No events currently listed.

Find a Fund

Peer Group Analysis View All»

| Index Selector Links | 1 Year | 3 Year | 5 Year |

|---|---|---|---|

13.37% |

9.29% |

9.27% |

|

5.11% |

5.70% |

2.95% |

|

-22.38% |

20.10% |

11.14% |

|

26.94% |

15.82% |

7.06% |

|

14.71% |

9.55% |

7.96% |

|

18.74% |

14.02% |

10.54% |

|

12.06% |

12.13% |

5.56% |

|

9.37% |

9.39% |

8.70% |

|

7.85% |

15.41% |

9.46% |

|

12.97% |

11.33% |

6.83% |

|

18.54% |

17.20% |

9.16% |

|

21.40% |

13.39% |

12.62% |

|

10.44% |

9.28% |

6.86% |

|

6.63% |

8.47% |

6.99% |

|

2.69% |

-0.01% |

3.15% |

|

8.33% |

8.74% |

7.90% |

Hedge Clippings

2 Apr 2026 - Hedge Clippings|02 April 2026

|

|

|

|

Hedge Clippings | 02 April 2026 Active vs Passive: why averages can send you in the wrong direction The latest S&P report says most active managers underperformed their benchmark over the past 12 months. Fair enough. That is the headline. But as ever in funds management, the headline is only half the story. Because averages can be deceptive. It is a bit like the old line about having your head in the oven and your feet in the freezer - on average, you are fine. In practice, not so much. The same applies to active management. Saying that the "average" manager underperformed may be statistically correct, but it tells investors very little about the spread of outcomes, or whether strong active managers were still well worth backing. Take Australian Small and Mid Cap funds. Over the past 12 months, only 22% beat the S&P/ASX Small Ordinaries Index return of 22.75%. That sounds like a damning result for active management. But those funds that did outperform returned an average of 32%, and three delivered more than 50%. Suddenly the story looks less like "active failed" and more like "picking the right manager mattered a lot". Stretch the horizon to seven years and the picture changes again. More than 67% of Australian small-cap funds outperformed the index, which returned just 8.73% per annum. The average return of the outperformers was 13.04% per annum, while the top five averaged 20% per annum. That is not a rounding error. That is a meaningful gap. Australian Large Cap funds tell a different story. Over the last 12 months, 40% outperformed the S&P/ASX 200 Total Return Index, which returned 7.37%. Those outperforming funds averaged 15.27%, beating the index by almost 8%. But over seven years, only 32% stayed ahead, with outperformers averaging 12.16% per annum versus the index's 10.13%. Then there are Equity Alternative funds - long/short and market neutral strategies - which flipped the script again. Over the past year, 62% of global funds and 53% of Australian funds outperformed their respective indices, with outperformers averaging 29% and 27%. Over seven years, however, those figures dropped sharply, with only 25% of global funds and 35% of Australian funds outperforming, and the margin of outperformance narrowing to 3% and 5%. So what is the takeaway? First, averages make neat headlines, but messy realities. They flatten out the differences that actually matter. Second, outcomes depend heavily on where you look. Small caps, large caps and alternatives do not behave the same way. Nor do Australia and global markets. Third, market conditions matter. In strong markets, weak markets and sideways markets, the proportion of active managers outperforming can shift materially. The real lesson is not that active always wins, or that passive always does. It is that broad-brush conclusions can miss the point. Investors do not own the average fund. They own a specific fund, run by a specific manager, with a specific process. That is why manager selection remains critical. The data may show that many active funds underperform, but it also shows that the better managers can add real value - and sometimes a lot of it. The trick is knowing how to separate them from the pack. That is where detailed performance analysis matters. Or, for those who prefer a shortcut, a disciplined framework such as AFM's Star Rankings across multiple timeframes can help identify the managers that have delivered consistently, rather than occasionally. Because in funds management, averages may make the news. But selection drives outcomes. News | Insights Waymo has 70 Humans Running 3000 Vehicles | Insync Fund Managers Software risk or renaissance? | Magellan Investment Partners February 2026 Performance News |

