NEWS

3 Jun 2021 - Why we sold out of Redbubble

|

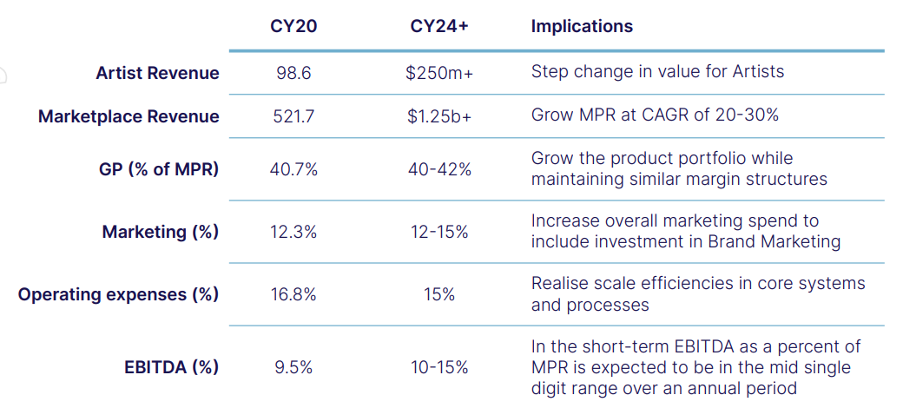

Why we sold out of Redbubble Joseph Kim, Portfolio Manager, Montgomery Investment Management 24 May 2021 Most articles we read are about hot stock tips to buy. Occasionally there are articles about "shorting" opportunities, albeit most are directed to sophisticated investors given the risks around shorting (i.e. a potential loss that exceeds your initial investment). Very few articles talk about when to sell. However, it can be just as important to know when to sell as when and what to buy, a key skill in active management. The Redbubble thesis revisited Last year, we highlighted Redbubble as a COVID winner with global aspirations. The business was a significant beneficiary of lockdowns and stimulus payments - with their years and dollars of investment in the artist platform, logistics and supply chains - paying dividends during the global e-commerce boom, especially in their key US markets. The company's execution during this period was stellar as it managed the significant spike in sales volume during the COVID work-from-home period. It was quick to take advantage of the boom in facemask demand - an entirely new product category - which immediately became a major contributor to revenue. The marketplace platform also demonstrated the power of operating leverage, as 96 per cent growth in Revenue delivered 1,028 per cent growth in EBITDA (albeit off a low base) in the December 2020 half. Incremental margins of 25-30 per cent helped drive improved profitability. The Redbubble flywheel helped generate interest during lockdowns, with significant social media interest on Tik Tok and Twitter as well as more mainstream media articles drive users. With all these positive tailwinds, why did we sell out of our holding in Redbubble? In my previous article, the empirical paper "Selling Fast, Buying Slow" referred to three discrepancies between the buying and selling performance of investors:

It is the final point which is relevant in our decision to sell our remaining holding. Assessing earnings risk At Montgomery, we not only focus on the price vs valuation of our investments but also the earnings risks - either higher or lower than market estimates. In many cases, it is these earnings risks that provide significant upside or downside potential relative to the current share price - especially for less mature businesses - as they drive the growth trajectory of future earnings. For Redbubble, the share price faced its first significant road-bump following its DecH20 result released in February. The update revealed some additional costs related to paid acquisition and shipping, as well as reduced gross margins related to promotional activity in the December quarter. Some of these took the market by surprise, and the share price sold off ~15 per cent in the weeks following the release as it too caught up in the broader "rotation" out of e-commerce winners. Earnings risk assessed for March quarter underpins exit thesis The next stock-specific catalyst was the March quarter sales update. With the share price re-based to $5-6/sh after some margin-related earnings downgrades, it was important to assess the likely trajectory of earnings for the June half of FY21. There were two key areas that underpinned our decision to sell prior to Redbubble's March quarter earnings release: Contribution of face masks to revenue While many investors were aware of facemasks being a significant contributor to revenue growth, there were few estimates of the quantum of revenue contribution. After peaking at ~25 per cent of revenue in July, we assessed facemasks had declined to ~5-7 per cent of revenue exiting December. This has a significant impact not only for Redbubble's revenue for March, but also the difficulty in "comping" elevated face-masks sales that were unlikely to be repeated in the September quarter 2021. We also assumed even if COVID did not recede, facemasks were unlikely to be a significant repeat contributor in the key US market due to i) greater competition in masks; and ii) warmer months in the northern hemisphere in conjunction with vaccine roll-out. Impact of currency on revenue growth Given the volatile moves in currency and the US' contribution to revenue, this represented a significant swing factor in our estimates of Redbubble's revenue trajectory. With >70 per cent of Redbubble's revenue from North America and the strength of the AUD vs USD, this represented ~15 per cent headwind to its top line versus the prior comparative period, which we assessed had yet to be fully factored in market earnings estimates. Where we could have been wrong While the decision to sell ahead of its April earnings release may appear to be obvious in hindsight, there were factors which we had to consider where we may be wrong:

All of these factors (and other unexpected positive developments) may have resulted in a higher share price. Despite this, we deemed the risk skew to the earnings and subsequent share price impact was to the downside. Where to given sell-off? With the Redbubble share price having re-based once again (more significantly than we had anticipated) - and with incremental new future sales targets, earnings and profit margins and investment focus areas, it may be worth re-assessing the shares once again as an investment opportunity.

Many of the aspects which initially attracted us to the Redbubble business - the flywheel, operating leverage, investment in supply chains, global reach and aspirations - remains intact. There is also increased awareness of the Redbubble brand given the spike in website viewer traffic and new customers acquired during COVID. It is also clearly a much more valuable company coming out of COVID than it was going in, and should new CEO Michael Ilczynski and the Redbubble team start delivering on its aspirational targets, will likely become more valuable over time. Funds operated by this manager: Montgomery (Private) Fund, Montgomery Alpha Plus Fund, Montgomery Small Companies Fund, The Montgomery Fund |

2 Jun 2021 - Manager Insights: ESG | Longlead Capital Partners

|

ESG investments grew considerably in the Asia-Pacific region in 2020 and there were a number of net-zero emissions targets released by Asia-Pacific countries in late 2020. Dr. Andrew West, Managing Director & Founder of Longlead Capital Partners, speaks about how this has changed the way Longlead look at companies and build their portfolio.

|

31 May 2021 - Manager Insights | Longlead Capital Partners

|

Damen Purcell, COO of Australian Fund Monitors, speaks with Dr. Andrew West, Managing Director and Founder at Longlead Capital Partners. Andrew discusses the structural growth opportunities Longlead is looking at and shares his views on how the rotation to value in global markets has affected Longlead's investment universe. The Longlead Pan-Asian Absolute Return Fund is an equity long/short fund investing in the Asia Pacific region. The Fund started in December 2020 and has risen +5.22% CYTD.

|

27 May 2021 - Australian Private Equity Well Positioned to Outperform

|

Australian Private Equity Well Positioned to Outperform Michael Tobin, Vantage Asset Management 25 May 2021 With Australia now emerging from its first recession in 29 years as a result of the slowing economy caused by the COVID-19 restrictions in 2020, it is timely to compare the historical performance of the Australian & New Zealand Private Equity market across all time frames, to the performance of those Private Equity funds that were established during, or otherwise invested across, previous recessionary periods. Summary statistics provided by AVCAL & Cambridge Associates reveal that the median and upper quartile net returns from Private Equity funds formed in Australia and New Zealand, between 1997 and 2018, focused on the later expansion and buyout financing stage, in which Vantage funds invest, was 11.1% p.a. and 20.3% p.a. respectively. These robust returns demonstrate Private Equity's ability to consistently outperform public markets as the return on the S&P ASX 200 Accumulation Index over the corresponding period was only 8.4% p.a.1. However, during periods of economic contraction, the performance of Private Equity was even more pronounced. Utilising data provided by Preqin (2020) 2, Vantage conducted an analysis of the investment returns delivered by Private Equity Funds during the recessionary periods following the "dot-com crash" in 2000 and the Global Financial Crisis (GFC) of 2008 to 2010. Australian and New Zealand Private Equity funds, focused on investing in the lower to mid-market segment, investing during and up to 2 years following these events generated median and upper quartile net returns of 19.6% p.a. and 45.0% p.a. respectively, significantly outperforming the public market comparables during these periods. WEIGHTED AVERAGE NET IRR % PERFORMANCE OF AUSTRALIAN & NEW ZEALAND PRIVATE EQUITY FUNDS The reason for this outperformance is due to a number of factors which include an increase in opportunities, less competition from listed and trade purchasers and an ultimate decrease in purchase multiples. Vantage's underlying managers' report that purchase multiples have followed a similar downward trajectory to that seen following the dot-com crash and the GFC, providing an increase in the number of attractive investment opportunities. As a result, it is likely that Private Equity funds investing during and following this recessionary period of 2020 - 2023 will more likely outperform historical returns, due to lower purchase multiples combined with the low interest rate environment and ample deployable capital available to be invested. A number of academic papers have analysed and reported on Private Equity's resilience versus non-Private Equity backed peers during past economic downturns. Research conducted by Wilson et la. (2012) 3, from a data set of 14 million financial records, found that Private Equity backed businesses in the United Kingdom during the period 1995 - 2010, experienced significantly positive growth, relative to peers that were non-Private Equity backed throughout the 2008 crisis. Further highlighting Private Equity's resilience during the GFC period, A recent Stanford Business School study, titled "Private Equity and Financial Fragility During the Crisis" by Bernstein, Lerner & Mezzanotti (2017) 4, confirmed that Private Equity backed companies are significantly more resilient and can act as an economic stabiliser during a recession. In the study, Private Equity lead companies were found to be less likely to face financial constraints during an economic downturn such as the GFC, allowing them to grow and increase market share versus their peers throughout the same period. Arguably the current economic contraction has signified the beginning of a new cycle in financial markets and the end of a prolonged period of asset inflation and increasing acquisition multiples. As a result, there will be an increase in attractive investment opportunities for Vantage's underlying Private Equity managers to invest capital at lower than historical valuation multiples, throughout the second half of the calendar year 2020 and into 2021. This re-rating of asset prices and Private Equity's ability to consistently outperform during and following recessionary periods, will ultimately deliver Vantage Fund investors with superior risk adjusted returns over the term of each Vantage Fund. References

