NEWS

16 Dec 2025 - What investors should expect when investing in infrastructure: yield

|

What investors should expect when investing in infrastructure: yield Magellan Asset Management December 2025 (10-minute read) |

|

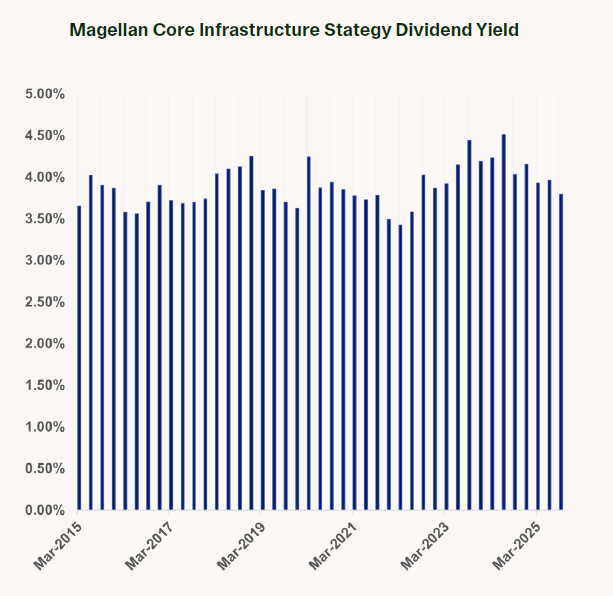

Dependable earnings growth is a core characteristic of the high-quality listed infrastructure companies in which we invest. Throughout past cycles we have seen consistent, solid returns. Given the earnings profile, operating models and potential for inflation protection that underpin these companies' assets, we expect this to continue. Moreover, we see sustained annual returns of CPI plus 5.0% over the investment cycle ahead for this asset class. This expected return, of approximately 7.0%-8.0% annually, can be broken down into three key components: yield, inflation protection and capital growth. Yield is one of these building blocks and is unpacked in more detail below. High-quality listed infrastructure companies provide consistent yield In looking at historical data, high-quality infrastructure companies in our portfolio1 delivered an average dividend yield of close to 4.0% over the past decade. We've also seen that this yield moves in a tight range, through both up and down economic cycles. For example, in 2020, with the covid shock to the economy, and sizeable interest rate cuts, the average dividend yield for our portfolio1 held in a range of 3.5%-4.5%. Subsequently, in 2022-2023, when there was an inflation surge and sharp rises in interest rates, the average yield was maintained in this range. We see similar patterns in economic cycles further back in time. For example, in the global economic upswing in 2015-2016, which saw commodity prices rally, our portfolio again recorded an average dividend yield in the 3.5%-4.0% range. In looking at historical data, high-quality infrastructure companies in our portfolio1 delivered an average dividend yield of close to 4.0% over the past decade. We've also seen that this yield moves in a tight range, through both up and down economic cycles. For example, in 2020, with the covid shock to the economy, and sizeable interest rate cuts, the average dividend yield for our portfolio1 held in a range of 3.5%-4.5%.

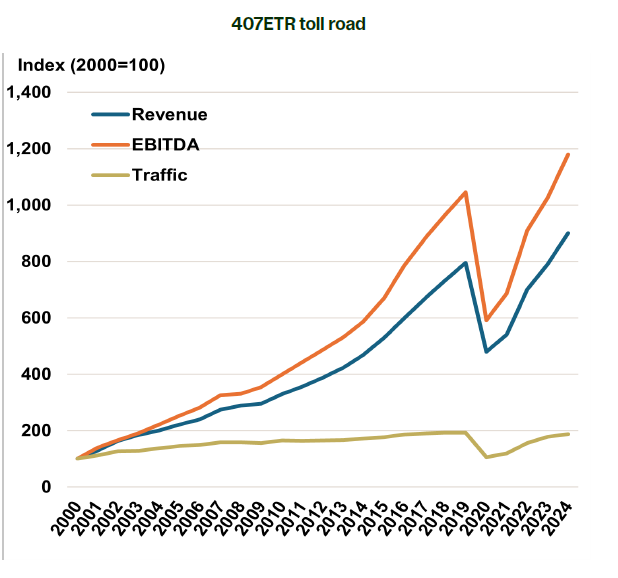

Source: Bloomberg. Magellan. The numerical information above is based on a representative portfolio. The representative portfolio is an account in the Global Core Infrastructure AUD Hedged Composite that closely reflects the portfolio management style of the strategy. Subsequently, in 2022-2023, when there was an inflation surge and sharp rises in interest rates, the average yield was maintained in this range. We see similar patterns in economic cycles further back in time. For example, in the global economic upswing in 2015-2016, which saw commodity prices rally, our portfolio again recorded an average dividend yield in the 3.5%-4.0% range. These examples highlight the stability of divided income yields to investors. The yield returned is consistent and largely unaffected by market cycles. Even in significant upswings and downdrafts, the yield does not deviate much from the long-term average of 4.0%. This is important, as it highlights the role of high-quality listed infrastructure as a diversifier in an investor's portfolio. Stable businesses support stable dividends Infrastructure companies can deliver consistent dividends because of the nature of their underlying assets. Fundamentally, infrastructure businesses provide essential services, which support predictable demand and income (for example, water services, or electricity). Earnings are typically secured in a regulated or non-competitive structure. For example, the Magellan Global Listed Infrastructure strategy invest in companies with the bulk of earnings (75% or more) sourced from high-quality infrastructure businesses that are predominantly natural monopolies or concession-driven businesses. Demand for the services these assets provide is typically stable. At the same time, many of these businesses have a regulated component to their earnings, which varies in its breadth but provides another parameter for certainty on earnings. This includes the regulated revenue allowance for utilities, regulated toll increases for toll road operators and regulated aero revenues for airports. As a result, these companies have a relatively stable cash flow profile. To see what this looks like in practice, let's look at a few sub-sector examples. Toll roads illustrate this well, offering captive traffic flows and consistent revenue and earnings growth and reflecting operating leverage in their business model. The 407ETR toll road in Canada, owned by Ferrovial, is another example, shown in the chart below. This road, like other high-quality toll road assets, captures the bulk of growth in traffic in its catchment. With the competing free road typically full at peak travel times, the toll road provides users with shorter transit times, with the added benefit that the concession allows for peak pricing and for different tolls for different segments based on demand.

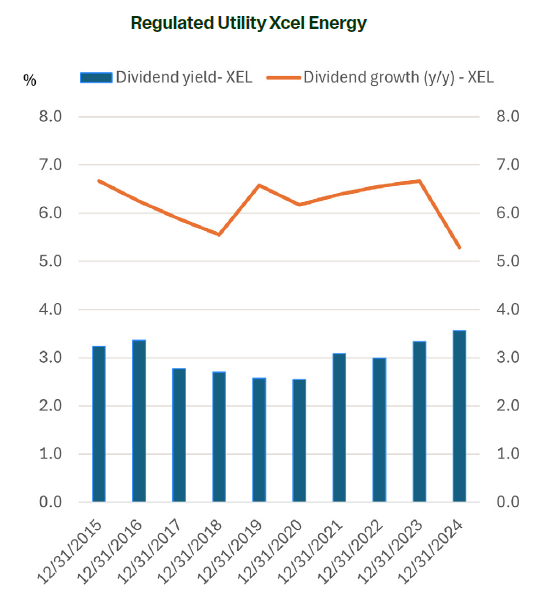

Regulated utilities show a similar dynamic, with their earnings linked to the growth of their regulated asset base. These companies invest in new projects, with spending approved by their regulator, to meet growing power demand, improve asset resilience, or upgrade existing infrastructure. These companies then typically earn an agreed rate of return on this asset base - of around 9.0%-10% for US integrated power companies like Xcel Energy and WEC Energy. High-quality airports (such as European airports including Aena) operate in regimes that entitle the operating company to earn predictable returns. This includes an entitlement to earn a fair rate of return on invested capital for aviation activities and provisions for minimum annual guarantees for commercial activities, such as retail. Looking at these examples, we can see that well-defined infrastructure companies have the advantage of high barriers to entry, pricing power and a regulated operating environment. These conditions allow these companies to have stable revenue linked to their asset base rather than to the business cycle. Under this distinct model, infrastructure companies can then pay predictable distributions to investors. Secular trends drive yield generation This is a snapshot of the translation of predictable demand and high-quality businesses into dividend yield at a point in time. Over time, there are clear catalysts for these companies to continue to generate yield, providing for durable returns to investors over an investment cycle. In simple terms, steady growth in earnings over time can support higher dividends. The dividend yield can therefore comfortably hold ground for these companies, at around 4.0%. Major secular trends in the market at any given time can be linked directly to the ability of infrastructure companies to generate predictable earnings over the long term. The rise of AI and ongoing demand for renewable energy generation are two such major trends. AI is expected to push electricity demand higher for years to come. That gives integrated utilities room to invest more, expand their asset base, and earn more on that capital. These allowable returns ultimately underpin dividends to investors. The resilience of renewable energy investment, reflecting improving cost competitiveness, also translates into greater capital investment for integrated utilities and transmission and distribution companies. As these are regulated utilities, we see robust growth in capex again driving solid earnings growth over the longer term. Historically, this earnings growth has translated into dividend growth for investors (for example, with US regulated utilities typically recording 5.0-7.0% EPS growth, and similar dividend growth), which also helps to sustain dividend yield over time. This is shown in the chart below for regulated utility Xcel Energy. The company demonstrates consistent dividend yield and dividend growth in the range of 5.0-7.0%, which is in line with its earnings growth over the last decade.