|

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday |

2 Apr 2026 - Unravelling the forces driving corporate credit's resilience

|

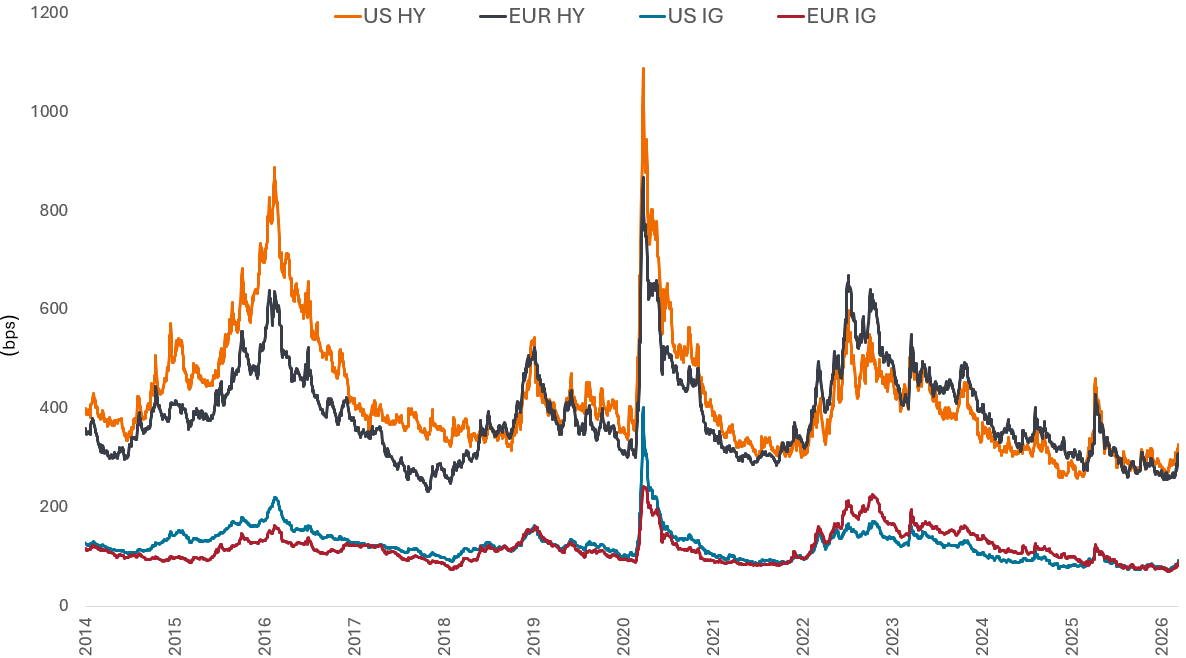

Unravelling the forces driving corporate credit's resilience Janus Henderson Investors March 2026 (8-minute read) Corporate credit has absorbed recent shocks with limited disruption. Head of High Yield Tom Ross and Corporate Credit Portfolio Manager James Briggs examine how fundamentals, market behaviour and dynamics as well as macro context are shaping credit resilience. Credit markets sanguine amid geopolitical riskThe conflict in the Middle East has drawn parallels with the outbreak of the Russia-Ukraine War, with concerns that an oil-induced supply and inflation shock could harm the global economy. So far, credit markets have reacted in a sanguine manner, with changes in credit spreads not dissimilar to the rates impact from rising government bond yields. As the chart below shows, the recent tick-up in credit spreads is muted when compared to last year's Liberation Day sell-off, let alone the 2015 energy sell-off after oil prices collapsed or the Covid spike. For now, the market assumption is that the conflict remains regional, although high oil and gas prices - caused by Iran's choke hold on ships transiting the Strait of Hormuz - could have a material impact on inflation and consumption were they to be sustained beyond the short term. For the time being, geopolitical shocks have not yet translated into a material deterioration in key economic data. So far, we see this as a volatility event rather than an economic event impacting inflation and consumption. Figure 1: Credit spread on high yield and investment grade corporate bonds