Past performance is not necessarily indicative of future performance. Funds operated by this manager: |

26 May 2021 - Webinar Invitation | Cryptocurrencies

|

|

|

Thursday, June 03, 2021 4:30 PM AEST Webinar - Cryptocurrencies

Interest in Bitcoin and other crypto currencies has accelerated recently in large part due to media coverage, and human nature which dictates that a relatively small outlay which leads to a massive payoff is seen as a reasonable "bet" - somewhat like buying a lottery ticket, but probably with better odds. That doesn't help the majority of people who're attracted by the risk/reward payoff, but either don't know where to start, or even if they did, don't believe they have the skills, expertise or time to enter the market. As a result we have organised a webinar to be held on Thursday June 3rd at 4:30 to try to clarify what to many is the unknown world of crypto currencies and for those - believers and disbelievers alike - who'd like to know more but perhaps didn't know where to start, or want to understand how to avoid the risks.

Time: 04:30 PM AEST Date: Thursday the 3rd of June, 2021

We look forward to seeing you there! |

|

|

Speakers |

|

|

Clint Maddock |

| CIO, Digital Asset Management | |

| Clint is founder of Sydney based Digital Asset Funds Management (DAFM), and CIO of their newly launched Digital Asset Fund. Clint heads DAFM's team of over 20 financial markets and software professionals and has over 17 years experience trading complex derivative products with an impressive CV that includes studying Aerospace Engineering before co-founding Tibra, a high frequency trading operation, in 2006. | |

|

Chris Gosselin |

| CEO, Australian Fund Monitors | |

| Australian Fund Monitors Pty Ltd was established in October 2006 to provide an information service to investors interested in the Australian Absolute Return sector. By providing an "eyes and ears" information and analysis service, both investors and Fund Managers are able to compare different funds and investment strategies using a common format and consistent analysis tools. As Founder and CEO, Chris has over 30 years experience in the Financial Services industry, including managing Macquarie Equities' and HSBC James Capel's Melbourne offices prior to establishing InfoChoice Ltd in 1993. | |

