NEWS

3 Feb 2026 - Global Matters: 2026 Outlook

2 Feb 2026 - Quarterly State of Trend report - Q4 2025

|

Quarterly State of Trend report - Q4 2025 East Coast Capital Management January 2026 3-minute read In this update, we present the quarterly State of Trend report for Q4, 2025. Our report covers the performance of trend following systems compared with traditional investments such as the S&P/ASX 200 Total Return index, and the Australia "60/40" portfolio. Trend following provides exposure to a diverse pool of underlying instruments, and implements trading strategies systematically and without emotional biases. Trend following outperforms Australian traditional assets In Q4 2025, Australian traditional risk assets faced headwinds as policy uncertainty, global growth concerns and persistent inflation volatility weighed on investor sentiment. Trend following systems delivered strong positive returns, benefitting from sustained momentum in metals, international equities and selective currencies. Key market movements in Q4 2025

Featured chart - Silver

See the full report at our website. Funds operated by this manager: |

2 Feb 2026 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

||||||||||||||||||||||

| Blue Owl Credit Income Fund AUT - Class A | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

Orbis Global Equity LE Fund |

||||||||||||||||||||||

|

||||||||||||||||||||||

|

||||||||||||||||||||||

| L1 Capital Gold Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

Want to see more funds? |

||||||||||||||||||||||

|

Subscribe for full access to these funds and over 900 others |

29 Jan 2026 - Navigating EMD: risks, rewards and what's ahead

|

Navigating EMD: risks, rewards and what's ahead abrdn January 2026 (6-minute read) We've been investing in emerging market debt (EMD) for over 30 years, with deep experience across both fast-growing frontier markets and established economies - at the corporate and sovereign level. So, what are the opportunities, risks, innovations and trends in EMD investing today? Read our far-reaching interview with Siddharth Dahiya, Global Head of EMD, to find out. Q: Why should investors consider emerging market debt in 2026 and what are some of the most attractive opportunities?Emerging market debt (EMD) enters 2026 in great shape. Across the asset class, we're seeing a range of positive dynamics. Hard currency sovereigns, for example, are experiencing a wave of ratings upgrades, reversing a decade-long trend of downgrades. This shift signals improving fundamentals and growing resilience across many EM economies. Q: How do you expect the EMD landscape to evolve over the next 12 months?We see the this year as a period of steady momentum rather than dramatic change. What is catching our eye is the growing interest in local currency debt, especially in frontier markets that used to fly under the radar. Investors are starting to take notice, attracted by improving fundamentals and compelling yields in these markets. Q: Which frontier markets stand out as offering unique potential - and what are the risks?Frontier markets present a diverse set of opportunities, each with its own idiosyncratic stories. The risks here are less about broad macro shocks and more about country-specific factors. For example, some frontier economies are heavily reliant on oil exports, making them vulnerable to price swings. Q: Are there thematic strategies within EMD that investors should pay attention to?Several themes are shaping the EMD landscape. The distinction between oil exporters and importers remains important, as does the impact of global tariffs and the ongoing trend towards nearshoring. Q: How do you balance sovereign versus corporate EMD exposure in the current environment?We believe both sovereign and corporate EMD have important roles to play in a well-constructed portfolio. Sovereign debt offers a wider dispersion of ratings, providing access to higher-yielding opportunities, while corporate debt tends to be higher quality, with a greater proportion of investment-grade issuers. Q: What role does currency exposure play in EMD returns, and how do you manage FX risk?Currency moves are a key component of the EMD narrative, especially in local markets. Last year, FX appreciation against the dollar was a significant contributor to performance. Investors can benefit from both currency gains and yield compression in local markets. If the dollar continues to weaken, local currency EMD should remain attractive. Q: How do you see global monetary policy shifts - especially potential rate cuts - impacting EMD performance?Global rate cuts are good news for EMD. Lower risk-free rates enhance the appeal of higher-yielding markets like EM, encouraging investors to seek out additional carry. When US Treasuries offer lower yields, the incentive to allocate to EMD increases, driving inflows and supporting performance. Q: What catalysts could unlock value in EMD over the next year?There are many. Country-specific reforms, successful restructurings, and geopolitical developments could all move the needle. Increased investor attention and flows are also important. Despite EM accounting for around half of global growth, it remains a small portion of most portfolios. A secular shift towards greater EM allocations could unlock significant value for investors. Q: For investors considering EMD today, what allocation strategies make sense - active vs. passive, hard vs. local currency?Active management makes the most sense. The asset class is diverse and idiosyncratic, and evidence shows active managers consistently outperform passive approaches. In such a complex market, skilled security selection, risk assessment and country analysis add meaningful value that passive exposures simply can't replicate. The choice between hard and local currency depends on risk tolerance. Local currency offers greater potential but comes with higher volatility, while hard currency can provide defensive qualities, especially in investment-grade segments. |

|

Funds operated by this manager: abrdn Sustainable Asian Opportunities Fund , abrdn Emerging Markets Equity Fund , abrdn Sustainable International Equities Fund , abrdn Global Corporate Bond Fund (Class A) |