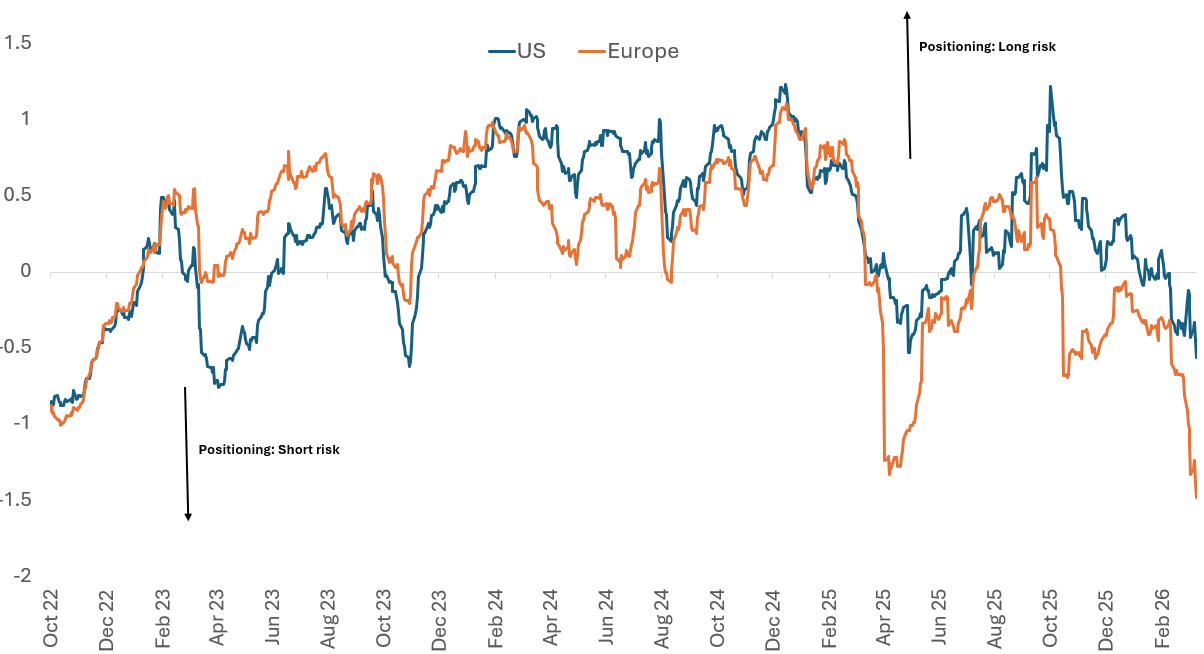

Source: Bloomberg, US HY = US High Yield:ICE BofA US High Yield Index; EUR HY = Euro High Yield: ICE BofA Euro High Yield Index, US IG = US investment grade: ICE BofA US Corporate Index, EUR IG = Euro Investment Grade: ICE BofA Euro Corporate Index, Govt OAS (option adjusted spreads over governments), 01 January 2014 to 13 March 2026. Bps= basis points. Spreads may vary and are not guaranteed. Past performance does not predict future returns. The forces behind corporate credit's resilienceWe believe there are several reasons why the corporate bond markets have responded in such an orderly way. First, investor positioning is light given credit spreads are at the tighter end of historical ranges (Figure 2). Anecdotally, most investors were neutrally positioned heading into this conflict and waiting for more attractive valuations to add risk. Recall that there had been nervousness around artificial intelligence (AI) disruption and private credit fears earlier in the year. Figure 2: Positioning in credit is light, as market trades short