|

|

|

25 May 2021 - Are we in a commodities supercycle?

|

Are we in a commodities supercycle? Tom Stevenson, Investment Director, Fidelity International 5th May 2021 There's nothing like a big round number to concentrate the mind. Investors, in particular, have a tendency to get excited about arbitrary price points with an abundance of zeroes. Think the 1999 best-seller 'Dow 36,000' (we're still waiting but not for long, I suspect). Last week's big round number was 10,000 - the price in (US) dollars for a tonne of copper. It was the first time the metal, which is used in everything from kettles to electric vehicles and wind turbines, had fetched that price since the peak of the last industrial metals upswing in 2011. When you consider that you could have bought a tonne of copper for US$4,300 a year ago, the recent rise is quite something. It is hardly surprising that talk of a commodities boom is picking up. And not just any old rally; what's getting investors excited is the prospect of a commodities supercycle. Most industries are cyclical to an extent, but commodities are more so than most because the price of metals, crops and energy are closely tied to real day to day supply and demand. The price of a share can be sustained by hopes for future growth in earnings, but the cost of a tonne of copper reflects the balance of buyers and sellers today. This means that commodities are always moving in mini bull and bear markets. Rising demand and constrained supply pushes prices higher and that, in turn, creates the oversupply that brings the market back into balance. A supercycle is different. It is always driven by some kind of structural change in which demand is transformed over a period of many years, and usually all around the world at the same time. The mass production of motor cars in the early part of the last century, and then the growth of aviation, fundamentally changed the supply/demand dynamic for oil, for example. Commodity supercycles are not that common, but when they kick in they last for years. There have probably only been four proper ones in the past 150 years. The first was triggered by American industrialisation and urbanisation, fuelled by the US's railway boom and accelerated by the First World War's demand for armaments. The causes of the other three are well-known: the post-war recovery in Europe and Japan; the 1970s oil shock, boosted by Lyndon Johnson's Wars on Poverty and in Vietnam, and the space race; and China's rapid growth after it joined the World Trade Organisation in 2000. So, the big question today is whether the recent price signals, from copper (which has doubled in a year), iron ore, nickel, zinc and other metals, indicate a temporary upswing as the world emerges from the Covid pandemic or the start of something more substantial. The answer to that question may well be one of the most important for investors today. It's easy to make the case for a short-term bull market in commodities. The economic data around the world in recent weeks has surprised economists if not stock market investors who identified the possibility of a V-shaped recovery in activity a year ago. Coupled with short-term supply interruptions due to the pandemic, and longer-term constraints thanks to a decade of falling prices, it's no surprise that prices should have bolted in recent months. What's more interesting, however, is the potential for that all-important multi-decade shift in demand. And for that you need look no further than the twin drivers of Joe Biden's transformational spending programme and the energy transition that has the potential to absorb however many trillions of dollars the world's big-spending governments want to print. A third of Biden's so-called American Jobs Plan is earmarked for transport infrastructure and electric vehicles. China, too, has decided that electric vehicles will be the mainstream option within 15 years. Here in Europe, time has already been called on the internal combustion engine over the next decade or so. By 2040, Wood Mackenzie forecasts, there could be 300 million electric vehicles on the world's roads. In 2019 there were 5 million. And that is just cars. Factor in green energy generation, let alone the once in a hundred years rebuilding of crumbling infrastructure on both sides of the Atlantic, and the demand for green metals like copper, nickel, aluminium and platinum is likely to soar. Glencore, the commodities trader and mining company, thinks demand for copper could double in 30 years. Importantly, capital investment in new capacity is well below what is needed to meet that growth in demand. Of the more than 200 big copper deposits to have been found in the past three decades, only a handful have come in the last 10 years. Only 80 or so are now in production or have been closed. It takes years to develop a copper mine and in recent years shareholders have encouraged the payment of dividends over preparing for a future boom. So, how might investors position themselves for the supercycle ahead? The simplest and cheapest way is via a commodities-focused exchange traded fund. There are plenty of different flavours but a broad-based exposure to metals and energy makes sense. To turbo-charge returns in the event of a prolonged upswing, investing directly in commodity producers is a better idea. With relatively fixed costs, miners' and oil companies' earnings will rise more quickly than the price of their underlying resources. The other advantage of investing in commodity-related shares is that they can also deliver a high and sustainable dividend income. The combination of price gains and re-invested dividends over the duration of a typical supercycle might point you towards your own big round number. Funds operated by this manager: Fidelity Australian Equities Fund, Fidelity Future Leaders Fund, Fidelity India Fund, Fidelity Global Emerging Markets Fund, Fidelity China Fund, Fidelity Asia Fund

|

24 May 2021 - The Capital Cycle: Chasing Narratives vs Owning Cash Flows

|

The Capital Cycle: Chasing Narratives vs Owning Cash Flows AIM 20th of May, 2021 |

|

|

|

Recently, investors have asked why we are not investing in certain sectors that are getting a lot of media attention, and seem to have very exciting growth prospects over the medium to long term. To answer the question, we refer to a framework called 'the Capital Cycle'. It's an analytical framework developed in the 1990s that tries to identify which areas of the market to avoid at a particular moment in time. We would argue it is even more relevant today, given that with interest rates at rock bottom levels, capital is basically free and the likelihood of a misallocation of capital is high. The key insight of the Capital Cycle framework is that investors focus too much on the growth in demand and not nearly enough on the supply-side response. Slide 2 illustrates the four stages of the capital cycle, starting at the 12 o'clock position and going clockwise.