28 Jan 2026 - Trip Insights: Canada - US

21 Jan 2026 - Why collaborating is key to climate change

Why collaborating is key to climate changePendal January 2026 5 minutes read time |

|

WHAT does it take to tackle climate change, food security, or pandemic risk? At the recent PRI Stewardship and Collaboration Forum, the answer was clear: collective action. The United Nations Principles for Responsible Investment (UNPRI) brought together global leaders in sustainable finance. This Sydney forum, hosted by Regnan, convened 45 asset owners, managers, and responsible investment professionals to share insights on collaborative stewardship. Regnan's Grace Zhang presented at a similar event in Melbourne. The power of collective actionInvestors face challenges that are global and demand collective action. Issues such as climate change are beyond the control of one individual company or investor. Investors who view their activities within the context of interconnected, dynamic systems recognise their role in building resilience across the financial ecosystem. This systems-thinking approach has long been central to Regnan's research, engagement, and advocacy. It is why Regnan is actively involved in industry associations and initiatives within the responsible investment industry. Why impact investing? Aligning investments with personal values to have a positive impact on the world while also generating a financial return. Why collaboration mattersCollaboration gives investors access to diverse perspectives, shared intelligence and optimises resources. It also offers greater scale. Regnan has long recognised the importance of bringing voices together to address big challenges. Since Regnan became part of the Perpetual Group, stewardship opportunities have been amplified. This represents greater funds under management (FUM), which has increased influence. Collaboration also enables different engagements across geographies, asset classes and fund types. We have found within the Perpetual Group that collaboration allows for diversity of thought through challenging assumptions and improving decision quality. Regnan research highlights that to achieve true diversity is not just by having varied backgrounds, but by also cultivating a culture where differences can be valued and expressed. Regnan also seeks to bring voices together across our industry. This has included hosting like with the PRI event earlier this month, as well as facilitating and bringing communities together. A few years ago, Regnan brought together different links along the food production supply chain to discuss sustainable agriculture. Last month, we walked around the Regnan eucalyptus trees we get our name from with key leaders in the biodiversity space for an exploration of the work Regnan is doing in advocating the Great Forest National Park. Regnan is also a supporter of the other initiatives by the UNPRI, working with the SPRING initiative which relates to nature, co-leads the Collaborative Sovereign Engagement on Climate, and has a longstanding membership with the Climate Action 100+ initiative. Challenges and realitiesPositive intentions alone do not guarantee smooth collaboration. As anyone who participated in group projects at university knows, not all contributions are equal. Internal alignment with specific funds, mandates, and client expectations are essential. Collaboration must connect with other stewardship and engagement efforts to avoid "collaborative fatigue" - multiple meetings with nebulous outcomes that fail to advance the purpose of the funds. Why now? Continued ramp up in focus on climate change and ways to achieve global net zero goals through the transition to clean energy is generating greater opportunities and diversification in impact investing. Navigating regulationRegulatory challenges are increasingly shaping the landscape of responsible investment. In the US, political resistance has led to changes in shareholder rights, antitrust claims, and investigations into proxy advisors. Closer to home, the ACCC has opened consultations to introduce a class exemption for certain types of beneficial collaboration. It is vital that joint stewardship activities, such as engagement on climate, human rights, and governance, remain permissible under competition law. Restricting such collaboration could undermine efforts to address systemic ESG risks that require collective action. Looking forwardCollaboration does not negate competitive tension. Our clients expect us to undertake stewardship activities that provide meaningful investment insights and strengthen portfolio holdings. Nevertheless, collaborative stewardship is essential for managing systemic risk. Regnan has been a pioneer in using a systems-thinking approach to sustainable investing, and involvement in these collective initiatives is vital to support the health and resilience of the entire system (which, incidentally, includes our investable universe). The stewardship work Regnan does for Regnan funds, and the support provided across the Perpetual boutiques, treats stewardship as a beneficial component to active management. Leadership in collaboration activities allows us to leverage our research and experience, ultimately making us better stewards of the portfolios we influence. Why Regnan Credit Impact Trust? Provides easy access to an institutional-grade impact investment fund that is highly liquid, diversified and scalable. |

|

Funds operated by this manager: Pendal MicroCap Opportunities Fund , Pendal Sustainable Australian Fixed Interest Fund - Class R , Pendal Focus Australian Share Fund , Pendal Horizon Sustainable Australian Share Fund , Regnan Credit Impact Trust Fund , Pendal Sustainable Australian Share Fund , Pendal Multi-Asset Target Return Fund , Barrow Hanley Concentrated Global Share Fund , Pendal Active Balanced Fund , Pendal Active Conservative Fund , Pendal Australian Equity Fund , Pendal Australian Long/Short Fund , Pendal Australian Share Fund , Pendal Dynamic Income Fund - Class R , Pendal Fixed Interest Fund , Pendal Global Emerging Markets Opportunities Fund - Wholesale Class , Pendal Global Property Securities Fund , Pendal Government Bond Fund , Pendal Imputation Fund , Pendal MidCap Fund , Pendal Monthly Income Plus Fund , Pendal Property Investment Fund , Pendal Short Term Income Securities Fund , Pendal Smaller Companies Fund |

|

This information has been prepared by Pendal Fund Services Limited (PFSL) ABN 13 161 249 332, AFSL No 431426 and is current as at December 8, 2021. PFSL is the responsible entity and issuer of units in the Pendal Multi-Asset Target Return Fund (Fund) ARSN: 623 987 968. A product disclosure statement (PDS) is available for the Fund and can be obtained by calling 1300 346 821 or visiting www.pendalgroup.com. The Target Market Determination (TMD) for the Fund is available at www.pendalgroup.com/ddo. You should obtain and consider the PDS and the TMD before deciding whether to acquire, continue to hold or dispose of units in the Fund. An investment in the Fund or any of the funds referred to in this web page is subject to investment risk, including possible delays in repayment of withdrawal proceeds and loss of income and principal invested. This information is for general purposes only, should not be considered as a comprehensive statement on any matter and should not be relied upon as such. It has been prepared without taking into account any recipient's personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation. The information may contain material provided by third parties, is given in good faith and has been derived from sources believed to be accurate as at its issue date. While such material is published with necessary permission, and while all reasonable care has been taken to ensure that the information is complete and correct, to the maximum extent permitted by law neither PFSL nor any company in the Pendal group accepts any responsibility or liability for the accuracy or completeness of this information. Performance figures are calculated in accordance with the Financial Services Council (FSC) standards. Performance data (post-fee) assumes reinvestment of distributions and is calculated using exit prices, net of management costs. Performance data (pre-fee) is calculated by adding back management costs to the post-fee performance. Past performance is not a reliable indicator of future performance. Any projections are predictive only and should not be relied upon when making an investment decision or recommendation. Whilst we have used every effort to ensure that the assumptions on which the projections are based are reasonable, the projections may be based on incorrect assumptions or may not take into account known or unknown risks and uncertainties. The actual results may differ materially from these projections. For more information, please call Customer Relations on 1300 346 821 8am to 6pm (Sydney time) or visit our website www.pendalgroup.com |