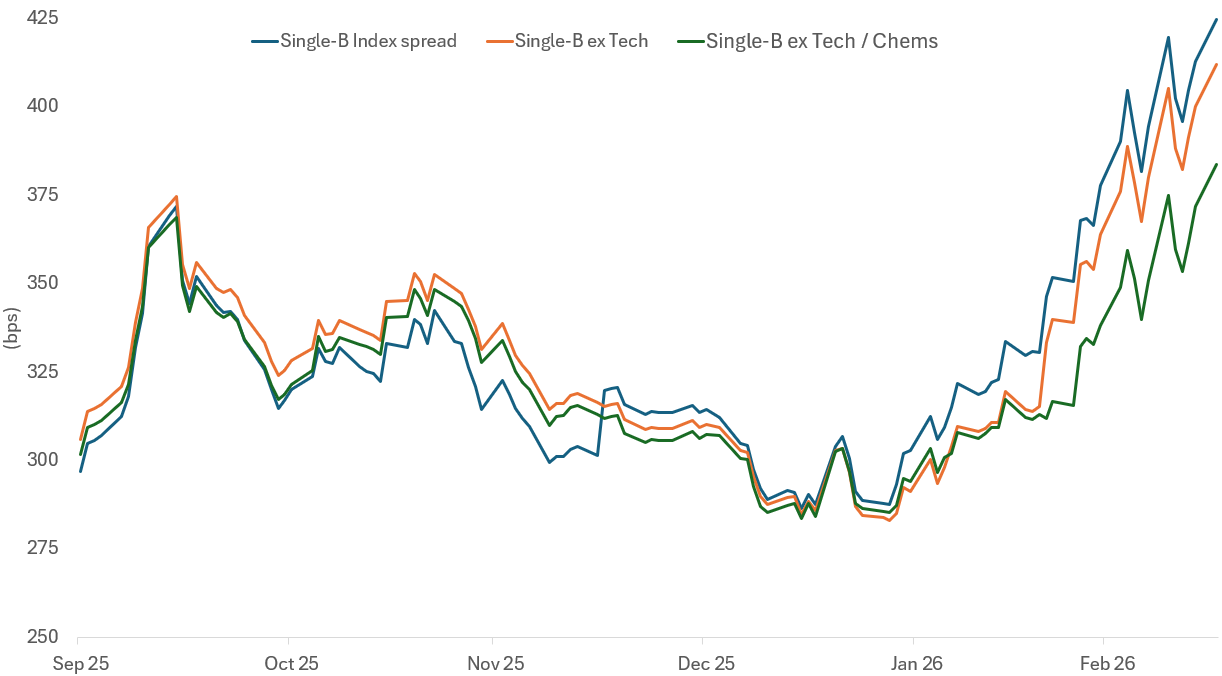

Source: ICI, Bloomberg, DTCC, BNP Paribas. The BNPP Positioning Indicator (BNPPIUS, BNPPIEU) reflects data on dealer inventories, funds' cash balances, Commodity Trading Advisors (CTA) positioning, Credit Default Swap (CDS) market positioning and option hedging, as at 12 March 2026. The BNPP Credit Positioning Indicator shows how long (positive number) or short (negative number) investors are positioned in credit markets, indicating whether exposure to credit risk is extended, neutral or defensive. Second, there has already been a reasonable amount of corporate bond issuance so far this year. US investment grade issuance was US$474 billion in the first 10 weeks of the year, up 6% compared to the same period in 2025, and US high yield and loans (leveraged finance) issuance was US$64 billion, up 34% compared with the same period in 2025. Over the same period European investment grade issuance is €170 billion, down a marginal 3%, but European high yield is €23 billion, up 40% year- on-year.1 A key concern has been the scale of tech-related issuance, particularly for the investment grade market. However, the hyperscalers have made good progress with their capital raising, with Oracle claiming they do not expect to issue any additional bonds for the remainder of the calendar year 2026.2 Taken together, companies have been successful in borrowing earlier in the year which should take some pressure off needing to come to the market in the very near term. The strong technical (market dynamics) picture that has been in place should remain intact. Third, turning to demand, higher yields are already attracting yield sensitive buyers, such as insurance companies stepping in as we have heard anecdotally. Yields on US high yield are back above 7% and are at 5.7% in European high yield. US investment grade is above 5% and European investment grade at 3.5%.3 As explained earlier, a portion of the yield change has been due to the rise in government yields reflecting higher inflation expectations. This has led to a moment of positive correlation between rates and credit spreads, which tends to be temporary. Credit fundamentals resilientAnother backstop to credit spreads is that corporate fundamentals generally remain supportive. Earnings expectations have not rolled over and continue to underpin credit quality. Near�'term earnings face a relatively low hurdle, as Q1 results last year were depressed by tariff speculation, limiting downside risk as we move through the upcoming earnings season. Consensus expectations point to a healthy 20% earnings-per-share growth by Q4 versus Q1, consistent with the typical second�'half earnings catch�'up seen in prior years. Even if those forecasts ultimately prove optimistic, interest rate coverage - earnings covering interest expenses - are broadly stable across investment grade and leveraged finance (high yield and loans). With macro growth still resilient - particularly in the US - credit quality is expected to remain robust enough to absorb market volatility. This provides a supportive macro backdrop for sufficient cashflows to service generally stable and manageable leverage levels. With all�'in yields at attractive levels, fundamentals and earnings serve as the anchor to allow investors to lean into wider spreads where attractive risk-adjusted potential can be captured. This is rather than idiosyncratic risk or geopolitical volatility spooking investors as signalling the start of a more adverse credit cycle. Idiosyncratic stress is rising - but is not systemicTo take a step back then, there is no evidence of a broad earnings downgrade cycle emerging across investment grade or high yield credit. Recent market volatility is increasingly being driven by idiosyncratic rather than broad�'based credit risk, with stress emerging unevenly across sectors and issuers. One area this surfaced in is software, where dispersion widened sharply and price action was severe in specific names as AI-related concerns dominated around revenue displacement. While software is a small component of high-yield indices, the volatility emerged more in the loans market, which has become increasingly bifurcated and private credit. For loans, selective mispriced opportunities have emerged, while CLOs, the main buyer of loans, continue to launch, with many warehouses looking for loans, supporting demand in the near term. This is important as leveraged finance does well in environments where readily available refinancing is present. Private credit, on the other hand, is facing rising redemption pressure. We are seeing headlines around the gating of funds and increased scrutiny of asset values, alongside banks reassessing collateral valuations and pulling back from certain lending relationships. Nevertheless, this adjustment appears to be gradual and uneven, unfolding over time rather than triggering an immediate spillover into public markets. In this context, stress in private markets need not be destabilising for public credit. As capital becomes more cautious it tends to be redeployed conservatively, such as into short-dated bonds or liquid investment grade credit. This may present a modest but constructive technical (demand) for public markets, particularly at a time when yields have become more attractive and markets are sensitive to reward the winners. Rising dispersion from a K-shaped economy

Figure 3: Single Bs are tighter excluding technology and chemicals

Source: Barclays, as 16 March 2026. Spreads may vary and are not guaranteed. Past performance does not predict future returns. For credit investors, this creates an opportunity that is incremental rather than wholesale. Valuations have moved off their tightest levels, but remain far from historic stress points, suggesting scope to add risk selectively. With spreads still tight in aggregate and macro uncertainty elevated, timing and discrimination matter. After all, historical analysis suggests that oil price shocks typically take months to mean-revert once conflicts stabilise. The opportunity therefore lies not in chasing beta, but in leaning into dispersion and adding risk where repricing has been meaningful and fundamentals remain intact, while remaining cautious where valuations have yet to adjust. In that sense, the current environment rewards patience and selectivity, allowing credit investors to engage constructively and with confidence that the forces underpinning resilience remain firmly in place, and in some cases appear to have strengthened. |

|

Funds operated by this manager: Janus Henderson Australian Fixed Interest Fund , Janus Henderson Conservative Fixed Interest Fund , Janus Henderson Diversified Credit Fund , Janus Henderson Global Natural Resources Fund , Janus Henderson Tactical Income Fund , Janus Henderson Australian Fixed Interest Fund - Institutional , Janus Henderson Conservative Fixed Interest Fund - Institutional , Janus Henderson Cash Fund - Institutional , Janus Henderson Global Multi-Strategy Fund , Janus Henderson Global Sustainable Equity Fund , Janus Henderson Sustainable Credit Fund All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect. The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested. Whilst Janus Henderson believe that the information is correct at the date of publication, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson to any end users for any action taken on the basis of this information. |