Source: Marathon, 'Capital Returns'

When a new sector is opened up through technological innovation, many potential entrants rightly look to set up a business and claim their slice of the pie. The upside potential of the sector is marketed and the excitement generated leads to a lot of capital being invested in order to capture the opportunity. Everyone is optimistic. However, as more and more people look to enter the industry, competition begins to increase. Margins erode, price wars intensify, and almost everyone ends up losing money for a period. At this point, returns drop below the cost of capital and the equity tends to underperform. With time, the weaker players can no longer afford to compete. They exit the industry, or the more successful players buy them out to begin a process of consolidation. At this stage, investors who have been burned are likely exiting as well. This provides an attractive entry point to long-term investors who've analysed the industry dynamics and can see the consolidation playing out. The consolidation then leads to more rational competition, leading to returns improving to levels above the cost of capital. Equity owners are generally rewarded at this point. Right now, we think we're somewhere between the investor optimism and rising competition phases. An enormous amount of capital has been invested to chase the opportunity in many hot sectors over the past 12 months. Without a defendable moat and rational competition, being able to forecast high levels of demand or a huge total addressable market is ultimately insufficient for investors, since the businesses in question may not be able to economically capture the opportunity to drive value in the industry. Let's make this a bit less theoretical and a bit more practical. Where are we seeing this play out?

Real-world examples It would seem a new buy now pay later service is being launched somewhere around the world every other month. Should one want to invest in BNPL, it is worth looking at it from many angles to fully understand the opportunities and competitive risks. In the next slide, we have taken a simple screenshot from the Officeworks website:

Source: Officeworks.com.au website

There are three BNPL services listed. Other than brand recognition, there is nothing to differentiate the three shown here from each other. Given the intense competition between all the BNPL players, it is unlikely that all of them can win, meaning an investor should consider what will happen when one player starts pulling ahead of its peers. We doubt that players number two and three will go gentle into that good night, meaning that they will likely start to compete on pricing. Possibly they can cut the fees they charge merchants or try and extend the repayment profile to their consumer. It can very quickly become a race to the bottom. We would argue the BNPL business model is also somewhat capital-intensive, in that merchants are generally paid prior to the BNPL provider being paid in full by their customer. To grow aggressively generally requires additional infusions of capital. What happens when capital providers either in the form of debt or equity demand a higher rate of return from the company? Access to cheap, external capital is in our view not a sustainable moat, particularly for companies that effectively run a single line of business, as many of the BNPL operators do. Another area where we have concerns is in the food and grocery delivery space. As recently reported in the Financial Times, there has been an inflow of roughly $14 billion of capital into this sector in recent months. Established businesses, such as Just Eats, Delivery Hero, Uber Eats and Deliveroo are all seeing increased competition in what is already an industry with razor thin margins. The new entrants are using the capital they have raised to effectively subsidize their offering in an attempt to gain market share. This is the equivalent of selling a $3 ice cream for $1 at the beach on a hot summer's day. You can sell as many ice creams as you want, as long as you are prepared to forgo $2 on each. Given the war chest some of these businesses have now raised, they can continue to do this for quite some time. We think this influx of capital will drive down returns for all players for a period of time. Eventually, there will be a shakeout, but in the meantime, consumers will enjoy the benefit of low prices and choice. However, we don't think this makes for an attractive investment opportunity, no matter how good the story is at the moment. And of course, all of this assumes the economics of food and grocery delivery are attractive at maturity, a topic we do not at this stage have a high degree of confidence in. Other sectors where we see similar dynamics playing out are telemedicine, autos and streaming. In a sense, the pandemic may have been the worst thing that could have happened to a business like Netflix, as it forced all their competitors to finally embrace streaming and take it seriously, leading to a surge in high quality content - alongside a step-change in content costs. In this short extract from the AIM quarterly webinar, portfolio manager Etienne Vlok explains why it is time to be clear-eyed about chasing sectors with an exciting "narrative", but without a clearly defined moat to sustainably capture the demand as new competition enters. It is 2 o'clock on the capital cycle clock, and competition is coming. Funds operated by this manager: AIM Global High Conviction Fund |