Source: Magellan analysis of company data In addition, infrastructure businesses are highly cash generative, which supports dividend yield generation for investors over time. This is especially the case for transport infrastructure assets, which have often high levels of free cash flow. Management of these businesses can use the excess cash to maintain stable dividend yields to investors through special dividends and share repurchases, even in times of unfavourable stock price performance. Durable yield and diversification benefits We believe infrastructure investors can expect consistency in income over time, with some key drivers in place for self-sustainment. At around 3.5-4.5%, we view this to be an attractive income return and would highlight our expectations of limited deviations (up or down) from this dividend yield range. In fact, reflecting its business model and the nature of income streams, infrastructure is not typically seen by investors as the high-growth part of the portfolio. Rather, it plays the role of the consistent, slower-growing diversifier that can provide compounding and real capital growth over time. Infrastructure has also demonstrated outperformance in certain market environments. We believe that high-quality listed infrastructure can be expected to provide a dividend yield of ~4.0%. This represents approximately 50%-60% of the CPI plus 5.0% return (7.0%-8.0% return) we would expect for the infrastructure asset class and underscores our confidence in achieving this outcome over the medium to long term. By Magellan Investment Team 1 Magellan Core Infrastructure Strategy (hedged and in AUD). |

|

Funds operated by this manager: Vinva Global Alpha Fund - Active ETF (ASX: V1AC) , Vinva Australian Equity Fund , Vinva Global Equity Fund , Vinva Australian Alpha Extension Fund , Vinva Global Alpha Extension Fund , Magellan Infrastructure Fund , Magellan Global Opportunities Fund No.2 , Magellan Infrastructure Fund (Unhedged) , Magellan Core Infrastructure Fund , Magellan Global Opportunities Fund Active ETF (ASX:OPPT) Important Information: This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 trading as Magellan Investment Partners ('Magellan Investment Partners') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision about whether to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to a Magellan Investment Partners financial product may be obtained by calling +61 2 9235 4888 or by visiting www.magellaninvestmentpartners.com Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of a Magellan Investment Partners financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. No guarantee is made that such information is accurate, complete or timely and no warranty is given regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Magellan Investment Partners or the third party responsible for making those statements (as relevant). Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. No representation or warranty is made with respect to the accuracy or completeness of any of the information contained in this material. Magellan Investment Partners will not be responsible or liable for any losses arising from your use or reliance upon any part of the information contained in this material. Any third-party trademarks contained herein are the property of their respective owners and Magellan Investment Partners claims no ownership in, nor any affiliation with, such trademarks. Any third-party trademarks contained herein are the property of their respective owners, are used for information purposes and only to identify the company names or brands of their respective owners, and no affiliation, sponsorship or endorsement should be inferred from such use. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Magellan Investment Partners. (080825-#W17) |

15 Dec 2025 - Expert Analysis of the RBA's December 9 Rate Decision

|

Expert Analysis of the RBA's December 9 Rate Decision FundMonitors.com December 2025 |

|

Chris Gosselin, CEO of FundMonitors.com, speaks with Nicholas Chaplin, Director and Portfolio Manager at Seed Funds Management, and Renny Ellis, Director & Head of Portfolio Management at Arculus Funds Management. In this discussion, they share their perspectives on the RBA's recent rate decisions, whether cuts came too early, and how inflation dynamics, subsidies, and employment data are shaping economic expectations. They also explore the likelihood of future rate movements and what investors should watch heading into 2026. |

15 Dec 2025 - Glenmore Asset Management - Market Commentary

|

Market Commentary - November Glenmore Asset Management December 2025 (2-minute read) Global equity markets were particularly volatile in November, driven by factors such as the US Government shutdown, concerns over a potential AI-related bubble and the direction of future US interest rates. The S&P 500 and NASDAQ reached intra-month lows of -4.4% and -6.9%, before recovering to end the month +0.1% and -1.5%, respectively. Returns were muted outside of the US, with the FTSE 100 remaining flat and the Euro Stoxx 50 rising +0.1%. Similar to the prior month, domestic markets underperformed their international peers. The ASX All Ordinaries Accumulation index fell -2.5%, as markets digested stronger than forecasted economic data. This was largely focused upon two releases, being 1) a stronger than expected jobs report and 2) hotter than anticipated October CPI, showing broad-based inflation across goods and services. As a result, markets now assume a greater chance of a rate hike rather than a rate cut over the next 12 months. In bond markets, the US 10-year bond yield declined -6 basis points (bp) to 4.01%, whilst its Australian counterpart rose 22bp to 4.52%. The Australian dollar remained flat, closing at US$0.655. Funds operated by this manager: |

12 Dec 2025 - AI fever hits bond markets - tactical play or a bigger bubble?

|

AI fever hits bond markets - tactical play or a bigger bubble? abrdn December 2025 (3-minute read) In the world of AI, a lot can change in six months. Back in July, there was little talk of AI investment in public bond markets. The sector's 'hyperscalers' (Amazon, Google, Meta, Microsoft and Oracle) had been funding their capital expenditure (capex) through strong free cash flow and by tapping private equity, private credit and other sources. This dynamic is changing - fast. Capex is set to ramp up significantly over the next 24 months. With free cash flow constrained by shareholder returns and share buybacks, hyperscalers are leaning harder on public bond markets. The last three months alone have seen a glut of debt issuance: $30 billion (bn) of bonds issued from Meta, $25bn from Alphabet (owner of Google), $20bn from Amazon, and $18bn from Oracle. Major investment neededThe rapid growth of AI-optimised data centres highlights how much investment is needed for businesses to keep pace with the AI race. Building an AI-specific data centre can cost up to $50bn - some three times more than a conventional facility, depending on the chips involved. Morgan Stanley estimates total data centre funding will hit $3 trillion (trn) by 2028, while JP Morgan and McKinsey put the figure at $5-7trn by 2030. Oxford Economics suggests the current pace of AI investment since 2023 matches the digital boom in the 1990s, when the internet took flight. With such major outlays required, capex guidance and forecasts are rising fast. The five hyperscalers are expected to grow capex by 40% in 2026 to $500bn, and by a further 17% to £600bn in 2027. Powering the futureIncreased energy demand is a major implication of AI and this too will require further investment and funding over time. The International Energy Agency estimates that total data centre electricity consumption will double by 2030. Data centres are essential for AI due to the massive computational power and high-speed networking required to train and run complex AI models. Electricity consumption by AI-optimised servers is expected to increase fivefold by 2030. BloombergNEF estimates that by 2035 global data centre power needs will hit 1.6TWh, which will take data centre share of global power demand from the current 1.3% to closer to 4.4%. Put another way, by 2030 it is estimated that if data centres were a country, they would be the fourth largest consumer of energy after China, the US and India. This surge in energy demand adds another layer to the investment challenge - and will likely keep funding needs elevated for years to come. Bond markets taking noticeBond markets are sitting up. US investment grade credit spreads have widened by 12% since the end of September - driven in part by a surge in issuance, as markets question how the AI boom will be funded. According to Morgan Stanley, just under half of the $3trn required by 2028 could come from cash generation, with a quarter from private credit and 10% from other sources, such as private equity and sovereign wealth. That leaves the remaining 15% roughly $450bn - to be raised in bond markets, with $200bn-250bn potentially coming from investment-grade credit markets. JP Morgan estimates that 14% of the US investment grade debt market is already tied to AI. In our view, AI-related corporate bond supply will likely continue to grow, both in absolute terms and as a share of the wider bond market. While AI issuance is unlikely to overwhelm the bond market, we do expect further periods of significant issuance from AI-related companies as they invest in their capabilities - potentially causing bouts of indigestion in public credit markets. What does it mean for investors?We see the technology sector as one to play tactically. For strategies focused on shorter-dated bonds, the surge in supply creates opportunities to lock in high-quality names at more attractive levels as markets reprice. For all-maturity or longer-dated funds, a nimbler approach is needed. This helps control exposure to the wider AI sector and leaves room to add when the next wave of major bond issuances arrives - which we expect in the not-too-distant future. Final thoughts...The AI revolution is well underway. The funding to power this new era will be significant. Bond markets are already taking notice as hyperscalers come to market. We expect this trend to continue at pace. Data centres alone will need an estimated $5-7tn by 2030. For investors, this wall of supply offers opportunities to pick up attractively valued securities ahead of any repricing. Staying nimble and selective will be key as the next chapter of AI-driven growth unfolds. |

|

Funds operated by this manager: abrdn Sustainable Asian Opportunities Fund , abrdn Emerging Markets Equity Fund , abrdn Sustainable International Equities Fund , abrdn Global Corporate Bond Fund (Class A) |

11 Dec 2025 - Why higher tracking error can mean lower risk

10 Dec 2025 - Infrastructure in focus: The industrial heartland

|

Infrastructure in focus: The industrial heartland Magellan Asset Management November 2025 (7-minute read) |

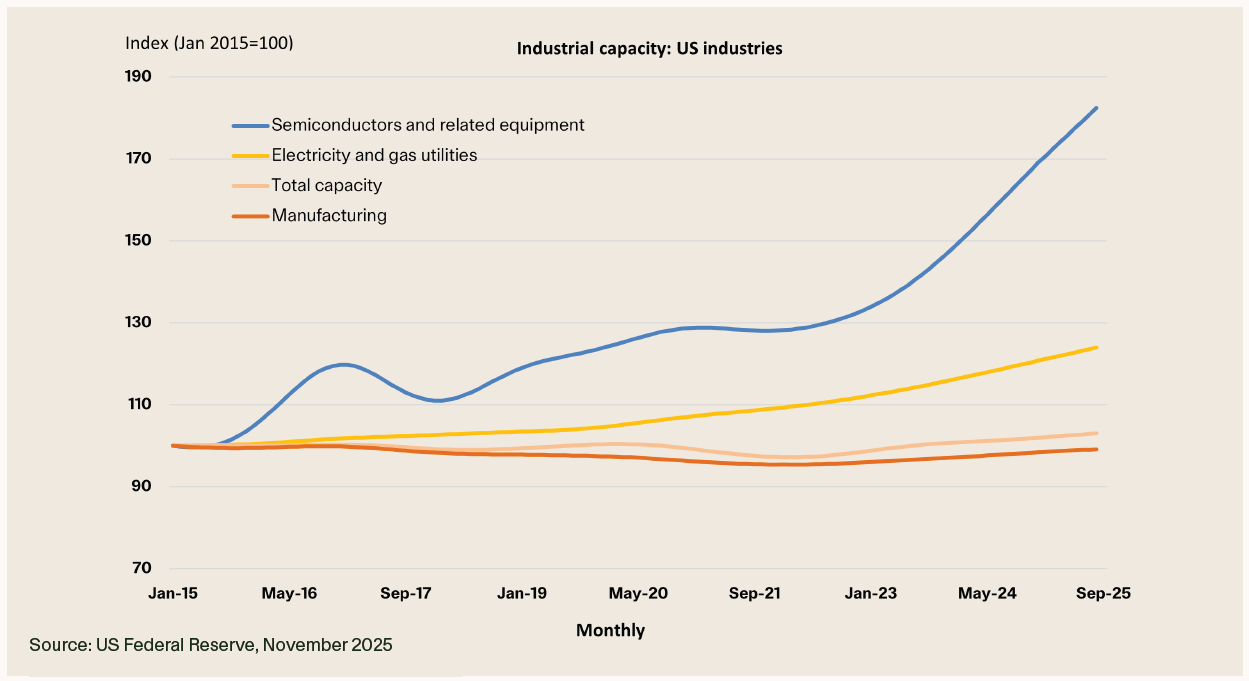

Looking at a country's industrial base can tell a lot about the makeup of its activities and its infrastructure needs. The chart below shows US industrial capacity, from 2015 to now. Several things stand out:

With the expansion in electricity and gas utility capacity outpacing total industrial capacity while growth in semiconductor production capacity is on a tear, what we see here is the real-world story of the AI boom. Exuberance on AI has been the predominant theme for markets this year, and the chart below shows a structural shift in economic activity underway.