1 Apr 2026 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

||||||||||||||||||||||

| Fidelity Japan Equities Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

|

||||||||||||||||||||||

| Aquasia Residual Stock Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

|

||||||||||||||||||||||

| Senjin Capital Fund I | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

Want to see more funds? |

||||||||||||||||||||||

|

Subscribe for full access to these funds and over 900 others |

31 Mar 2026 - Performance Report: Equitable Investors Dragonfly Fund

[Current Manager Report if available]

31 Mar 2026 - Software risk or renaissance?

|

Software risk or renaissance? Magellan Investment Partners February 2026 (5-minute read) |

|

Artificial intelligence (AI) is driving a structural shift across the technology landscape. This transition has sparked recent fear regarding the long-term viability of traditional software vendors and their established business models. Much of this fear stems from the perceived disruptive threat of AI challengers and the falling cost of software development. In our view, AI brings both risk and opportunity to software. It is a mistake to view the sector as a monolith. Software is as diverse as the applications and industry verticals it serves. Consequently, the impact of AI will vary significantly across the spectrum of vendors. When the market penalises the sector as if it were a homogeneous entity, it creates some opportunity to identify mispriced assets. We believe a number of enterprise software incumbents remain among the most attractive investment opportunities today. What exactly are the concerns? We break these down to four distinct areas.

All of these concerns are both valid and, to some degree, observably taking place. The risk-weighted impact, however, depends on the software category and the software vendor being considered.

AI is a transformative development, and we expect further emergence of compelling new applications that could change how people work. Because the software sector is so diverse, what this means for any given vendor depends on their specific circumstances. For some software names, AI will be disruptive and a risk to their business models. For the highest-quality software vendors like SAP, Microsoft and Intuit, AI is likely to bring a 'renaissance' of opportunity. Adrian Lu, Senior Investment Analyst |

|

Funds operated by this manager: Magellan Global Fund (Open Class Units) ASX:MGOC , Magellan Infrastructure Fund , Magellan Global Opportunities Fund No.2 , Magellan Infrastructure Fund (Unhedged) , Magellan Global Fund (Hedged) , Magellan Core Infrastructure Fund , Magellan Global Opportunities Fund Active ETF (ASX:OPPT) Important Information: This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 trading as Magellan Investment Partners ('Magellan Investment Partners') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision about whether to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to a Magellan Investment Partners financial product may be obtained by calling +61 2 9235 4888 or by visiting www.magellaninvestmentpartners.com Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of a Magellan Investment Partners financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. No guarantee is made that such information is accurate, complete or timely and no warranty is given regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Magellan Investment Partners or the third party responsible for making those statements (as relevant). Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. No representation or warranty is made with respect to the accuracy or completeness of any of the information contained in this material. Magellan Investment Partners will not be responsible or liable for any losses arising from your use or reliance upon any part of the information contained in this material. Any third-party trademarks contained herein are the property of their respective owners and Magellan Investment Partners claims no ownership in, nor any affiliation with, such trademarks. Any third-party trademarks contained herein are the property of their respective owners, are used for information purposes and only to identify the company names or brands of their respective owners, and no affiliation, sponsorship or endorsement should be inferred from such use. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Magellan Investment Partners. (080825-#W17) |

30 Mar 2026 - Performance Report: ASCF High Yield Fund

[Current Manager Report if available]

30 Mar 2026 - Waymo has 70 Humans Running 3000 Vehicles

26 Mar 2026 - Performance Report: DAFM Digital Income Fund (Digital Income Class)

[Current Manager Report if available]

26 Mar 2026 - Becoming wary of software

|

Becoming wary of software Challenger Investment Management March 2026 (9-minute read) Many of you will have seen news over the past few weeks regarding the US Private Credit sector's exposure to software and flow on concerns regarding the impact of AI on the software businesses. Investor concerns have centred around those managers who are most exposed with most press articles focussed on Blue Owl Capital as amongst the largest players in the private credit market they have the highest exposure.

Turning to the domestic private credit market we think the following is important:

The constant challenge for investors which is especially true in this environment is that the assessment of the risk of a fund is not just about the assets, it's not just about the manager and not just about their governance practices. A major determinant of outcomes will be how other investors respond. This is a much tougher proposition for investors to assess - size and scale matters here, access to institutional capital, transparency and approach to governance. A private credit firm with one open ended fund, poor valuation discipline, external leverage and lack of scale is far more exposed than the alternative. Challenger IM Credit Income Fund , Challenger IM Multi-Sector Private Lending Fund For Adviser & Investors Only Disclaimer: This material has been prepared by Challenger Investment Partners Limited (Challenger Investment Management or Challenger), ABN 29 092 382 842, AFSL 329 828. This document does not relate to any financial or investment product or service and does not constitute or form part of any offer to sell, or any solicitation of any offer to subscribe or interests and the information provided is intended to be general in nature only. This should not form the basis of, or be relied upon for the purpose of, any investment decision. This document is not available to retail investors as defined under local laws. This document has been prepared without taking into account any person's objectives, financial situation or needs. Any person receiving the information in this document should consider the appropriateness of the information, in light of their own objectives, financial situation or needs before acting. This document is provided to you on the basis that it should not be relied upon for any purpose other than information and discussion. The document has not been independently verified. No reliance may be placed for any purpose on the document or its accuracy, fairness, correctness, or completeness. Neither Challenger Investment Management nor any of its related bodies corporates, associates and employees shall have any liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of the document or otherwise in connection with the presentation. |