24 May 2021 - Are we now at the top of the V-shaped recovery?

|

Are we now at the top of the V-Shaped Recovery? Tim Toohey, Yarra Capital Management May 2021 By now most investors are tiring of their inboxes being filled by sell-side economists and strategists talking about reflation, how much more optimistic they are relative to consensus, and for how much longer the reflation trade will persist. To be clear, there were very few people talking about a strong V-shaped recovery this time last year. Indeed, a scan of the forecasts of leading sell side economists in April 2020 shows consensus* forecasts of 3% for the CY21 for Australia and 3.8% for the USA. Indeed, peak pessimism was not reached until September 2020, when economic growth downgrades ceased and modest upgrades commenced. Currently, consensus for CY21 has risen to 5.7% in the USA and 4.4% for Australia. By contrast, our forecasts for the US in 2021 - which we published in mid-April 2020 - was 6.5% (represented by the cross in Chart 1). For Australia (Chart 2) we were even more optimistic, forecasting 7.0% economic growth. As we moved through 2020, it was clear the expected contraction in economic growth in 2020 was going to be less than expected and hence we reduced our forecast rebound in Australia's economic growth in 2021 to a still sizeable 6.0%. Much of our more upbeat analysis was based on: (i) the nature of the shock being more akin to a natural disaster; (ii) the quantum of the fiscal packages; (iii) excess credit growth; (iv) the outlook for vaccine development; (v) and the prospect of pent up demand. One year on, the clambering to upgrade growth estimates has only intensified. Over the past two months, consensus forecasts for Australian economic growth in 2021 have been upgraded a further 0.7%. In the USA the revision over the past 2 months is a remarkable 1.6%. In other words, consensus economic growth forecasts are now more realistic, but the upward revisions are not yet complete and there is still scope for consensus to upgrade economic growth further in coming months to nearer our long held forecasts. Indeed, when we compare our forecasts for economic growth to consensus there are now examples of economic growth forecasts for the US that exceed our forecast. The most notable is the Bank of Canada's recent upgrade of 2021 US economic growth from 5.0% to 7.0%. Given the US is Canada's largest trading partner, the Bank of Canada has a strong incentive to get its US outlook near the mark! The Bank of Canada also lifted its global growth forecast in 2021 to 6.8%, which is 1.25% higher than any global growth year since IMF data commenced (1980) and 0.8% above the IMF's April forecasts! However, one of the largest gaps between consensus and our own 2021 forecasts is for Australia. We remain 1.5% above the consensus forecast and around 1% above the most optimistic forecaster. Given there remains an appreciable gap between our forecasts and other forecasters, it's reasonable to ask what supports our optimism? 1. Australia's data continues to consistently beat economic forecasters Charts 3 and 4 show our calculation of economic data surprises for economic activity and inflation relative to consensus forecasts (US vs Australia). A positive reading represents economic data beating consensus expectations weighted by data importance and time decay. Clearly, Australia's economic activity data is not only continuing to beat increasingly upbeat economic forecasts, the positive data surprises are larger in Australia. 2. Real economic growth is expanding at pace Secondly, our nowcasting techniques (Chart 5) for gauging in real-time how fast the economy is expanding already suggest that real economic growth is expanding at 4%yoy by the end of 1Q2021. That is, we are about to see a very solid 1Q GDP print for Australia that we expect will be the catalyst for a further upgrade of the consensus view.