Highlights

By Magellan Global Listed Infrastructure Investment Team |

|

Funds operated by this manager: Vinva Global Alpha Fund - Active ETF (ASX: V1AC) , Vinva Australian Equity Fund , Vinva Global Equity Fund , Vinva Australian Alpha Extension Fund , Vinva Global Alpha Extension Fund , Magellan Infrastructure Fund , Magellan Global Opportunities Fund No.2 , Magellan Infrastructure Fund (Unhedged) , Magellan Core Infrastructure Fund , Magellan Global Opportunities Fund Active ETF (ASX:OPPT) Important Information: This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 trading as Magellan Investment Partners ('Magellan Investment Partners') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision about whether to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to a Magellan Investment Partners financial product may be obtained by calling +61 2 9235 4888 or by visiting www.magellaninvestmentpartners.com Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of a Magellan Investment Partners financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. No guarantee is made that such information is accurate, complete or timely and no warranty is given regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Magellan Investment Partners or the third party responsible for making those statements (as relevant). Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. No representation or warranty is made with respect to the accuracy or completeness of any of the information contained in this material. Magellan Investment Partners will not be responsible or liable for any losses arising from your use or reliance upon any part of the information contained in this material. Any third-party trademarks contained herein are the property of their respective owners and Magellan Investment Partners claims no ownership in, nor any affiliation with, such trademarks. Any third-party trademarks contained herein are the property of their respective owners, are used for information purposes and only to identify the company names or brands of their respective owners, and no affiliation, sponsorship or endorsement should be inferred from such use. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Magellan Investment Partners. (080825-#W17) |