25 Mar 2026 - Performance Report: DS Capital Growth Fund

[Current Manager Report if available]

25 Mar 2026 - Emerging Markets: How AI concerns are impacting India

|

Emerging Markets: How AI concerns are impacting India Pendal March 2026 (5 minutes read time) |

|

Fears that rapid advances in artificial intelligence could slow global IT spending have weakened investor confidence in Indian software stocks. Pendal's Global Emerging Markets Opportunities team investigates the implications for India's growth and current account balance. THE explosion in capability of AI models in recent months has led some equity market participants to become more cautious about the outlook for various service sector industries, leading to selloffs in sectors from software to financial planning. As investors who approach the asset-class primarily through top-down, country-level developments, the GEMO team has been thinking about what this might mean for India. India is one of a group of emerging markets that tend to run current account deficits. "These are countries that have significant latent domestic demand but where, for various historical, geographical or institutional reasons, domestic production falls short. These markets tend to have higher beta to global liquidity and risk appetite," says James Syme, senior fund manager, JOHCM. "Most pertinently for India, the growth cycles of these countries tend to be constrained by inflation and external deficits, with both vulnerabilities reflecting demand running too far ahead of supply." Since the end of 2010, India's current account deficit has averaged 1.7 per cent of GDP, although the maximum deficit was 5.1 per cent of GDP. The structure of the current account balance has developed through time, and changed with India's economic cycle, but some components remain structurally important. In 2025, India ran a deficit in non-oil goods of US$189 billion (4.9 per cent of GDP). Net oil imports were US$122 billion (3.2 per cent of GDP). The resultant trade deficit of US$311 billion (8 per cent of GDP) was substantially offset by a net positive services balance of US$210 billion (5.4 per cent of GDP). Notably, the surplus in IT services was US$227 billion (5.9 per cent of GDP). India also ran a positive income balance of US$85 billion (2.2 per cent of GDP), for an overall current account deficit of US$17 billion (0.4 per cent of GDP). Syme says this relationship between IT service exports and oil imports is key for India's economy, and the two have grown together. In fiscal year 2019, net IT service exports were US$85 billion, and oil imports were US$93.9 billion. "The varying cycles in global IT service spending and the oil price are key for the health of the Indian economy," explains Syme. At a time of higher oil prices, what does the downturn in sentiment towards software and IT service stocks mean for India? In the first two months of 2026, the MSCI India IT Index has fallen over 20 per cent in USD terms. "This is concerning, because the aggregate revenue of India's listed IT companies has a high correlation with the economy's IT service exports," says Syme. If the negative outcome that stocks are pricing in comes to pass, particularly with higher oil prices, India's growth may be constrained by the current account balance. "However, it is important to note that the 12-month forward consensus estimates for both the revenues and profits of the constituents of MSCI India IT Index have increased by 3.4 per cent year to date," notes Syme. "This steady growth in the fundamental outlook for these companies suggests both opportunity in the sector, where we remain overweight, and ongoing support for the Indian economic growth story, although we remain underweight the country on valuation grounds. "We do not feel that share price moves alone constitute a macro-level signal for India at this time." |

|

Funds operated by this manager: Pendal MicroCap Opportunities Fund , Pendal Global Select Fund - Class R , Pendal Sustainable Australian Fixed Interest Fund - Class R , Pendal Focus Australian Share Fund , Pendal Horizon Sustainable Australian Share Fund , Regnan Credit Impact Trust Fund , Pendal Sustainable Australian Share Fund , Pendal Sustainable Balanced Fund - Class R , Pendal Multi-Asset Target Return Fund |

|

This information has been prepared by Pendal Fund Services Limited (PFSL) ABN 13 161 249 332, AFSL No 431426 and is current as at December 8, 2021. PFSL is the responsible entity and issuer of units in the Pendal Multi-Asset Target Return Fund (Fund) ARSN: 623 987 968. A product disclosure statement (PDS) is available for the Fund and can be obtained by calling 1300 346 821 or visiting www.pendalgroup.com. The Target Market Determination (TMD) for the Fund is available at www.pendalgroup.com/ddo. You should obtain and consider the PDS and the TMD before deciding whether to acquire, continue to hold or dispose of units in the Fund. An investment in the Fund or any of the funds referred to in this web page is subject to investment risk, including possible delays in repayment of withdrawal proceeds and loss of income and principal invested. This information is for general purposes only, should not be considered as a comprehensive statement on any matter and should not be relied upon as such. It has been prepared without taking into account any recipient's personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation. The information may contain material provided by third parties, is given in good faith and has been derived from sources believed to be accurate as at its issue date. While such material is published with necessary permission, and while all reasonable care has been taken to ensure that the information is complete and correct, to the maximum extent permitted by law neither PFSL nor any company in the Pendal group accepts any responsibility or liability for the accuracy or completeness of this information. Performance figures are calculated in accordance with the Financial Services Council (FSC) standards. Performance data (post-fee) assumes reinvestment of distributions and is calculated using exit prices, net of management costs. Performance data (pre-fee) is calculated by adding back management costs to the post-fee performance. Past performance is not a reliable indicator of future performance. Any projections are predictive only and should not be relied upon when making an investment decision or recommendation. Whilst we have used every effort to ensure that the assumptions on which the projections are based are reasonable, the projections may be based on incorrect assumptions or may not take into account known or unknown risks and uncertainties. The actual results may differ materially from these projections. For more information, please call Customer Relations on 1300 346 821 8am to 6pm (Sydney time) or visit our website www.pendalgroup.com |