[1] 3. Treasury's projections have been comfortably exceeded Much stronger economic growth, much lower unemployment and much stronger commodity prices have combined to already deliver a $23bn better fiscal outcome relative to Treasury's December projections and closer to a $50bn saving over the next 4 years. The question for Q2 is how much more of an "economic surprise" dividend will likely flow through the Budget and what will the Government do with it? In simple terms, we believe the Treasury's growth figures are 0.5% too low for 2020-21 and 1.25% too low for 2021-22. The unemployment rate is likely too high by as much as 2%. And an iron ore assumption of $55/t embedded in the Budget is currently 1/3rd of the current iron ore price. Clearly there are further major revenue upgrades to come. Our take is that the May Budget will be used mainly to evidence the vastly better Budget and economic outcomes that have been achieved. We expect the true election Budget will come in late 2021 (i.e. mid-year Budget), with more strategic spending and tax changes announced to setup a May 2022 Election. This strategy allows plenty of time for the Coalition to address its problems in WA, QLD and metro Melbourne, where no doubt most of the Budget windfall will be redirected through 2H21. The combination of the Coalition's political challenges and the Budget's economic windfalls will likely spark additional fiscal spending later in 2021, sufficient to bolster economic growth expectations. Mid-2021 will likely mark the peak of global business sentiment surveys and global economic data surprises. It will also mark the final phase of economic growth upgrades. Nevertheless, we believe there is more oxygen in Australia's economic recovery and that consensus has long been too slow to recognise the domestic economy's capacity to expand at close to 6% through 2021. Indeed, recently the RBA used the May Monetary Policy Meeting as a platform for a significant upgrade in economic growth forecasts, in a similar vein to the Bank of Canada's recent upgrade, lifting economic growth to December 2021 to 4.75%, from 3.5% previously. We believe the RBA will further upgrade its economic growth forecasts over the next six months. While this will set off expectations of a higher cash rate ahead of the RBA's 2024 guidance, the RBA can be expected to attempt to allay those fears by making the case that inflation expectations and wage growth remains too low to be consistent with their inflation objective. Nevertheless, the likely RBA growth upgrades will almost certainly end the prospect of the RBA rolling the 3-year bond beyond the April 2024 target. Together with the end of the Term Funding Facility in mid-2021 the reality is that a very modest tightening cycle is already commencing. [1] Our nowcasting methodology is to estimate real time economic growth via both dynamic factor models and principal component models for each of the major economies to provide an alternative underlying picture of economic growth to the often noisier official GDP data. Disclaimer * References to 'consensus' throughout relate to Bloomberg consensus unless otherwise stated. To the extent that this document discusses general market activity, industry or sector trends, or other broad based economic or political conditions, it should be construed as general advice only. To the extent it includes references to specific securities, those references do not constitute a recommendation to buy, sell or hold such security. Yarra Funds Management Limited (ABN 63 005 885 567, AFSL 230 251) believes that the information contained in this document is correct and that any estimates, opinions, conclusions or recommendations contained in this document are reasonably held or made as at the time of publication. Email messages may contain computer viruses or other defects, may not be accurately replicated on other systems, or may be intercepted, deleted or interfered with without the knowledge of the sender or the intended recipient. To the maximum extent permitted by law, Yarra Capital Management Holdings Pty Ltd, Yarra Funds Management Limited, Yarra Capital Management Services Pty Ltd, their related bodies corporate and each of their respective directors, officers and agents (together, the "Yarra Capital Management Group") make no warranties, and expressly disclaim any liability, in relation to the contents of this message. The Yarra Capital Management Group reserves the right to intercept and monitor the content of e-mail messages to and from its systems. This message may contain information that is confidential or privileged, and may be subject to copyright. It is intended solely for the use of the intended recipient (s). If you are not the intended recipient of this communication, please delete and destroy all copies in your possession, notify the sender that you have received this communication in error, and note that any review or dissemination of, or the taking of any action in reliance on, this communication is expressly prohibited. © 2020 Yarra Capital Management. Funds operated by this manager: Yarra Australian Equities Fund, Yarra Emerging Leaders Fund, Yarra Income Plus Fund, Yarra Enhanced Income Fund