9 Dec 2025 - News and Views: The impact of a steeper yield curve on global listed infrastructure

|

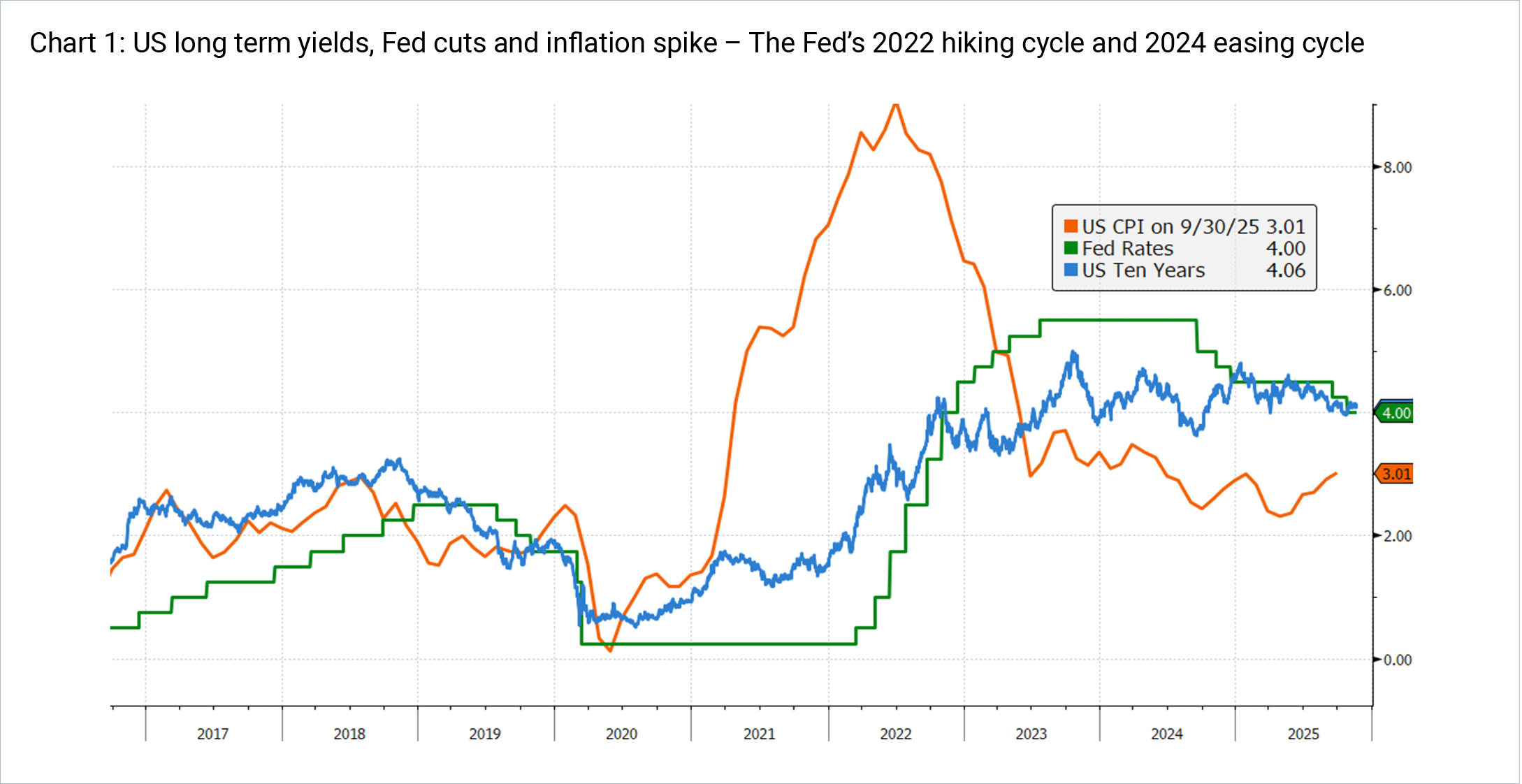

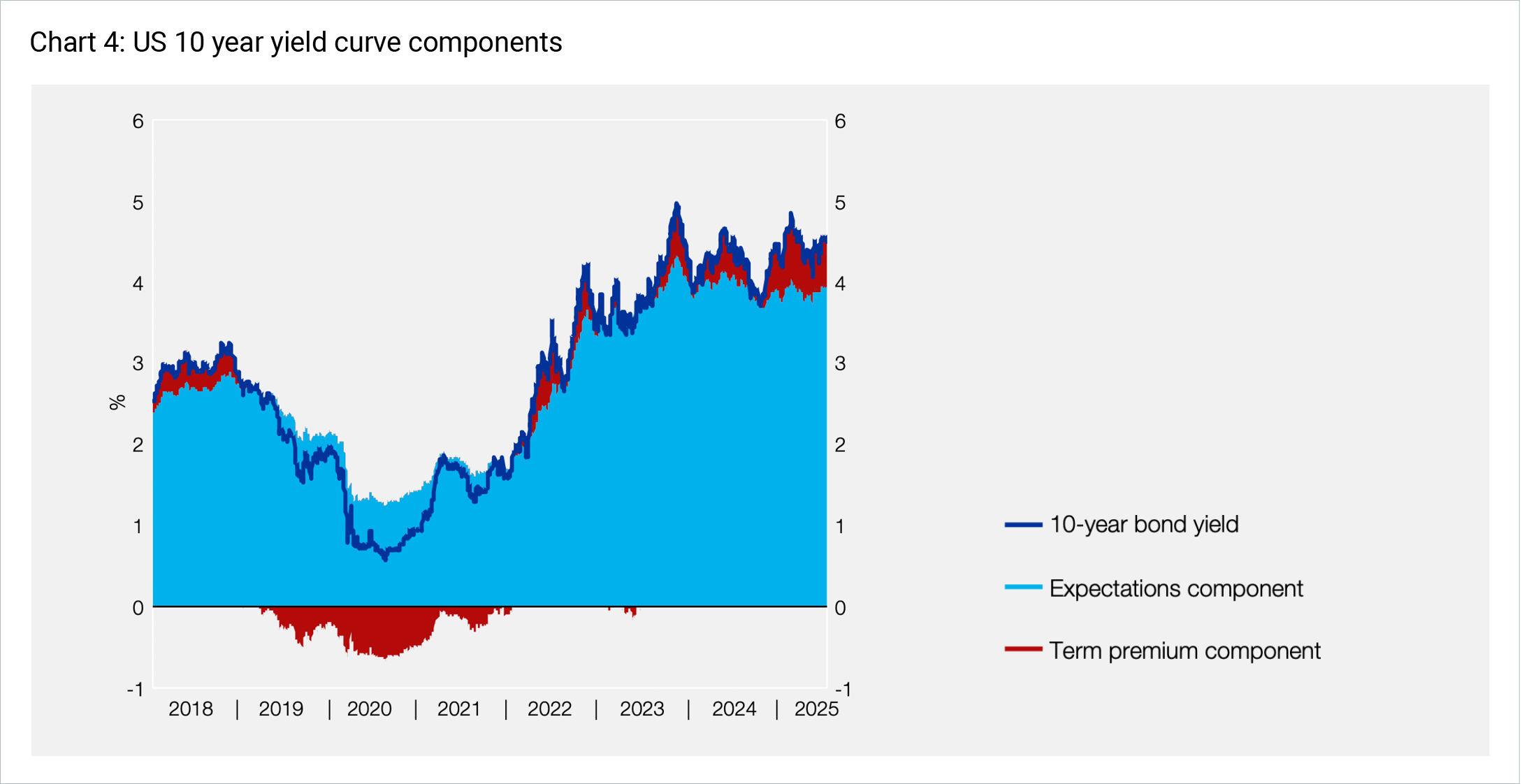

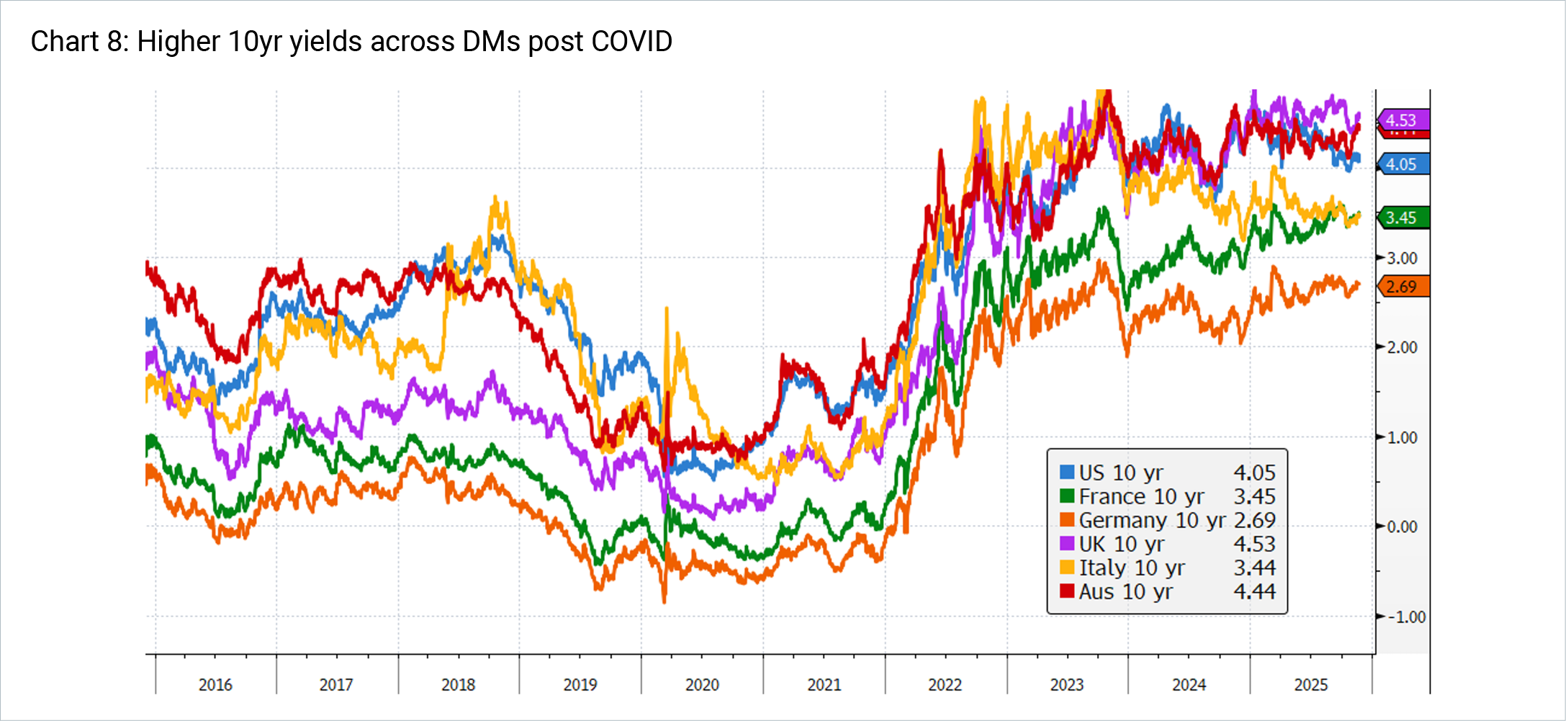

News and Views: The impact of a steeper yield curve on global listed infrastructure 4D Infrastructure December 2025 15-minute read Utilities and infrastructure valuations, typically sensitive to long-term yields, have been challenged by an exceptional rise in US bond yields despite significant Fed rate cuts, prompting an examination of the drivers, sustainability, and implications of this move for global listed infrastructure sectors. Utilities and infrastructure companies own very long dated assets characterised by high up front capital costs and returns often correlated to economic parameters. As such their valuations can be sensitive to changes in long term bond yields, some sectors more than others. The sharp inflation spike of 2021-22 led the US Fed to raise rates at a record pace, from 0.25% to 5.5% over 18 months, representing a headwind for certain segments of the infrastructure universe, particularly US utilities (no explicit inflation or interest rate pass through). Positively, this Fed action reigned in inflation and market expectations turned to Fed cuts. The subsequent easing cycle, commencing in September 2024, was expected to be a tailwind for infrastructure and in particular for utilities that have strong fundamental linkages to interest rates. While Fed interest rate cuts of at least 25bps generally coincide with a decline in long term bond yields this easing cycle has proved to be an anomaly: the Fed has cut by a cumulative 150bps and US ten-year yields have risen by ~50bps. In this News & Views we investigate what has driven this increase, if it can be sustained and the outlook from here. Finally, we then assess the impact this has on global listed infrastructure (GLI) valuations and how 4D manages these risks and opportunities. Bond yields - short & long term, components & moves after Fed cutsShort term yields are mainly driven by central bank policy rates and near-term inflation and growth expectations. By contrast, long term yields reflect expected future short-term rates as well as longer-run views on inflation, growth and a 'term premium' for compensating investors for the risk of holding longer dated bonds. Specifically, recent studies on the parameters affecting bond yields across maturities point to two key components:

As an infrastructure investor, the level and direction of long term yields are more important to us than short term moves as they have the largest impact on valuations, portfolio construction and risk management. As mentioned above, the inflation spike from very loose COVID monetary and fiscal policies led to a very steep Fed rate hiking cycle in 2022. The subsequent fall in inflation from above 9% to towards the Fed's 3% target led to the shifting of market expectations to an easing cycle.

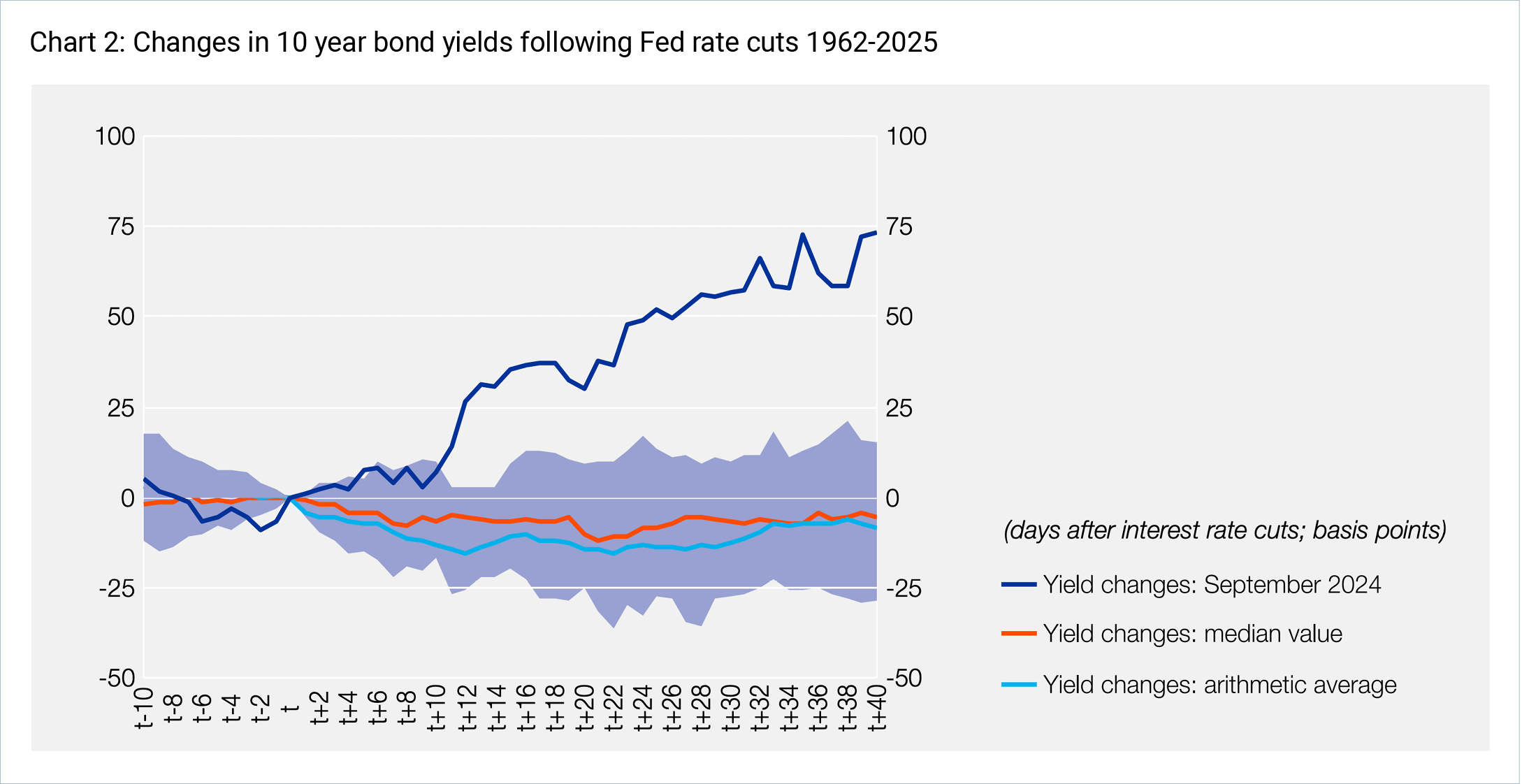

According to central bank research, since the 1960s Fed cuts of at least 25bps are followed by an average decline in long term bond yields of 10-16bps over the following calendar month, before stabilising at the lower level.2 This can be seen in the lower blue and red lines in Chart 2 below.