19 Mar 2026 - Expert Analysis of the RBA's March 17 Rate Decision

|

Expert Analysis of the RBA's March 17 Rate Decision FundMonitors.com March 2026 |

|

Chris Gosselin, CEO of FundMonitors.com, spoke with Nicholas Chaplin, Director and Portfolio Manager at Seed Funds Management, and Renny Ellis, Director & Head of Portfolio Management at Arculus Funds Management, about the RBA's decision to raise interest rates by 0.25% in March. Both described the move as premature, noting the narrow 5-4 board vote reflected significant internal disagreement. They argued that last month's rate rise had yet to flow through to the economy, and that the board was relying on last year's inflation numbers prior to the release of the February figure due next week. In a nutshell, the decision to raise rates in March, rather than wait 6 weeks until the meeting scheduled for May 4th and 5th, was premature. The discussion also considered the role of rising oil prices and geopolitical developments, with both suggesting the RBA may have acted too quickly given the uncertain economic outlook. |

16 Mar 2026 - Manager Insights | Allspring Global Investments

|

Chris Gosselin, CEO of FundMonitors.com, speaks with George Bory, Chief Investment Strategist at Allspring Global Investments. They discussed Allspring's public-markets fixed-income approach, focusing on risk-aware portfolio management, steady income above inflation, and global diversification, before turning to how geopolitical tensions, oil prices, inflation, and US politics may shape bond markets and investment positioning. Key topics by timestamp:

|

9 Mar 2026 - Manager Insights | Cyan Investment Management & Equitable Investors

|

Chris Gosselin, CEO of FundMonitors.com, spoke with Dean Fergie, Director & Portfolio Manager at Cyan Investment Management and Martin Pretty, Director at Equitable Investors. They discussed the sharp market volatility during the latest reporting season, driven by elevated expectations around AI, shifting investor sentiment, and significant valuation resets across industrial stocks. The conversation also explored how changing money flows, speculation, and indexing influenced portfolio management and highlighted the importance of diversification in an increasingly volatile investment environment.

|

9 Mar 2026 - How to get the most from Fundmonitors | Webinar Recording 04 August 2025

|

How to get the most from Fundmonitors Webinar Recording FundMonitors.com 04 August 2025 |

|

To help you get a better understanding of the www.fundmonitors.com database, watch this webinar recording to help you learn to navigate the database and get the most out of its powerful fund analytics. The webinar covered the following:

If you like to see just 1 aspect of the webinar feel free to jump to the relevant timestamp: |

26 Feb 2026 - Manager Insights | East Coast Capital Management

|

Chris Gosselin, CEO of FundMonitors.com, speaks with Simone Haslinger, Chief Executive Officer at East Coast Capital Management. They discuss ECCM's systematic global trend-following strategy, recent strong performance driven by broad trends across commodities, currencies, and equity markets, and how disciplined risk management supports consistent results. The interview also highlights the importance of diversification and the role trend-following strategies can play in strengthening portfolios amid changing market conditions.

|

10 Feb 2026 - Magellan Global Equities Quarterly update January 2026

|

Magellan Global Equities Quarterly update January 2026 Magellan Investment Partners January 2026 (Viewing time: 14 mins) |

|

Against a backdrop of elevated market volatility, shifting monetary policy and divergent market dynamics, Portfolio Managers Alan Pullen and Casey McLean share their latest quarterly update on the Magellan Global Equities strategy. They discuss the impact of diverging interest-rate paths, the maturing AI trade and signs of a rotation in global equity markets. They also reflect on company earnings, broader market conditions and where they see opportunities. Looking ahead, Alan and Casey share their outlook and how the portfolio is positioned. |