|

21 May 2021 - Insights for investors into key trends: housing and consumer markets

|

Insights for investors into key trends: housing and consumer markets Sean Fenton, Sage Capital May 2021 Clear trends and themes have emerged in investment markets as a result of the pandemic and its effect on discretionary and non-discretionary spending and where we live. Exploring these themes was the focus of Sage Capital's recent webinar, which delved into how these dynamics are playing out in Australia and around the world. Bricks and mortar drives markets The webinar provided perspectives on the nature of the current housing boom and how long it can continue. It explored a related theme of consumer spending and how it has shifted one year after the first COVID lockdowns. The housing market cycle was the main theme during the session, given low interest rates the world-over have stimulated a boom in residential property markets. Detached dwellings in particular have benefitted, as people seek more space at home when they are prevented from travelling too far from their homes due to stay-at-home orders and border closures. As a result, apartment prices have not experienced the same gains as stand-alone homes. Flagging demand for inner-city properties is also the result of many people embracing the opportunity to move out of the city given the widespread adoption of the work-from-home way of working. Inner city apartments notwithstanding, the booming housing market isn't just good news for property, it also has flow-on effects to other sectors. The strong residential real estate market has translated to high demand for mortgages, which is good news for lenders and also service providers such as mortgage insurers. It's worth noting the lending sector is strong for another reason. At the start of the pandemic, many lenders made very large bad debt provisions, assuming borrowers would be stretched as a result of the pandemic leading to shut downs in many areas of the economy. These provisions, at least in Australia, have proven to be too generous, largely due to government stimulus programs helping borrowers to meet their obligations and taking the pressure off lenders. While this has been good news for financial institutions and also the housing market, concerns are emerging about whether the market is running too hot. Governments and regulators are also worried about housing affordability. As a result, some countries are taking action to moderate house price growth. As examples, New Zealand has taken steps to cool its housing market and Canada has recently tapered its bond-buying program. The Reserve Bank of Australia has not given any indication it's going to steer away from its lower for longer approach to interest rates. But that does not mean investors should not be informed by actions in other jurisdictions. It's a trend of which our portfolio managers should be aware, as these same trends could play out in other markets. What's happening at the checkout? Turning to consumer spending patterns, one of the fundamentals we're always curious about is the connection between housing market movements and consumer spending, and how this may play out across the investments in our portfolios. Retail spending is highly correlated with house prices. So when house prices are strong, we're much more likely to buy a new car, renovate and buy furniture and appliances. But this trend often reverses as interest rates and home loan repayments rise, and people are less inclined to spend money on non-discretionary items. We are also closely watching shifts in consumer spending as a result of the pandemic, investigating whether and when these shifts normalise and who the winners are in the short- medium- and long-term. When it comes to discretionary and non-discretionary spending, consumers will look for alternate ways to spend their money if recreational travel remains off the table. Which is why Sage Capital has been scouring the market for retailers with a real digital capability that may have been so far largely overlooked by investors. Retailers that are strong omni-channel marketers that have a demonstrated ability to do online fulfilment are well placed, especially those with strong national store networks, so they can easily deliver orders on the same day they are placed. This is a real advantage over online competitors that rely on big fulfilment centres for retail distribution. Achieving same day delivery is going to be very difficult for these operators and require significant capital expenditure to maintain their competitive position. Our ability to add value At Sage Capital, we understand these trends and aim to position the portfolio accordingly. These insights help us form a view on when to rotate in and out of stocks exposed to the housing market and the retail sector. As for the future, there are still many unknowns. These include the COVID-19 vaccination rollout in Australia and around the world and how that may affect international border openings and the future of international travel. The way these themes play out has implications for any investments exposed to the movement of people and goods across borders. These are just some of the themes we have been investigating at Sage Capital and that inform our approach to portfolio management. We look forward to sharing further insights form our webinars in the future. As a long short manager, the investment team is able to use its shorting powers to benefit from a falling market. At the same time, it can go long stocks when markets rise. This investment style, and the diversified nature of the portfolio, helps mitigate risks and provides protection when markets correct. Sage Capital is an Australian long-short equities manager with two investment strategies, the CC Sage Capital Equity Plus Fund and the CC Sage Capital Absolute Return Fund. Long-short strategies are often popular with investors when traditional asset classes are challenged. It's a strategy that aims to provide consistent returns through market cycles. Both Funds have performed well for investors over the one year to 31 March 2021. The CC Sage Capital Equity Plus Fund delivered a net return of 43.59%* and the CC Sage Capital Absolute Return Fund delivered a net return of 9.98%*, outperforming their respective benchmarks for the same period by 6.12% and 9.89%. *Past performance is not indicative of future performance. This information is for Wholesale and Professional Investors only and is provided by the Investment Manager, Sage Capital Pty Ltd ACN 632 839 877 AR No. 001276472 ('Sage Capital'). Channel Investment Management Limited ACN 163 234 240 AFSL 439007 ('CIML') is the responsible entity and issuer of units in the CC Sage Capital Equity Plus Fund ARSN 634 148 913 and the CC Sage Capital Absolute Return Fund ARSN 634 149 287 (collectively 'the Funds'). Channel Capital Pty Ltd ACN 162 591 568 AR No. 001274413 ('Channel') provides investment infrastructure services for Sage Capital and is the holding company of CIML. This information is supplied on the following conditions which are expressly accepted and agreed to by each interested party ('Recipient'). This information does not purport to contain all of the information that may be required to evaluate Sage Capital or the Funds and the Recipient should conduct their own independent review, investigations and analysis of Sage Capital and of the information contained or referred to in this document. This email (including attachments) is subject to copyright, is only intended for the addressee/s, and may contain confidential information. Unauthorised use, copying, or distribution of any part of this email is prohibited. Any use by unintended recipients is expressly prohibited. To the extent permitted, all liability is disclaimed for any loss or damage incurred by any person relying on the information in this email. This communication has been prepared for the purposes of providing general advice, without taking into account your particular investment objectives, financial situation or needs. Past performance is not indicative of future performance. All investments contain risk. An investor should, before making any investment decisions, consider the appropriateness of the information in this communication, and seek professional advice having regard to these matters, any relevant offer document and in particular, you should seek independent financial advice. For further information and before investing, please read the Product Disclosure Statement available from www.sagecap.com.au and www.channelcapital.com.au. Funds operated by this manager: CC Sage Capital Absolute Return Fund, CC Sage Capital Equity Plus Fund |

20 May 2021 - AIM Quarterly Webinar

|

The AIM Investment team discusses why we are at a point in the cycle where it's time to be disciplined. Sectors discussed include streaming, BNPL, food delivery, telemedicine and autos. Funds operated by this manager: |