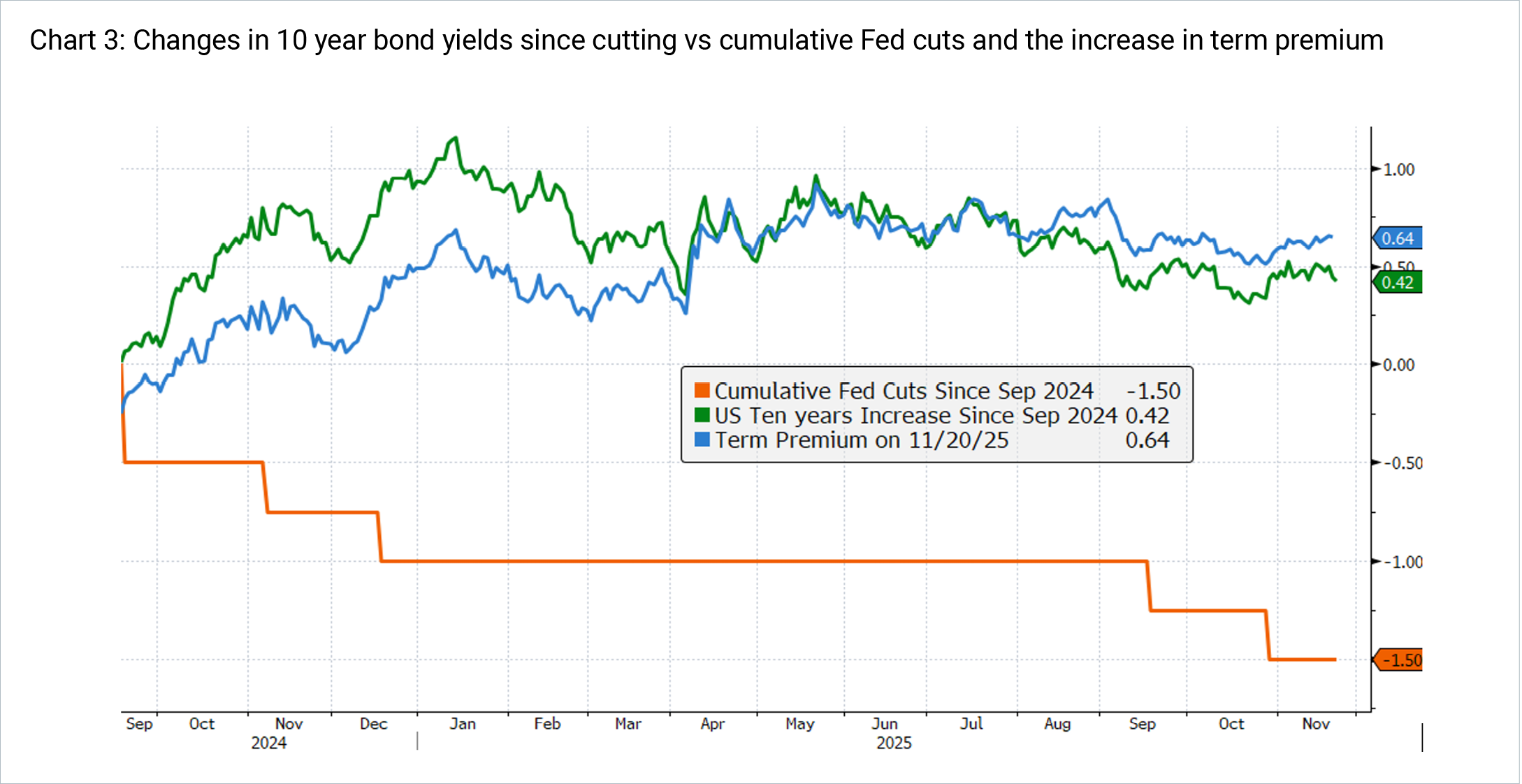

The market movements since the Fed started cutting in September 2024 have been very different to the historical price action seen above. As can be seen in Chart 3, as at November 2025 the Fed has cut 150bps while 10 year yields have increased 42bps. This move is rare - with this level of increase in the upper 10% of historical observations in the chart above, where the dark purple shaded area is the 25%-75% range of observations in the distribution.

In order to investigate the reasons for the long bond yield increase, we can split up the components of the yield into its expectations component and term premium (explained above). We can see that over this recent period, the expectations component was largely stable (the light blue in Chart 4).

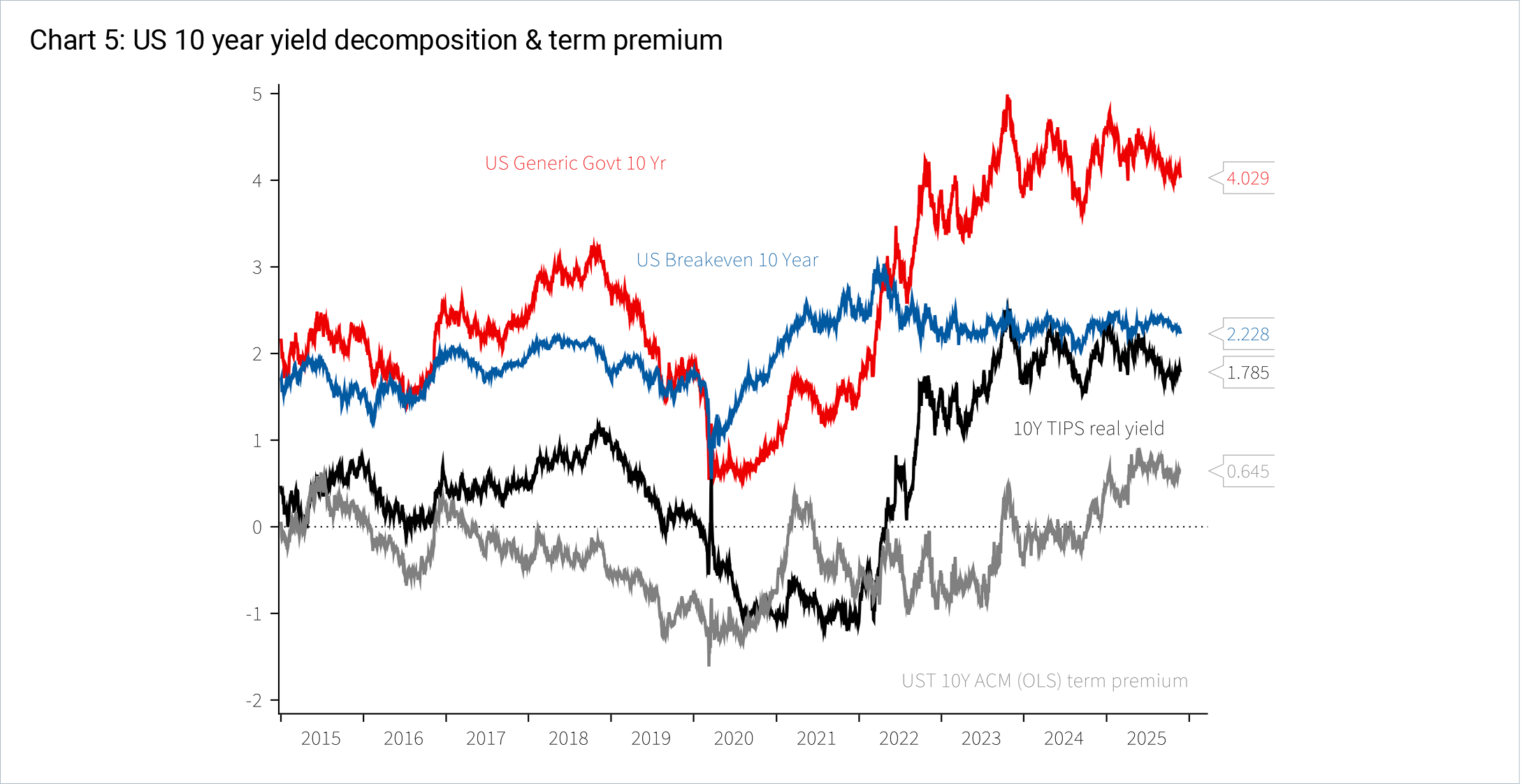

Furthermore, as can be seen in Chart 5, inflation expectations have stayed broadly stable too, indicated by the US breakeven below in blue.

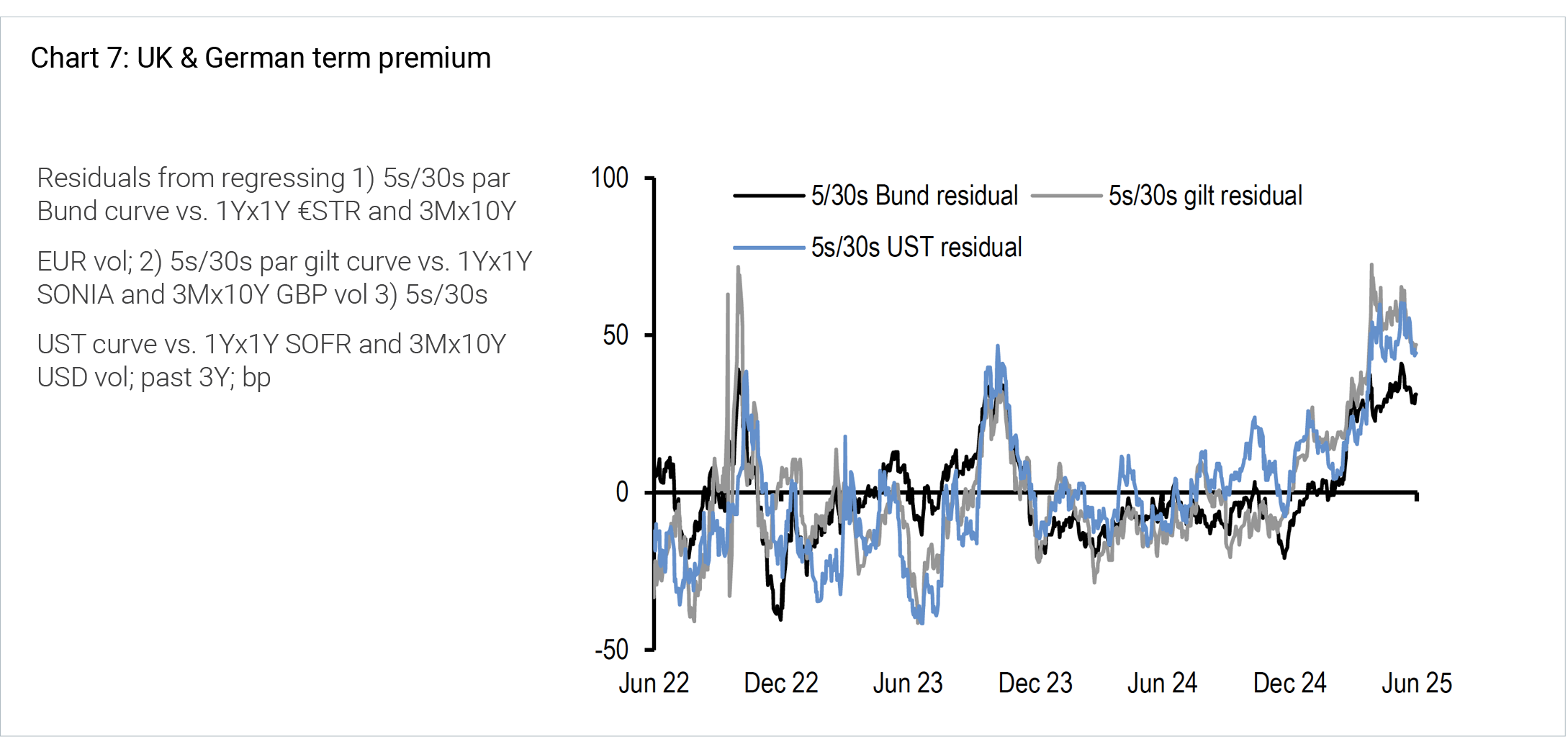

This implies that an increase in term premium has caused a steepening of the yield curve, despite short rates dropping since September 2024. The term premiumOver 2025 there has been a lot of debate among central bankers, academics and market participants, as to the cause of the increase in term premiums by 50-100bps since the Fed's easing cycle began in 2024. Arguments include:

Other reasons for a steepening in the curve:

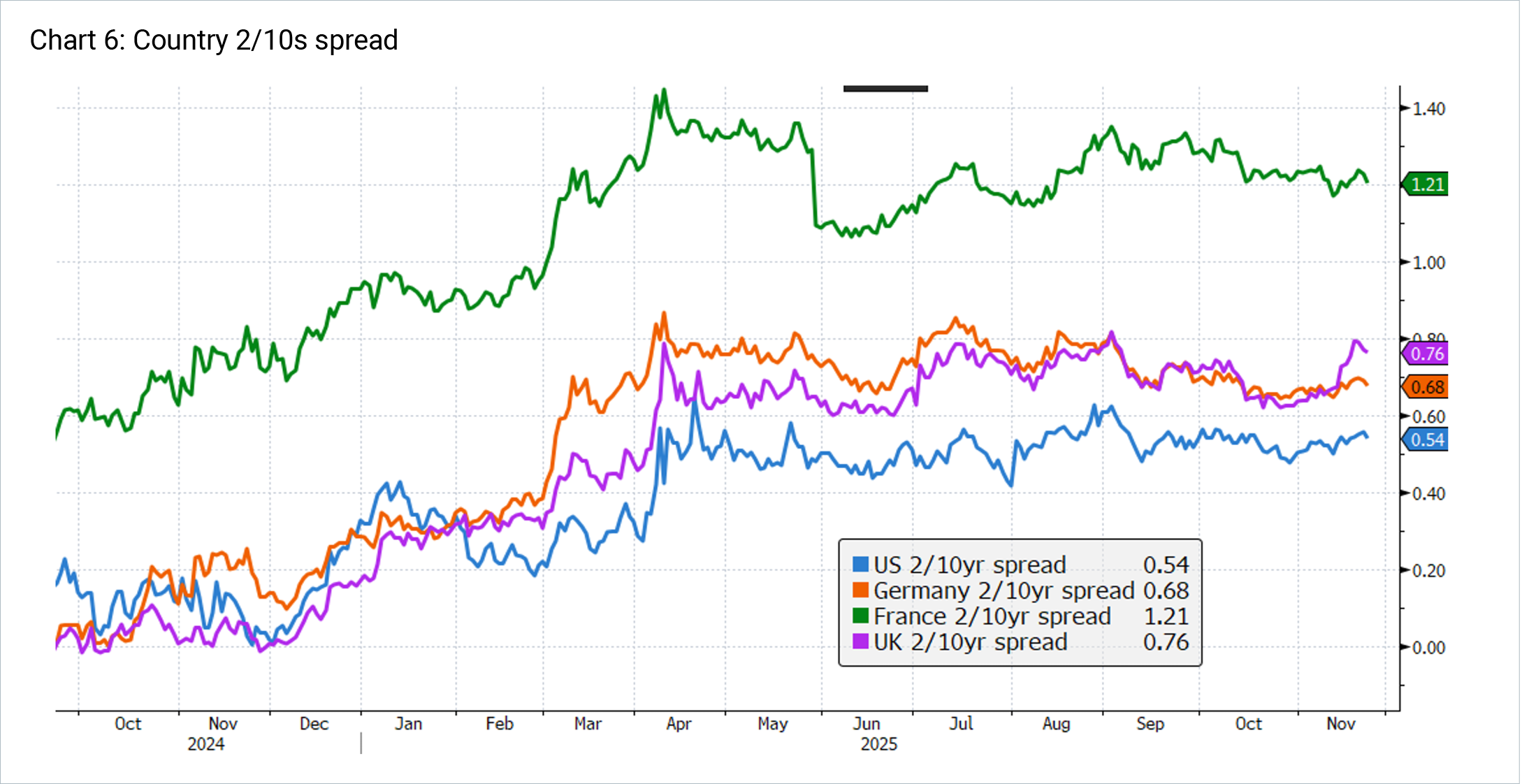

US Fed Governor Michelle Bowman summed up another risk of higher yields brought on by higher term premiums in a speech on 26 September 2025: Term premiums...A second challenge for monetary policy would be a significant rise in longer-term interest rates driven by higher term premiums, which could offset a reduction in the expectations component stemming from monetary policy easing. This scenario would weaken the transmission of changes in the policy rate to economic activity, as investment decisions of households and businesses are dependent on longer-term rates, such as mortgage rates and corporate bond yields.5 While the term premium has risen sharply, and many are looking for reasons why, it is worth noting that it remains below levels that persisted prior to the GFC. As JP Morgan note, "while this is a big move, it is not unexpected: term premium has retraced closer to average levels observed in the decade prior to the GFC, and does not seem to be unduly high in our opinion right now. Moreover, the demand for longer duration assets seems to be receding globally now as well". Transmission mechanism to the rest of the worldThe steeper yield curve has not been isolated to the US. As seen below, German, French and UK yields have also been steepening over the last 18 months - evidenced by the spread between the 2 and 10 year yields. Part of this has been the linkages in sovereign debt markets with the US, while other drivers are country specific. These all include common traits of worsening debt metrics and political impasse:

Likewise, JP Morgan analysis estimates the term premium for these economies, despite fiscal idiosyncrasies between them, remain well correlated.

At an absolute level, long bond yields across developed economies remain higher than pre-COVID. In part this is because of higher long run neutral rates (known as r*), due to structurally higher inflation expectations (less global slack), as well as larger government deficits, higher investment needs and more issuance.

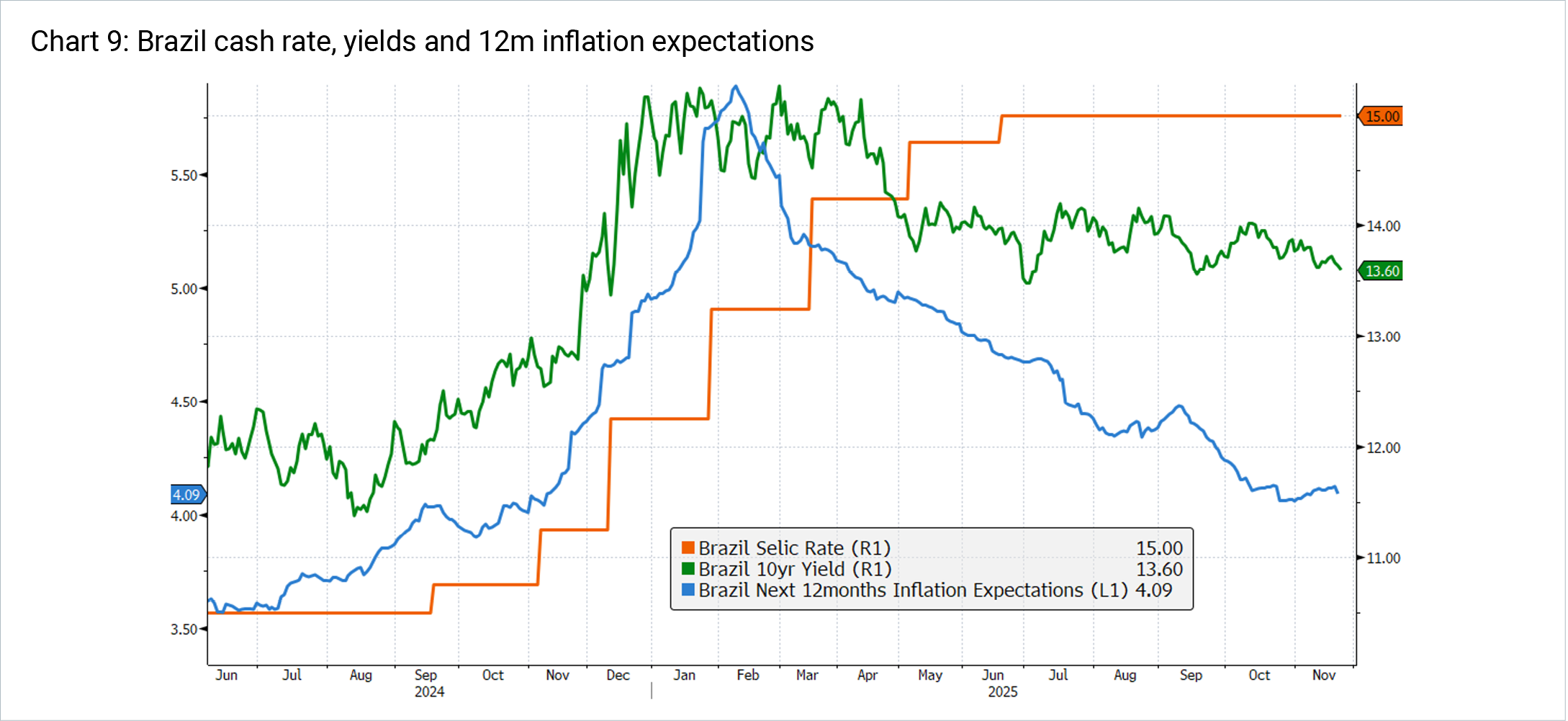

By contrast, Brazil has reported the opposite moves in short term cash rates and long term yields. From mid 2024 the central bank aggressively raised the SELIC rate 450bps to 15% to combat rising inflation expectations due to market expectations of lower government fiscal discipline and constraint around annual budget planning. This aggressive hiking cycle, while painful, also aimed to cool strong domestic economic growth. To date this has proved successful, with inflation expectations coming back down towards the target range. Since the start of 2025 cash rates are up 275bps and 10 year yields have actually fallen 120bps. A key reason for this, according to Bloomberg's Brazilian Economist, is the ultra hawkish approach has actually given the central bank a credibility boost, which has reduced the risk perception and lowered inflation expectations. Looking at the 5 year rate, which declined to 13.2% from 15.5% at the start of the year (even as policy rates rose 275bps), Bloomberg states that their "model attributes 150bps of the cumulative 240bp drop to an improvement in risk factors. In our view, this largely reflects reduced concerns over monetary policy making under Gabriel Galipolo, who became central bank governor in January for a 4 year term" 6