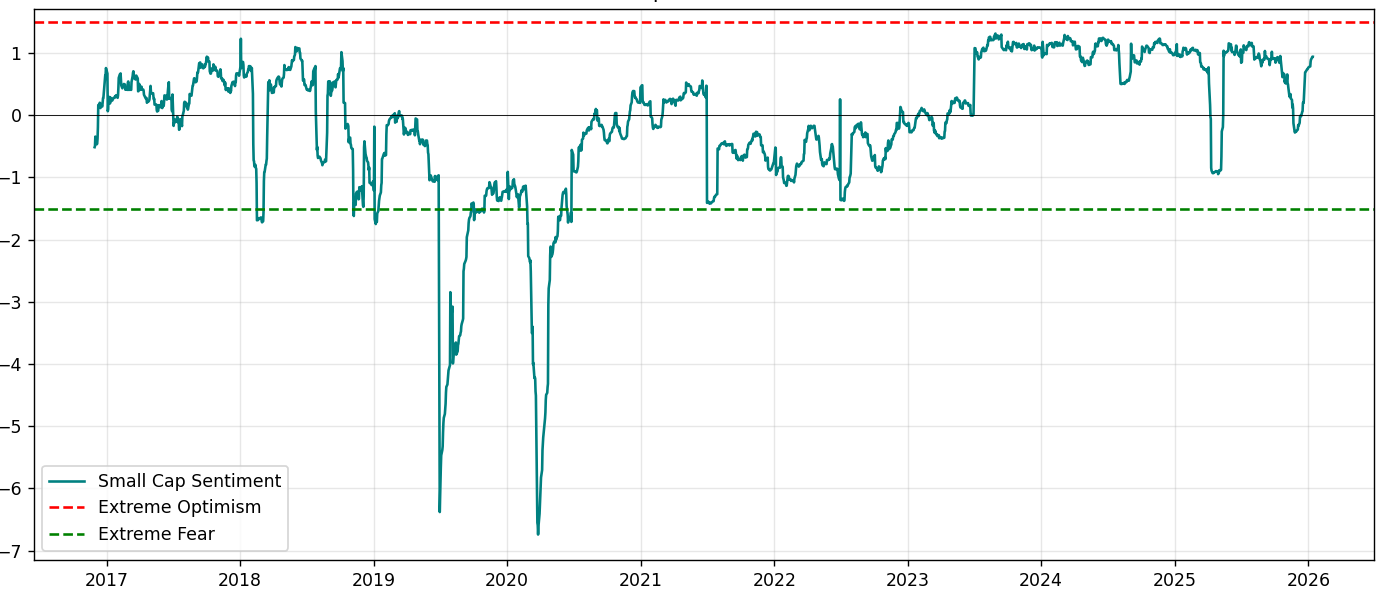

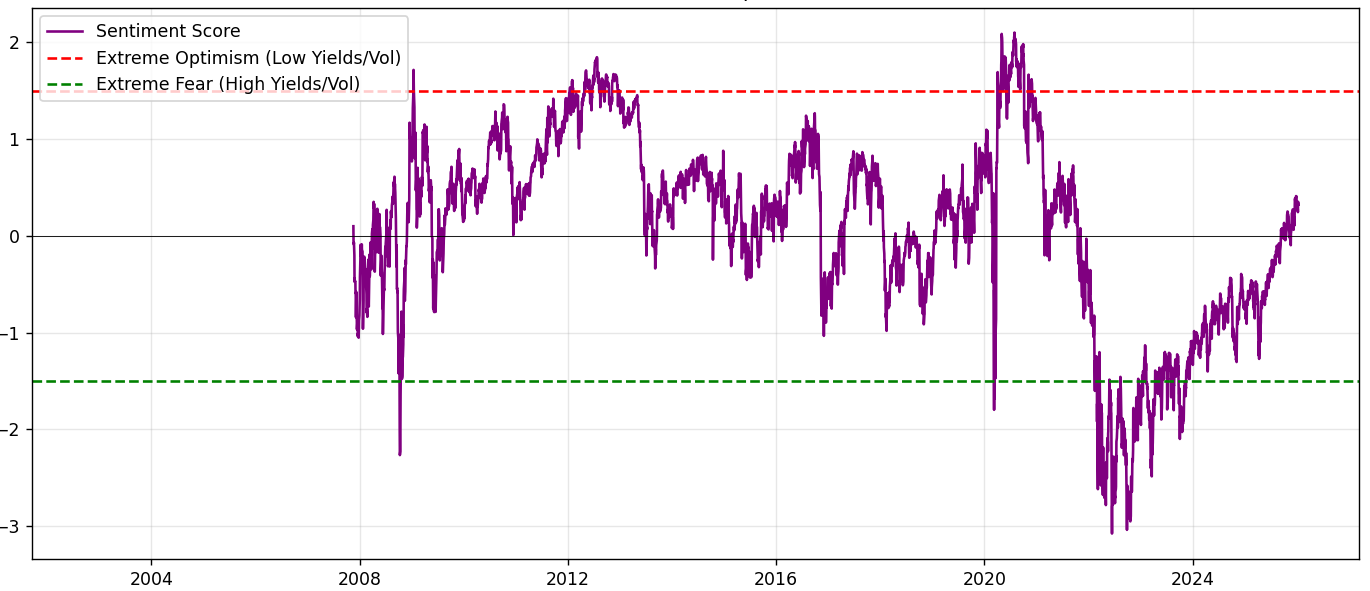

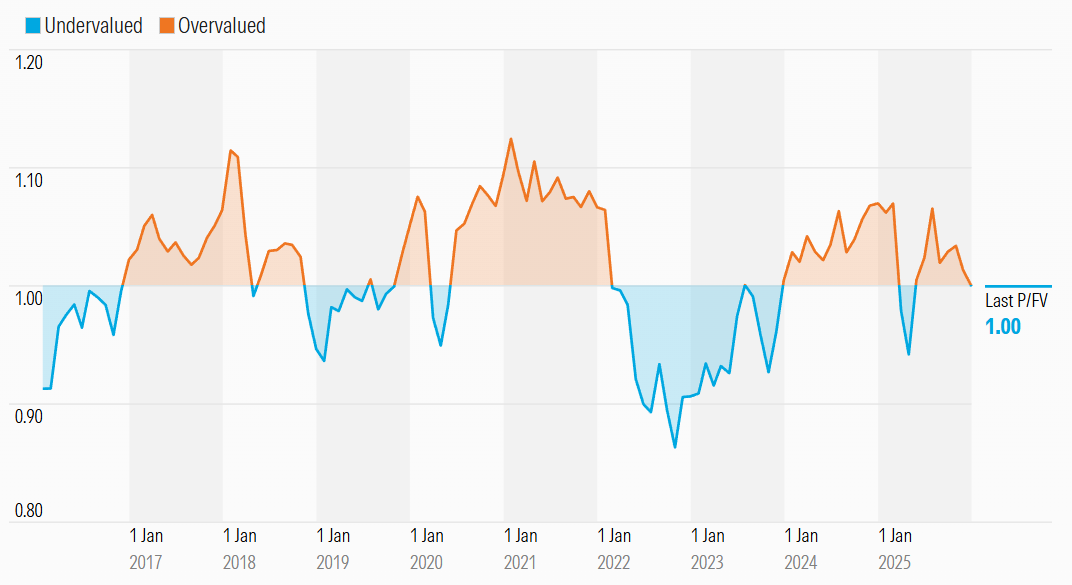

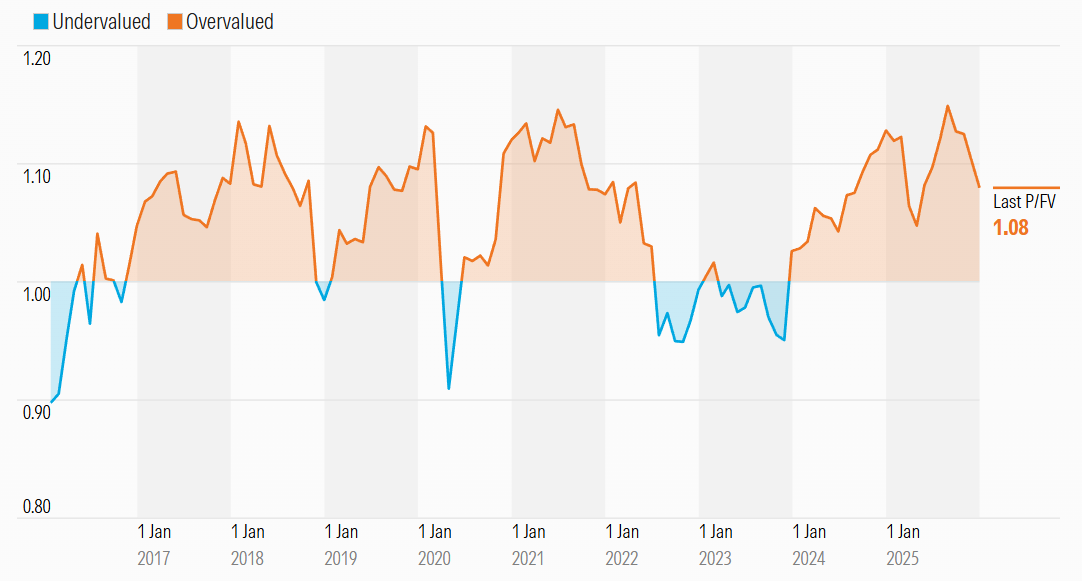

19 Jan 2026 - 10k Words | January 2026

|

10k Words Equitable Investors January 2026 (2-minute read) We kick off calendar 2026 by trying our hand at our own sentiment indicators - combining valuation and implied volatility for the US equity and bond markets, the Aus equity market and ASX small caps. Are investors paying a premium price for market calmness? Then we check in on Morningstar's bottom-up valuations. There is a chasm between small and large cap valuations based on revenue multiples but not so much on earnings. Tech has done the heavy lifting in large cap valuation AND earnings in the US over the past decade and the trend is expected to continue - but can US smalls deliver on lofty targets and drive a catch-up? In US dollars, the US market has underperformed most major markets in the Americas. Then we look at how short-term (daily) volatility itself is becoming more volatile over time. Turning to the economy, we look at personal loan delinquencies and savings rates, with signs of deterioration in consumer behaviour. A custom US equity market sentiment score - based on CAPE adjusted equity risk premium and the VIX relative to their historical average and volatility

Source: Equitable Investors A custom ASX equity market sentiment score - based on the dividend yield spread on bonds and the ASX VIX relative to their historical average and volatility

Source: Equitable Investors A custom ASX small cap sentiment score - based on the dividend yield spread on bonds and realised volatilty relative to their historical average and volatility

Source: Equitable Investors A custom US debt market sentiment score - based on 10 year bond yield and MOVE Index of implied volatility relative to their historical average and volatility

Source: Equitable Investors Market price relative to US market bottom-up valuations from Morningstar

Source: Morningstar Market price relative to ASX market bottom-up valuations from Morningstar

