NEWS

Hedge Clippings | 19 April 2024

US Fed Chair Jerome Powell has been walking back - or talking back - expectations for an imminent rate cut in the US for some time now. At the end of last year, market expectations were for the Fed to cut up to six times this year.

Read more...

Performance Report: Bennelong Twenty20 Australian Equities Fund

The Bennelong Twenty20 Australian Equities Fund rose by +2.03% in March. Since inception in November 2009, the fund has returned +9.88% per annum, an outperformance of +1.64% relative to the ASX 200 Total Return benchmark which has...

Read more...

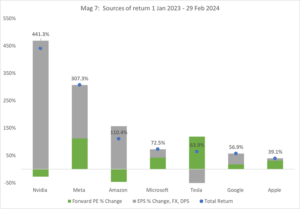

Why 2024 will be a 'show me' year

2023 global equity returns were dominated by an alphabet soup of megatrends. From (Chat)GPT shining the spotlight on the lifechanging potential of Generative Artificial Intelligence (GEN AI), to a broader adoption of Glucagon-Like Peptide...

Read more...

Performance Report: Altor AltFi Income Fund

The Altor AltFi Income Fund rose by +0.75% in March. Since inception in April 2018, the fund has returned +11.86% per annum, a difference of +5.37% relative to the RBA Cash Rate + 5% benchmark which has returned +6.49% on an annualised...

Read more...

An upgrade to the financial system's plumbing

The RBA looks set to re-build our financial system's plumbing. Pendal's head of government bond strategies, Tim Hext, explains what it could mean for investors.

Read more...

Performance Report: Bennelong Emerging Companies Fund

The Bennelong Emerging Companies Fund rose by +1.06% in March. Since inception in November 2017, the fund has returned +18.22% per annum, an outperformance of +9.33% relative to the ASX 200 Total Return benchmark which has returned +8.89%...

Read more...

Performance Report: Argonaut Natural Resources Fund

The Argonaut Natural Resources Fund rose by +7.7% in March, outperforming the S&P/ASX 300 Resources TR benchmark by +3.47%. Since inception in January 2020, the fund has returned +30.63% per annum, an outperformance of +19.95% relative to...

Read more...

Glenmore Asset Management - Market Commentary

Equity markets were stronger in March. In the US, the S&P 500 rose +3.1%, the Nasdaq was up +1.8%, whilst in the UK, the FTSE 100 rose +4.2%. In Australia, the All Ordinaries Accumulation Index rose +3.1%

Read more...

Performance Report: Skerryvore Global Emerging Markets All-Cap Equity Fund

The Skerryvore Global Emerging Markets All-Cap Equity Fund rose by +2.08% in March. Since inception in August 2021, the fund has returned +5.04% per annum, an outperformance of +5.63% relative to the benchmark which has fallen -0.59% on an...

Read more...

Performance Report: Airlie Australian Share Fund

The Airlie Australian Share Fund rose by +3.13% in March. Since inception in June 2018, the fund has returned +11.6% per annum, an outperformance of +2.6% relative to the ASX 200 Total Return benchmark which has returned +9% on an...

Read more...