Find a Fund

Peer Group Analysis »

| Index Selector Links | 1 Year | 3 Year | 5 Year |

|---|---|---|---|

8.41% |

7.02% |

8.38% |

|

5.96% |

5.95% |

3.07% |

|

45.16% |

40.64% |

48.57% |

|

20.19% |

10.53% |

6.55% |

|

12.54% |

8.27% |

9.13% |

|

14.15% |

11.57% |

10.67% |

|

15.16% |

9.50% |

7.95% |

|

12.90% |

10.71% |

11.36% |

|

17.83% |

16.34% |

11.76% |

|

20.31% |

11.45% |

10.04% |

|

20.69% |

17.27% |

11.68% |

|

15.17% |

8.89% |

10.39% |

|

9.40% |

7.53% |

7.10% |

|

8.20% |

8.42% |

7.45% |

|

7.87% |

0.36% |

4.35% |

|

8.88% |

8.75% |

7.76% |

Hedge Clippings

Hedge Clippings | 06 December 2024

As we approach the end of the year it's normal to reach for the crystal ball and peer into the future. This is particularly the case as there's so much at stake, and so much that might - or in the case of the RBA's stance on interest rates...

Read more...

15 Jan 2025

Performance Report: 4D Global Infrastructure Fund...

The 4D Global Infrastructure Fund (Unhedged) rose by +5.75% over the past 12 months. Since inception in March 2016, the fund has returned +8.9% per...

15 Jan 2025

Performance Report: Bennelong Australian Equities...

The Bennelong Australian Equities Fund rose by +7.07% over the past 12 months. Since inception in February 2009, the fund has returned +11.69% per...

15 Jan 2025

10k Words | January 2025

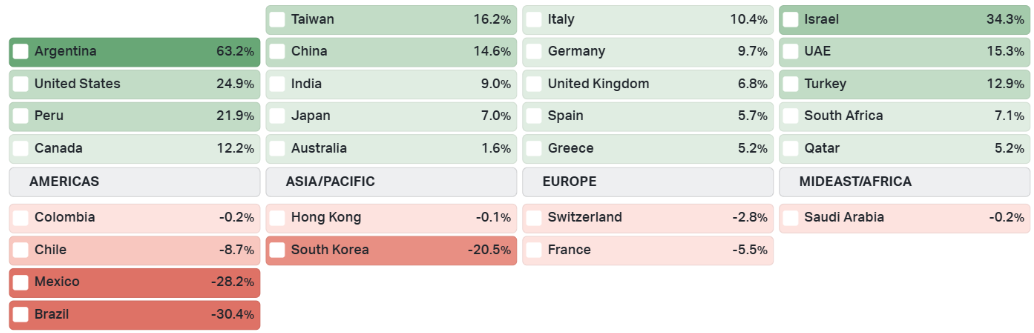

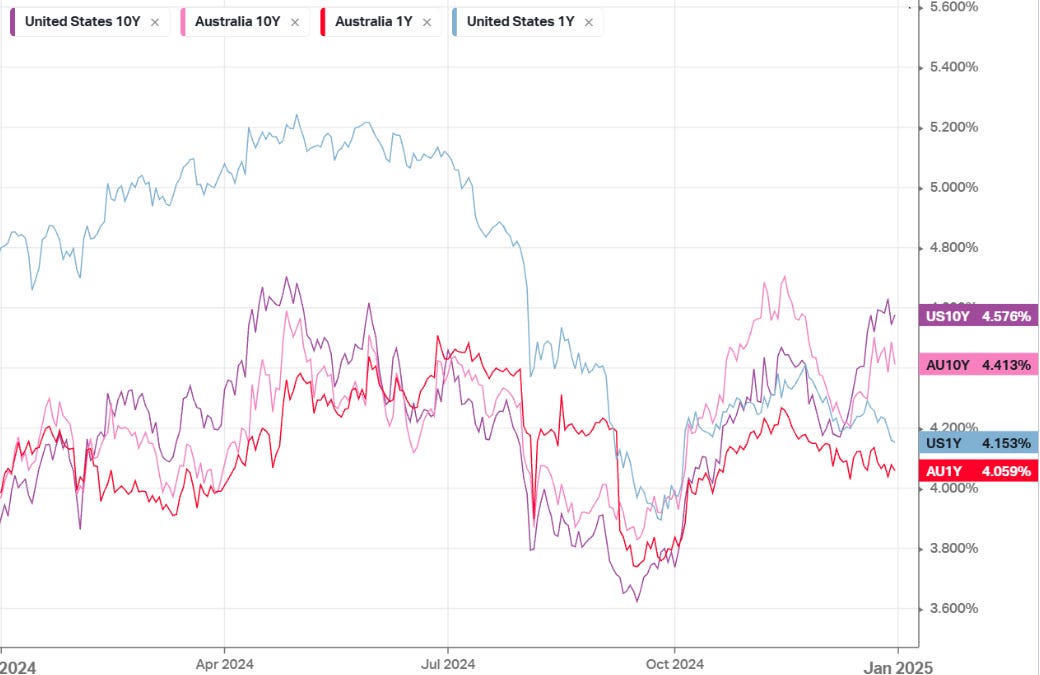

Only Argentina's sharemarket outpaced the US in CY2024, with a mediocre performance from Australia; 10-year bond yields expanded despite the Federal...

14 Jan 2025

The door for rate cuts opens further

Australia's latest GDP figures suggest the door for rate cuts has opened further, writes Pendal's head of government bond strategies.

Source: Westpac Economics

Source: Westpac Economics

13 Jan 2025

Understanding Bridging Loans: A Comprehensive...

In the world of finance, the term "bridging loan" often comes up in conversations about short-term funding solutions. Bridging finance may seem...

20 Dec 2024

Performance Report: Insync Global Quality Equity...

The Insync Global Quality Equity Fund rose by +5.57% in November, outperforming the All Countries World (AUD) benchmark by +0.57%. Since inception in...

20 Dec 2024

Performance Report: Insync Global Capital Aware...

The Insync Global Capital Aware Fund rose by +5.24% in November, outperforming the All Countries World (AUD) benchmark by +0.24%. Since inception in...

20 Dec 2024

Performance Report: PURE Resources Fund

The PURE Resources Fund returned -0.55% in November, outperforming the S&P/ASX Small Resources TR benchmark by +4.83%. Since inception in May 2021,...

20 Dec 2024

Performance Report: PURE Income & Growth Fund

The PURE Income & Growth Fund rose by +6.85% over the past 12 months. Since inception in December 2018, the fund has returned +10.06% per annum, an...

20 Dec 2024

Performance Report: ECCM Systematic Trend Fund

The ECCM Systematic Trend Fund rose by +6.29% in November, outperforming the SG Trend benchmark by +3.02%. Since inception in January 2020, the fund...

Online Applicatons

Free, simple and secure

Olivia123 - the fast simple and secure online alternative to completing paper based application forms.