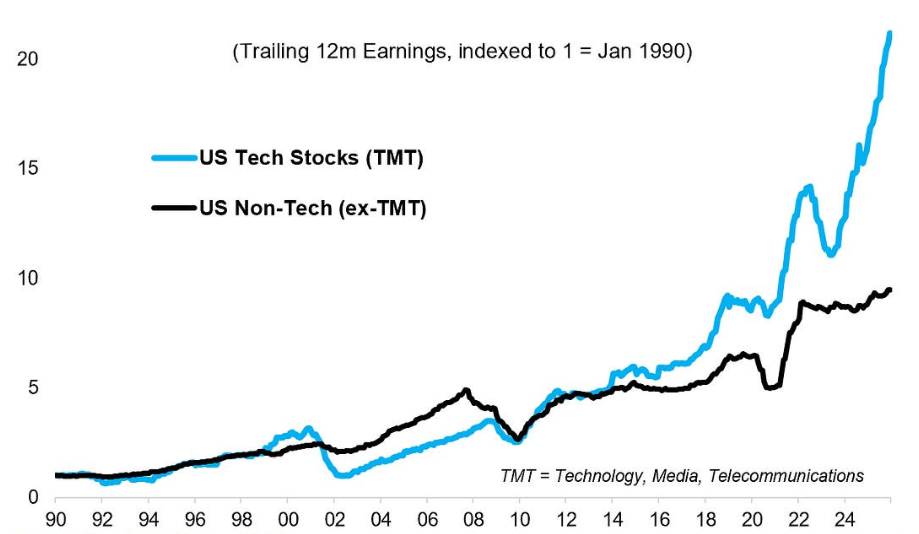

Source: Morningstar Earnings: US Tech vs the Rest

Source: Topdown Charts Actual reported and bottom-up consensus EPS growth estimates

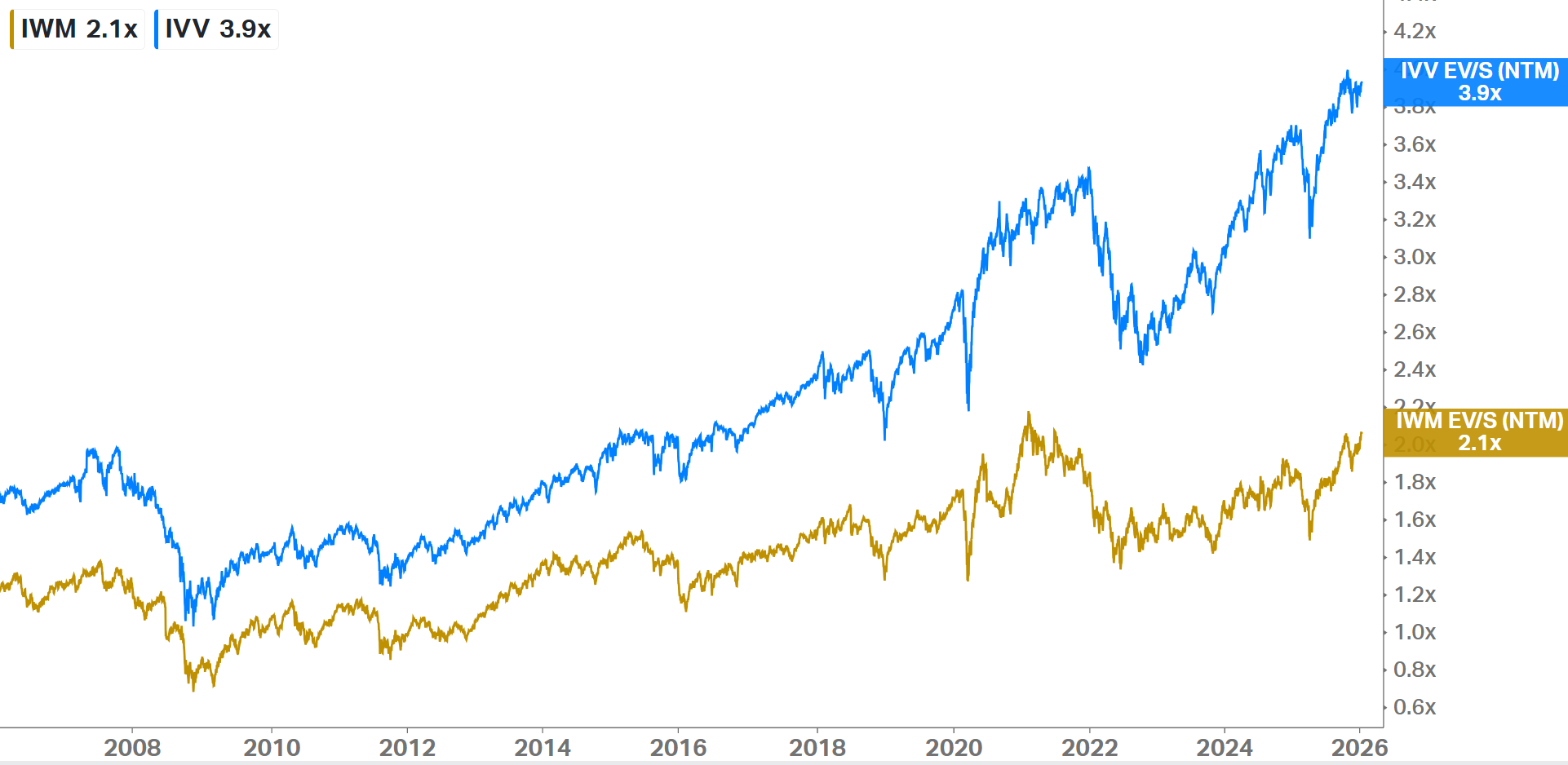

Source: Goldman Sachs Global Investment Research Enterprise Value / consensus sales - S&P 500 (IVV ETF) v US microcaps (IWM ETF)