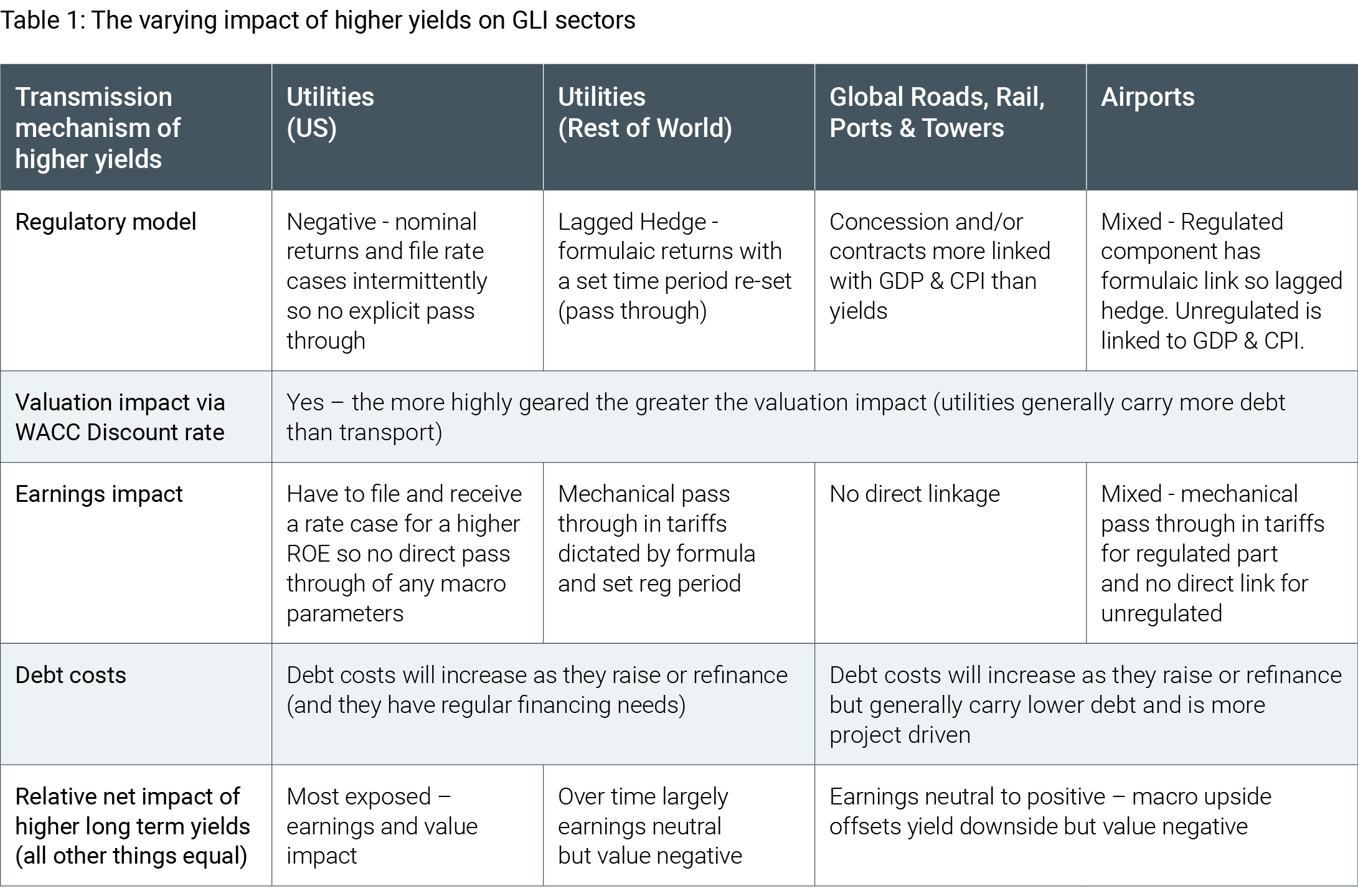

Why this matters - the relationship between infrastructure values and yieldsAt 4D, we use long bond yields to discount the cashflows from these long duration assets. Therefore, a steeper curve - as well as a permanently higher curve - has an impact on valuations of infrastructure assets as a simple function of discount rates. It also impacts fundamental cash flow modelling through forecast regulated return profiles, inflation expectations and borrowing costs, as well as the ability to borrow. In very general terms, it has a greater impact on the utility segment relative to other sub-sectors due to its greater correlation to economic indicators like government yields (as a building block of regulated returns) and in some cases inflation. This is where stock and sector selection within the GLI universe becomes crucial, and a truly active approach to investing is highly valuable. Across the global infrastructure universe 4D has the ability to shift between geographies and sectors where there is more or less sensitivity to long bond moves (both steepness and level of change) and look for exposures that can fundamentally capitalise on moves better than others - as well as exposures with greater ability to pass through inflation, serving to mitigate the impact of higher rates alone.

Also, ignoring sentiment and historic correlations, a number of sector dynamics are supporting fundamental growth outside historical long term yield dynamics. This is particularly relevant for the utility sector which is undergoing a seismic shift in investment mandates to support AI and data centre themes (US) and/or network upgrades to support energy transition and replacement spend (Europe). As such, the historic tight correlation of utility share price performance with yields is potentially no longer warranted, as seen in Chart 11 from early 2024.

ConclusionOne must be careful not to naively assume the Fed's easing cycle is a slam dunk for long duration assets such as utilities and infrastructure assets. The long end of the curve drives GLI valuations more than the short end, and since the Fed started cutting rates in 2024 we have witnessed something rare by historical standards - an increase in long term yields. This has been driven by an increase in the term premium, due to increased political and economic uncertainty, worsening debt metrics, long term budget outlooks and supply-demand dynamics. At 4D we monitor these risks and construct and actively manage a portfolio to balance the risks and opportunities across geographies and sectors. Furthermore, with an active approach to portfolio construction, we can target exposures with idiosyncratic drivers of earnings growth to offset these factors, such as those seen in the networks businesses globally.

The content contained in this article represents the opinions of the authors. This commentary in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the authors to express their personal views on investing and for the entertainment of the reader. |

|

Funds operated by this manager: 4D Global Infrastructure Fund (Unhedged) , 4D Global Infrastructure Fund (AUD Hedged) |

Source: 4D, Bloomberg as at 20/11/25M

Source: 4D, Bloomberg as at 20/11/25M Source: Bank of Greece, Federal Reserve Bank of Saint Louis and LSEG

Source: Bank of Greece, Federal Reserve Bank of Saint Louis and LSEG Source: 4D, Bloomberg as at 20/11/25

Source: 4D, Bloomberg as at 20/11/25 Source: Bank of Greece, Federal Reserve Bank of Saint Louis and LSEG

Source: Bank of Greece, Federal Reserve Bank of Saint Louis and LSEG Source: NAB, Bloomberg, Fed Reserve Bank of New York, Macrobond

Source: NAB, Bloomberg, Fed Reserve Bank of New York, Macrobond Source: 4D, Bloomberg

Source: 4D, Bloomberg Source: JP Morgan

Source: JP Morgan Source: 4D, Bloomberg

Source: 4D, Bloomberg Source: 4D, Bloomberg

Source: 4D, Bloomberg

Source: 4D, Bloomberg

Source: 4D, Bloomberg

8 Dec 2025 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

||||||||||||||||||||||

| Paradice Australian Mid Cap Fund - Active ETF | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

Paradice Australian Equities Fund |

||||||||||||||||||||||

|

||||||||||||||||||||||

|

||||||||||||||||||||||

| Antipodes Global SMID Active ETF (ASX: MIDS) | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

||||||||||||||||||||||

| ELM Responsible Investments Global Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

ELMRI ANZ Conviction Fund |

||||||||||||||||||||||

|

||||||||||||||||||||||

|

Want to see more funds? |

||||||||||||||||||||||

|

Subscribe for full access to these funds and over 900 others |

5 Dec 2025 - Laffont's Take on the AI Bubble

|

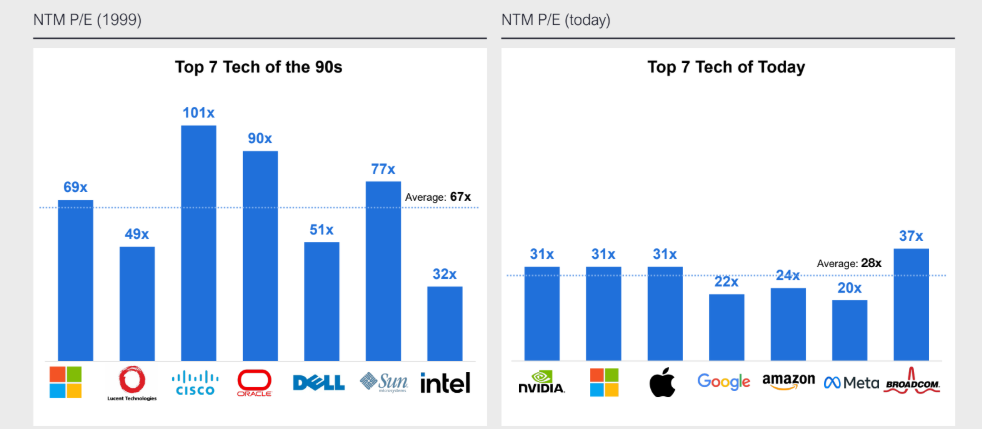

Laffont's Take on the AI Bubble Marcus Today November 2025 5-minute read With Warren Buffett stepping down from public life at 95, younger investors are looking for a new sage to follow. God knows the legendary Buffett gave us enough wise words on life and markets over the years. I'm not sure he can help us today anyway. Buffett's no expert on artificial intelligence, at least as far as I know. He doesn't even have a computer in his office or a smartphone. AI is the new guy's problem. Hunting for a New Buffett in the AI EraWhom to select as a Buffett replacement as the next global sage? Some would suggest Phillipe Laffont might do the trick. He runs a firm called Coatue Management. It now has (approx.) $70bn under management. Laffont's calls on the US tech boom have been prescient for a long time. Last month, Coatue Management released his latest thinking publicly and he addressed the big question of our times: Is AI a bubble, after all? Well, it could be. You can make an argument for the case, and he at least addresses it. Yes, capital expenditure is big. Adoption may not happen on a sufficient scale. The circularity of deals is something to watch for. But Laffont was, and remains, an AI bull. Why the AI Bulls Still Have a CasePerhaps the most compelling point for the bull case, at least for me, is that AI adoption is massive, and yet still so early. There's a long runway here. A further point is that, while the US market is richly valued, it's not crazy, and certainly not like the dot-com boom. You can see how he presents this point below:

Source: Coatue Management We can extrapolate this point further. Much of AI spending is from existing cash flow, at least for now. There isn't the same financial fragility as historic bubbles usually show. Laffont adds that the Big Tech firms may even have lots more cash to splash. That's if a core promise of AI comes to fruition: less labour costs. The numbers around this are quite something. Coatue say that the top 50 tech companies in the US could save $75bn in labour costs annually if AI can reduce headcount by 6%. Imagine what it could do with a higher percentage. All those figures around "headcounts" are to do with human beings, and their livelihoods. There's a big discussion for society to have on this point. But as far as the stock market goes, it leads, all else being equal, to higher profits. Good for share prices. It may not be wise to go against this for too long. Amazon (NASDAQ: AMZN) is already shedding thousands of people. It's usually an early mover on all the big trends. There are no certainties in the markets, or life for that matter. I'm sure Buffett would agree on this point. Bubble Risk vs Opportunity in the Next AI WaveCoatue sees the most likely outcome as AI increasing productivity and GDP. That keeps inflation contained, and, left unsaid, the big US debt problem for another time. Coatue are not blind to the risks. They see a 1/3 chance that the AI bubble bursts and takes the market down with it. But their conclusion seems to be that there's too much potential in the next wave of adoption, such as enterprise AI apps and how AI companies like OpenAI monetise their user base. Don't forget that even a titan like Google (NASDAQ: GOOG) is now under threat here. That should be enough for a lot of companies to shake in their boots... and us watching for the next behemoth to emerge. No moat, a feature so beloved by Buffett, looks safe from the AI encroachment. I can't tell you today what the next wave of AI winners will be. But we won't find them if we don't even look. Rather than fret about whether AI is a "bubble", I'm sure we'll both be better served by looking to see who benefits. That's my takeaway from Laffont's messaging. I'd like to think Buffett might say the same. |

|

Funds operated by this manager: |

4 Dec 2025 - US Private Credit Signals Superior Value Down Under

|

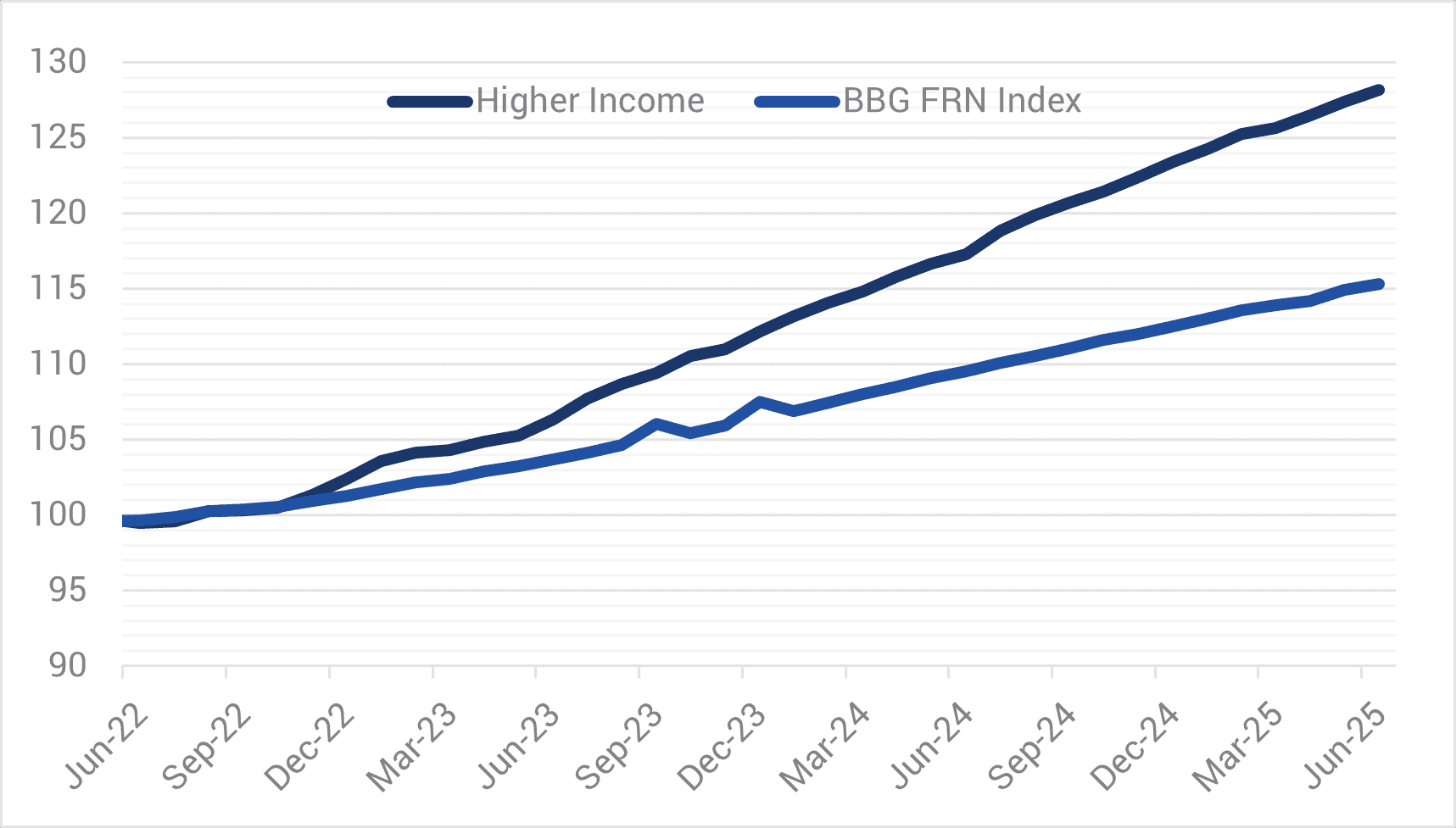

Phil Strano: Is now the sweet spot for active bond management? Yarra Capital Management July 2025 The volatility currently seen in bond markets is being fuelled by a combination of macroeconomic forces. In the U.S., ballooning fiscal deficits and a new $3.8 trillion tax bill are putting upward pressure on long-term interest rates. At the same time, foreign demand for U.S. Treasuries appears to be weakening. Central banks are reducing interest rates, yet are constrained in their influence over longer-dated bonds. Meanwhile, Australia faces a decade of projected deficits of its own, and our yield curve continues to respond more to global forces than domestic settings. These pressures are driving significant steepening in the yield curve - the difference between short- and long-dated bond yields. Steepening curves allow skilled credit managers to adjust risk exposure and capitalize on price differences. In this environment, extending the maturity of our bond holdings has become more appealing, particularly given longer-term bonds can offer stronger price gains as they approach maturity - a dynamic we term "rolldown." At the same time, we're also seeing anomalies in credit spreads, where less sophisticated investors are prioritising yield over relative value, creating pockets of possible mispricing. This is where active management proves its worth. Passive bond funds are bound by index rules. They cannot reposition for anticipated curve moves, nor can they selectively add risk when prices dislocate. Given the Bloomberg FRN Index is more highly rated (average AA- compared to BBB) with shorter spread duration (~two years compared to ~three), the Yarra Higher Income Fund (HIF) is well placed to outperform during risk-on periods (refer Chart 1). However, HIF's outperformance during certain risk-off periods demonstrates the potential benefits of active management. HIF outperformed the index through 2022 in an environment of both higher bond yields and credit spreads and more recently in April 2025. Outperformance in April provides a recent example of how nimble decision-making up and down the curve may contribute to risk adjusted returns. While the FRN Index posted a negative excess return of 11bps compared to the RBA Cash Rate, HIF posted a positive 32 bps excess return despite credit spreads widening by 20-30bps over the month. In April, we started the month expecting volatility around geopolitical events, which prompted us to lift cash levels and position our portfolios with higher overall interest rate duration. Crucially, we also implemented this with a steepening bias or, in other words, a view that long-term interest rates would rise faster than short-term rates. By focusing our exposure on the front of the curve, or short-term bonds, and being underweight long-term bonds at the back end, we were well-positioned when the long end sold off sharply while the short end remained stable. Chart 1 - Cumulative Return - Yarra Higher Income Fund v. Bloomberg FRN Index

Source: YCM/BBG, June 2025.In terms of stock selection, April also presented some fantastic buying opportunities for us to take advantage of spread widening and add high-quality credit exposures at discounted levels. One such name was the USD-denominated Perenti 2029 bonds, an issuer we had previously sold at tight spreads of BBSW+180bps and were able to buy back ~200bps wider (BBSW+380bps). Credit spreads have since contracted ~100bps from these wides, providing a tidy return on investment. While our portfolio positioning has not changed markedly from 12 months ago, these two recent examples show how we're actively managing nimble, benchmark-unaware portfolios that are more 'all-weather' credit in nature. Our April performance, in which both Yarra's Enhanced Income Fund (EIF) and Higher Income Fund (HIF) posted positive absolute returns, underscores the value of our approach. Our strategy came together as a result of preparation, speed, and conviction, none of which are available to passive strategies. Looking beyond the tactical wins, and the case for active credit is supported by the broader macro context. While spread volatility continues, outright yields in the front and mid-parts of the curve have held steady. That means the income on offer remains attractive - and investors are simply being rewarded through a different mix of risk premia. The flexibility to shift between spread and rate risk allows us to preserve capital and position for growth, depending on where the market is offering best value. It's a powerful setup. Investment-grade credit today is offering yields that, on a 12-month view, look comparable to long-term equity market returns - but without the same drawdown risk. Across the spectrum, private credit looks less compelling: the illiquidity and default risk required to justify allocations to private credit simply aren't being compensated in this environment. Looking ahead, we see the drivers of this opportunity set - fiscal overreach, inflation variability, and steepening curves - as persistent features of the bond market over the next 6 to 12 months. We believe this is a sweet spot for credit investing. High running yields and steeper curves, allowing active positioning across durations are compelling and signal the era of 'buy everything and wait' in fixed income is over. Today's market rewards clarity of view, agility of execution, and a willingness to lean into volatility when others step back. |

|

Funds operated by this manager: Yarra Australian Bond Fund , Yarra Australian Equities Fund , Yarra Emerging Leaders Fund , Yarra Income Plus Fund , Yarra Enhanced Income Fund , Yarra Australian Smaller Companies Fund , Yarra Ex-20 Australian Equities Fund , Yarra Global Small Companies Fund , Yarra Higher Income Fund |