|

Funds operated by this manager: Magellan Global Fund (Open Class Units) ASX:MGOC , Magellan Infrastructure Fund , Magellan Global Opportunities Fund No.2 , Magellan Infrastructure Fund (Unhedged) , Magellan Global Fund (Hedged) , Magellan Core Infrastructure Fund , Magellan Global Opportunities Fund Active ETF (ASX:OPPT) Important Information: This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 trading as Magellan Investment Partners ('Magellan Investment Partners') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision about whether to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to a Magellan Investment Partners financial product may be obtained by calling +61 2 9235 4888 or by visiting www.magellaninvestmentpartners.com Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of a Magellan Investment Partners financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. No guarantee is made that such information is accurate, complete or timely and no warranty is given regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Magellan Investment Partners or the third party responsible for making those statements (as relevant). Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. No representation or warranty is made with respect to the accuracy or completeness of any of the information contained in this material. Magellan Investment Partners will not be responsible or liable for any losses arising from your use or reliance upon any part of the information contained in this material. Any third-party trademarks contained herein are the property of their respective owners and Magellan Investment Partners claims no ownership in, nor any affiliation with, such trademarks. Any third-party trademarks contained herein are the property of their respective owners, are used for information purposes and only to identify the company names or brands of their respective owners, and no affiliation, sponsorship or endorsement should be inferred from such use. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Magellan Investment Partners. (080825-#W17) |

5 Feb 2026 - Expert Analysis of the RBA's February 03 Rate Decision

|

Expert Analysis of the RBA's February 03 Rate Decision FundMonitors.com February 2026 |

|

Chris Gosselin, CEO of FundMonitors.com, speaks with Nicholas Chaplin, Director and Portfolio Manager at Seed Funds Management, and Renny Ellis, Director & Head of Portfolio Management at Arculus Funds Management. The discussion examines the Reserve Bank of Australia's latest rate hike, with both guests arguing the RBA misjudged conditions by cutting rates last year and is now reacting too heavily to short-term data. They highlight the role of policy lags, the strengthening Australian dollar, and bond market signals, warning that further tightening risks overshooting and undermining economic stability. |

27 Jan 2026 - Magellan Infrastructure Quarterly Update January 2026

|

Magellan Infrastructure Quarterly Update January 2026 Magellan Investment Partners January 2026 (Viewing time: 15 mins) |

|

Following a strong year for listed infrastructure assets, Co-Heads of Infrastructure and Portfolio Managers Ofer Karliner and Ben McVicar provide an overview of performance drivers and the outlook for the sector. They reflect on companies that performed well during the final quarter of 2025, as well as areas that lagged. They also discuss the key risks and opportunities facing the infrastructure sector in 2026 and outline how the portfolio is positioned to manage these risks while remaining exposed to long-term structural growth themes across global infrastructure. |

|

Funds operated by this manager: Magellan Global Fund (Open Class Units) ASX:MGOC , Magellan Infrastructure Fund , Magellan Global Opportunities Fund No.2 , Magellan Infrastructure Fund (Unhedged) , Magellan Global Fund (Hedged) , Magellan Core Infrastructure Fund , Magellan Global Opportunities Fund Active ETF (ASX:OPPT) Important Information: This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 trading as Magellan Investment Partners ('Magellan Investment Partners') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision about whether to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to a Magellan Investment Partners financial product may be obtained by calling +61 2 9235 4888 or by visiting www.magellaninvestmentpartners.com Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of a Magellan Investment Partners financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. No guarantee is made that such information is accurate, complete or timely and no warranty is given regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Magellan Investment Partners or the third party responsible for making those statements (as relevant). Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. No representation or warranty is made with respect to the accuracy or completeness of any of the information contained in this material. Magellan Investment Partners will not be responsible or liable for any losses arising from your use or reliance upon any part of the information contained in this material. Any third-party trademarks contained herein are the property of their respective owners and Magellan Investment Partners claims no ownership in, nor any affiliation with, such trademarks. Any third-party trademarks contained herein are the property of their respective owners, are used for information purposes and only to identify the company names or brands of their respective owners, and no affiliation, sponsorship or endorsement should be inferred from such use. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Magellan Investment Partners. (080825-#W17) |

15 Dec 2025 - Expert Analysis of the RBA's December 9 Rate Decision

|

Expert Analysis of the RBA's December 9 Rate Decision FundMonitors.com December 2025 |

|

Chris Gosselin, CEO of FundMonitors.com, speaks with Nicholas Chaplin, Director and Portfolio Manager at Seed Funds Management, and Renny Ellis, Director & Head of Portfolio Management at Arculus Funds Management. In this discussion, they share their perspectives on the RBA's recent rate decisions, whether cuts came too early, and how inflation dynamics, subsidies, and employment data are shaping economic expectations. They also explore the likelihood of future rate movements and what investors should watch heading into 2026. |

24 Nov 2025 - Manager Insights | Magellan Investment Partners

|

Chris Gosselin speaks with Alan Pullen from Magellan Investment Partners about the philosophy behind the Magellan Global Opportunities Fund. Alan explains how the team focuses on high-quality global businesses, disciplined valuation, and long-term investing-especially important amid today's AI-driven market volatility.

Funds operated by this manager: Magellan Global Fund (Open Class Units) ASX:MGOC , Magellan Infrastructure Fund , Magellan Global Opportunities Fund No.2 , Magellan Infrastructure Fund (Unhedged) , Magellan Global Fund (Hedged) , Magellan Core Infrastructure Fund , Magellan Global Opportunities Fund Active ETF (ASX:OPPT) |

Online Applicatons

Free, simple and secure

Olivia123 - the fast simple and secure online alternative to completing paper based application forms.