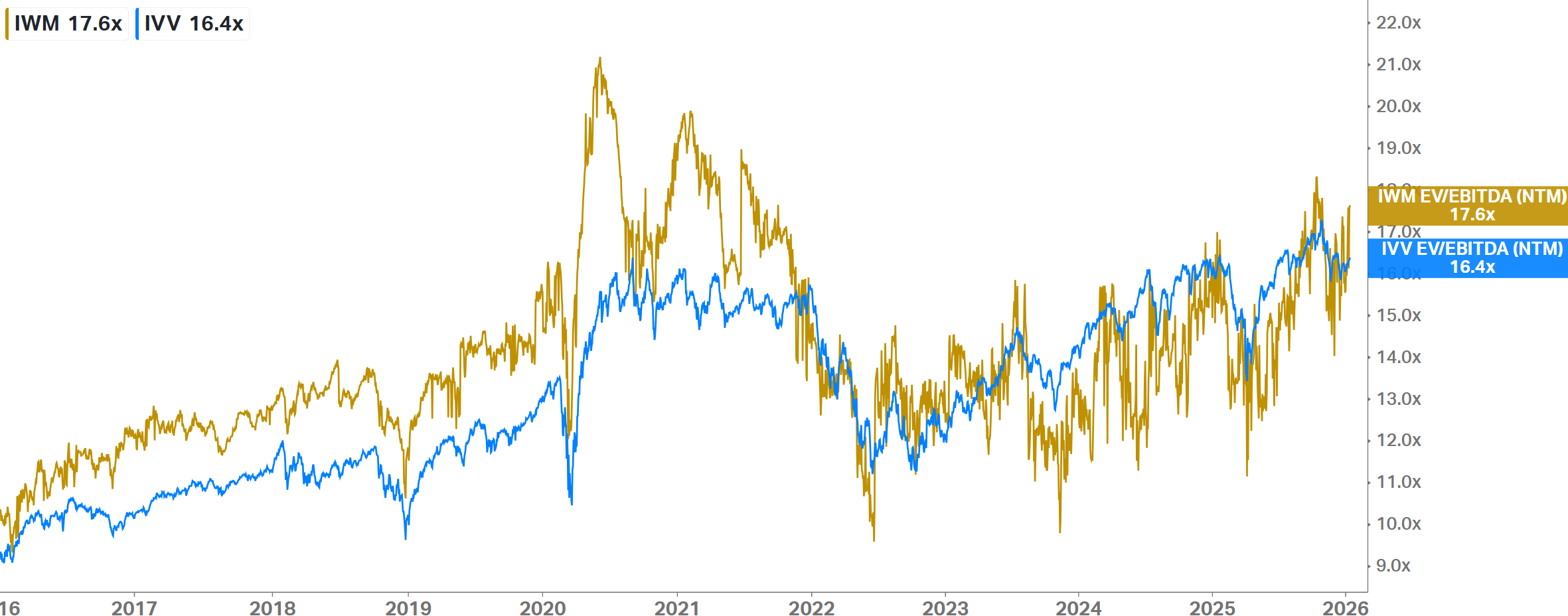

Source: Koyfin Enterprise Value / consenus EBITDA - S&P 500 (IVV ETF) v US microcaps (IWM ETF)

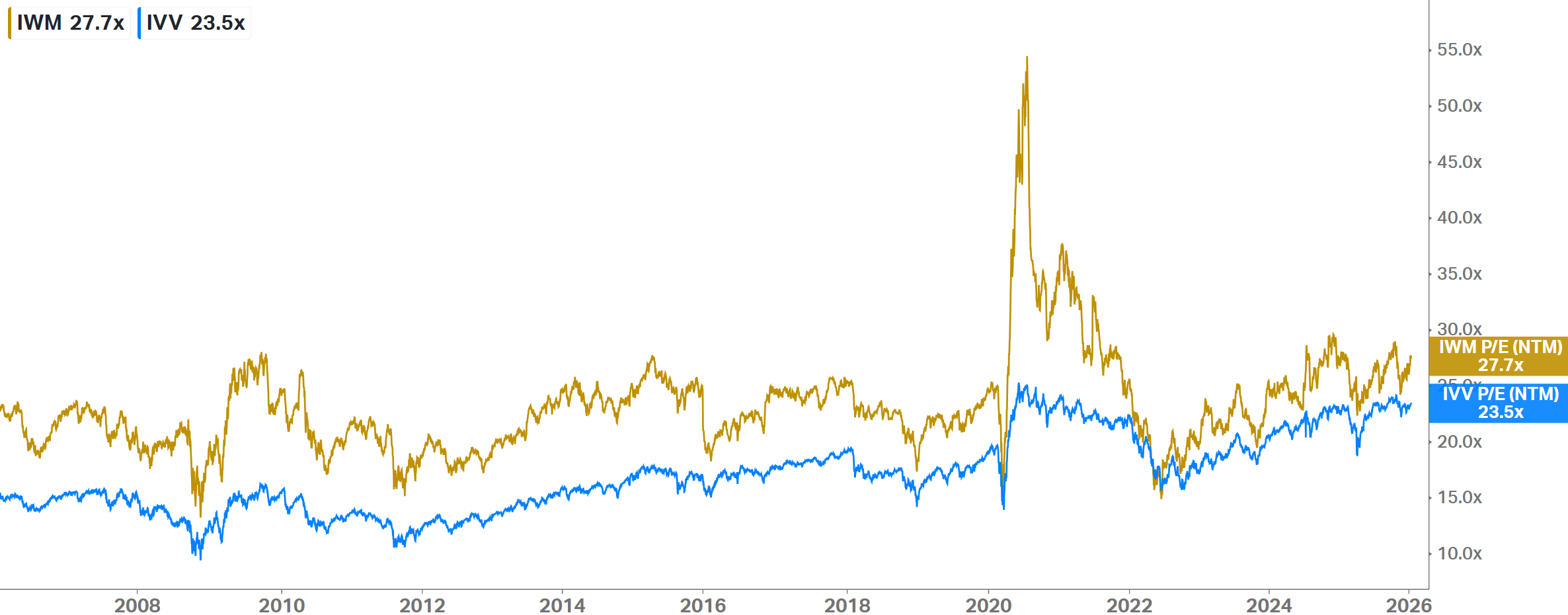

Source: Koyfin Price / consenus EPS - S&P 500 (IVV ETF) v US microcaps (IWM ETF)

