italgas (BIT: IG) after a very strong run. This is a gas utility in Italy that is run by a very strong management team. They acquired the second-largest gas network in Italy and expect to create significant synergies from the combined company. But as the price has gone up, the opportunity has narrowed.

What's your favourite chart or data point from this week?

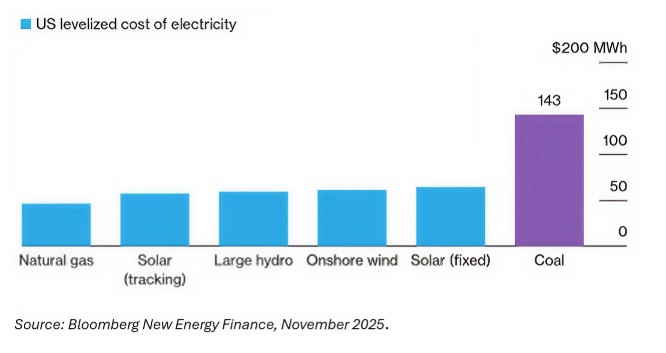

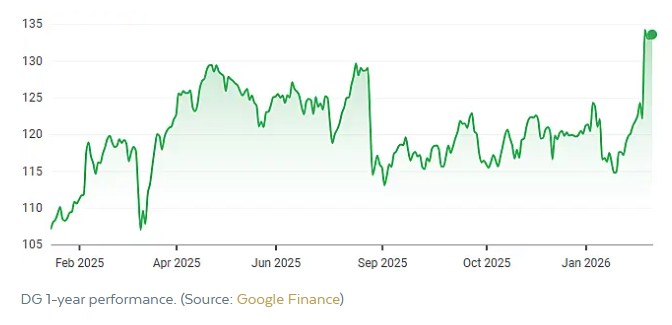

This shows the levelised cost of energy estimates. There's an upswing in power demand that is data centre related. This is a change from the 2005-2020 experience, where power demand growth was limited. This is leading to pressure to develop new power capacity. Gas generation is viable but constrained by supply chain bottlenecks. This makes renewables the most cost-effective and available source of new power. Combined with national and corporate carbon targets, this explains the ongoing investment we're seeing in the technologies. What was your weekly high - a standout market moment or highlightVinci (EPA: DG), a French infrastructure and contracting business, went up almost double-digit on its results. This is a long-standing position, and we've added to it during dips caused by French political turmoil. It's good to see the market focused on the robust fundamentals of this business.

What was your weekly low - a market disappointment or challenge?Customer power prices have gone up as demand has gone up in many regions. In the US utilities, we're diving into the risks and opportunities that come from the outlook of customer rate affordability and the impacts of an election year in many states. What first drew you to markets and what continues to keep you inspired today?I knew I wanted to be an investor before I even started uni. The craft of investing, finding opportunity and building a portfolio to take advantage of these opportunities while managing risk is an endlessly interesting job to be in. What's one piece of advice you'd give to new investors?Be patient, don't overestimate your abilities and wait for the opportunity that jumps off the page at you. You'll know it when you see it. How do you unwind when you're not thinking about the market?Why would you do that? But seriously, exercise. I find I need active 'rest' to stop me thinking about different opportunities or problems I'm focused on in markets. Rapid fire!Favourite investing book? Snowball by Alice Schroeder. Favourite investing or finance/markets-related podcast? I enjoy listening to learn new ideas - the Knowledge Project Podcast (Shane Parish). The first thing you read each morning? I check how the portfolio is trading and then get onto the international press (FT, etc.). Favourite restaurant? Continental Deli - Newtown. Something people are surprised to learn about you? I first started dating my (now) wife when I was 16 and she was 15. I get the impression it's unusual for my generation! |

|

Funds operated by this manager: Vinva Global Alpha Fund - Active ETF (ASX: V1AC) , Vinva Australian Equity Fund , Vinva Global Equity Fund , Vinva Australian Alpha Extension Fund , Vinva Global Alpha Extension Fund , Magellan Infrastructure Fund , Magellan Global Opportunities Fund No.2 , Magellan Infrastructure Fund (Unhedged) , Magellan Core Infrastructure Fund , Magellan Global Opportunities Fund Active ETF (ASX:OPPT) Important Information: This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 trading as Magellan Investment Partners ('Magellan Investment Partners') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision about whether to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to a Magellan Investment Partners financial product may be obtained by calling +61 2 9235 4888 or by visiting www.magellaninvestmentpartners.com Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of a Magellan Investment Partners financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. No guarantee is made that such information is accurate, complete or timely and no warranty is given regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Magellan Investment Partners or the third party responsible for making those statements (as relevant). Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. No representation or warranty is made with respect to the accuracy or completeness of any of the information contained in this material. Magellan Investment Partners will not be responsible or liable for any losses arising from your use or reliance upon any part of the information contained in this material. Any third-party trademarks contained herein are the property of their respective owners and Magellan Investment Partners claims no ownership in, nor any affiliation with, such trademarks. Any third-party trademarks contained herein are the property of their respective owners, are used for information purposes and only to identify the company names or brands of their respective owners, and no affiliation, sponsorship or endorsement should be inferred from such use. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Magellan Investment Partners. (080825-#W17) |

9 Mar 2026 - Performance Report: 4D Global Infrastructure Fund (Unhedged)

[Current Manager Report if available]