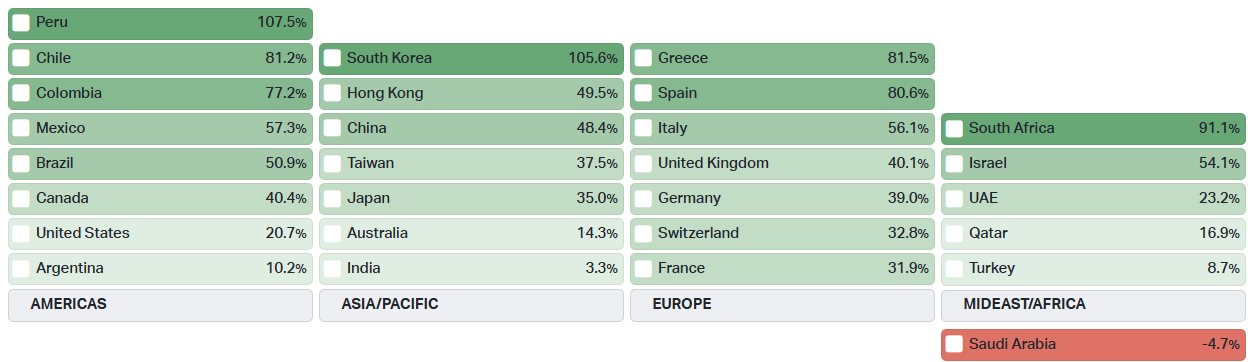

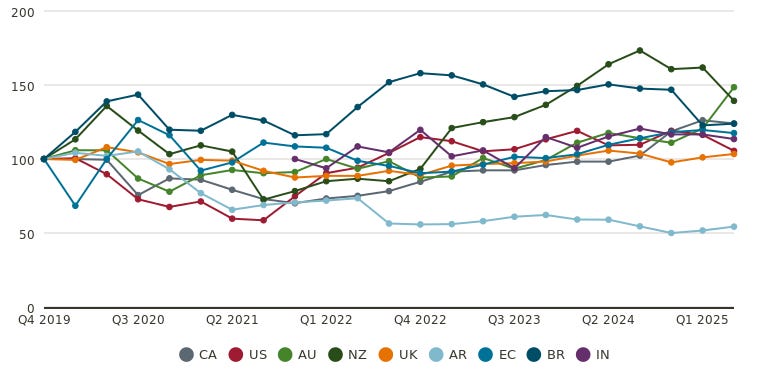

Source: Koyfin Country ETF performance over past 12 months (in USD)

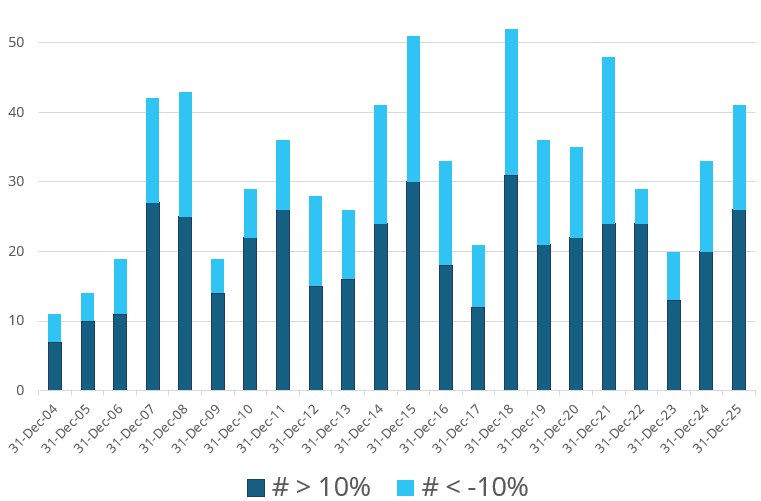

Source: Koyfin No. of daily 10% swings per calendar year in the VIX (CBOE Market Volatility)

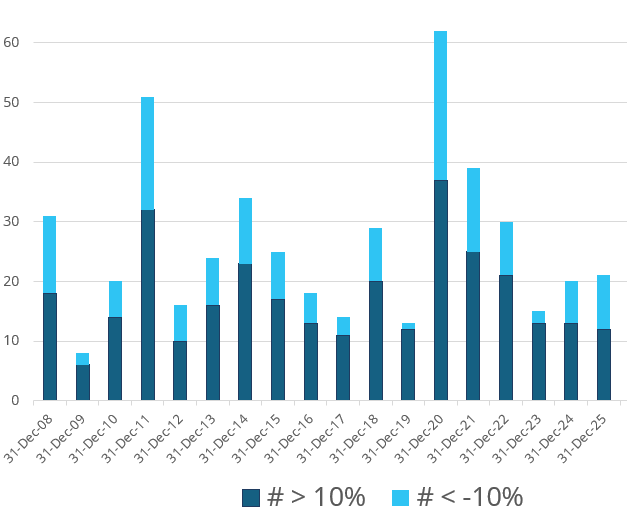

Source: Iress, Equitable Investors No. of daily 10% swings per calendar year in the S&P/ASX VIX

Source: Iress, Equitable Investors Personal Loans - 90+ Delinquency (#)

Source: Equifax Australian savings ratio

Source: RBA USA personal saving

Source: St Louis Fed Funds operated by this manager: Equitable Investors Dragonfly Fund Disclaimer Past performance is not a reliable indicator of future performance. Fund returns are quoted net of all fees, expenses and accrued performance fees. Delivery of this report to a recipient should not be relied on as a representation that there has been no change since the preparation date in the affairs or financial condition of the Fund or the Trustee; or that the information contained in this report remains accurate or complete at any time after the preparation date. Equitable Investors Pty Ltd (EI) does not guarantee or make any representation or warranty as to the accuracy or completeness of the information in this report. To the extent permitted by law, EI disclaims all liability that may otherwise arise due to any information in this report being inaccurate or information being omitted. This report does not take into account the particular investment objectives, financial situation and needs of potential investors. Before making a decision to invest in the Fund the recipient should obtain professional advice. This report does not purport to contain all the information that the recipient may require to evaluate a possible investment in the Fund. The recipient should conduct their own independent analysis of the Fund and refer to the current Information Memorandum, which is available from EI. |

14 Jan 2026 - Private markets outlook 2026: navigating opportunities through structural change

|

Private markets outlook 2026: navigating opportunities through structural change abrdn January 2026 (4-minute read) Private markets should enter 2026 with a renewed sense of purpose. After a period of volatility and recalibration, the landscape has shifted in favour of long-term investors seeking resilience, diversification, and access to secular growth themes. From the growing role of private credit in corporate finance to the acceleration of digital and green infrastructure, the past year has underscored the strategic importance of private assets in modern portfolios. The macroeconomic backdrop is evolving. Global growth has slowed but remains intact, and inflationary pressures are beginning to ease. Central banks are approaching the end of their tightening cycles, with some already pivoting towards more accommodative stances. This shift in monetary policy is improving financing conditions, and supporting deal activity and valuations across private markets. Against this backdrop, our latest Private Markets House View outlines a cautiously optimistic outlook across the four major asset classes: private equity, private credit, infrastructure, and real estate. Each offers distinct opportunities, shaped by structural trends and regional dynamics. Private equity: rebound and realignmentPrivate equity has staged a strong recovery, with deal-making regaining momentum as confidence returns to the market. Improved credit availability and greater alignment between buyers and sellers have helped restore activity levels. Valuations, which had softened during the previous downturn, have rebounded, reflecting both stronger financing conditions and a focus on higher-quality assets. Thematic investing remains central to private equity strategies. Technology and healthcare continue to attract capital, driven by innovation and demographic shifts. Businesses that harness digital tools, automation, and artificial intelligence are particularly appealing. Meanwhile, sectors more exposed to economic cycles are being approached with greater caution, as investors prioritise resilience and long-term growth potential. Looking ahead, private equity is expected to maintain its role as a key driver of portfolio returns. While macroeconomic risks persist, the combination of structural tailwinds and a disciplined investment approach positions the asset class well for the coming years. Private credit: filling the lending gapPrivate credit has cemented its place as a vital source of capital, particularly as traditional banks scale back lending. In some regions, deal activity has been more subdued, reflecting recent market volatility and policy uncertainty. However, the underlying demand for private credit remains robust, with investors drawn to its income-generating potential. In Europe, direct lending has been especially active. It is supported by structural trends, such as bank disintermediation and the continued appetite for flexible financing solutions. Lenders are focusing on smaller, mid-market transactions where pricing and terms remain attractive. Credit quality has held up well, with lenders adopting more conservative structures to mitigate downside risk. As interest rates stabilise, the appeal of floating-rate instruments and the potential for enhanced yields continue to attract capital. Private credit opportunities are emerging in both traditional lending and more opportunistic strategies. Infrastructure: investing in the futureInfrastructure investment is thriving, fuelled by the global push towards digitalisation and decarbonisation. Capital deployment has accelerated, with strong interest in sectors such as renewable energy and digital infrastructure. These areas are benefiting from long-term policy support and growing demand for sustainable and connected solutions. Investors are increasingly looking beyond traditional core assets, seeking exposure to opportunities that offer a blend of stability and growth. Core-plus strategies, which involve assets with modest development or operational risk, are gaining traction as they offer the potential for higher returns without sacrificing predictability. The pipeline for infrastructure projects remains healthy, supported by public and private sector initiatives. As the energy transition gathers pace and digital connectivity becomes ever-more critical, infrastructure is set to remain a cornerstone of private market allocations. Real estate: a market in transitionPrivate real estate is showing signs of stabilisation following a period of adjustment. The easing of monetary policy is beginning to support valuations, and certain regions are experiencing a modest recovery. However, performance remains uneven, with outcomes varying significantly by geography and sector. A clear polarisation is emerging within the asset class. Investors are gravitating towards high-quality, future-fit assets that align with long-term trends. Logistics and residential properties are in favour, driven by structural demand and limited supply. In contrast, traditional office and retail assets face ongoing challenges, with changing work patterns and consumer behaviour reshaping demand. The focus is increasingly on assets that offer sustainability credentials, adaptability, and strong tenant demand. Value-add strategies, which involve repositioning or upgrading properties, are also gaining interest as investors seek to unlock value in a shifting landscape. Final thoughts...As we look to the year ahead, private markets offer a compelling proposition. Each asset class presents unique opportunities, underpinned by structural change and evolving investor needs. While selectivity and discipline remain essential, with improving macro conditions, private markets will continue to be a key driver of portfolio diversification and resilience. Private markets have become a vital component of investors' asset allocation. By embracing innovation, sustainability, and long-term thinking, investors can position themselves to navigate uncertainty and capture the opportunities that lie ahead in 2026 and beyond. |

|

Funds operated by this manager: abrdn Sustainable Asian Opportunities Fund , abrdn Emerging Markets Equity Fund , abrdn Sustainable International Equities Fund , abrdn Global Corporate Bond Fund (Class A) |

13 Jan 2026 - Affordability is a hot button issue for 2026